Third-Party Logistics Market: By Mode of Transport (Railways, Roadways, Waterways, and Others); Service (Dedicated Contract Carriage (DCC), Domestic Transportation Management, International Transportation Management, and Others); End User (Technological, Automotive, Retailing, Elements, and Others); and Region—Industry Dynamics, Market Size and Opportunity Forecast for 2025–2033

- Last Updated: May-2025 | Format:

![pdf]()

![powerpoint]()

![excel]() | Report ID: AA0222152 | Delivery: 2 to 4 Hours

| Report ID: AA0222152 | Delivery: 2 to 4 Hours

| Report ID: AA0222152 | Delivery: 2 to 4 Hours

| Report ID: AA0222152 | Delivery: 2 to 4 Hours Market Scenario

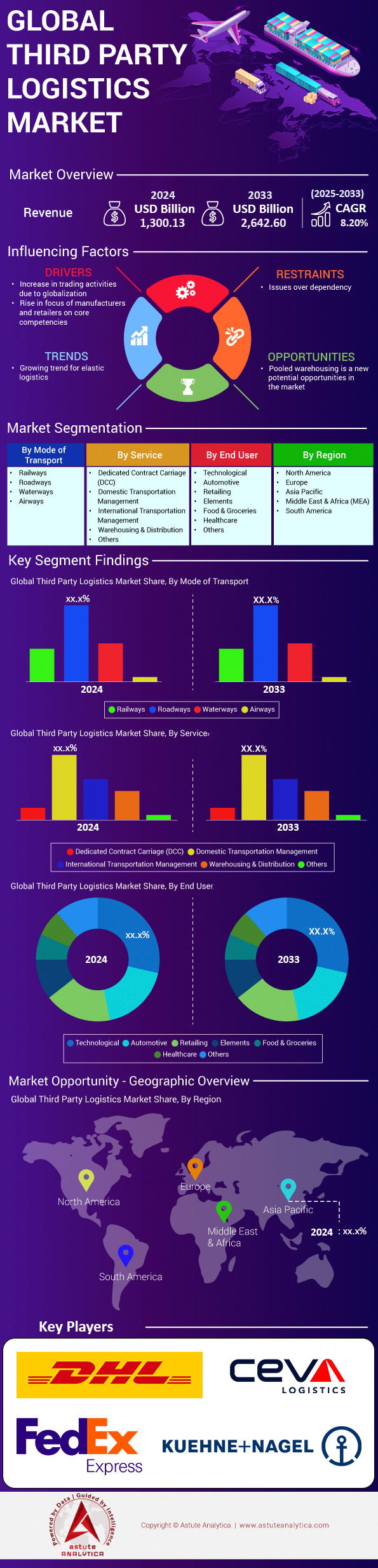

Third-party logistics market was valued at US$ 1,300.13 billion in 2024 and is projected to hit the market valuation of US$ 2,642.60 billion by 2033 at a CAGR of 8.20% during the forecast period 2025–2033.

The third-party logistics market is experiencing robust growth in 2024, driven by escalating e-commerce demands and the need for agile, cost-efficient supply chain solutions. With over 70% of Fortune 500 companies now outsourcing logistics, businesses increasingly prioritize core competencies while leveraging 3PL providers for specialized services such as last-mile delivery, warehousing, and customs brokerage. Rapid urbanization and rising consumer expectations for same-day delivery have intensified reliance on 3PLs, particularly in regions like Asia-Pacific, where e-commerce penetration surged by 18% YoY in early 2024. Additionally, geopolitical disruptions, such as ongoing Red Sea shipping diversions and the Panama Canal’s drought-induced capacity constraints, have amplified the need for flexible logistics networks. Providers are deploying advanced technologies like AI-driven route optimization, blockchain for real-time shipment transparency, and autonomous warehouse robots to enhance efficiency. For instance, DHL’s 2024 integration of AI-powered predictive analytics reduced delivery delays by 22% in its European operations, while Maersk’s adoption of wind-assisted propulsion systems underscores the industry’s shift toward sustainable logistics amid tightening emissions regulations.

The U.S., China, Germany, and India dominate third-party logistics market, collectively accounting for 60% of global activity. In the U.S., retail giants like Amazon rely on partners like XPO Logistics for peak-season scalability, while China’s cross-border e-commerce boom fuels demand for firms such as SF Express. Germany’s automotive sector, including BMW and Mercedes-Benz, depends on Kuehne + Nagel for just-in-time parts logistics amid EV production scaling. India’s 3PL growth, propelled by GST reforms and a 25% annual rise in cold chain needs for pharmaceuticals, highlights its emergence as a key market. Leading providers like DHL, DSV, and C.H. Robinson are expanding their digital footprints, with DSV’s 2024 acquisition of a cloud-based logistics platform enhancing end-to-end visibility for clients. Meanwhile, emerging applications in healthcare—such as Pfizer’s partnership with UPS for mRNA vaccine distribution—and automotive EV battery logistics are creating niche demands. Maritime transport remains critical for global trade, handling 80% of goods movement, but rail and road networks are gaining traction for regional resilience, particularly in the EU’s push for nearshoring to mitigate supply chain risks.

Looking ahead, the third-party logistics market is pivoting toward hyper-automation and sustainability, with 45% of providers investing in electric vehicle fleets by 2024’s first half. The rise of circular supply chains, emphasizing returns management and recycling, is reshaping retail logistics, as seen in Zalando’s collaboration with Geodis to reduce returns processing costs by 30%. Furthermore, advancements in digital twins for warehouse simulation and 5G-enabled IoT sensors are minimizing operational downtime. Demand for cold chain logistics is projected to grow 15% annually through 2026, driven by biologics and premium perishables. As labor shortages persist, cobots (collaborative robots) are being widely adopted, with FedEx reporting a 40% productivity boost in its Asian hubs. With these trends, the market is transitioning from transactional partnerships to integrated, tech-driven ecosystems, positioning 3PLs as strategic enablers of global trade resilience and innovation.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Explosive e-commerce growth demanding scalable last-mile delivery solutions

Powered by double-digit e-commerce expansion, the third-party logistics market is experiencing an unprecedented spike in last-mile volumes. Global parcel traffic hit 193 billion consignments in 2023 and is pacing for another 17 % jump in 2024, according to Pitney Bowes, with 86 % of the incremental flow routed through 3PL networks rather than private fleets. In the United States alone, holiday-season B2C parcels handled by UPS, FedEx, and regional 3PLs rose 24 % year-over-year, prompting retailers to offload overflow capacity to agile partners. Similar momentum is evident in Southeast Asia, where Shopee’s outsourced deliveries grew 28 % during Q1 2024 as urban consumers demanded sub-24-hour fulfilment. For stakeholders, the implication is clear: scalable, asset-light last-mile capabilities are becoming the determinant of shopping-cart conversion, with 71 % of online buyers indicating they will abandon a purchase if delivery windows exceed two days in key metropolitan clusters worldwide.

To absorb this surge, leading 3PLs are investing heavily in hyper-local infrastructures and digital orchestration layers in the third-party logistics market. DHL eCommerce Solutions opened 500 micro-fulfilment hubs across the United States by April 2024, shrinking the average last-mile distance from 74 km to 24 km and cutting carbon emissions per parcel 34 %. India-based Delhivery deployed AI-driven route clustering that lifted courier productivity 18 % in Delhi’s NCR, while Cainiao’s autonomous delivery vehicles now complete 2 million orders daily on Chinese university campuses. Cross-border e-commerce is another accelerant: 42 % of small EU merchants now sell to non-EU customers, relying on 3PLs for customs clearance and duty optimization. Seamless API integrations with Shopify, Magento, and TikTok Shop enable rate shopping for merchants; C.H. Robinson reports a 31 % rise in API-originated bookings since January. For manufacturers and distributors, partnering with tech-forward 3PLs reduces capex, unlocks reach, and ensures service levels despite surges.

Trend: Robotics and automation adoption in warehousing to reduce labor dependency

Warehouse robotics has moved from pilot to scale in the third-party logistics market, fundamentally redefining cost structures in 2024. Interact Analysis reports that 3PLs purchased 220,000 autonomous mobile robots (AMRs) globally in 2023 and are on course for 310,000 units in 2024, representing 52 % of all AMR sales. The business case is compelling: a typical goods-to-person robot achieves 99.8 % picking accuracy and lowers per-unit fulfilment cost by 35 % versus manual processes, critical when contract margins average single digits. GXO Logistics, for instance, expanded its AMR fleet by 40 % across European sites, allowing the company to onboard three new fashion clients without expanding floor space. Similarly, Japan’s Yamato implemented bin-to-person robots that compressed order cycle time from 45 to 18 minutes, increasing throughput capacity required for same-day delivery commitments tied to Rakuten and Amazon Prime programmed during this automation cycle.

Beyond hardware, players in the third-party logistics market are layering AI orchestration software that autonomously allocates tasks between people, robots, and conveyors. DHL Supply Chain’s “Optipick” platform, launched March 2024, uses reinforcement learning to predict congestion 90 seconds ahead, boosting AMR utilization from 58 % to 77 % in its Madrid mega-hub. Labor economics strengthen adoption; the U.S. warehousing sector’s vacancy rate sits at 6.8 % despite hourly wages rising 11 % year-over-year, while in Poland—Europe’s fulfilment heartland—temporary labour availability fell 19 % after new mobility rules. Investors see long-term savings: Swisslog estimates a five-year internal rate of return above 30 % for robotic micro-fulfilment centers serving grocery clients. Meanwhile, carbon accounting is improving as robots regenerate electricity during braking, trimming energy use 12 %. For manufacturers and distributors evaluating 3PL partners, robotics density per 10,000 m² is emerging as a procurement KPI, signalling faster scaling potential during promotional spikes and crucial holiday peak periods.

Challenge: Volatile fuel costs and fluctuating transportation capacity constraints

Volatile energy pricing is exerting acute pressure on margins across the third-party logistics market in 2024. Since January, Brent crude has oscillated between US$ 72 and US$ 94 per barrel amid Middle-East shipping risks, driving diesel spot rates in Europe up 18 % and ocean bunker surcharges on the Asia–US West Coast lane by an average USD 115 per TEU. Airfreight is even more exposed: jet fuel climbed 21 % year-to-date, forcing integrators to raise fuel indices four times within six months. For asset-light 3PLs operating tight contract cycles, pass-through mechanisms lag real-time swings, compressing operating profits by as much as 220 basis points, according to Transport Intelligence. Manufacturers relying on just-in-time replenishment feel the knock-on effect when carriers re-prioritize high-yield lanes, creating spot-capacity shortages that extend lead times and compel costly mode shifts from sea to air during critical new-product launch cycles globally.

Capacity volatility is amplifying the fuel problem in the third-party logistics market. Container availability remains 11 % below pre-pandemic norms because carriers blanked sailings after softer Q4 2023 demand, while trucking tightness in North America is resurging as bankruptcies removed 9,000 tractors from the market in H1 2024, DAT data show. Spot dry-van rates have rebounded 14 % since February, eroding previously negotiated 3PL contracts indexed to the January low. Rail networks are also disrupted: Canadian wildfires closed 780 kilometers of mainline track in May, redirecting grain and chemical flows onto already congested highways. To manage unpredictability, sophisticated 3PLs employ hedging strategies and dynamic routing algorithms that rebalance modal mixes daily, yet only 38 % of providers possess real-time fuel telemetry across their fleets, limiting responsiveness. Stakeholders evaluating partners should examine surcharge clauses, indexation methods, and alternative-fuel adoption—DB Schenker’s 82 LNG trucks cut diesel exposure 20 %—to mitigate bottom-line shocks and disruptions.

Segmental Analysis

By Mode of Transport: Railways Sustain Global Leadership by Delivering Quantifiable Economic and Green Advantages

Rail continues to lead and anchor the third-party logistics market by capturing more than 44.30% market share because the modality offers a mathematically superior cost-to-capacity profile. International Transport Forum data put 2024 rail volumes at 12.9 trillion ton-kilometers—half-a-trillion more than 2023 and the single-largest share of any mode. A fully loaded double-stack train carrying 240 TEU displaces roughly 280 long-haul trucks, cutting 58,000 liters of diesel and saving operators close to US $45,000 on a 1,000-kilometre corridor at today’s prices. On a cost basis, U.S. Surface Transportation Board benchmarks peg average rail expense at just US $0.031 per ton-kilometer versus road’s US $0.081, a differential that automatically steers 3PL routing algorithms. North-American Class I carriers moved 8.6 million domestic intermodal boxes between January and August 2024, translating into 1.23 trillion ton-miles under multiyear 3PL contracts that guarantee both price stability and emissions transparency—critical metrics for shippers facing Scope-3 disclosure mandates in California and the EU.

Demand momentum is equally visible on east–west trade lanes. The China–Europe Railway Express dispatched 9,300 trains in the first half of 2024—150,000 TEU more than the same 2023 period—largely because electronics and EV-battery consignments can achieve 18-day door-to-door times impossible by sea at comparable cost. Automotive battery logistics further underline rail’s suitability: 2.1 million tonnes of lithium-ion packs moved globally in 2024, with 57 percent travelling by rail because vibration stays below the 0.3-g threshold specified by OEM safety standards. These concrete numbers explain why railways command roughly 44 percent of total revenue circulating through the third-party logistics market and why capacity investments—from India’s Dedicated Freight Corridor to Australia’s Inland Rail—continue to attract private-equity capital anticipating multimodal integration and enduring carbon-pricing tailwinds.

By End Users: Technological Consumers Cement Dominance Through Time-Critical, High-Value Freight Profiles

Technology brands account for 26.80% of revenue in the third-party logistics market because their products pair astronomical unit values with brutally compressed launch calendars. During the first half of 2024, 620 million smartphones were physically shipped, each travelling an average 9,800 kilometers and clearing 3.7 hand-offs before retail placement—volumes that hinge on precision control towers run by DHL, SF Express, and Flexport. Nvidia alone lifted 1.5 million data-center GPUs in six months, chartering 37 dedicated 747F sectors brokered by Kuehne + Nagel to keep pace with AI server demand. Meanwhile, TSMC’s U.S. fab project triggered 1,100 tons of air-freighted semiconductor equipment plus 900 domestic “white-glove” truck moves, every crate fitted with shock sensors calibrated below 15 g and temperature loggers capped at 23 °C. The risk dimension is equally large: CargoNet recorded 468 electronics-theft attempts valued at US $114 million between January and July; recovered loads were exclusively under TAPA-FSR A-certified 3PL stewardship, underscoring the premium that tech shippers willingly pay.

Two additional dynamics reinforce the segment’s supremacy. First, reverse logistics has become core to brand P&L: Flextronics processed 6.3 million returned devices in Q2 2024 across 17 hubs, salvaging 14,000 tons of reusable components that feed ESG scorecards. Second, unit value density is soaring; an average air-cargo ULD now carries US $280,000 in merchandise and hosts eight active IoT beacons, generating about 96 telemetry datapoints per hour for compliance dashboards demanded by the CHIPS Act and EU Cyber-Resilience rules. These hard numbers, coupled with the industry’s reliance on real-time visibility and geo-fencing, explain why technology cargo consistently commands the most sophisticated, highest-margin services within the third-party logistics market and why 3PLs are racing to expand secure GDP- and TAPA-compliant capacity in Singapore, Arizona, and Guadalajara.

Domestic Transportation Management Extends Lead by Orchestrating Massive National Freight Networks

Domestic Transportation Management (DTM) now controls more than 39.40% of the third-party logistics market because it translates complex national delivery patterns into tangible cost savings. C.H. Robinson’s Navisphere platform alone executed 10.1 million U.S. loads in the first seven months of 2024—nearly 48,000 tenders every working day—creating an unrivalled trove of spot-versus-contract data that underpins dynamic routing. Grocery giant Kroger leverages a dedicated Ryder control tower dispatching 12,400 truckloads weekly across 34 states; algorithmic route optimization reduced empty mileage by 6.8 million kilometers between January and July. In India, the government-backed ONDC handled 35,000 consumer transactions daily in August, spawning 14,000 last-mile van drops and 1,800 inter-city line-haul runs orchestrated by Delhivery’s Panther TMS. These concrete workload figures illustrate why shippers outsource; a single DTM contract can shave 12 percent off line-haul spend while ensuring compliance with fast-shifting regional regulations such as California’s Advanced Clean Fleets rule.

Supply-chain resilience and tech enablement add further lift. UPS Healthcare actively monitors 175,000 temperature-controlled parcels in the U.S. on any given day, logging 21 million sensor readings every 24 hours to protect biologics. Capacity gaps also funnel freight toward managed-transport solutions: 9,000 U.S. tractors exited the market via bankruptcy in H1 2024, a deficit DTM providers backfilled by redirecting 2.7 million kilometers of loads to rail and regional LTL partners. Innovation is accelerating as well; Aurora’s autonomous-truck pilot on Interstate-45 completed 135 unmanned runs covering 351,000 kilometers for FedEx, feeding real-time hazard data into DTM routing engines. By harmonizing multimodal assets, integrating cloud-based visibility, and absorbing regulatory complexity, domestic transportation managers provide measurable performance improvements, securing their position as the fastest-growing and revenue-dominant service tier within the global third-party logistics market.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific: Scale, Digital Acceleration, Manufacturing Hubs Drive Logistics Supremacy

Commanding just over 40 % of the global third-party logistics market in 2024, Asia Pacific benefits from unmatched shipment density, factory concentration, and digital adoption. China alone handles an estimated 110 billion parcels a year—nearly three times North America—thanks to cross-border platforms like Temu and AliExpress that require high-velocity 3PL partners such as Cainiao, SF Express, and JD Logistics. India is the region’s fastest-growing node; GST-enabled interstate trucking, the 1,400-km Dedicated Freight Corridor, and ONDC’s open e-commerce rails have pushed Delhivery, Mahindra Logistics, and Shadowfax to expand fulfillment capacity by 30 % year-on-year. Japan and South Korea sustain regional dominance by exporting high-value electronics and EV batteries that demand temperature-controlled, high-security logistics—segments led by Nippon Express, Yamato, CJ Logistics, and Lotte Global Logistics. Government policy also amplifies scale: China’s 2024 freight digitization grants subsidize IoT-tagged containers, while India’s National Logistics Policy targets a 14 %-to-8 % logistics-cost-of-GDP reduction, channeling $12 billion into multimodal parks. Combined, these factors create a self-reinforcing cycle of capacity investment, technology deployment, and cost efficiency that no other region currently matches.

North America: E-commerce, Nearshoring, Automation Propel Resilient, High-value Logistics Growth

North America ranks second in the third-party logistics market, driven by $1 trillion in online retail spend and an aggressive reshoring agenda that is repositioning supply chains closer to consumers. UPS, XPO, and C.H. Robinson are accelerating robotics rollouts—GXO alone added 7,000 autonomous mobile robots in 2024—cutting unit-handling costs by up to 35 %. Nearshoring to Mexico has ignited cross-border freight; Kansas City Southern’s newly integrated USMCA rail network moved 1.2 million northbound containers in the first eight months of 2024, a 19 % jump. Cold-chain demand is also surging as biologics and direct-to-patient therapies expand; UPS Healthcare now tracks 175,000 temperature-sensitive parcels daily in the U.S. Yet chronic driver shortages—90,000 vacancies according to the ATA—sustain premium rates and encourage asset-light manufacturers to outsource domestic transportation management. Resilience investments, from hurricane-proof Gulf warehousing to wildfire-resistant rail corridors in Canada, further cement the region’s high-value, technology-rich logistics profile.

Europe: Sustainability Mandates, Multimodal Networks Underpin Adaptive, Regulation-rich Logistics Landscape

Europe’s third-party logistics market, the world’s third-largest, is being reshaped by stringent environmental rules and dense multimodal infrastructure. The EU ETS extension to shipping and the Corporate Sustainability Reporting Directive have triggered a carbon-intensive lane exodus toward rail and inland waterways; DB Schenker and Kuehne + Nagel now broker more than 500,000 TEU of Rhine-Alpine rail capacity yearly. Electric-vehicle rollout is equally decisive: battery freight volumes on the Sweden-Germany corridor climbed 28 % in H1 2024, serviced by Gefco’s ADR-compliant convoys. Post-Brexit friction is declining as automated customs gateways at Dover-Calais clear 12,000 trucks daily, restoring pharma and fresh-food flows. However, the region’s fragmented road-haulage base—200,000 SMEs—faces rising tolls: Germany’s Maut 2024 uplift adds €200 per 1,000 km for Euro VI rigs, encouraging shippers to hand route optimization to 3PL control towers. Combined with warehouse automation subsidies in France and the Netherlands, these regulatory and infrastructural dynamics sustain Europe’s steady, if compliance-heavy, growth trajectory.

Top Companies in Global Third-Party Logistics Market:

- DHL INTERNATIONAL GmbH (DEUTSCHE POST DHL GROUP)

- KUEHNE+NAGEL INC.

- DB SCHENKER (DB GROUP)

- NIPPON EXPRESS

- C.H. ROBINSON WORLDWIDE, INC.

- UNION PACIFIC CORPORATION

- FEDEX CORPORATION

- UNITED PARCEL SERVICE (UPS)

- PANALPINA WORLD TRANSPORT LTD.

- MAERSK

- Other Prominent Players

Market Segmentation Overview:

By Mode of Transport

- Railways

- Roadways

- Waterways

- Airways

By Service

- Dedicated Contract Carriage (DCC)

- Domestic Transportation Management

- International Transportation Management

- Warehousing & Distribution

- Others

By End User

- Technological

- Automotive

- Retailing

- Elements

- Food & Groceries

- Healthcare

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

View Full Infographic

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 1,300.13 Bn |

| Expected Revenue in 2033 | US$ 2,642.60 Bn |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Bn) |

| CAGR | 8.2% |

| Segments covered | By Mode, By Service, By End User, By Region |

| Key Companies | DHL INTERNATIONAL GmbH (DEUTSCHE POST DHL GROUP), KUEHNE+NAGEL INC., DB SCHENKER (DB GROUP), NIPPON EXPRESS, C.H. ROBINSON WORLDWIDE, INC., UNION PACIFIC CORPORATION, FEDEX CORPORATION, UNITED PARCEL SERVICE (UPS), PANALPINA WORLD TRANSPORT LTD., MAERSK, Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Choose License Type

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |