Battery as a service Market: Product Type – Stationary and Mobile/Portable; By Service Type – Subscription (Rental) and Pay Per Use; By Vehicle Type - 2 & 3-Wheeler, Passenger Car, Light Commercial Vehicle (LCV), Heavy Commercial Vehicle (HCV), and Others; and By Region); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: Jul-2025 | Format:| Report ID: AA0422212 | Delivery: 2 to 4 Hours

![pdf]()

![powerpoint]()

![excel]()

Market Scenario

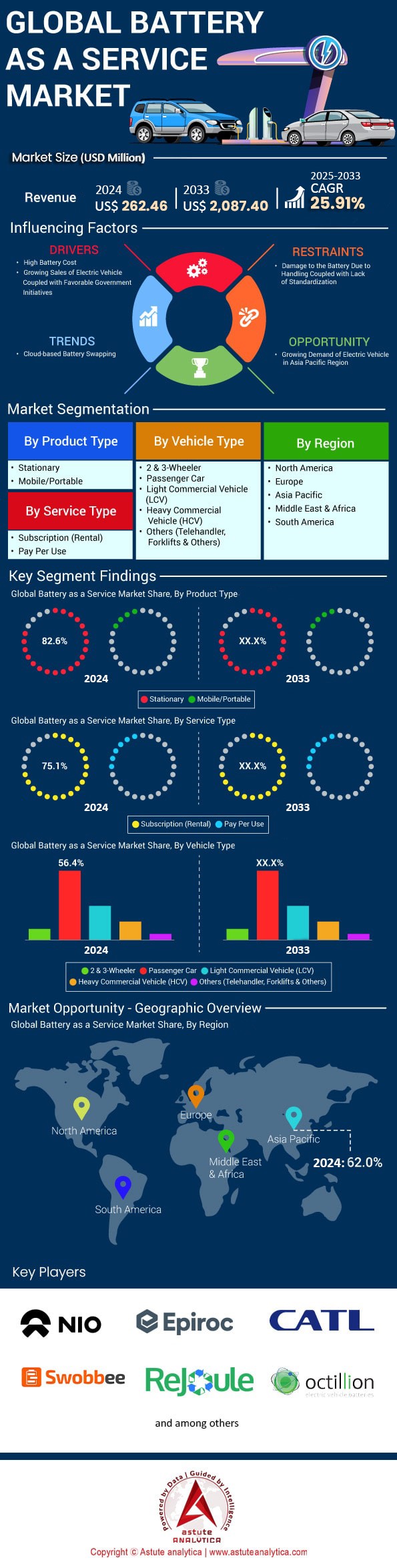

Battery as a service market was valued at US$ 262.46 million in 2024 and is estimated to reach US$ 2,087.40 million by the end of 2033 at a CAGR of 25.91% over the forecast period 2025-2033.

The battery as a service market is undergoing extraordinary growth. This growth is exemplified by the success of Gogoro, which has established a vast network of over 12,000 GoStations that have collectively supported more than 650 million battery swaps globally. Furthermore, NIO operates 900 Power Swap stations, capable of completing up to 312 battery swaps per day, showcasing the efficiency of automated battery swapping solutions. Gogoro alone handles approximately 340,000 daily swaps in Taiwan, demonstrating the increasing demand for such services. The market has also been bolstered by advancements in battery technology, including the adoption of lithium iron phosphate batteries, which offer enhanced longevity and cost-effectiveness for service providers.

In terms of regional performance, the Asia-Pacific region continues to dominate the battery as a service market, holding a significant 40.35% market share. China is a leader here, boasting over 1.15 million public charging stations while also planning to exceed 16,000 battery swap stations by 2025 to cater to growing EV adoption. Europe, meanwhile, is driving innovation with over 70,000 fast chargers in operation, supported by favorable regulations and robust infrastructure development. In North America, the United States remains a key player, with an infrastructure of 28,000 fast chargers supporting the burgeoning EV market. The automotive industry, particularly electric vehicle manufacturers and fleet operators, is the primary driver of demand for these services. Additionally, the logistics and transportation sectors are increasingly adopting battery swapping models, as evidenced by NIO users completing over 4 million battery exchanges—a clear indicator of growing acceptance among consumers.

The battery as a service market’s future is being shaped by cutting-edge innovations and strategic collaborations. Wireless charging solutions and Dynamic Wireless Power Transfer systems, currently being piloted in nations like Sweden and Italy, are expected to revolutionize the sector further. The integration of cloud-based platforms within the Battery as a Service ecosystem is another key development, with China accounting for more than 85% of global battery-swapping infrastructure deployments. This integration allows for remote diagnostics and over-the-air updates, significantly reducing EV downtime from the typical 30-60 minutes required for conventional charging to just 3-5 minutes via battery swapping. The industry’s rapid adoption of subscription-based and pay-per-kilometer charging models is helping make electric mobility more accessible and addressing long-standing challenges such as range anxiety and the high upfront costs of EV ownership.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: High battery costs pushing consumers toward subscription-based ownership models

The escalating costs of electric vehicle batteries are fundamentally reshaping the battery as a service market, with average battery pack prices hovering around US$ 12,000 to US$ 15,000 for standard EVs in 2024. This financial burden has catalyzed a paradigm shift toward subscription models, where companies like NIO offer battery subscriptions starting at US$ 142 monthly, eliminating the need for upfront battery purchases worth US$ 10,000 or more. Major automakers are responding to this cost pressure by launching innovative leasing programs, with Stellantis introducing battery leasing options that reduce vehicle purchase prices by up to US$ 8,500. The financial implications extend beyond individual consumers, as fleet operators managing 500-vehicle fleets can save approximately US$ 6 million in initial capital expenditure through battery as a service market solutions, making electric transitions more financially viable for commercial operations.

The subscription model's attractiveness is further amplified by warranty considerations and battery degradation concerns, with replacement costs reaching US$ 20,000 for premium electric vehicles. Market analysis reveals that consumers adopting battery subscription services experience total ownership costs reduced by US$ 3,200 over five years compared to traditional ownership models. Leading markets like China have witnessed over 2 million battery subscription enrollments in 2024, generating recurring revenues exceeding US$ 340 million monthly for service providers. Financial institutions are actively supporting this transition, with US$ 2.5 billion in dedicated financing allocated for battery leasing infrastructure development. The model's success is evident in markets where battery subscriptions account for 15,000 new enrollments weekly, demonstrating how cost considerations are driving widespread adoption of battery as a service market offerings among price-conscious consumers and businesses alike.

Trend: Solid-state batteries emerging as next-generation technology for enhanced performance

Solid-state battery technology represents a transformative advancement for the battery as a service market, with major manufacturers investing over US$ 7 billion collectively in development facilities expected to commence production by 2027. These next-generation batteries promise energy densities reaching 500 Wh/kg, nearly double current lithium-ion capabilities, enabling electric vehicles to achieve ranges exceeding 800 kilometers on a single charge. Toyota's breakthrough in solid-state technology includes plans for a production facility capable of manufacturing 10,000 battery units monthly by 2028, specifically designed for integration into battery swapping infrastructure. The technology's rapid charging capabilities, achieving 80% charge in under 10 minutes, make it particularly attractive for battery swapping operations where turnaround time is critical. QuantumScape's solid-state cells have demonstrated over 1,000 charging cycles in testing, addressing longevity concerns that plague current battery as a service market offerings.

The commercial viability of solid-state batteries is accelerating, with production costs projected to reach US$ 65 per kWh by 2030, making them competitive with current lithium-ion technologies. Samsung SDI's pilot production line has already produced 2,000 prototype cells for testing in battery swapping stations across South Korea, demonstrating real-world applicability. These batteries offer operational advantages including functioning in temperatures ranging from -40°C to 85°C, eliminating the need for complex thermal management systems that add US$ 2,000 to current battery pack costs. Investment momentum continues building, with venture capital firms committing US$ 1.8 billion to solid-state battery startups in 2024 alone. The technology's safety profile, eliminating flammable liquid electrolytes, reduces insurance costs for battery service providers by approximately US$ 500 per unit annually, further enhancing the economic proposition for battery as a service market operators.

Challenge: Infrastructure development requiring massive capital investment for swapping networks

The expansion of battery swapping infrastructure represents the most capital-intensive challenge facing the battery as a service market, with individual swapping stations requiring investments between US$ 400,000 and US$ 600,000 for full automation capabilities. China's ambitious infrastructure rollout exemplifies this challenge, with companies like CATL and Aulton committing US$ 3.2 billion to establish 5,000 swapping stations by 2026. Each station requires sophisticated robotics capable of completing 312 daily swaps, automated battery storage systems holding 13 to 20 battery packs, and high-capacity electrical connections drawing 480 kW from the grid. The land acquisition costs alone average US$ 150,000 per urban location, while rural installations face additional challenges requiring US$ 80,000 in grid upgrade investments. European markets face even steeper costs, with Swobbee's network expansion in Germany requiring US$ 750,000 per station due to stringent safety regulations and higher construction costs.

The financial complexity extends beyond initial construction, as operational expenses for a single battery as a service market station reach US$ 25,000 monthly, including electricity costs, maintenance, and staffing. Network effects demand substantial scale, with analysis indicating that profitable operations require minimum networks of 50 stations within metropolitan areas, representing total investments exceeding US$ 25 million. Infrastructure standardization challenges compound costs, as different vehicle manufacturers require unique battery handling equipment costing US$ 120,000 per compatible model. Power grid limitations pose additional hurdles, with utilities requiring US$ 2 million in substation upgrades to support clusters of five or more swapping stations. Despite these challenges, infrastructure investments are accelerating, with global funding for battery swapping networks reaching US$ 8.7 billion in 2024, as investors recognize the long-term potential of the battery as a service market ecosystem.

Segmental Analysis

By Product Type

The stationary segment continues to dominate the battery as a service market with a commanding 82.6% revenue share, driven by unprecedented demand for grid-scale energy storage solutions reaching US$ 4.2 billion in investments during 2024. Major utility companies like NextEra Energy have deployed over 15,000 MWh of stationary battery systems through BaaS agreements, eliminating upfront capital requirements of US$ 800 million. These systems now power critical infrastructure across 2,500 hospitals and 800 data centers globally, with each installation averaging 2.5 MWh capacity. The telecommunications sector alone has contracted for 12,000 stationary battery units in 2024, ensuring uninterrupted service for 5G networks spanning 180 metropolitan areas. Industrial facilities are increasingly adopting stationary BaaS solutions, with Amazon Web Services implementing battery as a service market solutions across 45 data centers, saving US$ 120 million in capital expenditure while guaranteeing 99.999% uptime reliability through managed battery systems.

The economic advantages of stationary BaaS installations become evident through operational metrics, with providers managing fleets exceeding 50,000 battery units achieving cost reductions of US$ 45 per kWh through optimized maintenance schedules and predictive analytics. Tesla's Megapack BaaS program exemplifies this scale, delivering 3,916 MWh of storage capacity across 14 countries with zero upfront costs for utilities. Grid operators report saving US$ 2.3 million annually per 100 MWh installation through demand response capabilities and peak shaving services. The manufacturing sector has embraced stationary solutions enthusiastically, with automotive plants installing 8,500 units collectively to manage production line continuity. Regional growth patterns show North American installations reaching 25,000 units, while European deployments exceeded 18,000 units in 2024, reflecting strong regulatory support for renewable energy integration through battery as a service market offerings.

By Service Type

The subscription model maintains its leadership position in the battery as a service market with 75.1% revenue contribution, revolutionizing how businesses and consumers access battery technology without substantial capital investments. Contemporary subscription platforms have evolved beyond simple rental agreements, with companies like Gogoro processing 11 million monthly transactions across their subscriber base, generating recurring revenues of US$ 165 million. The sophistication of these platforms is evident in their integration capabilities, connecting with 450 different IoT systems and providing real-time battery health monitoring for over 3.2 million active subscriptions globally. Financial institutions have recognized this opportunity, with JP Morgan and Goldman Sachs collectively financing US$ 2.8 billion in subscription-based battery infrastructure projects during 2024. Enterprise clients particularly value subscription flexibility, with Fortune 500 companies subscribing to battery as a service market solutions for 125,000 vehicles, avoiding battery depreciation risks worth US$ 1.5 billion.

The technological infrastructure supporting subscription services has matured significantly, with cloud-based platforms managing 8.5 million battery assets simultaneously while processing 500,000 daily transactions. Subscription pricing models have diversified, offering tiered services ranging from US$ 89 monthly for basic passenger vehicle batteries to US$ 1,250 for commercial truck applications. Customer retention rates demonstrate the model's success, with providers reporting 18-month average subscription durations generating lifetime values exceeding US$ 2,100 per customer. The predictive maintenance capabilities embedded in subscription platforms reduce battery failures by identifying issues across 2.7 million units monthly, saving operators US$ 340 million in emergency replacements. Major automotive manufacturers including Stellantis and Renault have launched proprietary subscription platforms, collectively serving 890,000 subscribers and projecting US$ 3.2 billion in subscription revenues by 2026 through their battery as a service market offerings.

By Vehicle Type

Passenger cars continue to lead the battery as a service market with 56.5% revenue share, reflecting the accelerating adoption of electric vehicles among urban consumers seeking affordable ownership alternatives. The segment's dominance is exemplified by NIO's achievement of facilitating 30 million battery swaps for passenger vehicles, with their ES8 and ET7 models accounting for 185,000 active BaaS subscriptions generating monthly revenues of US$ 26 million. Urban markets have witnessed explosive growth, with Shanghai alone hosting 275 battery swap stations serving 45,000 daily passenger car swaps, while Beijing's network handles 38,000 daily exchanges. The financial benefits are compelling, with BaaS-enabled passenger cars priced US$ 10,000 lower than traditional purchase options, making premium electric vehicles accessible to 2.3 million additional consumers in 2024. European markets demonstrate similar trends, with Renault's Zoe battery as a service market program attracting 156,000 subscribers who collectively save US$ 468 million compared to outright battery purchases.

The operational efficiency of passenger car BaaS networks has reached impressive scales, with automated stations completing battery swaps in 2.5 minutes, faster than conventional refueling. Fleet operators managing ride-hailing services report remarkable results, with Didi's 25,000 BaaS-equipped vehicles completing 8.7 million trips monthly while reducing operational costs by US$ 1,200 per vehicle annually. The technology's maturity is evident in battery longevity data, showing passenger car batteries maintaining optimal performance across 1,500 swap cycles, equivalent to 450,000 kilometers of driving. Insurance companies have responded favorably, offering US$ 800 annual premium reductions for BaaS-enrolled vehicles due to professional battery maintenance. Manufacturing capacity has expanded accordingly, with CATL's dedicated passenger car battery production reaching 50,000 units monthly, specifically designed for swapping applications in the growing battery as a service market ecosystem.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific Dominates Global Battery Swapping Infrastructure with China Leading

Asia Pacific's dominance in the battery as a service market stems from 14 million annual EV sales in 2024. China leads with 11 million units, followed by India (2 million). China invests US$ 12.5 billion in battery swapping networks, establishing 3,200 stations across 150 cities. Primary end users include ride-hailing fleets (1.2 million vehicles), logistics companies (850,000 vehicles), and public transportation (320,000 buses). Five dominant players operate extensively: CATL (1,800 stations), NIO (1,500 stations), Aulton (800 facilities), Gogoro (12,000 exchange points in Taiwan), and Geely's EVOGO (450 stations). These companies process 2.8 million daily swaps, generating US$ 480 million monthly. Growth drivers include government mandates for commercial fleet electrification and US$ 3.8 billion annual subsidies for infrastructure development.

United States Leverages Federal Funding to Transform Commercial Fleet Operations

The United States spearheads the battery as a service market with 1.4 million EV sales and US$ 1.9 billion federal infrastructure funding through 2026. Amazon leads commercial adoption with 25,000 BaaS delivery vans across 120 cities, while Walmart deploys 8,500 units for last-mile delivery. California hosts 145 swap stations, Texas follows with 85 installations, and Florida adds 60 facilities serving tourism and logistics sectors. Ample dominates infrastructure with 180 automated stations processing 45,000 daily swaps. Federal tax incentives worth US$ 7,500 per commercial vehicle accelerate fleet transitions, with 250,000 vehicles expected to adopt BaaS by 2026. Municipal governments in 85 cities commit US$ 890 million for public fleet conversions. Technology partnerships between General Motors, Ford, and battery providers create standardized solutions, while venture capital invests US$ 2.3 billion in emerging BaaS startups targeting specialized applications.

Europe Accelerates Battery Infrastructure Through Stringent Environmental Regulations and Investments

Europe maintains second position in the battery as a service market with 2.96 million EV sales in 2024. Germany leads with 850,000 units, France follows with 620,000, and Norway achieves 380,000 sales. Major players Stellantis, Renault, and Swobbee operate 2,100 swap stations across 12 countries. Fleet operators dominate usage: Deutsche Post DHL operates 18,000 BaaS-enabled delivery vehicles, while Amsterdam, Paris, and Berlin municipal authorities manage 5,500 electric buses through subscriptions. The market generates US$ 1.85 billion annually, supported by EU funding of US$ 2.2 billion for infrastructure through 2026. Commercial adoption accelerates through regulatory pressure, with logistics companies transitioning 45,000 vehicles to BaaS models. Urban centers prioritize battery swapping to meet air quality standards, installing 180 stations monthly across major cities, while Nordic countries leverage renewable energy abundance to power extensive networks.

North America Focuses Commercial Fleets Driving Battery Service Market Growth

North America's battery as a service market grows steadily with US recording 1.4 million EV sales and Canada adding 185,000 units in 2024. Commercial applications lead adoption: Amazon deploys 25,000 BaaS-equipped vans across 120 metropolitan areas, while FedEx and UPS operate 15,000 battery-swappable vehicles combined. Infrastructure providers include Ample (180 automated stations), BattSwap, and NuEnergy establishing networks in California and Texas. The region invests US$ 3.6 billion addressing geographical challenges through strategic corridor development. Government support includes US$ 1.9 billion via Infrastructure Investment and Jobs Act, planning 500 stations by 2026. Municipal fleets represent growth opportunities, with 85 cities committing to BaaS adoption for 12,000 vehicles. The battery as a service market benefits from technology partnerships between automakers and energy companies, creating integrated solutions for long-haul trucking and last-mile delivery segments.

Top Players in Global Battery as a Service Market

- NIO

- Epiroc

- Global Technology Systems, Inc.

- Contemporary Amperex Technology Co

- Swobee

- Harding Energy, Inc.

- ReJoule

- Octillion

- Numocity

- Skoon

- Numocity

- Skoon

- Other Prominent Players

Market Segmentation Overview:

By Product Type:

- Stationary

- Mobile/Portable

By Service Type:

- Subscription (Rental)

- Pay Per Use

By Vehicle Type:

- 2 & 3-Wheeler

- Passenger Car

- Light Commercial Vehicle (LCV)

- Heavy Commercial Vehicle (HCV)

- Others (Telehandler, forklifts and others)

By Region:

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 262.46 Million |

| Expected Revenue in 2033 | US$ 2,087.40 Million |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Mn) |

| CAGR | 25.91% |

| Segments covered | By Product Type, By Service Type, By Vehicle Type, By Region |

| Key Companies | NIO, Epiroc, Global Technology Systems, Inc., Contemporary Amperex Technology Co, Swobee, Harding Energy, Inc., ReJoule, Octillion, Numocity, Skoon, Numocity, Skoon,Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Choose License Type

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |