Washed Silica Sand Market: By Fe Content (Less than 0.01% and More than 0.01%), Form (Coarse (0.1 mm to 2.0 mm), Medium (0.05 mm to 0.5 mm), Fine (0.025 mm to 0.1 mm), Ultra-Fine (0.06 mm - 0.01 mm)); Application (Glassmaking, Ceramic & Refractories, Industrial Abrasives, Metal Casting, Paints & Coatings, Water Filtration, Others); Distribution Channel (Online and Offline (Direct and Distributors/ Wholesalers); Industry (Construction and Building, Fiberglass and Glass, Foundry, Metallurgy, Sport And Leisure, Oil and Gas, Others); Region— Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 22-Oct-2025 | | Report ID: AA1223712

Market Snapshot

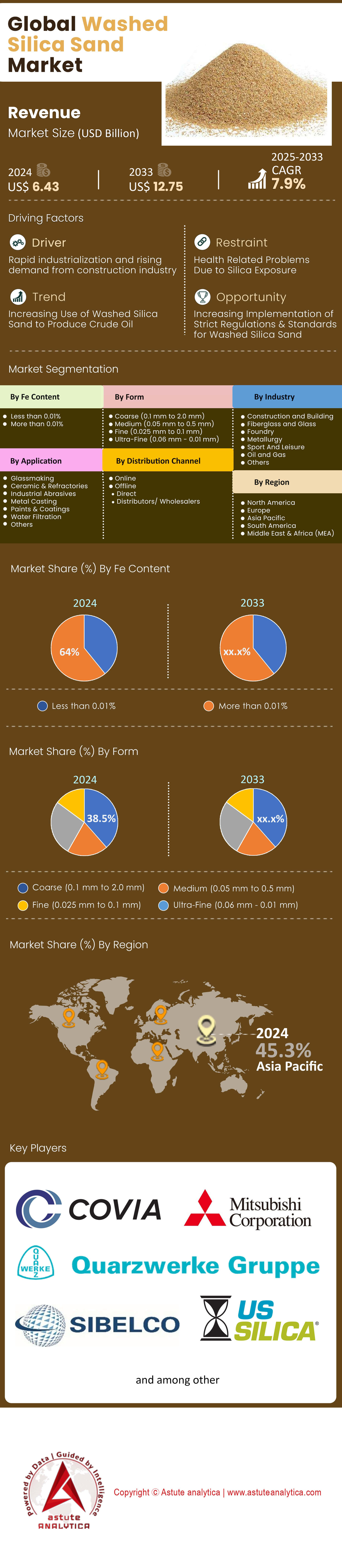

Washed silica sand market was valued at US$ 6.43 billion in 2024 and is projected to attain market valuation of US$ 12.75 billion by 2033 at a CAGR of 7.9% during the forecast period 2025–2033.

Key Findings Shaping the Market

- Based on Fe content, the segment with more than 0.01% iron (Fe) content is the most dominant, commanding a significant share of 64.0%.

- In terms of form, the coarse (0.1mm to 2.0mm) segment of the global market holds the highest share of 38.5%.

- In the application spectrum, the glassmaking segment dominates the washed silica sand market with the highest share of 37.4%.

- The fiberglass and glass industry segment holds the highest share in the market, accounting for 34.4%.

- Asia-Pacific region emerging as a dominant player by holding more than 45% of the market's revenue share.

The washed silica sand market is undergoing a significant evolution in 2025, driven by powerful new demand streams and a fundamental shift in industrial philosophy. While traditional pillars like general construction and glassmaking remain crucial, the market's most dynamic growth is now being dictated by the explosive expansion of digital infrastructure and a deepening commitment to circular economy models. The insatiable demand for concrete in data center construction is creating a new primary consumption channel, while innovations in glass recycling and sustainable industrial practices are reshaping the supply and demand landscape for high-purity silica.

The global construction market is projected to reach $17,045.95 billion in 2025, providing a strong foundational demand for washed silica sand market in concrete and building materials. This growth is increasingly influenced by the high-tech sector. The global construction of data centers, for example, is accelerating at an unprecedented rate, with 7.8 gigawatts of capacity currently under construction in North America alone as of mid-2025. These facilities are massive consumers of concrete; a single hyperscale data center campus can require upwards of 1 million metric tons of cement over its construction phase, a key ingredient of which is silica sand. In the U.S., data center construction is expected to consume approximately 247,000 metric tons of cement in 2025 alone.

The glass industry, a traditional cornerstone of silica sand demand, is also a focal point of transformation for the washed silica sand market. The global specialty glass market is expected to grow from $69.4 billion in 2025, driven by demand in electronics and renewable energy. The automotive sector's shift to electric vehicles (EVs) is a key factor, as lightweighting becomes critical for extending battery range. Advanced lightweight glass is a key component in this effort. Beyond new production, the industry is increasingly focused on sustainability. In Europe, new circular economy initiatives are being implemented in 2025 to increase the amount of recycled glass (cullet) used in manufacturing, which reduces the need for virgin raw materials, including silica sand. These programs aim to improve upon the fact that currently, over 80% of flat glass in Europe ends up in landfills.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Digital Revolution's Physical Footprint Fuels Unprecedented Demand

The single most powerful new driver for the washed silica sand market in 2025 is the physical build-out of the world's digital infrastructure, particularly the voracious construction of data centers. The surge in AI, cloud computing, and big data has created an insatiable demand for data processing and storage capacity, translating directly into a massive global construction boom. As of mid-2025, an additional 31.6 GW of data center capacity is in the planning stages in North America, a tenfold increase from just five years prior.

These are not ordinary construction projects; their scale and material intensity are immense. Data centers are concrete-heavy structures designed for security, thermal stability, and resilience. Inflation-adjusted spending on data centers has skyrocketed by nearly 850% over the last decade, with a 55% jump in 2024 alone. Projections show the number of data centers in the U.S. is on track to exceed 6,000 by 2027, up from 5,426 in early 2025. This expansion is creating concentrated hotspots of intense demand for washed silica sand market. States like Texas, Virginia, Arizona, and Georgia are poised to benefit from a wave of new projects between 2025 and 2027. The sheer volume is staggering, with forecasts predicting the U.S. will require nearly 1 million metric tons of cement for data center construction over the next three years. As a primary component of that concrete, washed silica sand is being pulled into this high-growth sector at a historic rate, providing a powerful and sustained demand driver for the foreseeable future.

Trend: The Circular Economy Reshapes the Glass Industry's Feedstock

A dominant trend reshaping the washed silica sand market in 2025 is the accelerating adoption of circular economy principles within the global glass industry. Driven by a combination of corporate sustainability goals, stringent government regulations, and a desire to reduce energy consumption, glass manufacturers are increasingly turning to recycled glass cullet as a primary raw material. This trend directly impacts the demand for virgin washed silica sand. Using cullet is one of the most effective ways to decarbonize glass manufacturing, as it melts at a lower temperature than raw materials, thereby reducing energy use and CO2 emissions.

Major corporations and regulatory bodies are putting ambitious targets in place, giving a significant push to the washed silica sand market growth. Pernod Ricard, for example, is targeting 50% post-consumer recycled content for its glass packaging by 2025. The flat glass industry in Europe is actively lobbying for a new Circular Economy Act in 2025 to create a more efficient market for secondary raw materials and support the dismantling and sorting of end-of-life glazing from buildings and cars. This is being enabled by technological advancements in automated sorting, which are improving the quality and purity of recycled cullet, making it suitable for a wider range of applications. While the current availability of high-quality cullet limits the decarbonization potential to about 10-15% at the industry level, the push for innovation and better collection infrastructure is relentless. This trend represents a paradigm shift, where a "waste" product is increasingly viewed as a valuable resource, creating a complex dynamic that both complements and competes with the traditional market for mined silica sand.

Restraint: Soaring Energy and Logistics Costs Squeeze Profit Margins

A significant restraint facing the washed silica sand market in 2025 is the dual pressure of volatile energy prices and escalating logistical costs. The process of mining, washing, grading, and drying silica sand is inherently energy-intensive. While industrial electricity prices in some regions like Europe are expected to see a slight ease in 2025, they remain structurally elevated compared to pre-crisis levels, putting sustained pressure on producers' operating costs. In North America, ongoing low inventories of distillate fuel oil, which includes diesel, have kept fuel prices high, directly impacting both stationary equipment and the transportation fleet essential for mining operations.

Compounding this issue are persistent challenges in the global supply chain. The cost of transporting a low-value, high-volume commodity like sand is a critical component of its final price. Fluctuations in shipping rates and logistical disruptions have introduced significant price volatility, particularly for exports and imports in the washed silica sand market. In September 2025, concerns over a slowing U.S. economy put downward pressure on crude oil prices, but this relief can be temporary and region-specific. These combined cost pressures squeeze profit margins for producers and can make long-distance transport economically unviable. This dynamic can, in some cases, lead to a preference for locally sourced, potentially lower-quality sand for applications where high purity is not essential, thereby capping the market potential for premium washed silica sand in certain regions and segments.

Segmental Analysis

By Fe Content

Within the washed silica sand market, the segment containing more than 0.01% iron (Fe) content remains the most dominant, holding a commanding share of 64.0%. This segment's prevalence is anchored in its extensive use in large-scale industrial applications where minor impurities do not compromise performance. The primary consumer is the construction sector, which requires vast quantities of sand for concrete, mortar, and other building materials. The growth in global construction output, expected to increase by 2.3% in 2025, ensures a stable and high-volume demand for this grade of sand. Furthermore, its application in producing certain types of container glass and in foundry castings, where absolute clarity or chemical purity is secondary to structural integrity, solidifies its market leadership.

In contrast, the segment with less than 0.01% Fe content is experiencing the most rapid growth in the washed silica sand market. This surge is directly linked to the expansion of high-technology manufacturing. The global semiconductor market, valued at $575.6 billion in 2025, is a key driver. The production of silicon wafers, the foundation of all microchips, demands silica of the highest possible purity. The establishment of new semiconductor fabrication plants, spurred by initiatives like the U.S. CHIPS Act, is creating concentrated demand for this premium material. Similarly, the specialty glass market, valued at over $37 billion in 2025, requires low-iron silica for applications like fiber optic cables, advanced display panels for the 1.5 billion smartphones expected to be sold in 2025, and high-transparency solar glass for the renewable energy sector.

By Form

Based on physical form, the coarse (0.1mm to 2.0mm) segment is the leader, commanding the highest share of 38.5% of the washed silica sand market. This segment's dominance is a result of its critical role in two major industries: construction and water filtration. In construction, coarse sand is a fundamental component of concrete, providing bulk and strength. Its grain size is optimal for creating durable and resilient building materials needed for the global infrastructure boom. Concurrently, its application in water filtration is a significant and growing demand driver. As nations invest heavily in water infrastructure to ensure safe drinking water, coarse silica sand is the preferred medium for granular bed filters in municipal and industrial treatment plants. In 2025, major funding is being directed toward upgrading these systems, such as the historic $547.1 million investment in Pennsylvania for clean water projects.

The coarse segment is also projected to grow at the highest rate in the washed silica sand market, propelled by these same powerful drivers. The global push to modernize aging water networks and build new treatment facilities to combat emerging contaminants will fuel demand. The U.S. alone is projected to see capital expenditures for water and wastewater treatment infrastructure grow from $37.2 billion to $57.3 billion annually over the next decade. Furthermore, its indispensable role in concrete production links its growth directly to major construction trends, including the rapid build-out of data centers. The combination of essential utility in foundational industries and its role in addressing critical global challenges like clean water positions the coarse sand segment for sustained and robust growth.

By Application

In the application landscape, glassmaking continues to be the primary consumer of washed silica sand market, dominating the market with the highest share of 37.4%. Silica is the fundamental building block of glass, constituting up to 70% of the raw materials used in its production. The demand is broad, spanning container glass for the food and beverage industry, flat glass for architectural and automotive use, and specialty glass for high-tech applications. The architectural push for sustainable buildings is a key factor, with advanced glass facades and windows capable of cutting energy costs by up to 30%. This widespread and essential use ensures the glassmaking segment's leading position.

The glassmaking segment is also forecast to expand at the highest rate, driven by innovation and growth in its end-markets. The automotive industry's transition to EVs, for example, is creating new demand for lightweight and multifunctional glass to improve battery efficiency. The market for EV lightweight materials in the washed silica sand market is expected to grow to $10.87 billion in 2025. Additionally, the renewable energy sector's expansion relies heavily on high-transparency, low-iron glass for solar panels. The market for specialty glass, which includes these advanced products, is projected to grow consistently as technological demands increase. This convergence of sustainability trends, automotive innovation, and the growth of green energy solidifies the glassmaking segment's trajectory as the fastest-growing application for washed silica sand.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By Industry

The fiberglass and glass industry segment collectively holds the highest share in the washed silica sand market, accounting for 34.4%. This leading position stems from the critical need for high-quality, chemically consistent silica sand in both glass and fiberglass production. The glass industry's demand is multifaceted, ranging from container and flat glass to more specialized products. The fiberglass sector utilizes silica sand to create a material prized for its strength, low weight, and insulation properties. This makes it indispensable in a variety of sectors, including construction, automotive, and renewable energy.

The segment is also projected to demonstrate the highest growth rate, propelled by the global transition towards sustainable energy and lightweight materials in the washed silica sand market. The demand for fiberglass in manufacturing wind turbine blades is surging as countries expand their wind energy capacity to meet climate goals. Similarly, the automotive industry's focus on lightweighting, particularly in EVs to maximize range, is driving the adoption of fiberglass composites. A 10% reduction in an EV's weight can increase its range by 5-7%. As the EV market continues its exponential growth, with sales of around 14 million units in 2023, the demand for lightweighting materials like fiberglass will escalate. Simultaneously, the glass industry is benefiting from the push for green buildings and innovations in smart glass. This synergy between the two major components of the segment ensures its position as the fastest-growing industrial consumer of washed silica sand.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia-Pacific: The Unrivaled Market Leader

The Asia-Pacific region stands as the preeminent force in the global washed silica sand market, commanding a revenue share of over 45%. This dominance is propelled by the region's immense scale of industrial activity, rapid urbanization, and massive governmental infrastructure initiatives. The construction sectors in China and India are the primary engines of demand. Despite a slowdown in some areas, China's construction output is still expected to grow in 2025, supported by central government policies. India's construction industry is on a formidable growth path, projected to reach US$ 1.4 Trillion by 2025, driven by the government's National Infrastructure Pipeline. Furthermore, the region has become the epicenter of global high-tech manufacturing. The Asia-Pacific semiconductor market is forecast to sustain double-digit growth in 2025, with sales increasing by 10%. Countries like China, Japan, and South Korea dominate semiconductor production and consumption, requiring vast quantities of ultra-high purity silica. This dual-pronged demand from both massive construction projects and cutting-edge electronics manufacturing solidifies Asia-Pacific's leadership position.

North America: Driven by Reshoring and Tech Infrastructure

North America represents a mature and technologically advanced washed silica sand market where demand is being reshaped in 2025 by strategic industrial policies and the AI-driven infrastructure boom. Government initiatives like the Infrastructure Investment and Jobs Act (IIJA) and the CHIPS Act are channeling substantial funds into new projects. This is fueling the construction of semiconductor fabrication plants, EV battery factories, and transportation networks, all of which are significant consumers of washed silica sand.

However, the most dynamic driver is the explosion in data center construction in the washed silica sand market. The U.S. data center construction market is expected to grow significantly, with a CAGR of 10.2% from 2025 to 2030. States such as Virginia, Texas, and Arizona are becoming global hubs, with billions in new investments announced in 2025, including Google's $25 billion regional data center plan and Blackstone's $25 billion commitment. This tech-centric construction wave, combined with continued demand from the region's oil and gas sector for hydraulic fracturing, creates a robust and high-value market.

Europe: A Market Defined by Green Regulations and Circularity

The European washed silica sand market is increasingly defined by the continent's ambitious environmental policies, particularly the European Green Deal and the Circular Economy Action Plan. Demand is strong in high-value sectors such as specialty glass manufacturing for the automotive and renewable energy industries. Europe's focus on decarbonization directly fuels the need for silica in solar panels and fiberglass for wind turbines. However, the market operates under a unique dynamic due to the strong regulatory push for sustainability.

In 2025, significant efforts are underway to establish closed-loop recycling systems for flat glass to reduce reliance on virgin raw materials. This drive toward circularity, while creating a competing feedstock in the form of recycled cullet, also spurs innovation in purification technologies. The market is therefore characterized by a demand for high-quality, responsibly sourced silica for advanced applications, balanced by an ever-growing emphasis on recycling and reducing the industry's overall environmental footprint.

Competitive Landscape: How Silica Sand Titans are Redefining Competition in 2025

The competitive landscape of the washed silica sand market is being aggressively redrawn along strategic, high-value lines. The old rivalry based on sheer volume has been supplanted by a fierce battle for dominance in the high-purity quartz (HPQ) sector, a direct response to the insatiable demands of the semiconductor and solar industries. In this new arena, market power is defined by the ability to produce ultra-pure grades. Simultaneously, robust Environmental, Social, and Governance (ESG) performance has evolved from a corporate checkbox into a critical competitive differentiator, directly influencing investment appeal, customer loyalty, and the social license to operate.

This strategic shift is clearly visible in the actions of industry leaders. Sibelco is aggressively cementing its dominance in the washed silica sand market by channeling over half a billion dollars into expanding its HPQ capacity to capture the lucrative tech supply chain. Covia Holdings competes on multiple fronts, broadcasting its ESG leadership through transparent reporting while consolidating market power via major mergers. Meanwhile, players like Badger Mining Corporation are executing targeted acquisitions to secure regional and logistical control in key end-markets. Diversified giants such as U.S. Silica leverage a vast product portfolio and assertive pricing strategies, demonstrating that resilience and market breadth remain powerful competitive tools in this dynamic industry.

Top Players in the Global Washed Silica Sand Market

- Adwan Chemical Industries

- AGSCO Corporation

- Badger Mining Corporation

- Chongqing Changjiang River Moulding Material (Group) Co. Ltd.

- Covia Holdings Corporation

- Euroquarz GmbH

- International Silica Industries Co

- JFE Mineral Co. Ltd.

- Mitsubishi Corporation

- Quarzwerke GmbH

- Short Mountain Silica Co.

- Sibelco NV

- Superior Silica Sands, LLC.

- Tochu Corporation

- U.S. Silica Holdings, Inc.

- VRX Silica Limited

- Other Prominent Players

Market Segmentation Overview:

By Fe Content

- Less than 0.01%

- More than 0.01%

By Form

- Coarse (0.1 mm to 2.0 mm)

- Medium (0.05 mm to 0.5 mm)

- Fine (0.025 mm to 0.1 mm)

- Ultra-Fine (0.06 mm - 0.01 mm)

By Application

- Glassmaking

- Ceramic & Refractories

- Industrial Abrasives

- Metal Casting

- Paints & Coatings

- Water Filtration

- Others

By Distribution Channel

- Online

- Offline

- Direct

- Distributors/ Wholesalers

By Industry

- Construction and Building

- Fiberglass and Glass

- Foundry

- Metallurgy

- Sport And Leisure

- Oil and Gas

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 6.43 Bn |

| Expected Revenue in 2033 | US$ 12.75 Bn |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Bn) |

| CAGR | 7.9% |

| Segments covered | By Fe Content, By Form, By Application, By Distribution Channel, By Industry, By Region |

| Key Companies | Adwan Chemical Industries, AGSCO Corporation, Badger Mining Corporation, Chongqing Changjiang River Moulding Material (Group) Co. Ltd., Covia Holdings Corporation, Euroquarz GmbH, International Silica Industries Co, JFE Mineral Co. Ltd., Mitsubishi Corporation, Quarzwerke GmbH, Short Mountain Silica Co., Sibelco NV, Superior Silica Sands, LLC., Tochu Corporation, U.S. Silica Holdings, Inc., VRX Silica Limited, Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |