Market Scenario

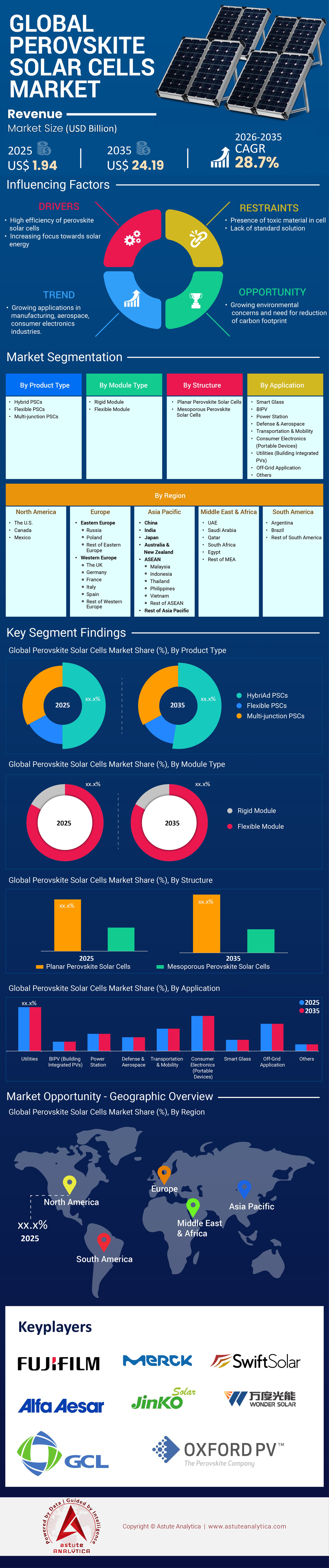

Perovskite solar cells market was valued at US$ 1.94 billion in 2025 and is projected to hit the market valuation of US$ 24.19 billion by 2035 at a CAGR of 28.7% during the forecast period 2026–2035.

Key Findings in the Market

- By Product Type, Hybrid Perovskite Solar Cells Seize Over 50% Market Share Through Superior Thermal Stability

- By Module, Rigid Modules Control Over 82% Revenue Share of the perovskite solar cells market By Guaranteeing Long Term Project Bankability

- By Application, BIPV Sector Commands 23% Share With Smart Facades Reducing Building HVAC Loads

- By Structure, Planar Structure Captures 69% Share By Enabling Rapid High Throughput Deposition

- Asia Pacific to Continue Leading the Market with Over 56% Market Share.

What Defines the Superior Performance of a Perovskite Solar Cell?

A perovskite solar cell utilizes a specific crystal structure—modeled after the naturally occurring mineral perovskite—to absorb light and generate electricity with remarkable efficiency. Unlike traditional silicon cells, which require thick, rigid wafers and high-temperature processing, a perovskite solar cell can be manufactured using solution-processing techniques to create Ultra-thin Solar Cells on flexible substrates. The technology’s demand is currently positioned as the superior successor to standard silicon photovoltaics, primarily because silicon is approaching its theoretical efficiency limit of roughly 29%.

In contrast, tandem configurations—where a perovskite solar cell is layered on top of a silicon cell—are shattering these boundaries in the perovskite solar cells market. For instance, LONGi set a certified efficiency record for silicon-perovskite tandem cells at 34.85% in April 2025. Similarly, JinkoSolar achieved 33.84% efficiency with its N-type TOPCon-based tandem cell in January 2025. Such performance metrics make the perovskite solar cell the most viable technology for the next generation of energy generation, offering higher power output in the same surface area compared to legacy technologies.

To Get more Insights, Request A Free Sample

Which Factors Are Triggering the Explosive Demand for Perovskite Technology?

The demand in the perovskite solar cells market is being catalyzed by three primary factors: breaching efficiency ceilings, versatility in application, and rapid industrial scalability. The primary driver is the sheer power density. UtmoLight produced a commercial-size module (2.8 m²) delivering 450 Watts, while Oxford PV achieved 421 Watts on a standard industrial format. These figures prove that the technology can deliver more power per square meter than conventional panels, a crucial factor for space-constrained urban environments.

Furthermore, economic viability is fueling this surge. A 2025 cost analysis estimated the manufacturing cost of a perovskite solar cell module at USD 0.57 per Watt, with projections dipping to USD 0.29–0.42 per Watt at full scale. Additionally, a Swiss study calculated a potential Levelized Cost of Electricity (LCOE) of USD 0.051 per kWh. Beyond economics, the ability to create lightweight, flexible films allows entry into markets silicon cannot touch. Sekisui Chemical, for example, began sales of 30 cm wide flexible films, targeting building facades where weight is a constraint.

Why is Asia Dominating the Global Production Landscape in Perovskite Solar Cells Market?

The global production landscape for the perovskite solar cell is heavily concentrated in Asia, specifically China, which has successfully transitioned from R&D to gigawatt-scale manufacturing. China’s dominance is justified by its aggressive industrial scaling and massive intellectual property accumulation. By October 2025, China held over 33,300 patents related to perovskite technology, dwarfing other regions. The region’s leadership is physically visible in Wuxi, where UtmoLight launched a 1 GW production line in February 2025 capable of churning out 1.8 million modules annually.

Simultaneously, Renshine Solar secured USD 171 million (1.25 billion RMB) to construct an 80,000-square-meter factory in Changshu. South Korea is also intensifying the regional foothold in the perovskite solar cells market, with Hanwha Qcells investing USD 102 million (136.5 billion KRW) specifically for tandem pilot lines. Japan complements this with high-value, specialized manufacturing; the government there set a target of 20 GW capacity by 2040 and awarded USD 167 million in subsidies to players like Panasonic. Consequently, Asia controls the majority of the supply chain and production capacity, making it the undeniable epicenter of the perovskite solar cell revolution.

Who Are the Commercial Giants Driving Large-Scale Manufacturing?

The competitive landscape of the perovskite solar cells market is defined by a race to operationalize gigawatt-level facilities. UtmoLight currently leads the pack with its fully operational 1 GW line. Renshine Solar is close behind, operating a 150 MW line while building its gigawatt base. In Europe, Oxford PV remains a key player, having shipped its first commercial residential modules to U.S. utilities, marking a milestone for Western manufacturing.

Japanese conglomerates are focusing on specialized applications. Sekisui Chemical committed USD 570 million (90 billion JPY) through 2030 to mass-produce flexible perovskite solar cell films, leveraging its materials expertise. Meanwhile, huge incumbent PV manufacturers like First Solar are pivoting resources, investing approximately USD 500 million in R&D infrastructure that includes dedicated perovskite development lines in Ohio. These companies are no longer treating the perovskite solar cell as a science experiment but as a core product line for 2026 and beyond.

How is the Global Supply Chain Adapting to Perovskite Materials?

Supply chain dynamics of the perovskite solar cells market are shifting toward material localization and security. Unlike silicon cells which rely on polysilicon, a perovskite solar cell depends on precursors like iodine, lead, and specialized solvents. Japan is leveraging its status as the world’s second-largest iodine producer to secure a domestic supply chain for companies like Sekisui Chemical. Europe is attempting to counter Asian dominance through policy; the Net-Zero Industry Act targets 40% of clean tech demand to be met by local manufacturing, forcing European entities to localize supply chains for glass and conductive coatings.

Equipment procurement is another critical supply chain node. Microquanta acquired vacuum deposition equipment valued at over €9 million from SMIT Thermal Solutions to ensure production quality. On the raw material front, First Solar is securing tellurium supplies via Canadian partnerships to support its thin-film and tandem ambitions. However, the industry still relies heavily on lead (Pb) for high-efficiency cells, as lead-free alternatives still lag in stability, though research continues.

What Price Trends Are Emerging in the Perovskite Solar Cells Market?

Pricing dynamics in the perovskite solar cell market are moving aggressively toward parity with, and eventually undercutting, silicon. While early commercial modules currently hover around USD 0.57 per Watt due to initial capex amortization, the trajectory is downward. Hanwha Qcells targets its tandem modules to be 20-30% cheaper to produce than existing silicon cells once fully scaled.

Startups in the perovskite solar cells market are utilizing superior performance to justify current premiums. Tandem PV claims its panels are 30% more powerful than average silicon panels, allowing them to offset higher initial costs by delivering a lower LCOE over the project's lifetime. To access subsidies, companies must prove cost-competitiveness; the European Commission’s €2.4 billion Net-Zero Technologies Call requires strict demonstration of economic viability. As yields improve—UtmoLight targets a 99.5% yield rate—the price gap between a perovskite solar cell and a standard module is rapidly closing.

Which Future Trends Are Shaping the Growth Trajectory?

The growth momentum of the perovskite solar cells market is being shaped by two dominant trends: the standardization of Tandem Photovoltaics and the commercialization of Building Integrated Photovoltaics (BIPV).

- The Tandem segment is dominant because it fits into existing utility-scale infrastructure while boosting output. The trend is evidenced by standard wafer sizes; Qcells developed tandem cells based on the M10 wafer (330.56 cm²), and Oxford PV utilizes the industry-standard 72-cell configuration. This compatibility ensures that the perovskite solar cell can drop directly into current solar farm designs without expensive retrofitting.

- Simultaneously, the BIPV segment is unlocking new market value for the perovskite solar cells market through stability and aesthetics. Microquanta modules are now designed with a targeted lifespan of 25 years, directly addressing historical durability concerns. Stability data supports this trend, with University of Surrey researchers demonstrating 1,530 hours of continuous performance under extreme conditions. Furthermore, "generating glass" by Panasonic (substrates >800 cm²) and custom BIPV modules (1,200 mm x 1,000 mm) by Microquanta are turning building facades into power plants. These trends confirm that the perovskite solar cell is evolving from a niche technology into a foundational element of modern construction and energy infrastructure.

Segmental Analysis

By Product Type: Hybrid Perovskite Solar Cells Dominate Market Through Unrivaled Efficiency and Tandem Compatibility

Hybrid perovskite solar cells currently command over 50% market share in the perovskite solar cells market, a dominance driven by their critical role in bridging emerging nanotechnology with established silicon photovoltaics. Unlike purely inorganic options, hybrid compositions mix organic cations with inorganic halides to create a tunable bandgap that maximizes light absorption across the solar spectrum. This segment’s leadership has been solidified by recent technological triumphs, including a world record efficiency of 34.6% for silicon-perovskite tandem cells, which shattered previous theoretical limits. This unparalleled efficiency potential serves as the primary engine for commercial interest, allowing manufacturers to layer hybrid perovskites atop existing silicon cells to boost output without discarding billions in legacy infrastructure.

The enthusiasm for hybrid types in the perovskite solar cells market is further supported by their superior charge-carrier mobility and processing versatility. Recent industry breakthroughs have demonstrated certified steady-state efficiencies of 26.7% for single-junction hybrid cells, proving that standalone hybrid devices are rapidly approaching silicon-grade performance. Commercially, the stakes are massive, with the global perovskite market seeing hybrid architectures absorb the majority of investment capital. Industry data indicates that over 60% of new pilot lines globally are specifically dedicated to hybrid tandem configurations, aiming to capitalize on the projected 38.05% CAGR for the sector. By offering the perfect synthesis of high efficiency and manufacturing feasibility, hybrid perovskites remain the undisputed market leader.

By Module, Rigid Modules Command Revenue By Leveraging Established Utility Infrastructure And Superior Durability

The rigid module segment is projected to generate over 82% revenue in the perovskite solar cells market, maintaining a monopoly largely due to its compatibility with the global solar utility infrastructure. While flexible films garner media attention, rigid glass-glass encapsulation provides the hermetic sealing necessary to protect sensitive perovskite layers from moisture and oxygen, which are their primary degradation triggers. The dominance of this segment is cemented by recent commercial shipments of perovskite tandem modules to utility customers, which boasted a commercial module efficiency of 24.5%. This performance significantly outperforms the average of standard silicon panels and promises up to 20% more energy generation over the same surface area, making them highly attractive for large-scale energy providers.

Rigid modules are the immediate revenue generators in the perovskite solar cells market because they fit seamlessly into the existing supply chain of racking, mounting, and tracking systems used in solar farms worldwide. Latest validations have seen rigid formats achieve a 28.6% efficiency record on large-area tandem cells, demonstrating that high performance is scalable on rigid substrates. Unlike flexible counterparts, which often suffer from lower efficiencies and higher encapsulation costs, rigid modules leverage standard industrial lamination processes. With utility-scale projects accounting for the vast majority of the total solar vertical, the demand for durable, high-yield rigid panels is insatiable. As manufacturers race to scale gigawatt-level factories, the rigid module’s proven ability to survive standard durability testing ensures it will remain the revenue king.

By Application, Building Integrated Photovoltaics Secure Leading Application Share Driving Global Net Zero Architecture

BIPV holds a revenue share of 23% in the perovskite solar cells market, establishing itself as the most lucrative niche application outside of utility-scale power. This segment is driven by the global imperative for Net Zero buildings and the unique optical properties of perovskites, which can be made semi-transparent or colored without the severe efficiency drops seen in silicon. The transparent solar cell market has seen BIPV applications capture nearly 47% of the transparent niche, signaling a massive shift in how architects view building façades. Major players are capitalizing on this trend, with perovskite BIPV glass projects on track for full commercialization by 2026, aiming to transform skyscrapers into self-powering entities.

The dominance of BIPV in the non-utility space across the global perovskite solar cells market is justified by the technology's ability to turn windows and skylights into power generators. Modern perovskite BIPV cells can now achieve transparency levels between 30% and 50% while maintaining power conversion efficiencies of 12% to 18%, a trade-off that is financially viable for commercial real estate. Recent breakthroughs have set records of 18.1% efficiency on large-area modules specifically designed for architectural integration, proving that aesthetics no longer require a sacrifice in performance. With global green building codes becoming stricter, and the BIPV market projected to grow rapidly, perovskites are the only technology capable of meeting the dual demand for translucency and energy density, securing this segment's robust market position.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By Structure, Planar Structure Dominates Manufacturing Sector Due To Low Cost and Scalable Processing

In the perovskite solar cells market, the planar structure segment is currently leading with a market share of 69%, a dominance anchored in the economic realities of mass production. Unlike the complex mesoporous structure, which requires a high-temperature sintering step often exceeding 450°C, planar architectures can be processed at temperatures below 150°C. This low-thermal budget is a game-changer, allowing manufacturers to reduce energy consumption and compatible equipment costs (CAPEX) by an estimated 30% to 40%. The shift toward planar designs is evident in the latest manufacturing trends, where leading entities utilize planar stacks to facilitate high-speed, slot-die coating and roll-to-roll printing techniques essential for commercial scaling.

The planar structure's command of the perovskite solar cells market is further justified by its superior defect management in large-area coating. Simpler layer stacking—typically just an electron transport layer, the perovskite absorber, and a hole transport layer—reduces the risk of pinholes that cause short circuits in larger modules. Research indicates that planar heterojunctions are the preferred structure for over 70% of emerging flexible perovskite patents, owing to their mechanical flexibility and resistance to cracking. Furthermore, planar structures are essential for the booming tandem market; their flat surface allows for uniform deposition on top of textured silicon cells. As the industry prioritizes lowering the Levelized Cost of Electricity, the planar structure’s compatibility with low-cost, solution-based manufacturing ensures it will retain its commanding market share.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific Dominance Driven by Gigawatt Scale Manufacturing and Government Policy

When it comes to Asia Pacific solar power, the commands a decisive 56% share of the perovskite solar cell market, a dominance fueled by China’s rapid transition from laboratory research to industrial mass production. By February 2025, UtmoLight’s 1 GW line in Wuxi was already operational, capable of churning out 1.8 million modules annually. This aggressive scaling is matched by Renshine Solar, which injected USD 171 million into its Changshu gigawatt-factory to secure supply chain supremacy.

Beyond China, Japan is fortifying the region's lead through strict policy mandates; the government’s target to achieve 20 GW of perovskite capacity by 2040 triggered Sekisui Chemical to commit USD 570 million for flexible film mass production. South Korea further cements this leadership with Hanwha Qcells investing USD 102 million specifically for tandem pilot lines, ensuring the region controls the bulk of global manufacturing capacity.

North America Strengthening Market Position Through Heavy R&D and Capital Injections

North America holds the second-largest spot in the global perovskite solar cells market, driven by substantial private equity flows and utility-scale adoption of the perovskite solar cell. First Solar serves as the region's industrial anchor, leveraging a massive USD 500 million R&D infrastructure investment and a USD 6 million DOE award to commercialize proprietary tandem technologies.

The region acts as a critical demand center; Oxford PV shipped its first commercial modules to U.S. utilities, proving that American grids are ready for next-gen integration. Investor confidence remains robust, evidenced by startup Tandem PV raising USD 50 million in Series A funding in March 2025. This unique combination of venture capital availability and high-demand utility projects ensures North America remains a key driver of commercial revenue.

Europe Sustaining Competitiveness via Net Zero Policies and Tandem Innovation

Europe perovskite solar cells market maintains its influential foothold by prioritizing high-efficiency tandem technology and strict supply chain localization. The region’s strategy relies heavily on policy-backed innovation, exemplified by the European Commission’s €3.4 billion Net-Zero initiative which directly funds commercially viable manufacturing lines. Oxford PV leads the commercial charge from Germany, delivering 421 Watt modules that have set the global standard for industrial performance.

Research depth here is unmatched and vital for market evolution; Helmholtz-Zentrum Berlin achieved 24.6% efficiency in specialized CIGS-tandems, while imec’s field tests in Cyprus confirmed essential one-year outdoor stability. These technological milestones ensure Europe remains the intellectual and quality control backbone of the global industry.

Perovskite Solar Cells Market Saw Pivotal Advancements From Key Players Via Official Announcements. Top 5 Developments As of 2025:

- Oxford PV Commercial Shipment (Apr 2025): Oxford PV shipped first perovskite-silicon tandem panels to a U.S. utility-scale customer, delivering 100 kW of 72-cell modules with 20% higher energy output than silicon, cutting LCOE.

- GCL Mass Production Launch (Oct 2025): GCL System Integration unveiled GW-scale 2.76 m² perovskite modules at 26.36% efficiency—the largest commercialized size—via their production line, redefining PV cost structures.

- JinkoSolar Efficiency Record (Dec 2025): JinkoSolar hit 34.76% efficiency in perovskite-silicon tandems, certified by China's NPVM lab, via n-type TOPCon and passivation innovations.

- Oxford PV-TrinaSolar Licensing (2025): Oxford PV inked a patent deal with TrinaSolar for perovskite PV manufacturing and sales, accelerating mainstream adoption.

- Ricoh Space Demo (Oct 2025): Ricoh installed perovskite cells on Japan Aerospace Exploration Agency's demonstration system, validating lightweight tech for satellites.

Top Companies in the Perovskite Solar Cells Market:

- BASF

- Dyenamo

- Energy Materials Corp.

- Frontier Energy Solution

- Fujifilm

- Fujikura

- GCL Suzhou Nanotechnology Co., Ltd.

- Greatcell Energy

- Hangzhou Microquanta

- Heiking PV Technology Co., Ltd.

- Hubei Wonder Solar

- Hunt Perovskite Technologies (HPT)

- InfinityPV

- Jinkosolar

- Kyocera

- LG Chem

- Li Yuan New Energy Technology Co.

- Merck

- Microquanta Semiconductor

- Oxford PV

- Panasonic

- Saule Technologies

- Sharp

- Solartek

- Solaronix SA

- Solliance

- Tandem PV

- Toshiba

- Trina Solar

- WonderSolar

- Other Prominent Players

Market Segmentation Overview:

By Product Type

- Hybrid PSCs

- Flexible PSCs

- Multi-Junction PSCs

By Module Type

- Rigid Module

- Flexible Module

By Structure

- Planar Perovskite Solar Cells

- Mesoporous Perovskite Solar Cells

By Application

- Smart Glass

- BIPV

- Power Station

- Defence and Aerospace

- Transportation and Mobility

- Consumer Electronics (Portable Devices)

- Utilities (Building Integrated PVs)

- Off-Grid Applications

- Other

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- The UK

- Germany

- France

- Italy

- Spain

- Russia

- Poland

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2025 | US$ 1.94 Bn |

| Expected Revenue in 2035 | US$ 24.19 Bn |

| Historic Data | 2020-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Unit | Value (USD Bn) |

| CAGR | 28.7 |

| Segments covered | By Product Type, By Module Type, By Structure, By Application, By Region |

| Key Companies | BASF, Dyenamo, Energy Materials Corp., Frontier Energy Solution, Fujifilm, Fujikura, GCL Suzhou Nanotechnology Co., Ltd., Greatcell Energy, Hangzhou Microquanta, Heiking PV Technology Co., Ltd., Hubei Wonder Solar, Hunt Perovskite Technologies (HPT), InfinityPV, Jinkosolar, Kyocera, LG Chem, Li Yuan New Energy Technology Co., Merck, Microquanta Semiconductor, Oxford PV, Panasonic, Saule Technologies, Sharp, Solartek, Solaronix SA, Solliance, Tandem PV, Toshiba, Trina Solar, WonderSolar, Other Prominent PlayersBASF SE, Oxford PV, GCL, Hubei Wonder Solar, Swift Solar, Merck, and other prominent players. |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

FREQUENTLY ASKED QUESTIONS

The global perovskite solar cells market was valued at USD 1.94 billion in 2025. Driven by rapid industrialization, the market is projected to reach USD 24.19 billion by 2035, expanding at a robust CAGR of 28.7% during the forecast period 2026–2035.

Perovskite technology is rapidly approaching cost parity. A 2025 analysis estimates current manufacturing costs at USD 0.57 per Watt, with projections dipping to USD 0.29–0.42 per Watt at full scale. Furthermore, techno-economic studies indicate a potential Levelized Cost of Electricity (LCOE) of USD 0.051 per kWh, challenging fossil fuel competitiveness.

The technology has successfully breached the theoretical limits of silicon. As of 2025, LONGi set a certified record for silicon-perovskite tandem cells at 34.85%, while JinkoSolar achieved 33.84% with N-type TOPCon tandems. These figures validate that perovskites offer superior power density for next-generation energy needs.

UtmoLight is a frontrunner in the perovskite solar cells market, having launched a 1 GW production line in China capable of producing 1.8 million modules annually. Other key players include Renshine Solar, constructing a gigawatt-scale factory, and Oxford PV, which has commenced commercial shipments to U.S. utilities.

Yes, significant strides have been made. Microquanta modules are now designed with a targeted lifespan of 25 years, enabling use in building materials. Additionally, University of Surrey researchers demonstrated cells maintaining performance for 1,530 hours under extreme conditions, proving readiness for outdoor environments.

Rigid modules for utility-scale projects dominate with an 82% revenue share, leveraging existing solar farm infrastructure. Simultaneously, Building Integrated Photovoltaics (BIPV) creates high value, holding a 23% share by utilizing semi-transparent cells for windows and facades in Net-Zero architecture.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |