Recycled Plastic Market: By Source (Plastic Bottles, Plastic Films, Synthetic Fibers, Rigid Plastics & Foams, Others); Type (Polyethylene Terephthalate (PET), Polyethylene (PE) - LPDE & HDPE, Polypropylene (PP), Polyvinyl Chloride (PVC), Polystyrene (PS), Polyamide (PA), Others); Recycling Method (Thermal decomposition, Heat compression, Distributed Recycling, Pyrolysis, Others); End-User (Packaging, Building & Construction, Textiles, Automotive, Electrical & Electronics, Others); Region— Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 28-Oct-2025 | | Report ID: AA0423411

Market Snapshot

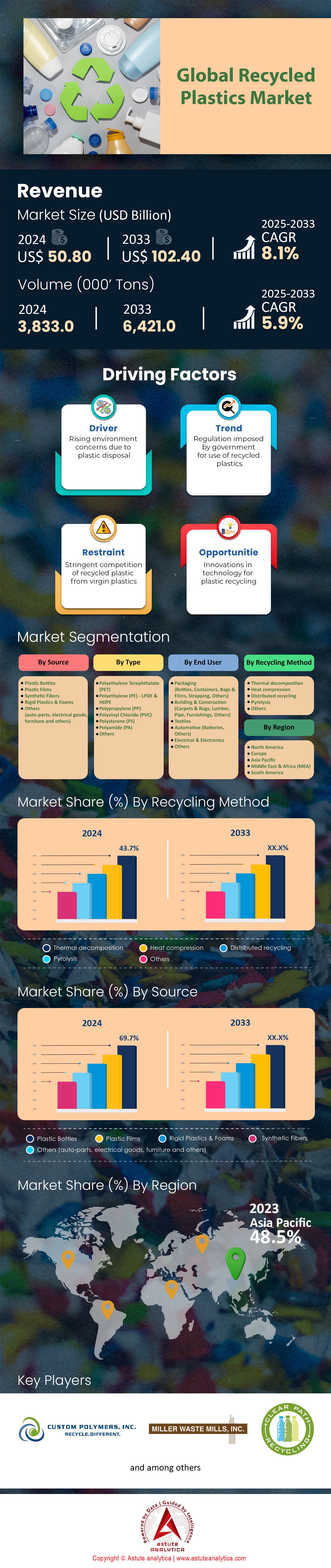

Recycled plastics market size projected to increase from US$ 50.80 billion in 2024 to US$ 102.40 billion by 2033, growing at a CAGR of 8.1% during the forecast period 2025-2033.

Key Findings Shaping the Market

- Based on sources, plastic bottles hold a 69.7% share in the market.

- Based on type, Polyethylene Terephthalate (PET) reigns supreme in the recycled plastics market by controlling over 54.9% market share.

- Based on end users, packaging industry remains the largest end users of market with over 53.9% market share.

- Asia Pacific is the dominant in global market with over 48.50% market share.

- Recycled plastics market size projected to increase from US$ 50.80 billion in 2024 to US$ 102.40 billion by 2033.

Tangible demand in the recycled plastics market is accelerating, driven by legally binding regulations and large-scale corporate procurement. EU producers will need to source approximately 5.4 million tons of rPE, rPP, and rPET annually by 2030 to meet the Packaging and Packaging Waste Regulation mandates. This figure is forecast to climb to 11.5 million tons per year by 2040 as rules expand. In the U.S., state-level actions, such as California's mandate for 50% recycled content in beverage containers by 2030, create significant regional demand pulls.

Major brand owners are translating sustainability goals into substantial, fixed demand. The Coca-Cola Company utilized 488,000 metric tons of rPET in 2023. Unilever’s annual consumption has surpassed 164,000 tons. These volumes provide the long-term offtake certainty required for recyclers to invest in new capacity. Further solidifying this demand, new investments are adding significant capacity. For example, ExxonMobil's planned expansions in Texas will add 350 million pounds of annual advanced recycling capacity by 2026. Waste Management is also adding three new facilities in 2024 to increase its capacity by 1 million metric tons by 2026.

These concrete numbers signal a structural shift. The demand is no longer speculative but is embedded in legal frameworks and corporate supply chains. Stakeholders in the recycled plastics market are responding to a clear, quantified need for materials, driven by some of the world's largest economies and corporations. This creates a stable foundation for future growth and investment across the value chain.

Production in recycled plastics market has expanded significantly, with global recycling capacity growing by 30% since 2022 to reach 350 million metric tons annually in 2024. This capacity growth is particularly notable in Asia, where it has doubled in the past two years. Advancements in sorting technologies, such as AI-driven systems, have reduced contamination rates in sorted plastic waste to 2%, down from 5% in 2022, leading to higher-quality recycled materials suitable for diverse applications. Chemical recycling has also made strides, with 50 commercial-scale plants now operational globally, up from 15 in 2022, collectively processing 3 million metric tons of plastic waste annually. Energy efficiency has improved as well, with mechanical recycling processes now requiring 60% less energy compared to producing virgin plastics, reducing the carbon footprint of recycled materials. The industry avoided 500 million metric tons of CO2 emissions and saved 250 billion liters of water in 2024, representing a 40% and 30% improvement, respectively, compared to 2022.

Governments worldwide have implemented robust initiatives to bolster the recycled plastics industry. Extended Producer Responsibility (EPR) programs now cover 75% of OECD countries, up from 60% in 2022, resulting in a 40% increase in plastic waste collection rates. The European Union has introduced an €800-per-ton tax on non-recycled plastic packaging, boosting demand for recycled plastics market by 25%, while the U.S. introduced a $0.20-per-pound tax credit for recycled plastics, driving a 35% increase in consumption by manufacturers. Investments in recycling infrastructure have surged, with China investing $15 billion since 2022, doubling its recycling capacity, and the EU allocating €10 billion to boost recycling rates by 30%. Globally, $25 billion has been invested in recycling technologies in 2024, a 50% increase since 2022, creating 5 million jobs and lifting the industry to new heights. These efforts underline the transformative progress in plastic recycling, driven by a confluence of consumer demand, corporate action, and government support, ensuring the industry’s continued growth and environmental impact.

To Get more Insights, Request A Free Sample

Emerging Frontiers Will Redefine the Recycled plastics market Landscape

The market is entering a new phase of innovation, with significant opportunities emerging in previously challenging sectors. These trends are poised to create new high-value applications and further embed recycled materials into the industrial economy.

- Textile-to-Textile Recycling Gains Commercial Momentum: Advanced sorting and chemical recycling technologies are beginning to unlock the vast potential of post-consumer textiles as a feedstock. Innovations in dissolution and enzymatic processes are enabling the separation of blended fibers like poly-cotton, turning old clothing into high-quality recycled polyester (rPET) and cellulosic fibers. Companies are moving beyond pilot projects to establish commercial-scale facilities capable of processing thousands of tons of textile waste annually. This creates a circular loop for fashion and reduces the industry's heavy reliance on virgin polyester, which is derived from fossil fuels.

- Recycled Plastics Become a Staple in Sustainable Construction: The construction industry is increasingly adopting recycled plastics to create durable, lightweight, and cost-effective building materials. Companies are producing building blocks made entirely from compressed, non-recyclable plastic waste. In infrastructure, recycled plastics are being incorporated into asphalt mixes to build longer-lasting, crack-resistant roads. Furthermore, recycled polymers are being used to manufacture plastic lumber for decking, fencing, railway sleepers, and sound barriers, offering a rot-resistant and low-maintenance alternative to traditional wood and concrete.

Food-Grade Approval Surge Creates High-Value Recycled plastics market Demand

A critical factor defining demand is the rapid expansion of regulatory approvals for food-contact recycled plastics. The U.S. Food and Drug Administration (FDA) issued Letters of No Objection (LNOs) to two dozen companies in the second half of 2024 alone, clearing their materials for use in food and drink packaging. These approvals are no longer limited to just PET; in 2024, the FDA cleared recycled HDPE, LDPE, LLDPE, and PP from producers like Circulus Holdings, NOVA Chemicals, and Blue Polymers. The momentum has continued into 2025, with PureCycle Technologies receiving an LNO for its recycled polypropylene covering all food types.

This regulatory green light is enabling major capacity investments targeted specifically at the high-value food-grade segment. For instance, NOVA Chemicals' new Indiana facility is projected to produce over 100 million pounds of FDA-compliant recycled LLDPE annually. The European Food Safety Authority (EFSA) is also advancing the market by authorizing new recycling processes and revising evaluation criteria to streamline approvals. These actions provide the assurance that brand owners in the food and beverage sector need to meet their recycled content goals, creating a powerful and non-negotiable demand stream for high-purity materials in the recycled plastics market.

Electronics and Consumer Goods Industries Drive Circular Material Demand

Beyond packaging, the demand for recycled content in consumer electronics and durable goods is becoming a significant force in the recycled plastics market. Major tech companies are now integrating substantial volumes of recycled materials into their products. For example, HP Inc. has already used more than a cumulative one billion pounds of recycled plastic in its printers and computers. Dell is aiming to make more than half of its product content from recycled or renewable material by 2030. These commitments require sourcing hundreds of thousands of tons of high-quality recycled polycarbonate, ABS, and other engineering plastics.

This demand is fueling investment in specialized e-waste recycling infrastructure. Aurubis recently opened its first U.S. recycling plant in Georgia, a $800 million facility designed to process over 180,000 tons of complex materials like recycled electronics annually. As companies increasingly design products for circularity, the demand for recycled plastics in long-lasting goods will grow. This trend diversifies the recycled plastics market away from its traditional reliance on single-use packaging and creates stable, high-value end markets for materials recovered from a wide range of post-consumer products.

Segmental Analysis

Recycled Plastic Bottles Shape Market Dominance: Why 69.7% Share?

Plastic bottles hold a commanding 69.7% share in the recycled plastics market, a testament to their established collection infrastructure and economic viability. The ease of sorting and processing widely used beverage and household bottles makes them a prime candidate for recycling. Municipal recycling programs frequently prioritize bottle collection due to their high volume and relatively clean stream, distinguishing them from other plastic waste. Many consumer goods companies are increasingly committed to incorporating recycled content into new bottles, creating consistent demand. This preference also stems from the relatively uniform polymer type often found in bottles, simplifying the recycling process and yielding a more predictable output. The extensive history of bottle recycling has fostered robust material recovery facilities equipped for high throughput, contributing significantly to the consistent availability of recycled bottle materials. Furthermore, brand initiatives to meet sustainability pledges often target bottle-to-bottle recycling, reinforcing market demand and further solidifying their impressive share within the Recycled plastics market.

- Advanced optical sorters are boosting bottle recovery rates.

- Deposit return schemes are enhancing bottle collection efficiency.

- Innovations in washing and flaking technologies improve recycled bottle quality.

PET Leads Recycled plastics market with a 54.9% Share: Understanding Supremacy

Polyethylene Terephthalate (PET) reigns supreme in the recycled plastics market, controlling over 54.9% of the share due to its excellent properties and widespread application. PET’s clarity, strength, and barrier properties make it ideal for food and beverage packaging, which represents a massive volume of plastic consumption. The material’s ability to be recycled multiple times without significant degradation maintains its value and appeal to converters. There is strong industry preference for rPET (recycled PET) in new product manufacturing, driven by corporate sustainability goals and consumer demand for eco-friendly products. Global efforts to reduce virgin plastic consumption often focus heavily on PET, given its ubiquitous presence in everyday items. The established end-markets for rPET, ranging from new bottles to fibers and strapping, ensure a stable demand for the recycled material. Moreover, technological advancements in PET depolymerization are opening new avenues for high-quality recycled material production, further cementing its leading position in the Recycled plastics market.

- Growing demand for rPET in textile industries is notable.

- Chemical recycling innovations for PET are advancing rapidly.

- Government mandates for recycled content in PET products are increasing.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Packaging Industry Dominates Recycled Plastic End-Use with 53.9% Market Share

The packaging industry remains the largest end-user of the recycled plastics market, accounting for over 53.9% of the market share, driven by increasing consumer and regulatory pressure for sustainable packaging solutions. Brands are actively seeking recycled content to enhance their environmental profiles and meet ambitious sustainability targets. Recycled plastics offer a viable alternative to virgin materials, helping companies reduce their carbon footprint and depend less on fossil resources. The versatility of recycled polymers allows their integration into various packaging formats, from rigid containers to flexible films. Investment in packaging design for recyclability is becoming a standard practice, facilitating a circular economy for packaging materials. Furthermore, cost efficiencies can sometimes be realized by utilizing recycled plastics, especially as virgin plastic prices fluctuate. The continuous innovation in processing technologies allows recycled plastics to meet the stringent quality and safety standards required for packaging applications, solidifying the sector's crucial role in the Recycled plastics market.

- E-commerce growth is accelerating demand for recycled packaging.

- Lightweighting trends in packaging are utilizing advanced recycled polymers.

- Increased adoption of closed-loop packaging systems is observed.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific’s Dominance in Recycled plastics market: 48.50% Market Share Explored

Asia Pacific leads the recycled plastics market with an impressive 48.50% market share, driven by robust industrial activity and burgeoning populations. China, for instance, has invested significantly in plastic waste processing capabilities, boasting thousands of recycling facilities. India’s informal collection networks gather millions of tons of plastic annually, feeding a vast domestic recycling industry. South Korea actively promotes bottle-to-bottle recycling, achieving high recovery rates for PET containers. Japan utilizes advanced material recovery technologies, extracting maximum value from mixed plastic streams. The region sees considerable private sector investment in novel recycling technologies, fostering innovation and efficiency. Government initiatives across Southeast Asia support the establishment of new recycling plants, augmenting processing capacity. Export volumes of recycled plastic flakes from several Asian nations remain substantial, indicating strong internal processing. Major brand owners in the region are committing to ambitious recycled content targets for their products. The presence of numerous small and medium-sized enterprises specializing in plastic reprocessing contributes significantly to the overall volume. Furthermore, circular economy policies adopted by countries like Singapore are creating a favorable environment for recycled plastics market expansion.

- Vietnam’s projected increase in plastic recycling capacity by 500,000 tons by 2025.

- Indonesia targets 70% plastic waste reduction by 2025 through recycling efforts.

- Thailand’s plastic waste generation of 2.5 million tons saw a 60% recycling rate in 2024.

North America’s Evolving Recycled plastics market: Strategic Growth Initiatives

North America exhibits a dynamic recycled plastics market, propelled by increasing corporate sustainability goals and technological advancements. The United States has seen hundreds of millions of dollars invested in upgrading recycling infrastructure, particularly for advanced sorting. Canada’s commitment to extended producer responsibility programs is stimulating higher collection volumes. Many American states are implementing policies that favor recycled content in packaging, driving demand. Companies in the region are forming partnerships to create closed-loop systems for specific plastic types. Investment in chemical recycling facilities across the continent is projected to reach several billion dollars by 2025. Demand for recycled plastic in non-packaging applications like automotive and construction is steadily growing. Innovation in plastic design for enhanced recyclability is a key focus for manufacturers. Collection rates for HDPE plastics are showing consistent upward trends. Collaborative efforts between industry and government bodies are aimed at harmonizing recycling standards.

Europe’s Pioneering Recycled plastics market: Circular Economy Mandates

Europe maintains a strong position in the recycled plastics market, characterized by stringent regulations and a mature circular economy framework. Germany boasts some of the highest plastic packaging recycling rates globally, exceeding 60%. The European Union’s Plastic Strategy is driving substantial investment in recycling capacity across member states. France has introduced penalties for packaging that is not easily recyclable, spurring innovation. The UK is developing robust collection systems for flexible plastics, addressing a historically challenging waste stream. Scandinavian countries are excelling in chemical recycling pilot projects, exploring new avenues for plastic waste. Demand for recycled content in construction and agricultural films is steadily increasing across the continent. Collaborations among different industries are fostering novel applications for recycled polymers. Investment in research and development for bio-based and recyclable plastics is a priority. Several European nations are implementing deposit return schemes, significantly boosting collection of beverage containers.

Top 10 Developments in Recycled plastics market

- PureCycle Technologies Funding: PureCycle Technologies secured substantial funding in early 2024 to expand its advanced polypropylene recycling facilities.

- Origin Materials Investment: Origin Materials received significant investment in 2024 for its bio-based materials platform, including recyclable plastics.

- Loop Industries Partnership: Loop Industries announced a major partnership in 2024 for the construction of a new PET recycling facility.

- Agilyx Strategic Investment: Agilyx secured a strategic investment in late 2024 to accelerate the deployment of its chemical recycling technology.

- Plastic Energy Funding Round: Plastic Energy completed a funding round in 2025 to scale up its advanced recycling operations in Europe.

- Brightmark Energy Expansion: Brightmark Energy received significant project financing in 2024 for its plastic renewal facility expansion.

- Valtris Specialty Chemicals Acquisition: Valtris Specialty Chemicals acquired a company focused on sustainable plastic additives in early 2024.

- Ineos Styrolution Partnership: Ineos Styrolution announced a new investment partnership in 2024 for a polystyrene recycling plant.

- Recycling Technologies Funding Boost: Recycling Technologies received a substantial funding boost in 2025 to develop new recycling solutions.

- Encina Development Investment: Encina Development Group secured significant investment in 2024 for its advanced circular economy facilities.

Key Recycled Plastic Market Companies:

- B&B Plastics

- B. Schoenberg & Co.

- Clear Path Recycling

- Custom Polymers, Inc.

- Envision Plastics

- Green Line Polymers

- Green-O-Tech India

- Jayplas

- Kuusakoski Group Oy

- KW Plastics, Inc.

- MBA Polymers Inc.

- Miller Waste Mills

- Recycled Plastic Inc.

- Plastipak Holdings

- Recyclex S.A.

- Seraphim Plastics

- UltrePET, LLC

- Veolia

- Other Prominent Players

Market Segmentation Overview

By Source

- Plastic Bottles

- Plastic Films

- Synthetic Fibers

- Rigid Plastics & Foams

- Others (auto-parts, electrical goods, furniture and others)

By Type

- Polyethylene Terephthalate (PET)

- Polyethylene (PE) - LPDE & HDPE

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Polyamide (PA)

- Others

By Recycling Method

- Thermal decomposition

- Heat compression

- Distributed recycling

- Pyrolysis

- Others

By End-User

- Packaging (Bottles, Containers, Bags & Films, Strapping, Others)

- Building & Construction (Carpets & Rugs, Lumber, Pipe, Furnishings, Others)

- Textiles

- Automotive (Batteries, Others)

- Electrical & Electronics

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- ASEAN

- Malaysia

- Philippines

- Singapore

- Thailand

- Indonesia

- Vietnam

- Cambodia

- Rest of ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |