Impact Modifier Market: By Type (Chlorinated Polyethylene (CPE), Methyl Methacrylate-Butadiene-Styrene Copolymer (MBS), Acrylonitrile-Butadiene-Benzene Copolymer (ABS), EVA, ACR, Random copolymer of acrylonitrile and butadiene (NBR), Others); Application (PVC, Nylon, PBT, Engineering Plastics, Others); End Users (Packaging, Construction, Consumer Goods, Automotive, Others); Region— Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 28-Oct-2025 | | Report ID: AA0124738

Market Snapshot

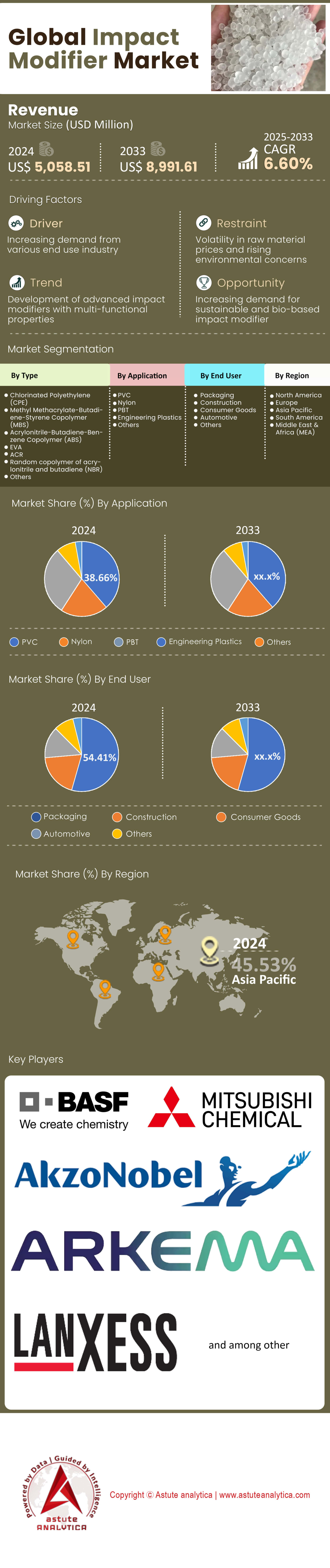

Impact modifier market was valued at US$ 5,058.51 million in 2024 and is projected to attain a market size of US$ 8,991.61 million by 2033 at a CAGR of 6.60% during the forecast period 2025–2033.

Key Insights

- Based on type, the acrylic (ACR) segment is a notable leader in the in the global impact modifier market by holding the highest market share of 28.68%.

- By application, the market is significantly led by Polyvinyl Chloride (PVC), with a dominant market percentage of 38.66%.

- Based on end user, the packaging segment emerges as a clear leader in the market as it commands a substantial market share of 54.41%.

- Asia Pacific is the dominant region in the market with over 47% market share.

- Global impact modifier market size is poised to reach US$ 8,991.61 million by 2033.

Escalating requirements from the global automotive sector are fundamentally shaping the Impact modifier market. The average passenger car in 2025 contains approximately 208 kilograms of plastic. European regulations are set to mandate that 52 kilograms of that plastic must come from recycled sources by 2030, a figure that will climb to 62.4 kilograms by 2035. This legislative push is driving the use of recycled plastics in vehicles to a forecast of 2,567 kilotons in 2025. Furthermore, the rapid adoption of electric vehicles, which surpassed 10 million in sales, is accelerating the need for lightweight yet durable components.

This automotive-led surge in the impact modifier market is complemented by massive demand from the construction industry. The rigid PVC market, a primary consumer of impact modifiers, is projected to be valued at US$ 48,687.84 million in 2025. The Asia-Pacific region alone will have a plastic additives market with a volume of US$ 35.04 billion in 2025, reflecting immense industrial activity. The underlying demand is so strong that the related Polyamide Impact Modifiers segment is expected to reach a volume of 104.98 kilotons in 2025.

Producers are responding directly to these powerful demand signals with significant capacity expansions. LG Energy Solution is investing over US$ 4.5 billion to add 70 GWh of battery manufacturing capacity in the U.S. impact modifier market by 2025. The company has already secured an order book worth 180 trillion won for EV batteries. Concurrently, LG Chem is increasing its cathode material production to 470,000 metric tons. These large-scale investments underscore the industry's confidence in sustained, long-term growth for the market.

To Get more Insights, Request A Free Sample

Unlocking New Frontiers for Growth in the Evolving Impact Modifier Market

- The push towards a circular economy is creating a substantial opportunity for specialized impact modifiers designed for recycled and bio-based polymers. As companies strive to meet sustainability goals, the demand for additives that can upgrade the performance of post-consumer recycled (PCR) materials is surging. For example, modifiers that improve the impact strength and processability of recycled PET and HDPE are becoming essential. Similarly, the bio-plastics market, particularly for Polylactic Acid (PLA), faces challenges with brittleness. Advanced impact modifiers that enhance the durability of PLA without compromising its compostability are opening new applications in packaging and consumer goods, creating a high-value niche in the Impact modifier market.

- Development of impact modifiers for high-performance engineering plastics used in extreme environments: Industries like aerospace, 5G telecommunications, and medical devices are increasingly using materials such as PEEK, PEI, and high-temperature polyamides. These polymers require specialized modifiers that can maintain impact resistance at elevated temperatures and withstand chemical exposure. The growing demand for lightweight components in electric vehicle battery housings and advanced electronics creates a compelling business case for developing these next-generation additives. Success in this area will allow producers to capture significant margins and establish strong positions in cutting-edge technology sectors.

Advanced Packaging Regulations and Circularity Goals Redefine Material Demand

The global packaging sector is undergoing a regulatory-driven transformation, creating specific and urgent demand within the Impact modifier market. In Europe, the Packaging and Packaging Waste Regulation (PPWR), which entered into force on February 11, 2025, sets aggressive targets that directly influence material science. The regulation mandates a 15% per capita reduction in packaging waste by 2040 compared to 2018 levels and requires all packaging to be recyclable by 2030. Furthermore, from January 2030, a range of single-use plastic packaging for items under 1.5kg will be banned entirely. These rules are compelling manufacturers to adopt materials that are not only durable but also compatible with a circular economy.

This shift creates a clear need for advanced impact modifiers that can enhance the integrity of thinner, lightweighted packaging and improve the performance of recycled resins. The PPWR also establishes specific minimum recycled content targets in the impact modifier market; for instance, by 2040, plastic packaging in the EU must contain between 50-65% recycled material. With global annual e-waste generation projected to reach 62 million tons in 2025, the pool of available recycled plastics is growing. However, these materials often have compromised mechanical properties. Impact modifiers are therefore essential to upgrade post-consumer resins, ensuring they meet the stringent performance requirements for bottles, containers, and other rigid formats, which constitute a market expected to grow from US$ 302.69 billion in 2025.

Connectivity and Electronics Boom Creates a High-Performance Materials Imperative

The relentless expansion of digital infrastructure and consumer electronics is creating a powerful new demand vector for the Impact modifier market. The global rollout of 5G is a primary catalyst, with the 5G base station market projected to grow from US$ 60.08 billion in 2025. This expansion requires tens of millions of new base station deployments, each housed in durable, weather-resistant plastic enclosures that rely on high-performance impact modifiers. Simultaneously, the data center construction market is set to expand from US$ 276.26 billion in 2025, driven by the growth of cloud computing and AI. These facilities utilize vast quantities of impact-modified plastics for server housings, cable trays, and cooling system components.

This infrastructure growth is mirrored in the consumer electronics sector, where the market for plastics is expected to reach US$ 16.53 billion in 2025. An average smartphone alone uses around 20 grams of plastic, and with billions of devices shipping annually, the volume is immense. The challenge in the impact modifier market is compounded by the staggering amount of electronic waste, forecast to hit 82 million tons by 2030. As regulations push for circularity, there is a growing need for impact modifiers that not only provide durability for new devices but also enhance the mechanical properties of recycled plastics recovered from this massive e-waste stream, which contains over 347 million metric tons of unrecycled material as of 2025.

Segmental Analysis

Acrylic Modifiers Forge Ahead with Superior Durability and Efficiency

The acrylic (ACR) segment's leadership in the global impact modifier market, holding the highest share of 28.68%, is rooted in its exceptional performance characteristics. ACR modifiers, built on a core-shell structure with a cross-linked acrylic core, significantly boost the durability of plastics. A key reason for their dominance is superior weatherability, making them the leading choice for weatherable building products for over 25 years. These advanced additives can increase a product's impact strength by more than six times and help it retain 90% of its toughness even at a frigid -40°C. The typical addition amount is small, ranging from just 0.5 to 5 parts per hundred resin (phr), delivering substantial improvements with minimal material. Their ability to prevent discoloration and chalking from long-term UV exposure makes them indispensable for outdoor applications.

The wide processing window of ACR modifiers is suitable for high-speed extrusion, enhancing manufacturing efficiency. The value they bring extends beyond toughness, as they are known to significantly improve the surface glossiness of final products. The market for these additives continues to expand as industries demand materials that offer longevity and resilience against environmental stress. The extensive use of these modifiers makes the impact modifier market a critical component of modern manufacturing.

- For applications requiring clarity, transparent ACR grades can maintain a light transmittance of over 85%.

- In synergistic blends with other modifiers like CPE, ACR can help lower the plate-out effect during processing.

- The unique chemistry of ACR has made it a leading modifier in building products for more than two decades.

PVC's Dominance Powered by Essential Impact Modification

Polyvinyl Chloride (PVC) leads the global impact modifier market by application, commanding a dominant 38.66% share because it is inherently brittle. Impact modifiers are essential to prevent brittle failure, especially in cold conditions. These additives form a flexible network within the rigid PVC matrix, with shear yielding acting as a key energy dissipation mechanism. The choice of modifier is tailored to the application; for example, chlorinated polyethylene (CPE) modifiers are selected for their excellent chemical and UV radiation resistance. For high-clarity products like films and medical devices, methacrylate-butadiene-styrene (MBS) modifiers are the ideal choice. Meanwhile, ACR remains the preferred modifier for durable outdoor profiles and siding.

The benefits extend beyond simple impact strength. Modifiers enhance the processability of PVC, making extrusion and molding more efficient for items like pipes and fittings that must withstand mechanical stress without cracking. This versatility has driven adoption in various sectors. For instance, modified PVC is now frequently used for automotive interior components. It is also highly compatible with foamed systems, allowing for a unique balance between rigidity and strength in products like decorative panels. The immense scale of PVC usage makes the impact modifier market foundational to global industrial output.

- Impact modifiers transform PVC from a fragile material into a durable and versatile engineering plastic.

- Different modifiers like CPE, MBS, and ACR are used to achieve specific properties for varied PVC applications.

- The automotive and construction industries are major consumers of impact-modified PVC products.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Packaging Sector's Leadership Driven by Need for Ultimate Product Protection

The packaging segment's clear leadership in the global impact modifier market, with a substantial 54.41% share, is propelled by the absolute necessity for durability. Packaging materials must withstand the rigors of handling and transportation to protect goods. For instance, Modified Atmosphere Packaging (MAP) can effectively double the shelf life of many food products. In red meat packaging, a gas mixture containing 70-80% oxygen is often used to maintain the appealing red color. Furthermore, a carbon dioxide concentration above 20% in MAP significantly reduces microbial growth, enhancing food safety. The technology is highly specialized; fish packaging may use CO2 levels around 50% to slow bacteria growth effectively.

The innovation in modifiers directly supports these advanced packaging formats. Specific Biostrength® modifiers are now designed for emerging biopolymers like PLA, improving their toughness for sustainable packaging solutions. MBS modifiers are crucial for creating clear PVC films that combine transparency with excellent drop-test integrity. A major advantage is that impact modifiers allow for downgauging, which is the process of creating thinner and lighter packaging films without sacrificing protective performance. Even minute additions, such as 0.4% carbon monoxide in meat packaging, can contribute to color stability. This deep integration into packaging science solidifies the critical role of the impact modifier market.

- Modified Atmosphere Packaging relies on specific gas mixtures to preserve food quality and extend shelf life.

- Impact modifiers enable the use of both traditional and sustainable polymers in high-performance packaging.

- The ability to create stronger, thinner films with impact modifiers reduces material usage and waste.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific Unrivaled Industrial Engine Powers Global Market Dominance

The Asia-Pacific region commands the Impact modifier market with an overwhelming 46% share, driven by its unparalleled manufacturing and construction scale. China's industrial might is a central factor, with the country aiming to produce over 95 million tons of key chemical materials in 2025. Its automotive sector alone is forecast to manufacture 31 million vehicles in 2024. This colossal output is supported by massive infrastructure projects, such as the planned investment of over US$ 140 billion in 102 major projects in Beijing for 2024. The demand for durable materials is immense, creating a vast appetite for performance-enhancing additives.

Furthermore, growth across the regional impact modifier market reinforces this dominance. India's automotive industry is projected to sell 4.8 million passenger vehicles in 2024. The nation is also expanding its polymer capacity, with Numaligarh Refinery Ltd. investing US$ 210 million in a new polypropylene unit. In South Korea, Samsung plans to invest US$ 230 billion through 2042 to create a massive semiconductor mega cluster, driving demand for high-purity plastics. Meanwhile, Japan's construction sector is expected to see 810,000 new housing starts in 2025, and Vietnam's government is targeting US$ 32 billion in foreign direct investment for 2024, much of it flowing into manufacturing.

North America Leverages Reshoring and Advanced Manufacturing Momentum

North America's Impact modifier market is defined by a resurgence in domestic manufacturing and massive investments in high-tech sectors. The US automotive industry expects to produce 15.8 million light vehicles in 2024. A significant driver is the electric vehicle boom, exemplified by Hyundai's new US$ 7.59 billion manufacturing plant in Georgia. This growth is supported by a robust construction sector, with total spending in the US projected to reach US$ 2.1 trillion in 2024.

Additionally, Mexico's role as a key manufacturing hub is expanding, with the country attracting US$ 36 billion in foreign direct investment in 2023, largely for nearshoring operations. In Canada, the construction industry is forecast to rebound with 232,000 housing starts in 2024. The region also benefits from abundant feedstock, with US natural gas production expected to reach 105 billion cubic feet per day in 2025. These converging factors create a stable and high-value demand base for the regional Impact modifier market.

Europe Navigates Regulatory Demands with a Focus on High-Value Applications

The European Impact modifier market is heavily influenced by stringent regulations and a strategic shift towards a circular economy. Germany remains the industrial core, with its automotive sector forecast to produce 4.1 million passenger cars in 2024. The region's chemical industry is undergoing significant investment, highlighted by INEOS's EUR 4 billion Project ONE ethylene cracker in Antwerp. This new capacity will supply essential building blocks for advanced polymer production.

Moreover, Europe's commitment to sustainability is creating new demand streams for the impact modifier market. The region aims to recycle 55% of its plastic packaging waste by 2030, a goal requiring advanced modifiers to upgrade post-consumer resins. The medical technology sector, which generated over EUR 160 billion in revenue in Germany in 2024, demands high-performance, medical-grade plastics. France is also supporting its chemical sector with a EUR 100 million investment fund. These factors ensure the European market remains a critical hub for innovation and specialized applications.

Strategic Investments and Acquisitions Reshape the Global Competitive Landscape of the Impact Modifier Market

- SK Capital Partners Acquires Valtris Specialty Chemicals: SK Capital, a private investment firm, completed its acquisition of Valtris Specialty Chemicals, a leading manufacturer of polymer additives, in January 2024.

- Celanese Acquires Next-Gen Materials Portfolio from DuPont: Celanese finalized its landmark US$ 11 billion acquisition of a majority of DuPont’s Mobility & Materials business, significantly expanding its engineered materials and additives portfolio in 2024.

- Avient Corporation Acquires DSM Protective Materials: Avient acquired the protective materials business from DSM for US$ 1.44 billion, enhancing its portfolio of high-performance engineered fibers and composite materials.

- LyondellBasell Breaks Ground on New US$ 200 Million Compounding Plant: In February 2024, LyondellBasell started construction on a new state-of-the-art plastics compounding facility in Germany to support the automotive sector.

- Adnoc and OCI Close Merger to Create Fertiglobe

While focused on fertilizers, the US$ 8.5 billion merger of Adnoc’s and OCI’s assets creates a chemical giant with significant influence on feedstock markets relevant to polymers. - Chase Corporation Acquires NuCera Solutions from SK Capital

In a US$ 250 million deal, Chase Corp. acquired NuCera, a producer of specialty polymers and waxes used in a variety of industrial applications. - SABIC and Sinopec Deepen Partnership with New Polycarbonate Plant

SABIC and Sinopec announced a new phase for their joint venture, including a new polycarbonate plant with an annual capacity of 260,000 tons, which started operations in 2024. - Röhm Invests in Expanding Global PMMA Production Capacity

Röhm announced an investment of over EUR 400 million by 2028 to expand its capacity for PMMA, a key plastic often used with impact modifiers.

Top Players in the Global Impact Modifier Market

- Akdeniz Chemson

- Akzo Nobel N.V

- Arkema S.A.

- BASF SE

- Clariant AG

- DuPont de Nemours, Inc

- Dow Chemical Company

- Evonik Industries AG

- Indofil Industries Limited

- Kaneka Corporation

- Lanxess AG

- Mitsubishi Chemical Group Corporation

- Shandong Novista Chemicals Co. Ltd

- SI Group, Inc

- Sundow Polymers Co. Ltd

- Other Prominent players

Market Segmentation Overview:

By Type

- Chlorinated Polyethylene (CPE)

- Methyl Methacrylate-Butadiene-Styrene Copolymer (MBS)

- Acrylonitrile-Butadiene-Benzene Copolymer (ABS)

- EVA

- ACR

- Random copolymer of acrylonitrile and butadiene (NBR)

- Others

By Application

- PVC

- Nylon

- PBT

- Engineering Plastics

- Others

By End-User

- Packaging

- Construction

- Consumer Goods

- Automotive

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 5,058.51 Million |

| Expected Revenue in 2033 | US$ 8,991.61 Million |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Mn) |

| CAGR | 6.60% |

| Segments covered | By Type, By Application, By End-User, By Region |

| Key Companies | Akdeniz Chemson, Akzo Nobel N.V, Arkema S.A., BASF SE, Clariant AG, DuPont de Nemours, Inc, Dow Chemical Company, Evonik Industries AG, Indofil Industries Limited, Kaneka Corporation, Lanxess AG, Mitsubishi Chemical Group Corporation, Shandong Novista Chemicals Co. Ltd, SI Group, Inc, Sundow Polymers Co. Ltd, Other Prominent players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |