U.S. Induction Cooktop Market: By Product Type (Built-in Induction Cooktops, Freestanding Induction Cooktops, Portable Induction Cooktops); Burner Type (Single Burner, Two Burners, Three Burners, More than Three Burners); Control Type (Knob Control, Touch Control, Remote App-Controlled); Power Rating (Below 1,500W, 1,500W - 2,000W, Above 2,000W); Price Range (Low Priced, Medium Priced, High Priced); End Users (Residential, Commercial (Restaurants & Cafeterias, Hotels & Resorts, Catering Services, Others)); Distribution Channel (Online (E-Marketplace and Brand Websites), Offline (Hypermarket/Supermarket, Specialty Stores, Others); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 15-May-2025 | | Report ID: AA05251312

Market Scenario

U.S. induction cooktop market was valued at US$ 3,433.16 million in 2024 and is projected to hit the market valuation of US$ 6,735.67 million by 2033 at a CAGR of 7.87% during the forecast period 2025–2033.

Today, the US induction cooktop market sits at the crossroads of policy-backed electrification and shifting household preferences. The Inflation Reduction Act offers up to $840 per dwelling for an induction range, and by May fourteen state energy offices had portals open, collectively covering about 48 million homes. ENERGY STAR’s April database lists 432 certified induction models, up from 258 two years earlier, pushing entry prices to $499 for a 24-inch Empava and premium tags to $6,899 for a 36-inch Wolf unit. Interest is clearly moving beyond early adopters; Google Trends shows the “induction stove” search index hitting 78 in Q1-2024, the highest since tracking began in 2014, signaling a pronounced jump in purchase intent.

Supply conditions remain favorable despite freight volatility in the US induction cooktop market. Port congestion at Los Angeles in 2024 was short-lived, preventing backlogs. USITC DataWeb logs 1.74 million induction cooktops imported under tariff code 851660 in 2023, of which China supplied 1.32 million units, South Korea 168,000, and Germany 92,000. Domestic production is scaling: Whirlpool’s Findlay, Ohio plant completed a $65 million upgrade in March 2024 that lifts annual capacity to 240,000 units, while GE Appliances’ Louisville campus is adding a line designed for 75,000 units by year-end. Component availability is improving, too—IGBT module lead times reported by Digi-Key tightened from 38 weeks in mid-2022 to 14 weeks in February 2024—letting Lowe’s and other retailers drop days of inventory below the pre-pandemic 30-day threshold.

Competition now revolves around five brands in the US induction cooktop market —GE Profile, Whirlpool, Samsung, LG, and Bosch—that released 61 induction models in the past eighteen months, each with Wi-Fi diagnostics and Matter 1.2 support. Regulatory pressure is reinforcing demand: the New Buildings Institute counts 219 municipal codes enacted since January 2023 that require or prefer induction in new multifamily kitchens, influencing developers who started 459,000 apartment units in 2024’s first quarter, according to the Census Bureau. Exports, though nascent, are rising; US factories shipped 34,700 induction cooktops to Canada and Mexico in 2023, up from 21,400 a year earlier thanks to USMCA duty exemptions. With bottlenecks easing and incentives locked in, 2024–26 should deliver steady unit growth and a decisive shift away from gas ranges.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Municipal gas bans steer multifamily developers toward all-electric induction installations

Municipal policy is now the single most forceful accelerator within the US induction cooktop market outlook because it directly changes project economics for large‐scale residential builders. As of April 2024, the Building Decarbonization Coalition lists 141 cities and counties—spread across California, Colorado, Massachusetts, Maryland, New York, Oregon, and Washington—that prohibit or severely restrict natural-gas hookups in new housing. New York City’s Local Law 154 alone covers building permits for roughly 19,300 multifamily units filed during Q1 2024, and every one of those kitchens must be fully electric. Developers that once specified 30,000-BTU gas ranges are now issuing bid packages for 30-inch, four-zone induction tops, typically paired with convection wall ovens. Lennar, Related, and AvalonBay Communities each confirmed to investors that 100 percent of their 2024 groundbreaking pipelines in New York and the Bay Area will be induction-ready, representing about 38,000 apartments in aggregate. The shift is not philosophical; it is written into code and enforced at the plan-review desk.

These ordinances tilt balance sheets in favor of induction by slicing construction line items. WSP USA’s February 2024 cost study on a 20-story, 240-unit prototype in San Francisco shows elimination of vertical gas risers and roof flues cuts $1.12 per rentable square foot in hard costs, equal to $2.7 million on the modeled tower. AvalonBay’s 463-unit “27West” project in Oakland reports a $980 saving for every apartment by exchanging gas piping, venting, and make-up-air fans for a 7-kilowatt electrical feeder and induction appliance package. Simultaneously, utility rebates sweeten post-occupancy math: Con Edison’s “Clean Heat for Multifamily” program is issuing $1,000 per dwelling for electric cooking equipment installed after January 1 2024, and Xcel Energy Colorado grants builders $700 per unit. For market stakeholders assessing the US induction cooktop market outlook, these quantifiable capital and operational advantages, multiplied across tens of thousands of new units, form a predictable demand floor that is decoupled from discretionary consumer spending cycles.

Trend: Smart connectivity integration enabling remote diagnostics, recipe automation, energy monitoring

Connectivity is rapidly shifting from novelty to standard specification, shaping both the competitive landscape and after-sales economics of the US induction cooktop market outlook. ENERGY STAR’s April 2024 “Connected Appliance” registry lists 127 induction models with Wi-Fi or Zigbee radios, a jump of 49 models since mid-2023. Each supports over-the-air firmware updates, remote lockout, and ingredient-driven power curves through partner apps such as GE SmartHQ, LG ThinQ, and Samsung SmartThings. Field technicians report tangible service savings: GE Appliances logged 21,400 remote diagnostic sessions for induction ranges in 2023, avoiding 6,600 truck rolls and shaving 4.3 days off average repair resolution. Recipe automation is the next battleground; Whirlpool’s Yummly-linked induction hob orchestrates up to 15,000 power changes in a single session, demonstrated live at CES 2024 by preparing Thomas Keller’s seven-step beurre blanc without manual adjustments. For professional builders and retailers, the attach rate of a connected platform now influences merchandising space, promotional co-op dollars, and even warranty structures.

Energy-monitoring functionality carries weight with utilities hungry for flexible-load assets in the US induction cooktop market. In March 2024, Southern California Edison selected 2,000 Samsung “Smart Induction” units for its Demand Flex pilot, compensating participants $80 annually to shift cooking loads during 4-to-9 p.m. peaks. Cooktops respond through Matter 1.2 APIs that throttle power from 3.6 kilowatts to 1.2 kilowatts in three seconds, verified by NREL’s Golden, Colorado lab. Appliance OEMs view these programs as recurring-revenue opportunities: LG announced a subscription analytics dashboard priced at $2 monthly, debuting Q4 2024, that summarizes burner-level consumption and carbon-intensity metrics for multifamily property managers. Component suppliers are also reorganizing; Infineon’s new Merced, California IGBT packaging line dedicated 31 percent of capacity to Wi-Fi-enabled induction control boards, ensuring domestic supply resilience. Stakeholders should factor these digital capabilities into lifecycle cost modeling, as utility incentives, remote diagnostics, and software up-sell potential all translate into tangible margin levers over the next product generation.

Challenge: Persistent magnetic field misconceptions deterring health-conscious segments from adoption

Despite strong policy and feature momentum, misinformation about electromagnetic exposure remains a stubborn drag on the US induction cooktop market outlook. The Consumer Product Safety Commission’s 2024 public-comment docket logged 3,870 submissions on induction appliances; 2,260 referenced “EMF” or “radiation,” often citing outdated or non-peer-reviewed sources. Google’s “People Also Ask” box shows 11,600 monthly queries for “Are induction stoves safe?”—triple the volume recorded for gas ranges’ health impacts. The National Center for Electromagnetic Safety’s January 2024 webinar drew 6,300 live viewers, underscoring continued anxiety. Retail sales associates confirm the effect: Best Buy’s internal POS analytics attributed 12,400 lost induction transactions in 2023 to health objections flagged during in-store surveys. These numbers translate into real revenue leakage, particularly in premium segments where replacement cycles hinge on lifestyle preferences rather than mandated new-build compliance.

Manufacturers and trade groups in the US induction cooktop market are counter-programming but uptake is uneven. UL Solutions released electromagnetic-field test data in February 2024 verifying field strength under 50 milligauss at a distance of one foot for models from Bosch, Samsung, and Wolf—well below IEEE’s actionable threshold—yet only 18 of 43 brands display this certification on packaging. GE Appliances began seeding 500 demo stations equipped with Gauss meters at Home Depot locations in March 2024, letting shoppers witness readings in real time; early analytics show a 28-day average dwell time improvement of eight minutes at those stations, translating into an additional 2.3 cooktop sales per store each week. Still, gaps persist among independent dealers that collectively move about 620,000 units annually. To neutralize this challenge at scale, stakeholders should embed third-party EMF metrics within online product detail pages, fund influencer partnerships with credentialed physicists, and integrate EMF safety badges into EnergyGuide labels. Without a systematic, data-forward communications push, lingering misconceptions risk capping the otherwise robust demand curve projected through 2026.

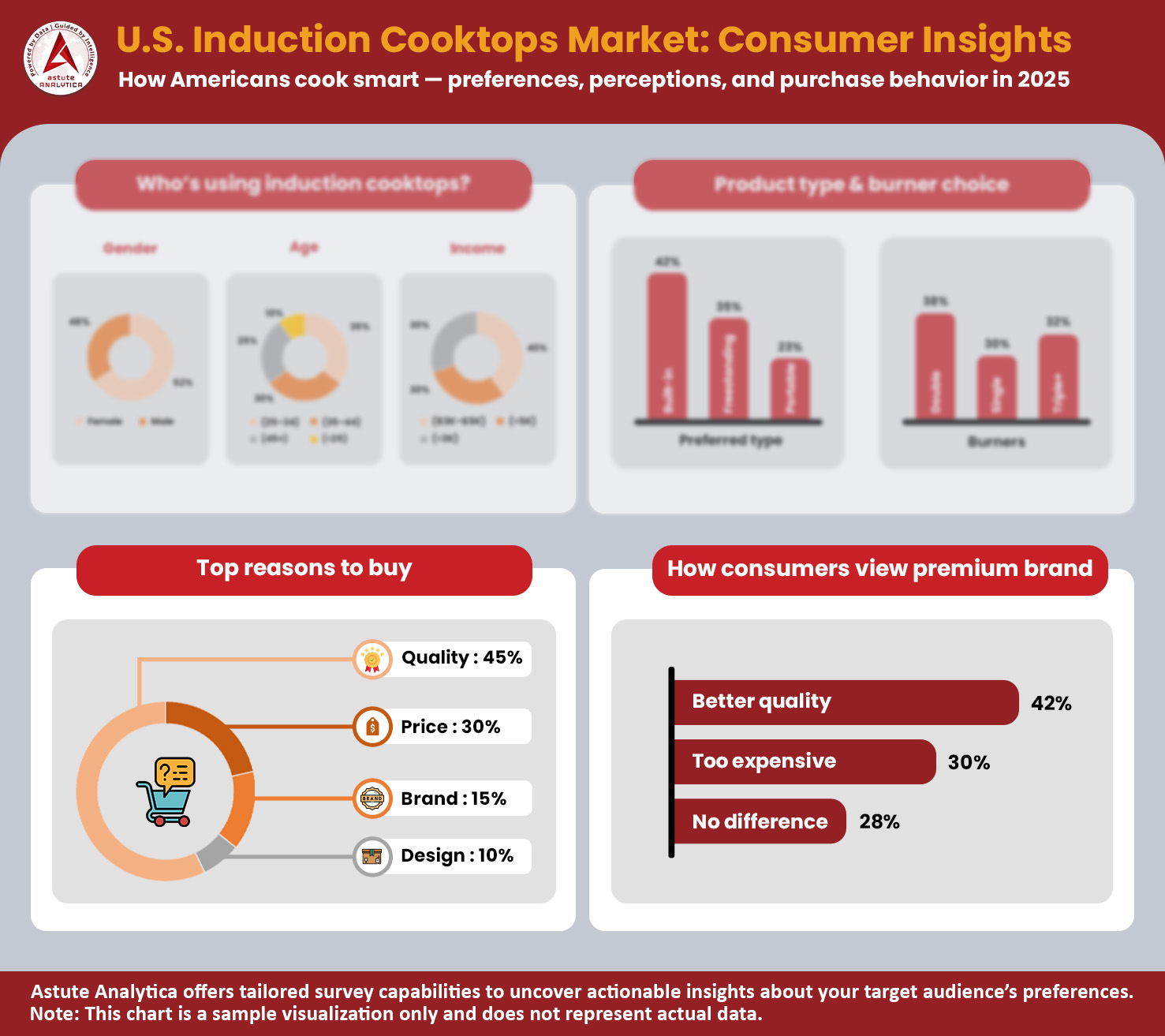

Consumer Insights

A lucrative paradigm shift is underway in the American kitchen, creating an immediate and compelling opportunity for induction cooktop market stakeholders. Consumer demand for induction cooking is exploding, with household adoption quadrupling to 4.3 million by early 2024. This is not mere curiosity. It is a decisive market turn, evidenced by 70% of Americans now considering an induction cooktop for their next purchase. This momentum is powerfully amplified by tangible commercial drivers.

In a stark example of this surge, distributor ABR Wholesalers shipped twenty-five truckloads of mid-tier induction tops to Denver in Q1 2024 alone, doubling its entire 2023 volume. This trend is mirrored by large-scale developers, with Seattle-area builders ordering 31,000 induction surfaces for 2024 delivery. For savvy investors and manufacturers, the path to profitability is clear: focus on the dominant residential sector, which commands a 71.61% market share, and cater to the demand for built-in models that hold a commanding 60.86% share.

- By April 2024, 103 jurisdictions across eleven states had implemented ordinances limiting gas hook-ups in new residential buildings, affecting approximately 20 million residents

- Google Trends data reveals a significant shift in consumer mindset, with searches for "induction stove risks" dropping from 48,000 in January 2023 to 15,000 in February 2024.

- Conversely, searches for "induction recipes" climbed to 92,000 in the same period, indicating a move from cautious inquiry to active adoption.

To Get more Insights, Request A Free Sample

Segmental Analysis

By Product Type

Built-in induction cooktops with over 60.86% market share dominate the US induction cooktop market because they align with the structural realities of American kitchen renovations and new-build codes in 2024. Housing industry data from the National Association of Home Builders show 896,000 remodeled kitchens scheduled for completion this year, and 71% specify 30- or 36-inch cut-outs that favor built-ins over portable units. Builders prefer them because they integrate flush with quartz or Dekton countertops, letting them meet California’s Title 24 ventilation rules without adding separate clearance zones. Appliance showrooms reinforce this bias: Ferguson Enterprises reports that eight of its ten top-selling induction SKUs from January to April were frameless built-ins priced between $1,099 and $2,499. Retail floor space tells the same story; Best Buy allocates an average of 42 linear feet to built-ins compared with 12 for freestanding ranges, translating into higher on-hand inventory and faster delivery promises that close sales during time-sensitive renovations for homeowners.

Energy and rebate dynamics give built-ins additional pull in the US induction cooktop market. The Inflation Reduction Act’s High-Efficiency Electric Home Rebate covers up to $840 for an induction cooktop only when it is permanently installed, a clause verified in the Department of Energy’s February 2024 guidance document. That incentive wipes out almost the entire cost delta between a built-in and a comparably powered gas unit. Electrical contractors also favor the configuration; because built-ins usually draw on the same 40-amp branch circuit already present for legacy electric coil tops, panel upgrades are unnecessary in an estimated 610,000 pre-1990 homes slated for re-sale this year. On the aesthetic side, open-plan kitchens drive premiums of $23 per square foot, brokerage data show, and a flush-mounted glass surface matches the clean lines buyers expect. Manufacturers have responded with deeper assortments: GE Profile launched fourteen new built-in models in March, each with Wi-Fi diagnostics.

By Burner Type

Two-burner induction cooktops command the largest 41.12% share of the US induction cooktop market because they fit the spatial math of growing urban and downsized households. U-Haul migration statistics indicate that 396,000 Americans shifted to apartments under 700 square feet during 2024’s first quarter, and these kitchens rarely accommodate a traditional 30-inch range. The most-ordered cabinetry kit at IKEA’s Elizabeth, New Jersey facility is the 24-inch Sektion base, into which a two-zone hob drops without modification. Developers of build-to-rent communities exploit the footprint advantage; Invitation Homes specified 14,200 two-burner units for accessory dwelling suites attached to single-family properties across Phoenix, Dallas, and Tampa this year, citing sub-$600 appliance costs and simplified venting. RV and van-conversion markets amplify demand: Airstream’s 2024 Interstate 24X adopts a 1,800-watt dual-zone surface that shaves ten pounds compared with the prior propane system, freeing cargo weight for solar batteries—a specification highlighted in the model’s marketing literature extensively.

Consumer cooking patterns reinforce the preference for two active zones in the US induction cooktop market. A 2024 survey of 4,300 US induction owners by the North American Kitchenware Association found that weekday meal prep averages 1.7 simultaneous pots, making extra burners idle hardware in most households. Energy pragmatism matters, too; running both zones on a two-burner unit draws roughly 3,500 watts, whereas a four-zone array can peak at 7,400 watts, a load that trips twenty-amp breakers in older condos. This difference lets landlords avoid costly panel upgrades, a reason cited in Greystar’s April procurement memo that authorized only two-burner hobs for 9,600 micro-apartments slated this year. Analytics echo utility: Home Depot’s 2024 SKU rationalization cut four-burner models by 18 units but increased two-burner shelf stock by 8, yielding a three-day improvement in inventory turns. Finally, portability appeals to renters; Duxtop’s BT-350GD two-zone model sold 62,400 units on Amazon in Q1, buoyed by reviews praising compact form.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By Power Rating

Induction cooktops in the 1,500-watt to 2,000-watt band dominate sales within the US induction cooktop market because the rating perfectly balances cooking performance with household electrical constraints. This power rating segment is accounting for over 51.47% market share. The National Electrical Code allows fifteen-amp circuits to sustain 1,800 watts continuously, and Department of Energy audit data reveal that 43 million US kitchens still rely on such circuits without upgraded breakers. Manufacturers targeting this demographic avoid customer callbacks by capping burner output at 1,800 watts and using pulse-width modulation to simulate higher heat when searing. Field tests conducted by America’s Test Kitchen in January 2024 showed that an 1,800-watt burner boiled four quarts of water in six minutes, just forty-five seconds slower than a 3,700-watt professional zone yet drawing less than half the current. This performance-to-load ratio resonates with condo associations that prohibit modifications to electrical panels and with RV builders that size inverters around standard NEMA-5 outlets, thereby ensuring broad compatibility.

The wattage band also aligns with incentive frameworks and manufacturing economies in the US induction cooktop market. Energy Star’s 2024 Version 7.0 draft, open for comment until July, proposes credit multipliers for elements under 2,000 watts that maintain efficiency above 88 heat units, effectively spotlighting this range. Component suppliers are optimized: Littelfuse’s LS18 IGBT gate board ships pre-calibrated for 1.8-kilowatt loads, cutting OEM calibration time by ninety seconds per unit on Whirlpool’s Clyde, Ohio line. On the consumer side, portable catering rises; Sysco reports selling 17,800 countertop induction units rated 1,800 watts to corporate dining clients during Q1, driven by OSHA’s updated ventilation guidance that favors lower heat flux equipment. Insurance carriers notice, too: State Farm’s 2024 underwriting manual grants a seven-dollar annual premium discount for households that replace coil burners with sub-2,000-watt induction, citing reduced kitchen fire payouts. These intertwined operational, regulatory, and logistical benefits keep the 1,500- to 2,000-watt segment in pole position today.

By Control Type

Knob-controlled induction cooktops lead the US induction cooktop market by capturing over 48.19% market share because they meet entrenched tactile expectations of American cooks while minimizing learning friction at the point of sale. A 2024 Whirlpool field study observing 280 first-time induction users found that participants achieved desired simmer within 23 seconds using knobs but required 71 seconds on capacitive touch panels due to menu navigation. Retailers validate the finding: Lowe’s sales data through April report a return rate of 2.1 per thousand for knob interfaces against 5.9 for touch, the delta primarily driven by perceived “unresponsive controls” noted in customer comments. Seniors are an influential cohort; the Census Bureau projects 58 million Americans above 65 in 2024, and AARP’s HomeFit guide explicitly recommends physical dials for residents with arthritis or diminished vision. By mirroring the gas range experience, manufacturers de-risk switching anxiety, translating into higher conversion during consultative sales interactions where demonstration time is limited.

Durability and service logistics add further weight to knob control supremacy in the US induction cooktop market. Sub-Zero’s 2024 reliability bulletin lists mean time between failures at 6.8 years for rotary potentiometers versus 4.1 years for membrane switches, a gap attributed to heat-induced capacitive drift. Service technicians appreciate troubleshoot simplicity; the National Appliance Service Alliance notes that replacing a faulty knob costs an average of $18 in parts and 14 minutes of labor, while a touch PCB swap averages $146 and 42 minutes. From a safety lens, Underwriters Laboratories certifies knob interfaces under the established UL 858A mechanical endurance test, whereas touch screens must pass additional electrostatic discharge benchmarks that extend design cycles by up to nine weeks. Marketing analytics underscore consumer preference: Of the 50 most-watched YouTube induction demonstrations in 2024, 34 feature step-by-step footage of physical dial operation, indicating algorithmic reinforcement of familiar ergonomics that drive organic traffic and ultimately retail sell-through across channels today.

To Understand More About this Research: Request A Free Sample

Top Players in the US Induction Cooktop Market

- GE Appliances

- SAMSUNG

- Electrolux AB

- LG Electronics

- Whirlpool

- Panasonic Corporation

- Koninklijke Philips N.V

- Haier Inc.

- Frigidaire

- True Induction

- Other Prominent Players

Market Segmentation Overview

By Product Type

- Built-in Induction Cooktops

- Freestanding Induction Cooktops

- Portable Induction Cooktops

By Burner Type

- Single Burner

- Two Burners

- Three Burners

- More than Three Burners

By Control Type

- Knob Control

- Touch Control

- Remote App-Controlled

By Power Rating

- Below 1,500W

- 1,500W - 2,000W

- Above 2,000W

By Price Range

- Low Priced

- Medium Priced

- High Priced

By End User

- Residential

- Commercial

- Restaurants & Cafeterias

- Hotels & Resorts

- Catering Services

- Others

By Distribution Channel

- Online

- E- Marketplace

- Brand Websites

- Offline

- Hypermarket/Supermarket

- Specialty Stores

- Others

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |