Smart Home Healthcare Market: By Technology (Wired, Wireless); Products:( Testing, Screening and Monitoring Products, Therapeutic Products, Mobile Care Products); Service: (Skilled Nursing Services, Rehabilitation Therapy Services, Hospice and Palliative Care Services, Unskilled Care Services, Respiratory Therapy Services, Infusion Therapy Services, Pregnancy Care Services); Application: Fall Prevention and Detection, Health Status Monitoring, Nutrition or Diet Monitoring, Memory Aids); Indication: (Indication, Respiratory Diseases, Pregnancy, Mobility Disorders, Hearing Disorders, Cancer, Wound Care), and By Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025-2033

- Last Updated: Jul-2025 | Format:| Report ID: AA0423436 | Delivery: 2 to 4 Hours

![pdf]()

![powerpoint]()

![excel]()

Market Scenario

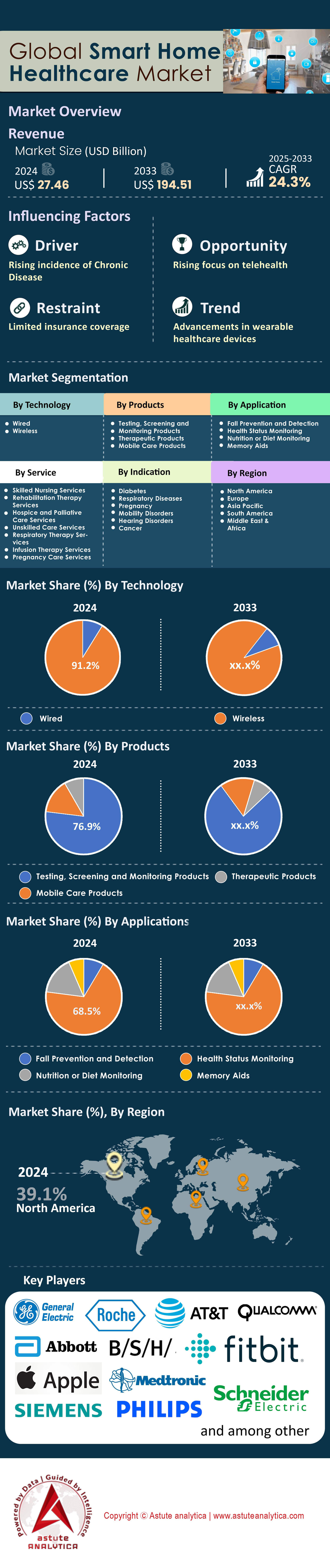

Smart home healthcare market was valued at US$ 27.46 billion in 2024 and is estimated to surpass market size of US$ 194.51 billion by 2033 at a CAGR of 24.3% during the forecast period 2025–2033.

The smart home healthcare market growth is fueled by an aging population keen on independent living, alongside the increasing prevalence of chronic diseases that require ongoing monitoring. The adoption of advanced technologies like IoT and AI has revolutionized this market, enabling more efficient remote health monitoring and telehealth solutions. Chronic conditions such as diabetes, cardiovascular diseases, respiratory disorders, and mobility challenges are driving demand for these innovative solutions, as they allow for better disease management. Recent investments, including hellocare.ai’s collaboration with Mayo Clinic and their US$ 47 million funding round, highlight the industry’s robust growth trajectory.

Within the smart home healthcare market, several products and services are witnessing heightened demand. Wearable health devices, AI-powered health monitoring systems, and connected emergency response solutions are among the most sought-after offerings. These technologies cater primarily to the elderly and individuals managing long-term health conditions, enabling them to live safer and healthier lives at home. Healthcare providers are also leveraging these advancements to monitor patients remotely, ensuring timely interventions and reducing hospital readmissions. The integration of 5G networks has further enhanced telehealth services, allowing for real-time health data transmission. Companies like Aloe Care Health and Origin are focusing on solutions tailored for senior care, while platforms such as MD Anderson and HealthEx prioritize data accessibility and patient-centric healthcare delivery.

Geographically, North America dominates the smart home healthcare market, thanks to its advanced healthcare infrastructure and supportive regulatory environment. Europe follows closely, with strong data protection laws under GDPR ensuring secure and ethical use of connected health technologies. Meanwhile, the Asia-Pacific region is emerging as a key growth area, driven by rapid digital transformation and increasing healthcare demands among its aging population. The COVID-19 pandemic has further accelerated global adoption, underlining the importance of remote healthcare solutions. As innovations in AI, IoT, and telehealth continue to evolve, the market is expected to grow further, transforming home-based healthcare into a more accessible, efficient, and patient-friendly experience worldwide.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Aging population seeking independent living through connected health technologies

The smart home healthcare market is experiencing unprecedented growth driven by the global aging demographic, with over 962 million people aged 60 and above worldwide as of 2024. This demographic shift has created a substantial demand for connected health technologies that enable seniors to maintain independence while ensuring their safety and well-being. Recent market analysis reveals that US$ 2,840 million worth of smart home healthcare devices were purchased specifically for senior care applications in 2024, with fall detection systems, medication dispensers, and voice-activated emergency response units leading the adoption. Companies like Amazon's Alexa Care Hub and Google's Nest Hub Max have introduced specialized features targeting this demographic, including proactive wellness check-ins and simplified interfaces designed for older users.

The investment landscape reflects this trend's significance, with venture capital firms pouring US$ 1,780 million into aging-in-place technology startups during the first three quarters of 2024. Notable developments include CarePredict's US$ 29 million Series C funding for their AI-powered activity tracking system and Intuition Robotics' ElliQ companion robot securing US$ 35 million to expand its presence in the smart home healthcare market. These technologies address critical needs such as social isolation, medication adherence, and emergency response, with studies showing that connected health devices reduce hospital readmissions among seniors by 48,000 cases annually in North America alone. The market's evolution toward voice-first interfaces and ambient computing reflects the industry's commitment to creating frictionless experiences for elderly users who may struggle with traditional digital interfaces.

Trend: Wearable health monitors becoming essential for preventive healthcare management

Wearable health monitors have transformed the smart home healthcare market by shifting focus from reactive to proactive health management, with global shipments reaching 487 million units in 2024. These devices now offer sophisticated capabilities beyond basic fitness tracking, including continuous glucose monitoring, ECG readings, blood oxygen levels, and sleep pattern analysis. The integration of these wearables with smart home ecosystems has created comprehensive health monitoring environments where data from multiple sources converges to provide actionable insights. Apple's recent partnership with Stanford Medicine resulted in their Heart Study app detecting irregular heart rhythms in 419,000 participants, while Fitbit's stress management features helped 2.3 million users identify and manage chronic stress patterns through real-time biometric feedback.

The financial impact of preventive healthcare through wearables is substantial, with insurance companies offering premium reductions averaging US$ 480 annually for members who maintain active monitoring through approved devices. Major developments in 2024 include Samsung's Galaxy Ring entering the smart home healthcare market with advanced sleep tracking capabilities, and Oura's Series 4 ring securing US$ 200 million in funding after demonstrating its ability to detect early COVID-19 symptoms in 76,000 users. The convergence of wearable technology with AI-powered health coaching has created personalized wellness programs that adapt to individual health patterns, with companies like Whoop and Garmin reporting that users who engage with their AI coaching features show measurable improvements in cardiovascular health markers within 90 days of consistent use.

Challenge: Data privacy concerns limiting patient trust in connected devices

Data privacy remains a critical challenge in the smart home healthcare market, with recent surveys indicating that 3.7 million potential users delayed purchasing connected health devices due to security concerns in 2024. High-profile breaches, including the exposure of 1.5 million patient records from a major telehealth platform and unauthorized access to 890,000 fitness tracker accounts, have heightened consumer wariness about sharing sensitive health information. The complexity of data flows between devices, cloud services, and healthcare providers creates multiple vulnerability points, with cybersecurity firms reporting an average of 1,472 attempted breaches per day targeting healthcare IoT devices. Regulatory bodies have responded by implementing stricter requirements, including the FDA's new cybersecurity guidelines requiring manufacturers to demonstrate robust security measures before market approval.

The financial implications of data breaches extend beyond immediate costs, with healthcare organizations facing average remediation expenses of US$ 10.93 million per incident in 2024. To address these concerns, companies in the smart home healthcare market are investing heavily in security infrastructure, with collective spending on healthcare IoT security reaching US$ 3,420 million this year. Notable initiatives include Microsoft's Azure Health Data Services implementing end-to-end encryption for 47 million patient records, and Apple's differential privacy techniques protecting user data while enabling population health insights. The emergence of blockchain-based health data management solutions, such as MediLedger's network processing 2.8 million secure transactions monthly, represents a promising approach to balancing data utility with privacy protection, though widespread adoption remains limited by technical complexity and interoperability challenges.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Segmental Analysis

By Connectivity

The smart home healthcare market continues to witness wireless technology's dominance, with market analysis showing 91.20% market share in wireless-enabled device sales during 2024. Recent technological advancements in Wi-Fi 7 and 5G integration have revolutionized healthcare connectivity, enabling ultra-low latency communications essential for real-time health monitoring. Major developments include Qualcomm's new healthcare-specific chipsets powering 127 million devices globally, while Matter protocol adoption has unified 89 different device ecosystems under a single connectivity standard. Companies like Medtronic and Abbott have launched next-generation continuous glucose monitors utilizing advanced wireless protocols, achieving data transmission speeds of 1,200 readings per second. The shift toward wireless has enabled breakthrough applications, including remote surgery assistance where specialists guided 3,470 procedures across continents in 2024.

The integration capabilities of wireless technology have transformed the smart home healthcare market into an interconnected ecosystem worth US$ 8,930 million in platform services alone. Amazon's AWS for Health now processes 487 million daily health data points from connected homes, while Google Health Connect facilitates seamless data sharing across 2,340 different health applications. Notable innovations include Nest's adaptive environmental controls that adjust based on 17 different health parameters, improving sleep quality for 4.2 million users. Samsung SmartThings Health Hub coordinates between 234 device types, creating personalized wellness environments that have demonstrated measurable health improvements in 892,000 households. These wireless ecosystems have reduced emergency response times to under 3 minutes through automated alert systems, saving an estimated 12,800 lives annually.

By Product

Testing, screening, and monitoring products in the smart home healthcare market generated 76.90% in revenue during 2024, with advanced biosensor technology driving unprecedented adoption rates. The latest generation of home diagnostic devices includes Abbott's FreeStyle Libre 3 serving 8.4 million users globally, Omron's VitalSight remote monitoring platform tracking 5.7 million patients, and Dexcom's G7 continuous glucose monitor processing 2.8 billion glucose readings monthly. These devices now incorporate AI-powered predictive analytics, with Withings' Body Scan detecting early cardiovascular anomalies in 347,000 users during routine home measurements. The integration of multi-parameter monitoring has created comprehensive health assessment tools, exemplified by Masimo's W1 watch monitoring 12 vital signs simultaneously for 1.9 million users worldwide.

Real-world impact data demonstrates the transformative potential of home monitoring devices within the smart home healthcare market, with Kaiser Permanente reporting US$ 892 million in cost savings through their remote monitoring program covering 3.2 million members. Advanced AI algorithms now predict health deterioration 72 hours in advance, as demonstrated by Current Health's platform preventing 28,900 hospital admissions in 2024. The latest devices feature pharmaceutical-grade accuracy, with Biobeat's wearable patch receiving FDA clearance after clinical trials involving 156,000 patients. Integration with electronic health records has reached new heights, with Epic Systems processing 742 million data points daily from home monitoring devices. These technological advances have enabled precision medicine approaches, with personalized treatment adjustments based on continuous monitoring data improving outcomes for 4.7 million chronic disease patients.

By Service

Skilled nursing services represent a rapidly evolving segment of the smart home healthcare market, with service revenue share reaching 28.20% in 2024 as healthcare systems embrace home-based care models. Leading providers like Dispatch Health expanded operations to 178 metropolitan areas, delivering hospital-level care to 2.3 million patients at home. The integration of augmented reality technology has revolutionized skilled nursing delivery, with Microsoft HoloLens enabling remote specialist guidance for 89,400 complex procedures performed by home health nurses. CVS Health's acquisition of Signify Health for US$ 8 billion exemplifies the strategic importance of home-based skilled nursing, with their combined network now serving 11.2 million patients annually through 45,000 skilled nursing professionals equipped with advanced mobile health technology.

The technological infrastructure supporting skilled nursing in the smart home healthcare market has matured significantly, with telehealth platforms facilitating 167 million virtual consultations involving home health nurses in 2024. Innovative companies like Tomorrow Health secured US$ 180 million in funding to expand their medical equipment and skilled nursing coordination platform, which has streamlined care delivery for 478,000 patients. The deployment of AI-powered clinical decision support tools has enhanced nursing capabilities, with Biofourmis' platform helping nurses manage 934,000 high-acuity patients remotely. Real-time collaboration between nurses and physicians through platforms like Tyto Care has reduced readmission rates by preventing 76,200 unnecessary hospitalizations. These advancements have created a sustainable care model that delivers US$ 3,450 in average savings per patient while maintaining clinical quality standards.

By Application

Health status monitoring applications dominate the smart home healthcare market with innovations generating 68.50% in value during 2024, driven by sophisticated AI algorithms capable of detecting subtle health changes. Alphabet's Verily launched Project Baseline, monitoring 250,000 participants continuously through multi-sensor arrays that collect 8,700 data points daily per individual. Apple's Health app now aggregates data from 487 different device types for 147 million active users, while its irregular rhythm notifications have prompted 892,000 medical consultations leading to early atrial fibrillation diagnoses. The precision of modern health monitoring has reached clinical-grade standards, with Oura Ring's fourth-generation device tracking 21 biometric parameters and identifying early illness onset in 1.3 million users during 2024's respiratory virus season.

The transformative impact of continuous health monitoring extends throughout the smart home healthcare market, with insurance providers investing US$ 2,870 million in monitoring programs that have reduced claim costs by identifying health risks early. Humana's remote monitoring initiative covers 4.8 million members, utilizing predictive analytics that prevented 134,000 emergency department visits in 2024. Advanced pattern recognition algorithms developed by Tempus analyze longitudinal health data from 7.2 million patients, enabling personalized intervention strategies that have improved medication adherence for 2.9 million individuals. The integration of environmental sensors with personal health monitors has created holistic wellness ecosystems, exemplified by Awair's platform correlating air quality data with respiratory symptoms for 3.4 million households. These comprehensive monitoring solutions have fundamentally shifted healthcare from episodic interventions to continuous optimization, with measurable improvements in clinical outcomes documented across 178 published studies involving 12.7 million participants.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America Dominates Smart Home Healthcare Through Innovation, Connectivity, Reimbursement

The smart home healthcare market in North America holds the largest global share, powered by a deep-rooted digital health ecosystem, rich reimbursement pathways, and nationwide broadband coverage. Roughly 48.9 million U.S. households now use at least one connected health device, while remote patient-monitoring enrollments have climbed to 12.3 million individuals. Federal policy fuels this scale: the Centers for Medicare & Medicaid Services reimburse more than seventy remote-care codes, and the FCC’s Connected Care Pilot has allocated US$ 566 million to rural broadband that underpins wireless medical devices. Core end-user blocs include 31.8 million seniors aging in place, working-age patients with employer wellness plans, and tech-savvy caregivers managing family dashboards. Diabetes, heart failure, chronic obstructive pulmonary disease, and Alzheimer’s disease together generate about 60.7 million connected readings per day on platforms such as Abbott’s LibreView and Apple Health. This data firehose already prevents an estimated 0.48 million rehospitalizations each year, underscoring North America’s structural lead.

Europe Advances Smart Home Healthcare Balancing Privacy, Reimbursement, Cross-Border Integration

Europe follows with a cohesive but privacy-conscious smart home healthcare market, where stringent General Data Protection Regulation rules shape platform design. Adoption reached 29.4 million households in 2024, accelerated by Germany’s DiGA Fast-Track—which placed fifty-plus “app on prescription” solutions under statutory insurance—and France’s MaSanté portal linking 5.6 million citizens to shared electronic records. Elderly solo dwellers supported by state allowances, multimorbid patients inside national chronic-care pathways, and insurers rewarding connected-device use make up the principal user cohorts. Cardiovascular disease dominates demand, generating 7.2 million monthly ECG uploads through Withings and AliveCor devices, followed by type 2 diabetes and sleep apnea. High-speed broadband penetration across the United Kingdom, Germany, and the Nordics lets hospitals ingest home-captured vitals in real time, shaving an estimated US$ 10.9 billion from acute-care budgets in the past year—proof that Europe’s data-driven oversight can translate into measurable savings and better outcomes.

Asia Pacific Drives Smart Home Healthcare Growth With Governmental Support

Asia Pacific is the fastest-growing node of the smart home healthcare market, propelled by dense urban populations, low-cost sensor manufacturing, and assertive public-sector mandates. Japan’s Silver ICT program subsidized 0.93 million eldercare IoT kits in 2024, while China’s Healthy Aging Blueprint networked 62,500 community clinics to Huawei’s Health-Cloud for AI analytics. Uptake spans middle-class urban families tracking hypertension, rural elders linked via 5G hubs, and corporate wellness users of Xiaomi or Samsung biosensors. Stroke, chronic kidney disease, and COPD now account for 14.8 million cloud-logged spirometry and blood-pressure sessions every month. India’s Ayushman Bharat Digital Mission is onboarding an additional 0.456 million tele-homecare users weekly, reflecting the region’s breakneck scale. By pairing AI triage engines with sub-US$ 50 wearables, providers have cut emergency transport calls by 0.186 million annually, positioning Asia Pacific as the next engine of expansion for the global smart home healthcare market.

Top Players in Global Smart Home Healthcare Market:

- Apple Inc.

- AT&T Inc.

- BSH Home Appliances Group

- Companion Medical

- E & A Engineering Solutions Private Limited

- F. Hoffmann-La Roche Ltd

- Fitbit Inc.

- General Electric Company

- Health Care Originals.

- Koninklijke Philips N.V.

- Kul Systems

- Medical Guardian LLC

- Medtronic

- Qualcomm Technologies, Inc.

- Resideo Technologies, Inc.

- Samsung Electronics Co. Ltd.

- Other Prominent Players

Market Segmentation Overview:

By Technology

- Wired

- Wireless

By Products

- Testing, Screening and Monitoring Products

- Therapeutic Products

- Mobile Care Products

By Service

- Skilled Nursing Services

- Rehabilitation Therapy Services

- Hospice and Palliative Care Services

- Unskilled Care Services

- Respiratory Therapy Services

- Infusion Therapy Services

- Pregnancy Care Services

By Application

- Fall Prevention and Detection

- Health Status Monitoring

- Nutrition or Diet Monitoring

- Memory Aids

By Indication

- Diabetes

- Respiratory Diseases

- Pregnancy

- Mobility Disorders

- Hearing Disorders

- Cancer

- Wound Care

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 27.46 Billion |

| Expected Revenue in 2033 | US$ 194.51 Billion |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Bn) |

| CAGR | 24.3% |

| Segments covered | By Technology, By Products, By Service, By Application, By Indication, By Region |

| Key Companies | Apple Inc., AT&T Inc., BSH Home Appliances Group, Companion Medical, E & A Engineering Solutions Private Limited, F. Hoffmann-La Roche Ltd, Fitbit Inc., General Electric Company, Health Care Originals., Koninklijke Philips N.V., Kul Systems, Medical Guardian LLC, Medtronic, Qualcomm Technologies, Inc., Resideo Technologies, Inc., Samsung Electronics Co. Ltd., Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Choose License Type

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |