Asia Pacific Solar Power Market: By Technology (Photovoltaic Systems (Monocrystalline silicon, Multicrystalline silicon, Thin-film, Others), Concentrated Solar Power Systems (Parabolic Trough, Fresnel Reflector, Power Tower, Dish-Engine), and Solar Heating and Cooling Systems); Solar Module (Monocrystalline Solar Panels, Polycrystalline Solar Panels, Thin-Film Solar Cells, Amorphous Silicon Solar Cell, Cadmium Telluride Solar Cell, and Others); End Use (Electricity Generation, Lighting, Heating, Charging, Others); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2024–2032

- Last Updated: 23-Jan-2026 | | Report ID: AA0923597

Market Scenario

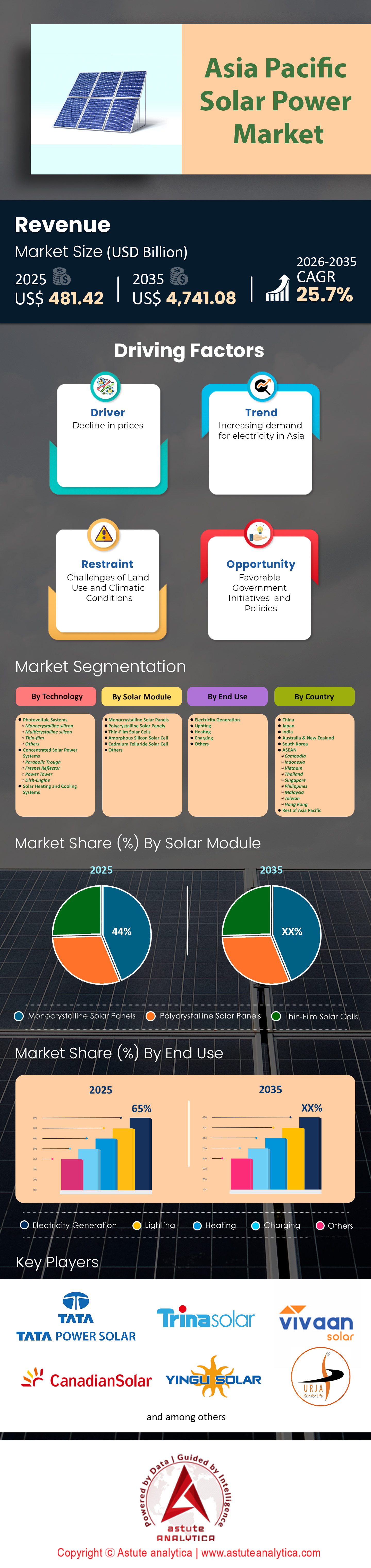

Asia Pacific solar power market was valued at US$ 481.42 billion in 2025 and is projected to attain a market valuation of US$ 4,741.08 billion by 2035 at a CAGR of 25.7% during the forecast period 2026–2035.

Key Findings

- Based on technology, PV systems accounts for 89% market share and is also projected to grow at an impressive CAGR of 26% over the years.

- Based on solar modules, monocrystalline solar panels leads the Asia Pacific solar power market by holding a 44% market share.

- Based on end users, the Asia Pacific solar power market is dominated by electricity generation segment as it accounts for an impressive 65% of the total market revenue.

- China is the most dominant country in the Asia Pacific market.

The sun rises in the East, and so does the future of the global energy transition. The Asia Pacific (APAC) region has transcended its former role as merely the world’s "factory" for solar components to become the planet’s largest and most dynamic deployment zone for photovoltaic (PV) technology.

As of 2026, the APAC solar market stands at a critical inflection point. No longer reliant solely on government subsidies, the market is being driven by genuine grid parity, energy security concerns, and corporate decarbonization mandates.

Market Dynamics: The Global Engine of Decarbonization

The Asia Pacific solar power market is currently responsible for over half of the world’s annual solar installations. This dominance is driven by a convergence of three macro-factors: Economic Growth, Climate Commitments, and Energy Security.

- The Strategic Shift from Fossil Fuel Dependency to Sovereign Energy Security and Domestic Power Generation

Historically, APAC economies were powered by imported coal and gas. However, recent geopolitical volatility and price spikes in fossil fuels have forced nations like India, China, and Japan to view solar not just as "green" energy, but as "secure" domestic energy. The sun cannot be sanctioned, and its price does not fluctuate with geopolitical conflict.

- Analyzing the Impact of Sovereign Climate Pledges and Net-Zero Targets on Regional Solar Deployment

The timeline to Net-Zero is tightening across the Asia Pacific solar power market.

- China: Aiming for carbon neutrality by 2060, with a massive interim goal of 1,200 GW of wind and solar by 2030.

- India: Prime Minister Modi’s "Panchamrit" pledge targets 500 GW of non-fossil fuel capacity by 2030 and Net-Zero by 2070.

- Japan & South Korea: Both nations have legislated Net-Zero by 2050, forcing a rapid restructuring of their energy mix away from imported LNG.

To Get more Insights, Request A Free Sample

Competitive Landscape Assessment: Evaluating the Rising Tide of Market Consolidation, Vertical Integration, and the Oligopoly of Super-Majors

The days of hundreds of small solar manufacturers competing for market share are over. The APAC solar power market is entering a phase of rapid consolidation, characterized by vertical integration and the dominance of a few "Super-Majors."

- Analyzing the Oligopoly of Super-Majors in the Asia Pacific Solar Power Market and How Bankability Requirements are Shaping the Competitive Ecosystem

The market is increasingly controlled by top-tier manufacturers, primarily based in China. Companies such as Longi Green Energy, Jinko Solar, Trina Solar, JA Solar, and Canadian Solar control a vast majority of the shipment volume.

- Bankability as a Moat: In the 65% utility-scale segment, financiers and banks require "Tier 1" equipment to underwrite loans. This creates a high barrier to entry for smaller, newer players who lack the historical performance data and balance sheets to be considered "bankable."

ii. The Strategic Importance of Vertical Integration for Manufacturing Survival and Margin Protection in a Commoditized Market

To survive the razor-thin margins of the Asia Pacific solar power market, leading players are pursuing aggressive vertical integration.

- The Chain: Instead of just assembling modules, top players now control the entire chain: Mining Polysilicon → Casting Ingots → Slicing Wafers→ Manufacturing Cells→ Assembling Modules.

- The Impact: This insulates the giants from raw material price shocks (like the polysilicon price spike of 2021/2022). Smaller, non-integrated players who must buy cells or wafers on the open market cannot compete on price against vertically integrated giants.

iii. Mergers, Acquisitions, and Distress: How Technological Darwinism is Forcing Tier-2 Manufacturers out of the Market

The Asia Pacific solar power market is witnessing a "cleaning out" of the market.

Technological Darwinism: Manufacturers who cannot afford the R&D CapEx to upgrade from P-type to N-type (TOPCon/HJT) technologies are being pushed out. This is leading to bankruptcies among Tier-2 Chinese and Indian manufacturers.

Downstream Integration: We also see consolidation downstream in the Asia Pacific solar power market, where large Independent Power Producers (IPPs) like Adani Green (India) or ACEN (Philippines) are acquiring smaller developers and EPC (Engineering, Procurement, Construction) firms to streamline project execution.

Strategic Technology Outlook: Identifying Key Disruptions Including Battery Storage Integration, Bifacial Modules, and Green Hydrogen Synergy

Beyond the basic metrics of PV and Monocrystalline growth, several trends will shape the next decade growth in the Asia Pacific solar power market.

- The Mandatory Integration of Battery Energy Storage Systems (BESS) to Mitigate Intermittency and Grid Instability

As solar penetration increases, the "Duck Curve" (where solar generation peaks at noon but demand peaks in the evening) becomes a problem.

Trend: The integration of Battery Energy Storage Systems (BESS) is becoming mandatory for new tenders in India and Australia. Solar is transitioning from "intermittent" energy to "firm, dispatchable" power.

- The Widespread Adoption of Bifacial Modules and Tracking Systems to Maximize Yield in Utility-Scale Projects

Bifacial modules produce power from both the front and back (using reflected light from the ground) in the Asia Pacific solar power market.

Adoption: In the utility-scale segment, bifacial modules are becoming the standard. They offer a 10-15% gain in energy generation for a marginal increase in cost, directly improving the Levelized Cost of Energy (LCOE).

- The Emerging Hydrogen Economy: How Solar Power is becoming the Primary Feedstock for Green Hydrogen Production

APAC is betting big on Green Hydrogen. Wherein, solar power is the primary feedstock for electrolyzers to produce green hydrogen. We expect massive "Solar-for-Hydrogen" plants to emerge in Australia and India by 2028, specifically to decarbonize heavy industries like steel and shipping.

Critical Market Inhibitors: Navigating Grid Infrastructure Bottlenecks, Land Acquisition Challenges, and Supply Chain Geopolitics in the Region

Despite the CAGR of 26%, significant headwinds remain in the Asia Pacific solar power market.

- The Growing Challenge of Grid Curtailment and the Urgent Need for High Voltage Transmission Infrastructure Upgrades

The grid in many Asian nations was built for centralized coal power, not distributed, variable solar power.

- The Issue: Curtailment. In parts of China and Vietnam, solar parks are forced to turn off (curtail) generation because the transmission lines cannot handle the surge of power during peak sunlight hours.

- The Need: Massive investment in High Voltage Direct Current (HVDC) transmission lines is required to move power from sunny remote areas to urban load centers.

- Complexities of Land Acquisition and Social Licensing in Densely Populated Asian Nations and Agrarian Economies

Solar requires vast amounts of land in the Asia Pacific solar power market. In densely populated India and Indonesia, acquiring land for the 65% utility-scale segment is becoming difficult. Conflicts with farmers and bureaucratic red tape regarding land conversion are the primary causes of project delays.

- Supply Chain Vulnerabilities and the Impact of Global Trade Barriers on the Free Movement of Solar Components

The "China Plus One" strategy is complicating the supply chain in the Asia Pacific solar power market. US and EU trade restrictions on Chinese solar goods (due to forced labor allegations in Xinjiang) impact APAC manufacturers. While this benefits India and Vietnam as alternative hubs, it creates short-term supply volatility and price friction.

Segmental Analysis

By Technology Analysis: Understanding Why Photovoltaic Systems Command an Overwhelming 89% Market Share and Projected Growth

Based on technology, PV systems accounts for 89% market share in the Asia Pacific solar power market and is also projected to grow at an impressive CAGR of 26% over the years.

The battle between Concentrated Solar Power (CSP) and Photovoltaic (PV) systems in Asia is effectively over. PV has emerged as the undisputed victor. Buy why?

- Cost Deflation: The cost of silicon PV modules has dropped by over 90% in the last decade. CSP, which relies on thermal dynamics and heavy mechanical infrastructure, has failed to achieve similar learning curve cost reductions.

- Scalability: PV systems are geographically agnostic. They can be installed on a rooftop in Mumbai, a floating platform in Vietnam, or a desert in huge Gobi installations. CSP requires high Direct Normal Irradiance (DNI), limiting it to specific desert belts.

- The 26% CAGR Factor: This aggressive growth rate is fueled by the "virtuous cycle" of manufacturing. As APAC manufactures more PV, the price drops, stimulating more demand, which justifies further manufacturing expansion.

By Module: Analyzing the Rise of Monocrystalline Panels and Their Dominant 44% Share in Asia Pacific Solar Power Market

Based on solar modules, Monocrystalline solar panels leads the Asia Pacific solar power market by holding a 44% market share. The solar industry is currently undergoing a massive technological migration from Polycrystalline (Poly) to Monocrystalline (Mono) technology.

- The Shift to Mono-PERC and TOPCon: While Polycrystalline panels were the standard for years due to lower costs, the efficiency gap has widened. Monocrystalline panels (specifically Passivated Emitter and Rear Cell or PERC) offer higher efficiency per square meter.

- Why 44% is just the beginning: In land-constrained Asian countries like Japan, South Korea, and the Philippines, maximizing power output per square meter is critical. Land is expensive; therefore, installing higher-efficiency Mono panels reduces the Balance of System (BoS) costs (fewer racks, less cabling, less land rent).

- The Decline of Poly: We forecast that the 44% share will expand to over 70% by 2030 as major Chinese manufacturers retrofit their gigafactories to produce n-type TOPCon and HJT (Heterojunction) Mono cells, effectively phasing out Poly production lines.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By End-User: How the Electricity Generation and Utility-Scale Segment Capture 65% of Total Market Revenue

Based on end users, the Asia Pacific solar power market is dominated by electricity generation segment as it accounts for an impressive 65% of the total market revenue.

While "rooftop solar" often grabs headlines for its consumer appeal, the real economic engine of the APAC solar market is Utility-Scale generation.

- State-Backed Mega Projects: The 65% revenue share is driven by massive infrastructure projects. China’s "clean energy bases" in the desert regions and India’s Ultra Mega Solar Parks (like Bhadla and Pavagada) operate on a scale unseen in Europe or the US. These are gigawatt-scale facilities connected directly to the high-voltage transmission grid.

- Corporate PPA (Power Purchase Agreements): Large industrial conglomerates in Asia (steel, cement, data centers) are bypassing the grid to sign direct PPAs with solar developers in the Asia Pacific solar power market. These projects fall under the electricity generation segment and are growing rapidly as companies seek to green their supply chains.

The Other 35%: The remaining market is split between Commercial & Industrial (C&I) rooftop and Residential. While Residential is growing in Australia and Japan, the sheer volume of panels required for utility-scale projects ensures the Electricity Generation segment will retain its dominance through 2030.

To Understand More About this Research: Request A Free Sample

Geographic Market Analysis: Deep Dive into the Distinct Growth Trajectories of China, India, and Emerging ASEAN Economies

The Asia Pacific solar market is not a monolith, it is a tapestry of distinct ecosystems, each characterized by unique regulatory drivers and maturity levels.

- The Dominant: China

China remains the undisputed gravitational center of the global solar power market, functioning as both the primary manufacturer and the largest consumer. The market is currently defined by a dual-track strategy: the massive "Clean Energy Bases" in the Gobi Desert—pairing gigawatt-scale solar with Ultra-High Voltage (UHV) transmission lines—and the "Whole County" policy, which mandates rooftop solar deployment on public infrastructure. China is on track to shatter its 1,200 GW wind and solar target well before 2030, driven by state-owned enterprises prioritizing energy security over pure profitability.

- The Growth Engine: India

India represents the highest potential growth story outside China. The Asia Pacific solar power market is undergoing a structural shift from import reliance to domestic self-sufficiency, fueled by the $2.4 billion Production Linked Incentive (PLI) scheme. This policy has spurred conglomerates like Reliance and Adani to build fully integrated gigafactories. As the world’s most price-sensitive market, India is dominated by the utility-scale segment, where competitive auctions frequently drive solar tariffs lower than coal, accelerating the country's march toward its 500 GW non-fossil fuel target.

- The Innovators: Japan, South Korea, and Australia

These mature economies in the Asia Pacific solar power market face significant land constraints (Japan/Korea) and grid saturation (Australia). Consequently, they are pivoting toward high-value innovation rather than raw volume. Japan is leading the region in Agrivoltaics (dual-use farmland) and offshore floating solar to bypass land scarcity. Meanwhile, Australia is transitioning from a rooftop solar leader to a "Green Energy Exporter," investing heavily in Green Hydrogen production hubs powered by solar to export clean fuel to its northern neighbors.

- The Emerging Countries: ASEAN

Southeast Asia (Vietnam, Indonesia, Thailand) solar power market is benefiting from the "China Plus One" strategy, becoming a critical alternative manufacturing hub to bypass Western trade tariffs. Operationally, the region is capitalizing on its geography to become the global epicenter for Floating PV (FPV), hybridizing solar arrays with existing hydropower dams to maximize infrastructure efficiency.

Top Players in Asia Pacific Solar Power Market

- Tata Power Solar System Ltd.

- Trina Solar

- Canadian Solar Inc

- Yingli Solar

- Urja Global Limited

- Vivaan Solar

- Waaree Group

- Shanghai Junlong Solar Technology Development Co., ltd

- Shenzhen Sungold Solar Co., Ltd

- BLD Solar Technology Co.,LTD

- Kohima Energy

- Wuxi Suntech Power Co. Ltd.

- Other Prominent Players

Market Segmentation Overview:

By Technology

- Photovoltaic Systems

- Monocrystalline silicon

- Multicrystalline silicon

- Thin-film

- Others

- Concentrated Solar Power Systems

- Parabolic Trough

- Fresnel Reflector

- Power Tower

- Dish-Engine

- Solar Heating and Cooling Systems

By Solar Module

- Monocrystalline Solar Panels

- Polycrystalline Solar Panels

- Thin-Film Solar Cells

- Amorphous Silicon Solar Cell

- Cadmium Telluride Solar Cell

- Others

By End Use

- Electricity Generation

- Lighting

- Heating

- Charging

- Others

By Country

- China

- Japan

- India

- Australia & New Zealand

- South Korea

- ASEAN

- Cambodia

- Indonesia

- Vietnam

- Thailand

- Singapore

- Philippines

- Malaysia

- Taiwan

- Hong Kong

- Rest of Asia Pacific

FREQUENTLY ASKED QUESTIONS

The Asia Pacific solar power market was valued at USD 481.42 billion in 2025. It is projected to skyrocket to USD 4,741.08 billion by 2035, growing at an aggressive CAGR of 25.7% during the forecast period.

Photovoltaic (PV) systems dominate with an 89% market share, projected to grow at a 26% CAGR, effectively sidelining Concentrated Solar Power (CSP). Within hardware, Monocrystalline panels lead with a 44% share, favored for high efficiency in land-constrained markets like Japan and Korea.

No. The market has transitioned from subsidy-dependence to grid parity. Current growth is driven by sovereign energy security strategies (reducing fossil fuel imports), competitive auctions, and corporate decarbonization mandates rather than direct feed-in tariffs.

The Electricity Generation (Utility-Scale) segment is the economic engine, accounting for 65% of total market revenue. This is fueled by gigawatt-scale mega-projects connected to high-voltage grids, such as China’s desert energy bases and India’s solar parks.

The Asia Pacific solar power market is forming an oligopoly of vertically integrated Super-Majors to protect margins. Simultaneously, supply chains are diversifying via a China Plus One strategy, with manufacturing hubs expanding into India and ASEAN to bypass Western trade barriers.

The biggest hurdles are grid curtailment—where transmission infrastructure lags behind rapid generation capacity—and difficult land acquisition processes in densely populated agrarian economies like India and Indonesia.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |