Bearing Market: By Product (Ball Bearings, Roller Bearings, Mounted Bearings, Linear Bearings and Others); Size (30 to 40 mm, 41 to 50 mm, 51 to 60 mm and others); material (Specialty Steel Alloys, Plastics and Ceramics); Industry (Automotive and Industrial); Industrial (OEM and Aftermarket); and Region—Industry Dynamics, Market Size and Opportunity Forecast for 2025–2033

- Last Updated: Aug-2025 | Format:| Report ID: AA0322183 | Delivery: 2 to 4 Hours

![pdf]()

![powerpoint]()

![excel]()

Market Scenario

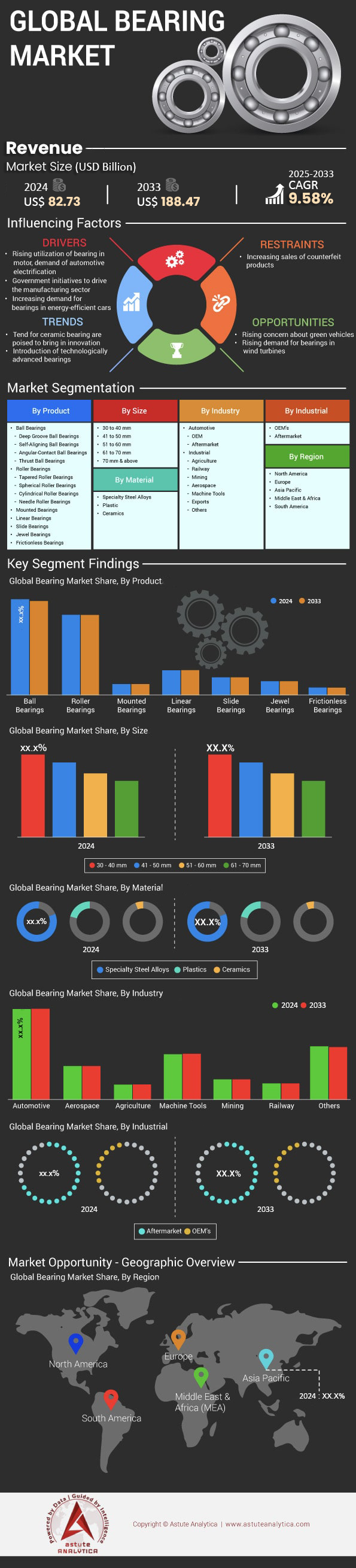

Bearings market was valued at US$ 82.73 billion in 2024 and is projected to hit the market valuation of US$ 188.47 billion by 2033 at a CAGR of 9.58% during the forecast period 2025–2033.

The demand landscape for the global market is being fundamentally reshaped by the twin forces of electrification and automation. For industry stakeholders, this signifies a crucial pivot from traditional components to specialized, high-performance solutions. The electric vehicle sector's demand is crystallizing into significant value, with the global EV bearings market valued at US$ 2.64 billion in 2024 and China's market alone generating US$ 939.7 million in revenue the same year. This is driven by production forecasts expecting over 30 million EVs by 2030. Concurrently, the rise of automation, with over 54 million vehicles expected to have some level of automation by 2024, necessitates precision bearings. In response, key players are innovating rapidly; NSK Ltd. launched bearings with embedded sensors in January 2024, while SKF introduced a new line of ceramic ball-equipped bearings in February 2025.

Massive investments in infrastructure and the clean energy transition are creating substantial, long-term revenue streams for the global bearings market. The wind power bearing market was valued at USD 5,903.91 million in 2024, bolstered by a record 38.4 GW increase in U.S. solar capacity in 2024 and a new €5 billion EIB initiative for European wind energy launched in August 2024. This signals a robust pipeline for bearing manufacturers. Similarly, railway modernization is a significant growth driver. The global railway sliding bearing market was valued at US$ 1.4 billion in 2024. This is supported by major government funding, including a US$ 249.5 million program in the United States and anticipated investments in India exceeding US$ 7.6 billion by 2025, ensuring sustained demand for durable rail-specific bearings.

The aerospace sector's resurgence provides another lucrative frontier, with its bearings market expected to reach US$ 9.6 billion in 2025. This growth is directly tied to the global commercial aviation fleet's projected expansion to over 36,000 aircraft by 2033. Leading manufacturers are capitalizing on this widespread growth. Schaeffler AG reported strong revenues of 5.9 billion euros in the first quarter of 2025. For the fiscal year ending March 31, 2025, NTN Corporation's net sales reached 825,587 million yen. In a key regional market, Schaeffler India posted a profit of Rs 938.86 crore for the year ended 2024. These figures demonstrate that companies aligned with these high-growth sectors are realizing tangible financial gains, a critical insight for stakeholders evaluating market positions.

Key Findings in Bearings Market

- By type, roller bearings contributed the highest market share of 43%

- By size, 30 to 40 mm bearings dominated the market with around 36% share

- By material, specialty steel alloys segment dominated the bearing market with around 89% share

- By industry, industrial segment accounted for the highest revenue share of 62%

- By distribution channel, OEMs are leading the market by generating more than 65% market share

- Asia Pacific is largest market with over 45% market revenue coming from this region alone

- Global bearings market set to attain valuation of US$ 188.47 billion by 2033

To Get more Insights, Request A Free Sample

Specialization, Green Energy, and IoT Integration Reshape Future Bearings Market Landscape

- Accelerated Specialization for Electric Mobility: A primary trend is the shift from generic automotive bearings to highly specialized components for electric vehicles (EVs). These new bearings must manage higher speeds, different load profiles, and offer insulation properties. This trend is quantified by the EV bearings market reaching a value of USD 2.64 billion in 2024 and underscored by manufacturers like SKF introducing specific ceramic ball-equipped bearings for EVs in February 2025. This move towards specialization is a direct response to the unique engineering demands of the burgeoning electric mobility sector.

- Dominance of Sustainable Infrastructure Projects: The global push for renewable energy is creating a massive and sustained demand pipeline for large, durable bearings. The Wind Power Bearing Market, valued at USD 5,903.91 million in 2024, is a focal point of this trend. Major financial commitments, such as the European Investment Bank's €5 billion initiative launched in August 2024 to support wind energy, solidify this as a long-term growth pillar, demanding robust components capable of withstanding extreme operational conditions for decades.

- Integration of Smart Technology and IoT: The market is rapidly moving towards intelligent bearings that incorporate embedded technology. This evolution transforms the bearing from a simple mechanical component into a smart, data-generating asset for Industry 4.0. The launch of bearings with embedded sensors by NSK Ltd. in January 2024 exemplifies this trend. These smart bearings enable real-time condition monitoring and predictive maintenance, offering significant value by increasing operational efficiency and reducing downtime for end-users across all heavy industries.

Electric Drivetrains and Autonomy Are Forging a New Bearings Market Demand

The global demand for bearings is being profoundly redefined by the dual revolutions in mobility: electrification and automation. This shift is not gradual; it is a seismic event quantified by massive production and sales figures. In 2024 alone, Chinese manufacturer BYD sold a remarkable 4,272,145 new energy vehicles, while China’s total NEV production reached 9.587 million units. In the U.S., Ford demonstrated this trend by selling 285,291 electric and hybrid vehicles in 2024, including 33,510 units of its F-150 Lightning truck. Projections show annual EV production will exceed 30 million units by 2030, creating a vast market for specialized bearings.

The move towards automation is equally impactful, with the number of vehicles featuring some autonomy expected to surpass 54 million by the end of 2024. This evolution demands smarter components. Bearing manufacturers are responding decisively. Schaeffler's E-Mobility division secured a massive 5.1 billion euros in orders in 2024. Key innovations include NSK Ltd.'s launch of bearings with embedded sensors in January 2024 and SKF's introduction of ceramic ball-equipped bearings for EVs in February 2025. Even the aerospace sector, with Airbus registering 494 gross orders in the first half of 2025, is driving demand for bearings compatible with increasing flight automation.

Sustainable Infrastructure Investments Are Building a Foundation for Long-Term Bearing Growth

A worldwide commitment to sustainable infrastructure is creating a powerful and long-lasting demand for durable, high-performance bearings. This trend in the bearings market is most visible in the renewable energy sector. The United States anticipated a record increase of 38.4 GW in solar capacity by the end of 2024, while India added an unprecedented 29.52 GW of renewable capacity in its 2024-25 fiscal year. This translates directly to component orders, evidenced by turbine maker Vestas securing firm orders for 3,369 MW of capacity in the first quarter of 2025.

Major financial backing, such as the European Investment Bank's €5 billion initiative for wind energy launched in August 2024, and active projects like Adani's 250 MW wind plant commissioned in July 2024, guarantee a robust project pipeline. This infrastructure boom extends to transportation, with the U.S. allocating $249.5 million in 2024 to modernize railways and India's rail investments projected to exceed $7.6 billion by 2025. The broader industrial ecosystem supporting bearings market growth is also thriving, with Japan's machine tool orders reaching JPY 1,485.1 billion in 2024. Companies are reaping the benefits; Schaeffler's industrial division generated revenue of 1,627 million euros in Q1 2025, and Boeing's delivery of 348 aircraft in 2024 further fed this industrial demand.

Segmental Analysis

By Product Type: Roller Bearings are Champions in Driving Revenue and Performance Across Industries

Roller bearings decisively lead the global bearings market, contributing over 43% of its total revenue. Their dominance is not accidental but a direct result of their superior design, which provides significant advantages in load-carrying capacity and operational durability. Unlike ball bearings, roller bearings utilize line contact, which distributes force over a wider area. This fundamental difference makes them inherently stronger and far more resistant to shock and impact, establishing them as the premier choice for heavy-load industrial applications. Their robust construction is a key reason they are engineered to handle heavier loads than their counterparts, a critical requirement in demanding sectors such as construction and mining where immense force and shock resistance are daily operational realities. This intrinsic strength underpins their commanding market position.

- The strategic lubrication of roller bearings is a critical practice for extending their service life and ensuring optimal performance in demanding industrial environments.

- In the power generation sector, roller bearings are essential components for crucial equipment like turbines and pumps, valued for their ability to manage large loads and high temperatures.

- The consistent growth in global vehicle production acts as a significant and direct driver for the roller bearings market, as these components are vital for smooth vehicle operation.

The versatility of roller bearings market is further amplified by their various geometries, each tailored for specific needs. Tapered roller bearings are uniquely capable of supporting both axial and radial loads simultaneously, making them indispensable in industries like agriculture and for engine motors. Spherical roller bearings are engineered to accommodate misalignment alongside heavy loads, making them the go-to solution for industrial gearboxes and large metal industries. For applications demanding high radial load capacity, such as in electric motors and pressure rollers, cylindrical roller bearings are the favored option. Their role is also expanding in the automotive sector, where they are increasingly specified in modern vehicles due to their superior load-bearing capacity and suitability for higher speeds, solidifying their extensive and varied application base.

By Size: 30-40mm Size Band is Versatile Core of the Modern Bearings Market

Commanding over 36% of the market share, bearings within the 30 to 40 mm size range have become the industry's sweet spot. This dominance in the bearings market is driven by immense demand from a vast array of common industrial and automotive applications where this size offers an optimal balance of load capacity, performance, and compact design. This versatility makes it a preferred choice for engineers globally. Specifically, linear ball bearings with a 30mm inner diameter and 40mm outer diameter are frequently selected for applications where radial space is limited. The closed design of these linear bearings makes them perfectly suited for effective use on shafts. This adaptability across countless common applications is the primary factor behind the size's significant market leadership and its central role in the overall bearings market.

- Full complement type needle roller bearings within this size range are specifically engineered for heavy-load applications that operate at low-speed rotation.

- Machined needle roller bearings with a 40mm bore size are purpose-built to provide high load-carrying capacity within radially compact arrangements.

- Certain 40mm needle roller bearing designs omit an inner ring, a feature that enhances running accuracy as performance is not influenced by the inner ring's assembly.

The utility of this size category is showcased by the variety of bearing types available. Heavy closed-end drawn cup needle roller bearings, such as the 30x40x30mm size, provide significant economic advantages, making them ideal for mass-produced items. At the same time, lightweight shell-type needle roller bearings in this size can handle impressively large load ratings. Further expanding its application scope in the bearings market, double row ball bearings with a 40mm inner diameter are integral to pumps, compressors, and automotive drives, where they support high-speed applications and moderate loads. For even more demanding scenarios, angular contact ball bearings with a 40mm inner diameter are designed to handle high rotational speeds and significant dynamic loads, proving the exceptional adaptability of this dominant size segment.

By Industry: Industrial Bearings Powering Global Industries and Dominating Market Revenue Streams

Industrial bearings are the undisputed frontrunners of the bearings market, contributing over 62% of its total revenue. This commanding lead over the automotive segment is propelled by vast and escalating demand from a diverse range of industrial sectors. Key drivers include rapid industrialization, particularly across the Asia-Pacific region, and massive global investments in infrastructure projects. These bearings are critical, irreplaceable components in the heavy machinery and equipment that power manufacturing, construction, mining, energy, and aerospace. Underscoring this trend, industrial machinery held a dominant market position in 2023, accounting for a massive share of bearing applications due to its extensive use in heavy equipment. This dynamic confirms the industrial segment's powerful influence on the global bearings market.

- The mining and construction sectors specifically demand exceptionally robust bearings that can reliably withstand heavy loads and harsh environmental conditions.

- A significant technological trend is the emergence of smart bearings, which are equipped with sensors to enable predictive maintenance and prevent downtime.

- Stringent safety and compliance regulations within the aerospace industry directly drive the production of specialized, high-performance bearings for aircraft parts.

The growth of the industrial segment in the bearings market is fueled by several powerful trends shaping modern industry. The rising adoption of automation and robotics in various sectors is creating a strong demand for high-precision and highly reliable industrial bearings. This is complemented by the manufacturing sector's broader automation push to enhance productivity. Furthermore, the global expansion of the renewable energy sector, especially in wind and solar power, has created a substantial new need for high-performance bearings capable of withstanding extreme operational conditions. In response, there is a clear trend towards using innovative materials like ceramics and composites to achieve better wear and heat resistance. This is coupled with a growing emphasis on energy efficiency, leading to innovations in bearing designs that minimize friction.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By Material: Specialty Steel Alloys are Unyielding Material Foundation of the Global Bearings Market

Specialty steel alloys are the bedrock of modern bearing production, used in more than 89% of all bearings manufactured worldwide. This overwhelming preference stems from the material's engineered properties, which provide the exceptional performance characteristics vital for the demanding conditions bearings endure. These alloys are formulated to offer superior mechanical strength, including exceptional wear resistance to withstand the constant abrasive forces of operation. Furthermore, they provide excellent corrosion resistance, which protects the components from degradation when deployed in harsh or chemically active environments. While standard chrome steel offers good durability, specialty steels are essential for applications requiring maximum performance and reliability, making them a non-negotiable choice for manufacturers and a key pillar of the bearings market.

- A critical property required of bearing steel is "rolling fatigue strength," which ensures smooth, long-lasting rotation under powerful and continuous forces.

- The historical development of bearing steel was driven by the industrial need for a specialized iron alloy that could uniquely meet the demands of rolling applications.

- Within the chemical processing industry, the ability of specialty steels like AISI 304 to effectively resist acids and alkaline environments is a crucial advantage.

Different steel compositions are selected for their distinct benefits in specific applications. High-carbon chromium steel, including grades like GCr15 and 52100, is a popular choice in the bearings market due to its high hardness and superior load capacity, making it better suited for heavy-duty applications compared to alternatives. This material is engineered to deliver superior fatigue strength, which ensures a prolonged service life under constant cyclic loading. In the food processing industry, a specialty steel like AISI 440C stainless steel is crucial for its high corrosion resistance and durability across a range of temperatures. For the most severe environments, specialty steels are unmatched in their high strength, stability, and resistance to extreme temperatures, solidifying their foundational role.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific: A Manufacturing and EV Juggernaut Fueling Bearing Demand

The Asia Pacific region continues to be the undisputed engine of the global bearings market, driven by its immense manufacturing base and leadership in the electric vehicle (EV) transition. China's automotive sector is a primary catalyst; BYD, a key player, sold a staggering 4,272,145 vehicles in 2024, with a significant portion serving its domestic market. This massive production volume creates a foundational demand for a vast array of automotive bearings. In Japan, the industrial machinery sector provides a steady stream of demand, with total machine tool orders reaching a substantial JPY 1,485.1 billion in 2024, of which JPY 1,043.6 billion came from foreign orders, indicating the global reliance on Japanese capital goods.

India is emerging as a critical growth frontier in the regional bearings market, powered by government initiatives and a burgeoning industrial sector. The country added a record-breaking 29.52 GW of renewable energy capacity in the fiscal year 2024-25, creating immense demand for specialized wind and solar bearings. Furthermore, India’s Index of Industrial Production for manufacturing stood at a strong 156.2 in December 2024, signaling robust factory output. This industrial growth potential is reflected in corporate earnings, with Schaeffler India reporting a solid net profit of ₹287.11 crore in the first quarter of 2025. Even company-specific sales in the region, such as Schaeffler's Greater China revenue, which stood at 991 million euros in Q1 2024, highlight the scale of this pivotal market.

Europe: Aerospace and Green Energy Investments Drive High-Value Bearing Sales

Europe's demand for bearings is increasingly shaped by high-value industries and a strategic focus on sustainability and advanced manufacturing. The aerospace sector is a significant contributor; Airbus, a European manufacturing giant, delivered 323 commercial aircraft in the first half of 2024 and registered 494 gross commercial aircraft orders in the first half of 2025, feeding a continuous need for high-precision aerospace bearings. In a clear move to bolster the region's green energy supply chain, the European Investment Bank launched a major €5 billion initiative in August 2024 specifically to support wind energy manufacturing, a direct stimulant for the wind power bearing market.

Corporate performance within the regional bearings market underscores its market strength. Schaeffler AG, a key German player, reported substantial revenue of 5.9 billion euros in the first quarter of 2025 alone. Its dedicated Bearings & Industrial Solutions division generated revenue of 1,627 million euros during that same period. The automotive sector remains vital, with the Volkswagen Group making significant deliveries across the continent. These activities are supported by a strong industrial backbone, evidenced by Germany's consistent flow of industrial orders. While specific data points vary, the collective momentum from aerospace, renewable energy investments, and strong corporate revenues solidifies Europe's position as a critical, high-value hub in the global Bearings market.

North America: Automotive Sales and Aerospace Powering Regional Bearing Demand

North America presents a dynamic and mature bearings, underpinned by a robust automotive sector and a world-leading aerospace industry. The U.S. light vehicle market demonstrated its strength by closing 2024 with total sales of 15.98 million units, providing a massive and consistent demand base for automotive bearings. The shift to electrification is also a key driver, with Ford reporting the sale of 285,291 electric and hybrid vehicles in 2024, including 33,510 units of its F-150 Lightning electric truck. This transition towards heavier electric vehicles creates new opportunities for specialized, high-load bearing solutions.

The region's aerospace and industrial sectors are crucial demand drivers for the bearings market. U.S. manufacturer Boeing delivered a total of 348 commercial aircraft in 2024, each requiring a multitude of sophisticated bearings. In the industrial space, major players like Timken and Schaeffler show significant regional activity. Schaeffler's Americas division posted revenue of 1,364 million euros in the first quarter of 2024. Demand is further supported by government-led infrastructure renewal, such as the $249.5 million allocated in 2024 through the CRISI Program to enhance U.S. railway infrastructure, which directly translates to orders for rail-specific bearings. The addition of significant renewable energy capacity, including new solar and wind installations, further diversifies the demand profile of the North American Bearings market.

Recent Developments in Bearings Market

- Schaeffler Finalizes Vitesco Technologies Merger: In a landmark move for the automotive supply sector, Schaeffler AG completed its merger with Vitesco Technologies in the fourth quarter of 2024. This strategic combination creates a "Motion Technology Company" with a massive portfolio, including significant strengths in e-mobility, directly impacting the supply chain for electric vehicle bearings.

- Timken Acquires Lagersmit: In April 2024, The Timken Company acquired Lagersmit, a Netherlands-based manufacturer of highly engineered sealing solutions for marine, dredging, and other industrial applications. This acquisition expands Timken's portfolio of engineered bearings and seals, strengthening its position in the marine and industrial aftermarket.

- EIB Launches €5 Billion Fund for European Wind Manufacturing: The European Investment Bank (EIB) announced a major €5 billion fund in August 2024 to enhance the European wind energy sector's manufacturing capabilities. This funding is designed to de-risk investments and improve access to finance for companies producing components like large-diameter bearings for wind turbines.

- Adani Commissions 250 MW Wind Power Plant: In July 2024, Adani Renewable Energy Forty One Ltd., a subsidiary of Adani Green Energy, commissioned a 250 MW wind power plant in Gujarat, India. This represents a significant private investment in renewable infrastructure that requires a substantial supply of specialized wind turbine bearings.

Top Companies in the Bearing Market

- IKO International

- ISB Industries (Italcuscinetti S.p.A. a Socio Unico)

- JTEKT Corporation

- LYC Corp.

- NSK Ltd.

- NTN Corporation

- Schaeffler AG

- SKF

- Timken India Ltd.

- THK CO., Ltd.

- Other Prominent Players

Market Segmentation Overview

By Product:

- Ball Bearings

- Deep Groove Ball Bearings

- Self-Aligning Ball Bearings

- Angular-Contact Ball Bearings

- Thrust Ball Bearings

- Roller Bearings

- Tapered Roller Bearings

- Spherical Roller Bearings

- Cylindrical Roller Bearings

- Needle Roller Bearings

- Mounted Bearings

- Linear Bearings

- Slide Bearings

- Jewel Bearings

- Frictionless Bearings

- Others

By Size:

- 30 to 40 mm

- 41 to 50 mm

- 51 to 60 mm

- 61 to 70 mm

- 70 mm & above

By Material:

- Specialty Steel Alloys

- Plastic

- Ceramics

By Industry:

- Automotive

- OEM

- Aftermarket

- Industrial

- Agriculture

- Railway

- Mining

- Aerospace

- Machine Tools

- Exports

- Others

By Industrial:

- OEM’s

- Aftermarket

By Region:

- North America

- The U.S.

- Canada

- Mexico

- Europe

- The U.K.

- Germany

- France

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- ASEAN

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- South Africa

- Israel

- Rest of the Middle East & Africa

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 82.73 Bn |

| Expected Revenue in 2033 | US$ 188.47 Bn |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Bn) |

| CAGR | 9.58% |

| Segments covered | By Product, By Size, By Material, By Industry, By Industrial, By Region |

| Key players | IKO International, ISB Industries (Italcuscinetti S.p.A. a Socio Unico), JTEKT Corporation, LYC Corp., NSK Ltd., NTN Corporation, Schaeffler AG, SKF, Timken India Ltd., THK CO., Ltd., Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Choose License Type

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |