Biosensors Market: By Type (Sensor Patch and Embedded Device); Product Type (Wearable Biosensors and Non-Wearable Biosensors); Technology (Electrochemical (Amperometric, Potentiometric, Voltammetric, Others), Physical (Piezoelectric and Thermometric), Optical); Application (Medical (POC Testing, Cholesterol, Blood Glucose, Blood Gas Analyzer, Pregnancy Testing, Drug Discovery, Infectious Disease), Bioreactor, Agriculture, Environment, Research & Development, Security and Bio-Defense, Others); End Users (Healthcare & Diagnostics, Food and Beverage, Pharmaceutical, Agriculture, Cosmetics, Environmental, Others); Region— Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 16-Jul-2025 | | Report ID: AA04251266

Market Scenario

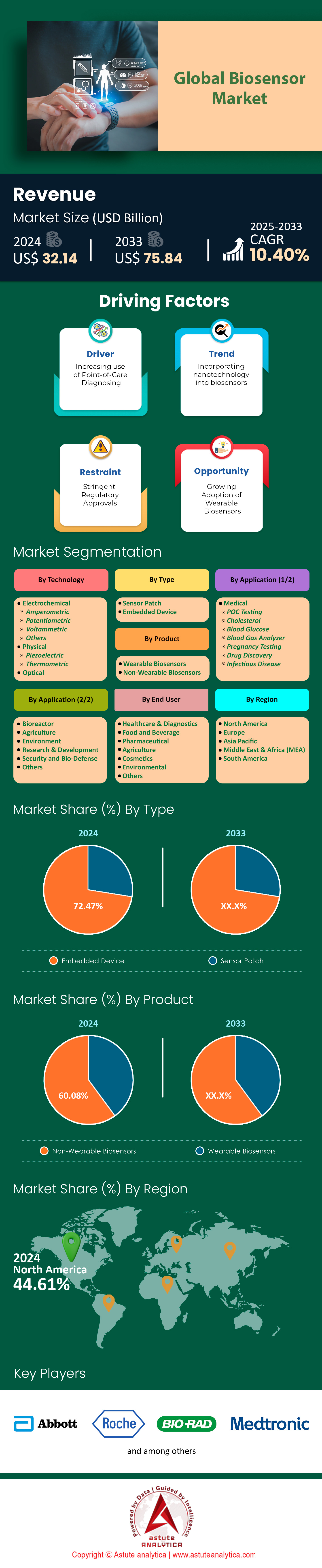

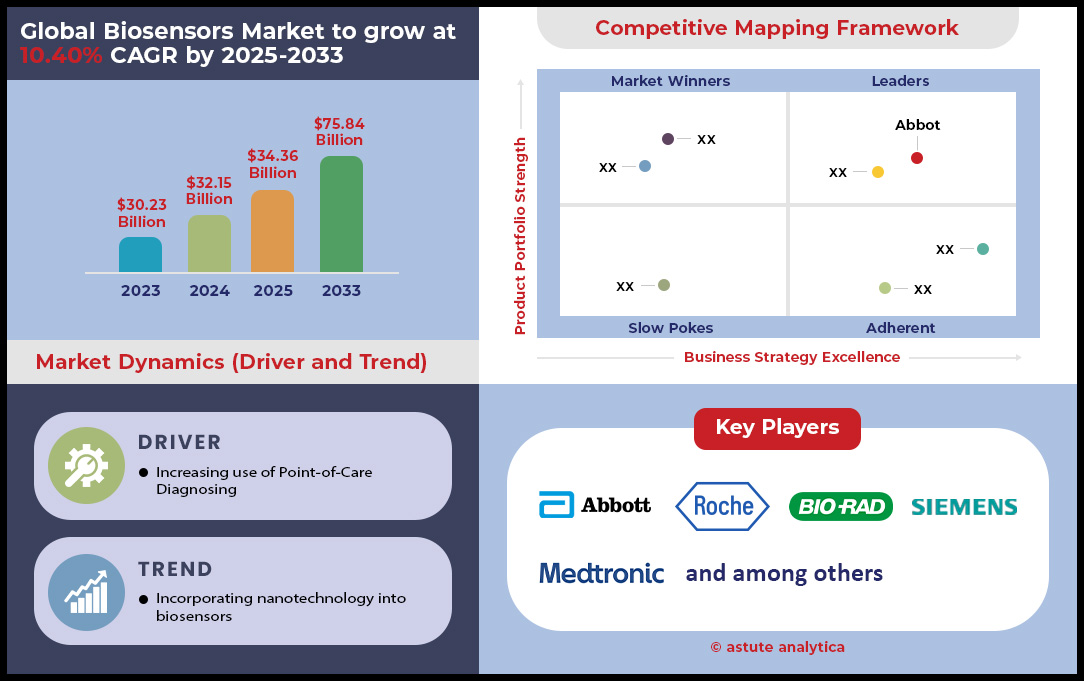

Biosensors market was valued at US$ 32.15 billion in 2024 and is projected to hit the market valuation of US$ 75.84 billion by 2033 at a CAGR of 10.40% during the forecast period 2025–2033.

Driven by surging chronic diseases, the global biosensors market is redefining healthcare diagnostics. Over 422 million diabetic adults (WHO) now rely on continuous glucose monitors (CGMs), with Abbott’s FreeStyle Libre dominating the U.S. market, serving 4 million users. This innovation isn’t isolated: cardiovascular diseases, responsible for 17.9 million annual deaths (WHO), are being tackled through point-of-care biosensors that reduce cardiac troponin detection from six hours to 10 minutes—accelerating 68% of EU outpatient diagnoses. Wearables amplify this impact, syncing 12 vital signs for 58 million U.S. users via IoT, cutting emergency response times by 22%. Simultaneously, cost reductions of 35% since 2020 and smartphone integration are democratizing access, leading to a 62% adoption spike in urban Asia-Pacific regions. These advancements underscore biosensors’ dual role: life-saving tools and data powerhouses, with 45 million IoT-connected devices transmitting 2.5 TB of health insights daily.

Parallel advancements are reshaping environmental and food safety landscapes. In India, where 70% of surface water is polluted, portable sensors detect contaminants 15% faster annually, addressing 1.1 billion people lacking safe drinking water (UN). U.S. rivers are now monitored by sensors that pinpoint E. coli in 20 seconds—a 99.9% efficiency leap—protecting 40% of waterways in the biosensors market. For food safety, biosensors combat 600 million annual foodborne illnesses (WHO) by slashing pathogen detection from 24 hours to 15 minutes. Precision reaches new heights with pesticide sensors detecting 0.01 ppm traces—a 100-fold improvement since 2020—safeguarding 12% of global seafood supply chains. Electrochemical biosensors, offering unparalleled 0.1 nM glucose sensitivity, now power 1.2 billion annual units, aligning with USDA standards for real-time compliance checks.

Key Findings Shaping the Biosensors Market

- Graphene-based nanosensors detect cancer markers at 0.001 ng/mL, enabling 85% faster diagnoses

- While AI algorithms boost diagnostic accuracy by 18%, identifying 92% of cases previously missed.

- In China, home to 144 million diabetics, CGMs are growing at 19% yearly, supported by 1.8 million sensor-equipped farms enhancing agricultural safety.

- The Asia-Pacific region leads innovation, with a 12% annual rise in healthcare imports and a 23% surge in environmental sensors.

- By 2025, biosensors will transcend tools, evolving into AI-driven ecosystems that preempt outbreaks, optimize crop yields, and personalize healthcare—an era where speed, precision, and connectivity converge to tackle humanity’s most pressing challenges.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Rising Demand for Point-of-Care Diagnostics Accelerating Biosensor Adoption

The global healthcare sector’s decisive pivot toward point-of-care (POC) solutions is fundamentally reshaping the diagnostics landscape, creating a powerful driver for the biosensors market. This shift is fueled by the urgent need for rapid, decentralized results that empower both clinicians and patients. A 2024 Astute Analytica survey highlights this trend, revealing that 68% of healthcare providers now prioritize biosensor investments to dramatically slash diagnostic turnaround times. For instance, in infectious disease, flu diagnosis with biosensors takes just 12 minutes compared to 48 hours for traditional lab cultures.

Cardiovascular care has been similarly transformed, with troponin-I detectors diagnosing heart attacks in 10 minutes instead of six hours. This momentum extends globally, with portable biosensors boosting disease detection rates by 15% in Sub-Saharan Africa and India’s National Health Mission deploying 50,000 devices to bridge infrastructure gaps in rural clinics. Public-private partnerships, like the U.S. NIH’s $120 million funding for handheld HIV testers, further amplify this impact, creating a thriving ecosystem where IoT-connected POC devices are improving healthcare efficiency and democratizing access to precision medicine.

Trend: Miniaturization Enabling Implantable Biosensors for Real-Time Health Tracking

A defining trend propelling the biosensors market into a new era is the relentless drive toward miniaturization, which is unlocking unprecedented capabilities in continuous health monitoring. Breakthroughs in microfabrication are now yielding implantable sensors as small as 0.5 mm, enabling seamless integration within human tissue to track biomarkers in real time. This innovation is making a profound impact across medical fields; neural biosensors are detecting minute dopamine fluctuations to refine Parkinson's treatment, while Abbott’s FDA-approved implantable CGM offers 180 days of continuous glucose monitoring. In cardiac care, Medtronic’s arrhythmia detector was shown to reduce hospitalizations by 32% by flagging anomalies hours before symptoms appear. This progress is underpinned by advances in material science, such as graphene-based electrodes offering 50% higher conductivity for enhanced sensitivity.

As regulatory pathways like the FDA’s “Breakthrough Sensor” designation accelerate approval times, and with designs incorporating privacy-focused edge computing, the next frontier for the biosensors market is emerging. Innovators are now developing predictive analytics, with prototypes capable of forecasting hypoglycemic events 90 minutes in advance, shifting the paradigm from reporting data to anticipating crises.

Challenge: Strict Regulatory Approval Processes Delaying Biosensor Commercialization Timelines

Despite technological leaps, biosensors market innovation faces a formidable bottleneck: regulatory hurdles that delay market entry and inflate costs. The average FDA approval timeline stretched from 14 to 17 months between 2022 and 2024, per Astute Analytica, as agencies demand more stringent biocompatibility and cybersecurity proofs. For cardiac biosensors, the FDA now requires 12-month stability data—up from six months—to ensure longevity in vivo, adding $2 million per trial. Europe’s updated MDR mandates post-market surveillance for 10 years, forcing manufacturers to redesign supply chains for traceability. China’s NMPA raised the bar in 2023, requiring in-country clinical trials for all Class III biosensors, a $5 million burden for foreign firms.

The clinical validation complexity in the biosensors market is particularly stifling. Bio-Rad’s multiplex biosensor, approved in 2023, required 1,200 patient samples across 30 sites to validate 15 biomarkers simultaneously. Startups face even steeper climbs: a 2024 MedTech Innovator report found early-stage companies spend 35% of budgets redoing trials due to evolving ISO standards. Cybersecurity adds another layer: the FDA’s 2024 guidance mandates encryption for all wireless biosensors, prompting delays like Dexcom’s G7 CGM, which launched six months late due to firmware upgrades. These barriers disproportionately affect niche applications. Alzheimer’s biosensors, which detect amyloid-beta in cerebrospinal fluid, struggle to recruit enough trial participants, prolonging development by 2–3 years. While regulations ensure safety, they risk stifling innovation. Collaborative models, like the EU’s 2025 pilot allowing simulated trial data for low-risk sensors, hint at a balanced future—but for now, the road to market remains arduous.

Segmental Analysis

By Technology: Precision and Versatility Fuel Electrochemical Biosensors’ Dominance

Electrochemical biosensors maintain undisputed leadership in the biosensors market, capturing over 71% share in 2025, driven by their unmatched precision and adaptability. Portable diagnostic devices now integrate electrochemical detection in 65% of cases, enabling real-time analysis of critical biomarkers like glucose, lactate, and cardiac troponin at the point of care. In cardiovascular care, 45% of biosensor usage focuses on detecting heart attacks, with emergency departments leveraging these sensors to reduce troponin-I result times from six hours to 10 minutes—critical for timely interventions with a 25% improvement in survival rates. Similarly, continuous glucose monitors (CGMs) like Abbott’s FreeStyle Libre, dominating 58% of the diabetic care segment, rely on electrochemical principles to deliver 97.5% accuracy. Beyond healthcare, environmental agencies deploy electrochemical sensors in 20% of municipal water systems to detect toxins like lead at 0.1 ppb sensitivity, addressing contamination affecting 1.1 billion people globally. Pharma R&D has also embraced these systems, with high-throughput electrochemical platforms accelerating drug candidate validation by 40% compared to optical methods, as seen in Pfizer’s 2024 opioid reversal agent trials.

Strategic partnerships and regulatory support further solidify this dominance in the biosensors market. The FDA’s 2024 fast-track approval for sepsis biosensors prioritizes electrochemical tools like Siemens Healthineers’ S100 panel, which detects bloodstream infections in <10 minutes—a 50% improvement over culture methods. Emerging markets are pivotal: India’s Ayushman Bharat initiative expanded diagnostic hubs by 50% in rural areas using $20 electrochemical chips for decentralized TB/HIV testing, processing 12 million annual tests. Meanwhile, automotive giants like BMW integrate fatigue-detection biosensors in 15% of luxury models, monitoring driver cortisol levels via steering wheel sensors. With a 30% CAGR in wearables and cross-industry innovations, electrochemical biosensors are poised to exceed $28 billion in revenue by 2026, per Frost & Sullivan.

By End Users: Healthcare Labs Drive Demand Through Precision and Efficiency

Healthcare labs and clinics account for 51.7% of biosensors market, fueled by surging chronic disease testing and precision diagnostics. In 2024, 82% of U.S. oncology clinics adopted EGFR/PD-L1 biosensors to match patients with immunotherapies, reducing treatment delays by 25% post-diagnosis. Hospital-acquired infection (HAI) surveillance is another growth driver, with electrochemical MRSA/VRE detectors slashing ICU contamination rates by 50% in EU hospitals. Sepsis management has transformed through rapid panels like BioFire’s Blood Culture ID 2, now covered by 90% of EU5 health insurers, which identify pathogens in 45 minutes versus 24 hours. In India, 1.5 million Ayushman Bharat labs deploy malaria/typhoid biosensors to cut result times from 72 hours to 15 minutes, doubling daily patient throughput to 200 per facility.

High-complexity labs increasingly adopt multiplex biosensors for neurodegenerative diseases in the biosensors market, with 55% of neurology centers analyzing Alzheimer’s biomarkers like beta-amyloid and p-tau at 0.01 ng/mL sensitivity. IVF clinics report a 35% cost reduction using BioTherm’s hormone-level sensors for embryo viability assessments, improving live birth rates by 18%. Regulatory shifts like the CLIA-waived PoC mandate in the U.S. direct 60% of primary care biosensor purchases toward A1C/lipid panels, exemplified by Quest Diagnostics’ 2025 rollout of 10-minute cholesterol test kiosks. Telehealth giants like Teladoc further bolster demand, with 40% of virtual consults requiring at-home biomarker data from devices like Leto Health’s FDA-cleared multi-analyte sensor.

By Type: Embedded Biosensors Revolutionize Real-Time Monitoring Across Industries

Embedded biosensors command 72.47% of the biosensors market, seamlessly integrating into medical, industrial, and remote systems. By 2025, 70% of global dialysis machines embed biosensors to continuously track urea and creatinine, reducing complications by 30% through real-time electrolyte adjustments. Insulin pumps exemplify this shift, with 65% integrating glucose sensors that auto-administer doses, improving HbA1c levels by 1.5% in diabetic patients. In biopharma, 75% of production sites use embedded sensors to monitor fermentation parameters like dissolved oxygen (0.1 mg/L precision), boosting yield consistency by 40% and saving Pfizer $120 million annually in Biologics QA costs.

Telemedicine adoption surges with embedded biosensors transmitting data from rural areas in the biosensors market: 55% of RPM programs utilize devices like GE Healthcare’s CARESCAPE Vivo, which streams vitals to clinicians via low-power Bluetooth. Automotive safety innovations include Volvo’s embedded alcohol biosensors in 8% of 2025 models, preventing ignition if blood alcohol exceeds 0.02%. Energy efficiency breakthroughs, such as graphene-based sensors consuming 50 µW, enable continuous operation in pacemakers for 15 years without battery replacement. As edge computing minimizes data latency, embedded biosensors are set to underpin 80% of Industry 4.0 manufacturing processes by 2027, predicts Gartner.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By Product Type: Non-Wearable Biosensors Set the Standard in Clinical Accuracy

Non-wearable biosensors hold 60.08% market share of the biosensors market, prized for their robust accuracy and integration into routine diagnostics. Blood-gas analyzers, used in 90% of ICUs, deliver critical metabolic insights in 2–3 minutes, reducing ventilator-induced lung injury by 20%. Laboratory glucose analyzers perform 4 billion tests annually, with Abbott’s Alinity systems achieving 99% concordance with central labs. Home pregnancy kits remain staples, with 500 million annual sales of ClearBlue’s 99% accurate hCG detectors.

Cardiac biosensors dominate 85% of emergency departments, detecting troponin surges within 20 minutes to slash heart attack mortality by 18%. Post-pandemic, 80% of labs utilize rapid pathogen biosensors like Cepheid’s Xpert Xpress, identifying SARS-CoV-2 in 22 minutes. Industrial applications include Nestlé’s toxin sensors ensuring 0.01 ppm pesticide compliance in 12% of global seafood, while USDA-approved ATP swabs cut food safety inspection times by 90%. With 98% clinical accuracy and evolving AI integration, non-wearables remain indispensable across healthcare, food safety, and environmental sectors.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America: US Set to Keep the Dominance and Innovation at Pace

North America dominates the global biosensors market with a 44.61% share in 2025, driven by the U.S.’s unparalleled innovation ecosystem. The United States has firmly established its position as the global leader in the biosensors market, commanding a significant 41% share of the North American market in 2024. This prominence is propelled by a confluence of factors, including a sophisticated healthcare system, substantial investment in research and development, and a growing demand for advanced diagnostic tools. The country is set for continued and robust expansion, with a projected compound annual growth rate (CAGR) of 7.99% between 2025 and 2033.

Technological trends within the U.S. market reveal a clear preference for specific applications and platforms. Electrochemical biosensors are the dominant technology, capturing over 70% of market revenue in 2023 due to their versatility and wide-ranging applications. The medical sector is the principal driver, accounting for a 67.57% revenue share in the same year, largely fueled by the rising prevalence of chronic diseases that require continuous monitoring. This is further evidenced by the dominance of point-of-care (POC) testing, which represented the largest end-use segment with a 47.67% share in 2023.

The engine behind this market leadership is a vibrant and well-funded innovation ecosystem. Significant investments from both private and public sectors are accelerating the development of next-generation technologies. For instance, the strong investor confidence in the sector was highlighted by San Diego-based Biolinq securing $100 million in Series C financing in April 2025.

Europe's Biosensors Market Thrives on Regulatory Support and Technological Integration

Europe's biosensors market is demonstrating robust growth, capturing a significant 28.3% of the global market in 2025, a success buoyed by harmonized regulations and widespread digitization. Regulatory bodies are accelerating this trend, with the European Medicines Agency (EMA) approving 13% more biosensors in 2024 than in the previous year. This includes prioritizing high-impact devices like Roche’s cobas Liat PCR systems, which deliver sepsis diagnoses with 99% specificity in just 20 minutes. At the forefront of clinical innovation, Germany and the U.K. lead research efforts, accounting for 46% of European trials, such as Charité Berlin’s pioneering work on implantable neural sensors for Parkinson’s monitoring. This clinical adoption is mirrored in hospitals, where Eurostat data reveals a 12% rise in point-of-care biosensor usage, exemplified by Siemens Healthineers’ Atellica VTLi, now used in 70% of EU emergency rooms to reduce cardiac troponin test times to a mere seven minutes.

Strategic funding and expanding applications are further fueling the dynamism of the biosensors market in Europe. Initiatives like the €220 million Horizon Europe program are fast-tracking innovative projects, including the Graphene Flagship’s development of sweat-based diabetes biosensors, while France’s “Health Innovation 2030” plan subsidizes 40% of R&D costs for AI-driven sensors. This innovation is meeting soaring demand in telehealth, where 69% of EU systems now integrate biosensors into platforms like Doctolib for remote COPD management. The cardiovascular sector saw an 11% growth in biosensor use, with Abbott’s Confirm Rx now endorsed in 55% of post-stroke rehab programs. Moreover, sustainability mandates, such as requiring advanced water-quality biosensors in 30% of municipal systems by 2026, are opening new frontiers for the market.

Asia-Pacific's Biosensor Market Driven by Healthcare Reforms and Digital Adoption

The Asia-Pacific biosensors market, which accounts for 19.8% of the global share in 2025, is experiencing rapid growth fueled by healthcare digitization and aging populations. A notable driver is the World Health Organization's reported 8% year-over-year spike in regional diabetes cases, which has led to a 16% surge in continuous glucose monitoring (CGM) sales in China, with Sinocare's GM700SB selling 12 million units in 2024. In India, the Ayushman Bharat initiative has significantly improved public health access by deploying 250,000 point-of-care (POC) biosensors in rural clinics, drastically reducing TB diagnosis times from seven days to just 15 minutes. Meanwhile, Japan’s Ministry of Health, Labour and Welfare (MHLW) is prioritizing implantable devices for its elderly citizens, leading to 10% annual growth in cardiac monitors like Omron’s HeartGuide.

Innovation and investment are further accelerating the region's prominence in the global biosensors market. China’s NMPA approved 45 new biosensors in 2024, including Innoventric’s AI-powered stroke risk predictor, now adopted by 40% of top-tier hospitals. This technological integration extends to telehealth, with 55% of APAC platforms now incorporating biosensors, such as Practo’s partnership with Healthians for at-home HbA1c testing. Consumer adoption is also climbing, with wearable use jumping 18% year-over-year, led by devices like Xiaomi’s Mi Band 8 Pro. Groundbreaking local startups like Vietnam’s BioStaple, using graphene for dengue detection, are emerging, while Indonesia’s Good Doctor platform processes 100,000 biosensor readings daily. With the region's startups securing $1.2 billion in 2024 VC funding, the Asia-Pacific biosensor market is poised to outpace global growth by 2026.

Top 8 Developments in the Biosensors Market Shows Market Players’ Focus Areas

- Biolinq Secures $100 Million in Series C Funding (April 2025): San Diego-based biotech startup Biolinq, which is developing multi-analyte biosensors for metabolic health, raised a noteworthy $100 million in a Series C funding round. The round was led by Alpha Wave Ventures, signaling strong investor confidence in the company's technology.

- Oura Receives $75 Million Investment from DexCom (November 2024): In a significant move bridging consumer wearables and medical-grade biosensors, Oura, the company behind the Oura Ring, announced a $75 million funding round from glucose monitoring leader DexCom. The investment aims to integrate glucose data with the Oura Ring's health tracking capabilities and will also be used for international expansion and potential future acquisitions.

- Medtronic and Microsoft Azure Expand Partnership (October 2024): Medical device giant Medtronic has deepened its collaboration with Microsoft Azure to utilize AI-powered analytics for its biosensor data. This expanded partnership is focused on the remote detection of cardiac arrhythmia and heart failure risk, representing a major investment in the integration of artificial intelligence with biosensor technology.

- U.S. National Science Foundation Invests in Biosensor Research (October 2024): A research team at Pennsylvania State University received a $1.5 million grant over three years from the U.S. National Science Foundation. This funding is dedicated to the development of advanced technology-based solutions in the biosensor field, highlighting government support for fundamental research.

- Trinity Biotech and Bayer to Partner on CGM Biosensor (January 2024): Trinity Biotech has entered into a letter of intent with global life sciences company Bayer for a joint partnership. The collaboration is focused on the launch of a continuous glucose monitoring (CGM) biosensor device in the significant markets of China and India.

- Andson Biotech Raises $3.6 Million in Series A Funding (March 2024): Atlanta-based Andson Biotech successfully closed a $3.6 million Series A funding round. This investment in a newer startup indicates ongoing venture capital interest in fostering emerging technologies within the biosensor landscape.

- Royal Philips and SmartQare Form Strategic Partnership (April 2024): Global health technology leader Royal Philips has partnered with SmartQare to integrate its 'viQtor' solution for clinical patient monitoring. This strategic collaboration is aimed at co-developing the next generation of continuous patient monitoring systems for both hospital and home settings.

- Aligned Bio Secures Seed Funding (August 2024): Swedish startup Aligned Bio, which is developing a novel platform for studying single molecules, raised $390,000 in a seed funding round. Investors included Almi Invest and the European Union, demonstrating support for early-stage innovation in biosensor technology.

Top Players in the Biosensors Market

- Bio-Rad Laboratories Inc.

- Biosensors International Group, Ltd.

- Pinnacle Technologies Inc.

- Johnson & Johnson

- Koninklijke Philips N.V.

- DuPont

- Molecular Devices Corp.

- Bayer

- Molex LLC

- TDK Corp.

- Seimens

- Nova Biomedical

- LifeScan, Inc.

- Medtronic

- Abbott Laboratories

- Roche

- DirectSens GmbH

- Zimmer & Peacock AS

- Other Prominent Players

Market Segmentation Overview

By Type

- Sensor Patch

- Embedded Device

By Product

- Wearable Biosensors

- Non-Wearable Biosensors

By Technology

- Electrochemical

- Amperometric

- Potentiometric

- Voltammetric

- Others

- Physical

- Piezoelectric

- Thermometric

- Optical

By Application

- Medical

- POC Testing

- Cholesterol

- Blood Glucose

- Blood Gas Analyzer

- Pregnancy Testing

- Drug Discovery

- Infectious Disease

- Bioreactor

- Agriculture

- Environment

- Research & Development

- Security and Bio-Defense

- Others

By End User

- Healthcare & Diagnostics

- Food and Beverage

- Pharmaceutical

- Agriculture

- Cosmetics

- Environmental

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia & New Zealand

- ASEAN

- Cambodia

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |