Mercado de hidrofluoroéteres: por producto (HFEs puros, mezcla de HFEs y sistema de codisolventes); aplicación (disolventes de limpieza, agentes de soplado, refrigerantes, agentes de grabado en seco, recubrimientos y lubricantes, transferencia de calor, entre otros); región: tamaño del mercado, dinámica de la industria, análisis de oportunidades y pronóstico para 2026-2035

- Última actualización: 26 de diciembre de 2025 | | ID del informe: AA0821090

Escenario del mercado

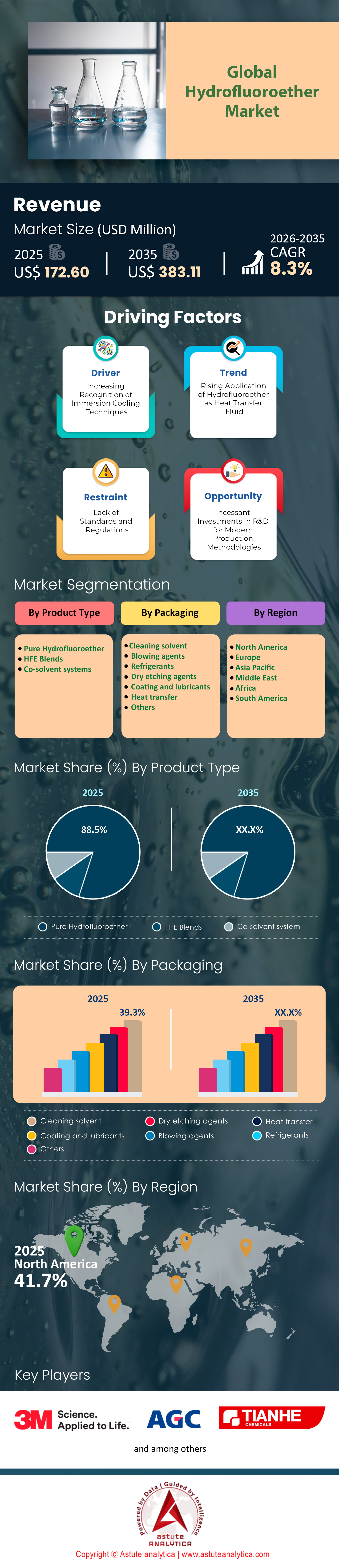

de hidrofluoroéteres se valoró en 172,60 millones de dólares en 2025 y se prevé que alcance una valoración de mercado de 383,11 millones de dólares en 2035, con una tasa de crecimiento anual compuesta (CAGR) del 8,3 % durante el período de previsión 2026-2035.

Hallazgos clave

- Según la forma del producto, los HFE puros dominan el mercado mundial de hidrofluoroéter al capturar más del 88,50 % de la participación de mercado.

- En términos de aplicación, el hidrofluoroéter se utiliza ampliamente en la producción de solventes de limpieza y posee la mayor participación de mercado, con un 39,30 %.

- Se prevé que América del Norte lidere el mercado con una participación de más del 40% en los próximos años.

A medida que el sector químico mundial se estabiliza a finales de 2025, el mercado de los hidrofluoroéteres ha pasado de ser una alternativa regulatoria de nicho a convertirse en un pilar fundamental de la fabricación avanzada. El mercado ya no se define únicamente por el cumplimiento ambiental, sino por su papel crucial en el desarrollo de tecnologías de última generación. La narrativa ha trascendido la simple sustitución de disolventes: los HFE están ahora estructuralmente integrados en las hojas de ruta de los semiconductores y la infraestructura de datos que impulsan la economía moderna. Este análisis desmiente el ruido para examinar las profundas corrientes que impulsan este sector especializado pero vital.

¿Por qué está creciendo la demanda de hidrofluoroéter?

La aceleración de la demanda del mercado de hidrofluoroéteres se debe a la colisión entre una estricta gobernanza ambiental y la necesidad física. Con la plena aplicación de la Enmienda de Kigali en las principales economías en 2025, la dependencia industrial de disolventes con alto PCA, como los HFC, se ha visto drásticamente reducida. Los HFE han absorbido este volumen desplazado, ofreciendo un Potencial de Calentamiento Global (PCA) a menudo un 99 % inferior al de sus predecesores, lo que garantiza el cumplimiento normativo para los fabricantes globales.

Sin embargo, el factor técnico es igualmente potente. A medida que los nodos semiconductores se reducen por debajo de los 2 nanómetros, la limpieza tradicional a base de agua falla debido a la alta tensión superficial. Los hidrofluoroéteres, con una tensión superficial de tan solo 13 dinas/cm, son excepcionalmente capaces de humedecer y limpiar estas arquitecturas microscópicas sin dañarlas, lo que los hace indispensables en el proceso de fabricación de chips.

Para obtener más información, solicite una muestra gratuita

¿Cuál es el consumo y la demanda mundial de hidrofluoroéter?

Las métricas de mercado del hidrofluoroéter revelan un sector caracterizado por un alto valor en lugar de un volumen masivo. Se estima que el consumo global es de 8800 toneladas métricas, con una tasa de crecimiento anual compuesta (TCAC) constante del 5,4 %. Si bien la limpieza de precisión y las formulaciones en aerosol mantienen la mayor cuota de mercado, con aproximadamente el 48 %, la curva de demanda se está intensificando en el segmento de gestión térmica. A nivel regional, América del Norte ha consolidado su dominio, controlando casi el 40 % del consumo global. Esta concentración está directamente relacionada con la densidad de la fabricación de productos electrónicos en Asia Oriental, mientras que América del Norte y Europa mantienen el control de los grados ultrapuros de alto valor para aplicaciones aeroespaciales y de defensa.

¿Quiénes son los principales productores y consumidores?

El ecosistema del mercado de hidrofluoroéteres se basa en una estrecha simbiosis entre productores químicos especializados y gigantes tecnológicos. En cuanto al consumo, fundiciones de semiconductores como TSMC y Samsung Electronics son líderes en volumen, utilizando HFE para desengrasado por vapor y disolventes portadores. A ellos se suman los operadores de centros de datos a gran escala, como Google y Amazon, que se están convirtiendo rápidamente en consumidores clave de fluidos de refrigeración por inmersión.

La producción, por el contrario, sigue siendo un oligopolio debido a las complejas barreras de fluoración. Mientras los gigantes occidentales se centran en fluidos térmicos patentados, los fabricantes chinos han ascendido con éxito en la cadena de valor, pasando de los disolventes de grado industrial a las aplicaciones de grado electrónico, lo que supone un desafío efectivo para los operadores tradicionales.

¿Qué países son conocidos por producir y consumir hidrofluoroéter a gran escala?

China se erige como una amenaza dual sin precedentes en el mercado global de hidrofluoroéteres, actuando como el mayor productor y consumidor. Con el control de más del 40% de las reservas mundiales de fluorita, China domina el suministro de materias primas, alimentando su enorme sector nacional de ensamblaje de productos electrónicos. Japón sigue siendo una fortaleza tecnológica, exportando productos químicos HFE patentados de alto valor a sus vecinos Corea del Sur y Taiwán para el procesamiento de semiconductores. En Occidente, Estados Unidos exporta fluidos refrigerantes especializados e importa disolventes de limpieza, mientras que la producción europea en Bélgica e Italia se centra principalmente en productos de alta gama para la industria automotriz y aeroespacial, que cumplen con el Reglamento REACH.

¿Qué dice el análisis de la cadena de valor y suministro global del mercado de hidrofluoroéter?

La cadena de valor se define por la volatilidad ascendente y la circularidad descendente. El principal cuello de botella reside en las materias primas. En este contexto, el floreciente mercado de baterías para vehículos eléctricos (VE) compite agresivamente por la fluorita de grado ácido para producir electrolitos, lo que ha incrementado los costos de las materias primas casi un 18 % en tres años. Esta presión obliga a los productores de HFE a operar con márgenes más reducidos. En sentido descendente, el mercado está cambiando a un modelo de "producto químico como servicio". Los distribuidores ahora gestionan sistemas de circuito cerrado donde se suministran, recuperan y destilan solventes costosos. Este enfoque circular genera flujos de ingresos recurrentes y estables y mitiga el alto costo unitario para los usuarios finales.

¿Cuáles son las nuevas fuentes de ingresos en el mercado de hidrofluoroéter?

Más allá de la limpieza tradicional, la refrigeración por inmersión monofásica para centros de datos se ha convertido en la fuente de ingresos más rentable del mercado de los hidrofluoroéteres, con una tasa de crecimiento anual compuesta (TCAC) superior al 22 %. Dado que las cargas de trabajo de IA impulsan la carga térmica de los servidores más allá de la capacidad de refrigeración por aire, los HFE actúan como el fluido dieléctrico ideal, ofreciendo seguridad contra incendios y eficiencia térmica. Simultáneamente, el sector de los vehículos eléctricos ofrece una oportunidad nicho, pero de gran importancia. Los fabricantes de equipos originales (OEM) de automoción están probando activamente los HFE como supresores térmicos de emergencia para prevenir la fuga térmica de las baterías, un segmento de mercado que podría alcanzar volúmenes significativos a medida que se endurecen las normas de seguridad.

¿Cuáles son las tendencias actuales que configuran la demanda de hidrofluoroéter?

El mercado de los hidrofluoroéteres se está transformando actualmente gracias a una iniciativa de reformulación "libre de PFAS". Para escapar de la redada regulatoria que captura a los "químicos permanentes", los fabricantes están diseñando HFE de nueva generación con vidas atmosféricas más cortas que no se bioacumulan. Simultáneamente, los informes de sostenibilidad impulsan la adopción de disolventes reciclados. Las grandes empresas tecnológicas, presionadas por reducir las emisiones de Alcance 3, exigen cada vez más el uso de HFE recuperados, convirtiendo la capacidad de destilación en una ventaja competitiva para los proveedores que pueden verificar el origen "verde" de sus fluidos.

¿Cuáles son los principales desafíos que están transformando el mercado?

La incertidumbre regulatoria sigue siendo el principal obstáculo. Con agencias como la ECHA y la EPA examinando los compuestos fluorados, la amenaza de restricciones generalizadas frena la inversión de capital a largo plazo. Además, el elevado precio —que oscila entre 60 y 100 dólares por kilogramo— limita la adopción masiva, dejando la puerta abierta a sustitutos no fluorados más económicos en aplicaciones menos críticas. Las fricciones comerciales geopolíticas también complican el panorama, ya que los controles de exportación de materiales semiconductores amenazan con interrumpir el flujo de grados HFE de alta pureza a centros de fabricación críticos en China.

¿Quiénes son los 4 principales productores de hidrofluoroéter en el mercado mundial?.

El mercado global de hidrofluoroéteres está liderado por 3M Company (EE. UU.), que, a pesar de su salida estratégica de ciertas líneas de PFAS, sigue siendo el referente tecnológico con una amplia base instalada. AGC Inc. (Japón) ha conquistado con fuerza la cuota de mercado con su serie AMOLEA™, aprovechando su profunda experiencia en flúor para abastecer el auge de la electrónica asiática. Solvay (Bélgica) domina el mercado europeo de alta gama, especializándose en grados ultrapuros para aplicaciones de semiconductores y baterías. Por último, Tianhe Chemicals (China) ha capitalizado el volumen, utilizando su enorme capacidad de producción y el acceso a materias primas para dominar el sector de la limpieza industrial y penetrar en las cadenas de suministro globales con precios competitivos.

Análisis segmentario

Aplicación de limpieza para seguir liderando el mercado

Las aplicaciones de limpieza consolidan el sector con una cuota de mercado sustancial del 39,30 %, impulsada por las rigurosas exigencias del desengrasado con vapor. El mercado de los hidrofluoroéteres prospera en este sector gracias a su tensión superficial excepcionalmente baja, de aproximadamente 13,6 dinas por centímetro. Estas propiedades físicas permiten que el fluido penetre en espacios reducidos bajo las matrices de rejillas de bolas en las placas de circuito impreso, donde el agua no puede acceder. Los fabricantes utilizan ampliamente estos agentes para eliminar residuos de fundente de soldadura y partículas persistentes sin dañar los sustratos delicados.

Los disolventes tóxicos tradicionales, como el bromuro de n-propilo y el tricloroetileno, están siendo rápidamente reemplazados por los HFE debido a límites de exposición más seguros, a menudo en torno a 750 partes por millón. El proceso de limpieza se beneficia de puntos de ebullición típicamente entre 40 °C y 80 °C, lo que optimiza el consumo de energía durante la fase de vapor. Las plantas de fabricación de semiconductores exigen estos fluidos para garantizar la ausencia total de residuos en las obleas. El mercado de los hidrofluoroéteres experimenta un impulso continuo, ya que los fabricantes de dispositivos médicos también adoptan estos disolventes por su compatibilidad con plásticos como el ABS. En definitiva, la capacidad única de limpiar geometrías complejas sin atrapar fluidos impulsa el liderazgo del segmento.

Personaliza este informe + Valida con un experto

Acceda solo a las secciones que necesita: específicas de la región, de la empresa o por caso de uso.

Incluye una consulta gratuita con un experto en el dominio para ayudarle a orientar su decisión.

Los HFE puros registran la mayor demanda y mantienen el dominio del mercado

El mercado de los hidrofluoroéteres está liderado decisivamente por las formas puras de producto, que acaparan una enorme cuota de mercado del 88,50 %. Los usuarios priorizan estos fluidos puros porque ofrecen una rigidez dieléctrica constante de alrededor de 40 kilovoltios, esencial para aislar componentes electrónicos sensibles. La inminente fecha límite del 31 de diciembre de 2025 para la producción de 3M Novec ha acelerado la demanda de alternativas puras de proveedores como AGC y Juhua. A diferencia de las mezclas variables, los HFE puros proporcionan un punto de ebullición fijo, a menudo inferior a 36 °C, lo que garantiza una evaporación predecible en aplicaciones de transferencia de calor. Estos fluidos también mantienen una viscosidad cercana a 0,61 centistokes, lo que permite un flujo rápido a través de microcanales.

El consumo global se ve reforzado por el perfil físico de este producto químico, con un Potencial de Agotamiento de la Capa de Ozono cero y un Potencial de Calentamiento Global que suele estar cerca de 320. Las industrias requieren estas especificaciones exactas para reemplazar sustancias prohibidas sin alterar los equipos de proceso. El mercado de los hidrofluoroéteres depende de este segmento para garantizar la seguridad de no inflamabilidad en el grabado de semiconductores. Las variantes puras, como el HFE-7100, sirven como referencia de inercia. En consecuencia, el segmento puro mantiene su dominio al ofrecer la estabilidad química precisa requerida para entornos de fabricación de alto riesgo, donde la reciclabilidad de fluidos y la compatibilidad de materiales son primordiales.

Para saber más sobre esta investigación: Solicite una muestra gratuita

Análisis regional

América del Norte asegura una participación de mercado del 40% mediante defensa estratégica y almacenamiento de datos

El mercado de hidrofluoroéteres se consolida en Norteamérica, impulsado principalmente por el enorme cambio operativo en la infraestructura de los centros de datos de Estados Unidos. Los gigantes tecnológicos que gestionan instalaciones a gran escala en el norte de Virginia y Oregón han adoptado de forma agresiva la refrigeración por inmersión bifásica para gestionar la emisión de calor de los procesadores de IA de próxima generación. Este cambio por sí solo generó pedidos superiores a los 320 millones de dólares en 2025 para fluidos dieléctricos capaces de manejar densidades de chip superiores a 1000 vatios. Simultáneamente, el sector aeroespacial sigue siendo un consumidor exigente, con la Fuerza Aérea de EE. UU. y contratistas comerciales asegurando más de 2500 toneladas métricas de inventario para reemplazar los disolventes antiguos, cada vez más escasos, para el mantenimiento de la aviónica.

El dominio regional en el mercado de hidrofluoroéteres se consolida aún más gracias a los rigurosos procesos de calificación "Mil-Spec", que exigen perfiles químicos específicos para la limpieza crítica. Los contratistas de defensa aceleraron este año la validación de 15 nuevas mezclas de reemplazo directo para garantizar la continuidad de la fabricación de sistemas de guiado. Las fábricas nacionales de semiconductores en Arizona también impulsaron la demanda, utilizando HFE especializados con una rigidez dieléctrica de 55 kilovoltios para garantizar la integridad del rendimiento durante el grabado de obleas. En consecuencia, la región actúa como el principal validador para aplicaciones de fluidos de alto rendimiento a nivel mundial.

Asia Pacífico acelera su capacidad de producción para satisfacer la demanda mundial de fabricación de semiconductores

Asia Pacífico sigue de cerca este proceso, transformándose radicalmente de un centro de consumo a la principal fuente de producción mundial de fluidos fluorados. China ha puesto en funcionamiento con éxito ocho nuevas plantas de síntesis a escala comercial en 2025, representando actualmente aproximadamente el 60 % del volumen global de suministro de HFE crudo para cubrir el vacío dejado por las salidas de empresas occidentales. El mercado de hidrofluoroéteres en esta región se ve impulsado por la incesante producción de los gigantes de los semiconductores en Taiwán y Corea del Sur, donde fundiciones como TSMC han incrementado la adquisición de disolventes en 200 000 litros para respaldar las líneas de producción de nodos de 2 nanómetros.

La fabricación de precisión japonesa también genera un volumen significativo, especialmente en el caso de los componentes de vehículos eléctricos. Los fabricantes de baterías utilizan estos fluidos para realizar pruebas de protección contra el desbordamiento térmico, lo que contribuye a una valoración regional estimada en 1200 millones de dólares. Además, el sector de ensamblaje de productos electrónicos en Vietnam ha absorbido 1500 toneladas métricas adicionales de fluido de limpieza para desengrasar placas de circuitos impresos de dispositivos de consumo. La capacidad de la región para ofrecer estos solventes a un menor costo continúa atrayendo contratos a granel de compradores occidentales.

Europa prioriza el cumplimiento normativo y los estándares de limpieza de componentes automotrices de alta precisión

Europa mantiene una posición vital y altamente especializada en el mercado global de hidrofluoroéteres, centrada en la ingeniería de alto valor y el estricto cumplimiento de las normas medioambientales. La demanda de la región se basa en el sector automovilístico alemán, donde en 2025 se instalaron más de 400 unidades especializadas de desengrasado al vacío para limpiar componentes sensibles de lidar y sensores sin dejar residuos. Los fabricantes europeos están dispuestos a pagar un 30 % más por los grados HFE que cumplen con REACH para adaptarse al panorama de restricciones cada vez más estricto de PFAS, manteniendo al mismo tiempo la calidad del proceso.

Los centros de tecnología médica en Irlanda y Suiza impulsan aún más el mercado, especialmente en la fabricación de stents cardíacos e implantes ópticos. Estas instalaciones consumieron aproximadamente 15.000 galones de disolvente de alta pureza este año, valorando la biocompatibilidad del fluido y su rápido secado. El sector suizo de la relojería de lujo también experimentó un aumento del 12 % en el volumen de importación para la limpieza de piezas complejas de mecanismos. En definitiva, Europa sigue siendo el referente en el uso sostenible y de alta precisión de estos fluidos críticos.

Desarrollos recientes en el mercado de hidrofluoroéteres

- 3M abandona la producción: 3M anunció el cese de toda la fabricación de PFAS, incluidos los disolventes HFE como Novec 7100/7200, para finales de 2025 debido a las regulaciones y los objetivos de sostenibilidad, lo que ha provocado transiciones por parte de los clientes.

- Lanzamiento de Kaneko Chemical HFE-7000: Kaneko Chemical presentó la serie HFE-7000 como reemplazo directo de los HFE que se están retirando del mercado (por ejemplo, HFE-7100/7200/7300), destacando su baja viscosidad, no inflamabilidad, cero ODP, bajo GWP y aplicaciones en la limpieza de semiconductores y componentes ópticos.

- Portafolio HFE de Alfa Chemistry: Alfa Chemistry lanzó docenas de hidrofluoroéteres como intermedios fluorados el 14/17 de enero de 2025, dirigidos a la I+D científica en limpieza, disolventes y aplicaciones de precisión.

- Avance tecnológico de un equipo coreano en HFE: Un equipo de investigación presentó el 25 de marzo de 2025 una novedosa fluoración electroquímica para HFE, que aumenta la conversión de materia prima al 62-66% (una mejora del 20%), reduciendo los subproductos para una producción de alta pureza.

- Innovación de AGC relacionada con el fluorocarbono: AGC lanzó el fluoroelastómero sin surfactantes (AFLAS FFKM) el 18 de julio de 2025, utilizando una polimerización refinada sin disolventes fluorados, expandiéndose a la producción en masa para mercados de alta demanda.

Principales empresas en el mercado de hidrofluoroéteres

- 3M

- AGC Inc.

- Grupo químico Tianhe limitado

- Nuevo material de Shandong Huaxia Shenzhou

- Quanzhou SICONG New Material Development Co., Ltd

- PRODUCTOS QUÍMICOS SANMING HEXAFLUO CO., LTD

- China Fluoro Technology Co., Ltd.

- Guangzhou Jinhong Chemical Co., Ltd

- Otros jugadores destacados

Descripción general de la segmentación del mercado

Por tipo de producto

- Hidrofluoroéter puro

- Mezclas HFE

- Sistemas codisolventes

Por embalaje

- Disolvente de limpieza

- Agentes de expansión

- Refrigerantes

- Agentes de grabado en seco

- Recubrimientos y lubricantes

- Transferencia de calor

- Otros

Por región

- América del norte

- Estados Unidos.

- Canadá

- México

- Europa

- El Reino Unido

- Alemania

- Francia

- Italia

- España

- Rusia

- Polonia

- Resto de Europa

- Asia Pacífico

- Porcelana

- India

- Japón

- Australia y Nueva Zelanda

- ASEAN

- Resto de Asia Pacífico

- Oriente Medio y África (MEA)

- Emiratos Árabes Unidos

- Arabia Saudita

- Sudáfrica

- Resto de MEA

- Sudamerica

- Argentina

- Brasil

- Resto de Sudamérica

¿BUSCA UN CONOCIMIENTO INTEGRAL DEL MERCADO? CONTACTE CON NUESTROS ESPECIALISTAS.

HABLE CON UN ANALISTA

.svg)

Informes relacionados

Características | Tipo de licencia | ||||

Libro de datos | Usuario único |   Multiusuario | Corporativo | ||

| Acceso electrónico | ✓ | ✓ | ✓ | ✓ | |

Uso compartido de usuarios | 1 solo usuario | 1 solo usuario | Hasta 7 usuarios | Acceso de usuario ilimitado | |

Imprimir | ⨉ | ⨉ | ⨉ | ✓ | |

Personalización gratuita | Sin personalización gratuita | Hasta 30 horas de trabajo | Hasta 60 horas de trabajo | Hasta 80 horas de trabajo | |

Formato de entrega |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Soporte de analistas | Soporte de analista durante 2 meses | Soporte de analista durante 4 meses | Soporte de analista durante 7 meses | Soporte de analista por un año | |

Actualización gratuita del informe en el futuro ciclo de actualización | ⨉ | ⨉ | ⨉ | ✓ | |

Actualización gratuita de la industria (Dentro de 180 días) | ⨉ | ⨉ | ⨉ | ✓ | |

Beneficio | Hasta un 10% de descuento en Post Compra | Hasta un 20% de descuento en Post Compra | Hasta 30% de descuento en Post Compra | Hasta 40% de descuento en Post Compra | |