Influenza Vaccine Market: By Type (Inactivated influenza vaccine (IIV) (Quadrivalent and Trivalent) and Live-attenuated influenza vaccine (LAIV)); Process (Egg Based, Cell Culture-Based, and Recombinant); Route of Administration (Injectable and Intra-nasal); Age Group (Pediatric and Adult); Distribution Channel (Hospitals & Pharmacies, Government Suppliers, and Others); Region— Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2026–2035

- Last Updated: 28-Jan-2026 | | Report ID: AA0124744

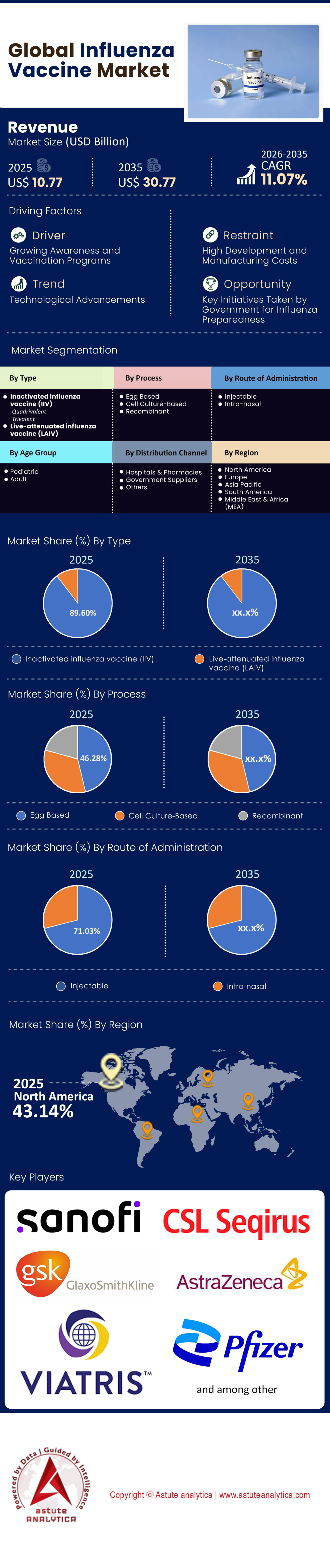

Market Snapshot

Influenza vaccine market was valued at US$ 10.77 billion in 2025 and is projected to hit the market valuation of US$ 30.77 billion by 2035 at a CAGR of 11.07% during the forecast period 2026–2035.

Key Findings

- By Type, Inactivated Influenza Vaccine (IIV) segment, holding an impressive 89.60% market share.

- By Process, egg-based segment holds the largest share of 46.28%.

- By Route of administration, injectable route of administration currently dominates the global influenza vaccine market, holding a major share of 71.03%.

- By age group, adult are the largest consumers of the market, accounting for 78.25% market share.

- North America, particularly the United States, leads the global influenza vaccine market with a commanding market share of over 43%

The global influenza vaccine market is currently undergoing its most significant structural transformation in five decades. Once characterized by commoditized, low-margin biologics and a reliance on 1940s-era egg-based manufacturing, the sector has pivoted into a high-value technology battleground. As of 2026, the market valuation stands at the intersection of three massive trendlines: the “premiumization” of prevention, the regulatory extinction of the B/Yamagata lineage, and the disruptive entry of mRNA technology.

While the influenza vaccine market has historically grown at a steady, double-digit CAGR, the market is witnessing a divergence in value versus volume. Volume growth is stabilizing, but revenue growth is accelerating due to the shift from Standard Dose (SD) vaccines to High-Dose (HD), Adjuvanted, and Recombinant formats. The era of the $15 flu shot is ending; the era of the $60+ high-efficacy prophylactic is here.

For stakeholders, the critical insight is that “seasonality” is no longer the only risk factor. The new variables are technological platform dominance (Egg vs. Cell vs. mRNA) and the rise of the "Respiratory Pan-Vaccine"—a single combination shot targeting Influenza, COVID-19, and RSV. This report provides a granular analysis of these shifts, forecasting a market that is rapidly moving away from legacy infrastructure toward precision immunology.

To Get more Insights, Request A Free Sample

The Technology Paradigm Shift: Analyzing Production Platforms

To understand the influenza vaccine market's future profitability, one must analyze the "Platform Wars." The method of manufacturing is no longer just a technical detail, it is the primary driver of Cost of Goods Sold (COGS), efficacy, and pricing power.

Egg-Based Manufacturing: The Legacy Anchor

Despite the industry's modernization, egg-based manufacturing remains a significant volume driver for the influenza vaccine market. However, its dominance is being eroded by "egg-adaptation" issues. When human influenza strains are grown in hen eggs, they often mutate to survive in the avian environment. This results in an antigenic mismatch—essentially, the vaccine produced does not look exactly like the wild virus circulating in the population. The phenomenon, particularly prevalent in the H3N2 strain, has historically capped egg-based vaccine efficacy at 40-60%. While COGS are low, the clinical ceiling has been reached.

Cell-Based Technology: The Current Gold Standard

Leading the transition is Cell-Based manufacturing (primarily championed by CSL Seqirus). By growing the virus in mammalian cell lines (MDCK cells) rather than eggs, manufacturers in the influenza vaccine market avoid egg-adaptive mutations. The result is a closer match to the circulating wild-type virus. From a market perspective, cell-based vaccines command a price premium and offer better scalability during pandemics, as they are not constrained by the 6-month lead time required to secure millions of specialized eggs.

Recombinant Technology: Precision Engineering

Sanofi’s recombinant platform (Flublok) represents the peak of protein engineering. By genetically programming insect cells to produce only the Hemagglutinin (HA) protein, this platform in the influenza vaccine market achieves 100% purity (no egg or antibiotic traces) and allows for a 3x antigen load. This is the "high-performance" segment of the market, specifically targeting stakeholders willing to pay for higher efficacy guarantees.

mRNA: The Disruptor

Moderna and Pfizer are aggressively entering the influenza vaccine market. The value proposition of mRNA is not necessarily higher efficacy (initial Phase 3 data has been mixed regarding superiority over high-dose incumbents), but rather speed. mRNA cuts the strain-selection-to-vial timeline from 6 months to under 60 days. This allows manufacturers to select strains much later in the season, significantly increasing the probability of a strain match. However, the high reactogenicity (side effects like fever/chills) seen in early mRNA flu trials remains a commercial barrier to entry that must be solved to capture the mass market.

The "Yamagata Extinction": Regulatory & Manufacturing Implications

Astute Analytica’s market analysis identifies the global regulatory shift from Quadrivalent (QIV) back to Trivalent (TIV) formulations.

The Disappearance of a Lineage

Since March 2020, the B/Yamagata lineage of influenza has not been confirmed globally—a collateral effect of COVID-19 lockdowns and non-pharmaceutical interventions. In response, the WHO and FDA VRBPAC have recommended removing the B/Yamagata antigen from vaccines.

The "Shrinkflation" Margin Opportunity

For manufacturers, this is a distinct financial positive. Removing the 4th strain frees up approximately 25% of manufacturing capacity (bioreactor space or egg volume). Crucially, market intelligence suggests that manufacturers will not lower the price of the Trivalent vaccine proportionally. Instead, they will likely maintain near-QIV pricing while reducing the antigen payload. This effectively increases the margin per dose. Stakeholders should view the transition to Trivalent formulations not as a loss of product value, but as an efficiency gain that improves the Gross Margin profile of the major incumbents starting in the 2025-2026 season.

The "Holy Grail": Combination Vaccines & Universal Flu Shots

The next frontier for influenza vaccine market expansion is the "Triple Threat" strategy. The standalone flu shot market is maturing, but the respiratory protection market is in its infancy.

The Combination Workflow

Moderna and BioNTech are racing to commercialize a combined Influenza + COVID-19 (and eventually + RSV) vaccine. The economic logic is undeniable: it solves the "vaccine fatigue" problem and streamlines the retail pharmacy workflow. For payers and insurers, a single administration fee is preferable to two or three. It is estimated that by 2027, combination vaccines will begin to cannibalize the standalone flu market, particularly in the working-age adult demographic where convenience drives compliance.

The Universal Influenza Vaccine (UIV)

While further out on the horizon, research into "stalk-based" immunity (targeting the conserved stem of the hemagglutinin protein rather than the mutating head) is progressing. If successful, this would transition the influenza vaccine market from an annual recurring revenue model to a booster-based model (every 3-5 years). While this lowers volume, the price-per-dose for a UIV would likely be 5x-8x that of a standard seasonal shot, preserving total addressable market (TAM) value.

Competitive Landscape: Strategic Positioning of Players in Influenza Vaccine Market

- Sanofi (The Incumbent): Sanofi is aggressively defending its market leadership by converting its portfolio to premium products. Their strategy relies on Efluelda/Fluzone High-Dose. They are building their own mRNA capabilities to hedge against Moderna but are currently winning on the proven efficacy of their recombinant and high-dose protein platforms.

- CSL Seqirus (The Cell Leader): CSL has successfully differentiated itself as the "Non-Egg" alternative in the influenza vaccine market. Their Flucelvax and Fluad (adjuvanted) brands are taking share from standard egg-based competitors. Their investment in self-amplifying mRNA (sa-mRNA) indicates they plan to skip the first generation of mRNA tech for a lower-dose, lower-side-effect version.

- GSK: GSK has pivoted toward an adjuvanted strategy but faces stiff competition. Their focus has shifted slightly toward their massive RSV success, leaving them vulnerable in the pure-play flu market compared to Sanofi and CSL.

Investment Risks & Future Outlook

While the influenza vaccine market trajectory is positive, stakeholders must navigate significant downside risks that are unique to this industry.

- The "Mild Season" Valuation Trap: The influenza market is uniquely sensitive to epidemiological luck. A "mild" flu season with low transmission rates leads to unused inventory and high returns (in markets with return policies). More importantly, a mild season reduces public urgency for the following year, causing cyclical dips in revenue. Investors must view flu stocks on a 3-year rolling average rather than year-over-year.

- Technological Execution Risk: The pivot to mRNA is not guaranteed. If Phase 3 trials for combined Flu/COVID shots show high reactogenicity (severe arm pain, fever) compared to standard flu shots, consumer uptake will be low. The "convenience" of a combo shot does not outweigh the fear of losing a day of work to side effects.

- Regulatory Strain Mismatch: Even with mRNA's speed, if the WHO selects the wrong strain for the season, vaccine effectiveness (VE) can drop below 30%. In the age of social media, a year of low VE can severely damage brand trust, leading to long-term hesitancy.

By 2035, the "one-size-fits-all" egg-based flu shot will be a relic. The market will belong to companies that can dominate the Adult (78% share) segment with Premium (Cell/mRNA/Recombinant) formulations. The winners will be those who successfully transition from selling a commodity to selling a high-efficacy, premium respiratory health service.

Market Segmentation: A Deep Dive into Structural Dynamics

By Vaccine Type: The Dominance of IIV (89.60% Share)

The Inactivated Influenza Vaccine (IIV) segment commands an overwhelming 89.60% of the market share in the influenza vaccine market. This dominance is not accidental; it is a result of clinical reliability and broad licensure.

- The Failure of LAIV: Live Attenuated Influenza Vaccines (nasal sprays) have failed to capture significant market share due to historical efficacy gaps (particularly against H1N1 in the mid-2010s) and contraindications for immunocompromised patients.

- Split-Virion vs. Subunit: Within the IIV category, the market is shifting toward "split-virion" and "subunit" technologies which are less reactogenic.

- The High-Dose Sub-Segment: A critical insight within the IIV figures is the internal shift toward High-Dose IIV (HD-IIV). While standard IIV provides the volume, HD-IIV drives the profitability. Sanofi’s Fluzone High-Dose, which falls under this IIV umbrella, accounts for a disproportionate amount of revenue relative to volume due to its premium pricing structure. The 89.60% share signifies that despite the hype of novel technologies, the dead-virus approach remains the undisputed regulatory king.

By Process: The Value-Based Reality of Egg-Based (46.28% Share)

The data indicates the egg-based segment holds a 46.28% market share.

- Analyzing the Decline: Historically, egg-based production accounted for 80-90% of global volume. A share of 46.28% represents a massive structural pivot. This figure likely reflects value share (revenue) rather than just volume. While egg-based vaccines (like basic Fluzone or Fluarix) are produced in massive quantities, they are sold at commodity prices (USD 10−18 per dose).

- The Rise of Non-Egg Competitors: The remaining ~54% of the market is now captured by Cell-Based (CSL Seqirus) and Recombinant (Sanofi) technologies. These technologies command significantly higher prices (USD 45−65 per dose).

- Manufacturing Economics: The drop to 46.28% is a signal to investors that the "egg monopoly" is over. The industry is effectively diversifying its risk. Reliance on chicken flocks is a biological security risk (e.g., Avian Flu wiping out supply flocks). The market is rewarding companies that have diversified away from eggs, pushing the legacy method into a minority revenue position for the first time in history.

By Route of Administration: Injectable Dominance (71.03% Share)

The dominance of the segment is not just about vials; it is driven by the rise of Pre-Filled Syringes. In developed markets (US, EU), PFS is the standard of care because it reduces dosing errors, ensures sterility, and speeds up patient throughput in retail pharmacies (CVS, Walgreens).

- The "Other" 29%: The remaining share is comprised of Nasal Sprays (FluMist) and the emerging field of Microneedle Patches and Jet Injectors. While the idea of a "pain-free" patch is attractive, the manufacturing complexity of thermostable patches has kept costs high. The injectable dominance is sustained by the established cold-chain infrastructure that is optimized for syringes, not patches.

Despite needle phobia, the injectable route is viewed as "clinically serious" by the adult population, whereas nasal sprays often struggle with a perception of being "for children," limiting their adult market penetration.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By Age Group: The Adult Economic Engine (78.25% Share)

Adults are the largest consumers, accounting for a staggering 78.25% market share. This market share is the single most important data point for profitability. The pediatric market is high-volume but largely commoditized (often covered by government Vaccines for Children programs at lower margins). The adult market, specifically the 65+ demographic, is where the "Premium" tier exists.

- Immunosenescence Strategy: As the immune system ages (immunosenescence), standard vaccines fail to trigger an adequate response. This biological fact has created the market for "Enhanced Vaccines" (High-Dose, Adjuvanted, Recombinant). These products are exclusively licensed for adults/seniors and cost 3x-4x more than pediatric doses.

- Workforce Protection: The 18-64 demographic is also a key driver, fuelled by corporate wellness programs and insurance mandates. The economic cost of flu-related absenteeism drives employers to subsidize adult vaccination, sustaining this 78% share.

- Future Growth: With the global population aging (particularly in Japan, Western Europe, and the US), the Adult segment will likely expand further, potentially breaking 80% market share by 2028. This demographic reality forces all pipeline development to focus on higher efficacy for older adults rather than novel delivery for children.

To Understand More About this Research: Request A Free Sample

Regional Analysis & Supply Chain Resilience

North America is the Value Hub in The Influenza Vaccine Market

The US and Canada represent the highest value region globally, despite not having the highest population. This is driven by the US "Open Market" model, where pricing is not capped by single-payer tenders, allowing for the widespread adoption of premium vaccines (High-Dose and Adjuvanted). The supply chain here is highly optimized for retail pharmacy distribution, with chains like CVS and Walgreens acting as the primary points of care.

Europe (The Tender Battleground):

Europe influenza vaccine market is characterized by fragmentation. Countries like the UK and Germany operate on tender-based procurement, where regional governments bid for supply. This drives prices down and favors volume-based competitors. However, the ECDC (European Centre for Disease Prevention and Control) is increasingly recommending enhanced vaccines for the elderly, slowly opening the door for premium products in wealthy EU nations. Supply chain complexity is higher here due to varying packaging and language requirements for each member state.

Asia-Pacific (The Growth Engine):

APAC is the fastest-growing region in the influenza vaccine market by volume. Japan has a rapidly aging population, creating a massive untapped market for high-dose vaccines. China represents a unique ecosystem dominated by domestic players like Hualan Biological Engineering. The supply chain in APAC is challenged by "last-mile" cold chain issues in developing nations (India, Indonesia), but significant investments in domestic manufacturing (Serum Institute of India) are reducing reliance on Western imports.

- Supply Chain Decentralization: The post-COVID era has forced a move from centralized bulk manufacturing (e.g., one giant plant supplying a continent) to "in-country" manufacturing to satisfy national security mandates. mRNA technology facilitates this, as smaller footprint "pod" factories can be established locally, reducing global shipping risks.

Top Players in the Global Influenza Vaccine Market

- Abbott Laboratories

- AstraZeneca

- Emergent BioSolutions Inc

- Emergex Vaccines Holding Limited

- GSK plc

- Merck & Co., Inc.

- OSIVAX

- Pfizer Inc.

- Sanofi SA

- CSL Limited

- Sinovac Biotech Ltd.

- SK bioscience Co., Ltd.

- Viatris Inc.

- Other Prominent Players

Market Segmentation Overview:

By Type

- Inactivated influenza vaccine (IIV)

- Quadrivalent

- Trivalent

- Live-attenuated influenza vaccine (LAIV)

By Process

- Egg Based

- Cell Culture-Based

- Recombinant

By Route of Administration

- Injectable

- Intra-nasal

By Age Group

- Pediatric

- Adult

By Distribution Channel

- Hospitals & Pharmacies

- Government Suppliers

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

FREQUENTLY ASKED QUESTIONS

Valued at US$ 10.77 billion in 2025, the market will reach US$ 30.77 billion by 2035 (CAGR 11.07%), driven by premium high-dose and mRNA shifts.

Egg-based (46%) declines due to mutations; cell-based and recombinant rise for better strain match and scalability, while mRNA cuts timelines to 60 days.

Lineage absent since 2020; trivalent shift frees 25% capacity, boosting margins as pricing holds despite reduced antigens.

IIV (89.6%), injectable (71%), adults (78.25%); North America leads (43%) via premium adult vaccines over commoditized pediatric volume.

Flu+COVID+RSV shots solve fatigue, streamline pharmacy ops; universal flu (stalk-based) eyes 3-5 year boosters at 5x pricing.

Sanofi (high-dose/recombinant), CSL Seqirus (cell/adjuvanted), GSK lag; mRNA entry risks reactogenicity but rewards speed dominance.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |