Polyisobutylene Market: By Product Type (High Molecular Weight, Medium Molecular Weight, Low Molecular Weight); Production Process (Polymerization Process, Co-polymerization Process, Other Production Techniques); Application (Adhesives & Sealants, Automotive Rubber Components, Fuel Additives, Lubricant Additives, Others); End Use Industry (Automotive, Chemical, Oil & Gas, Consumer Goods, Pharmaceuticals and Healthcare, Others); Distribution Channel (Direct Sales to End Users, Distributor Networks, Online Retail and E-commerce Platforms, Others); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: Jul-2025 | Format:| Report ID: AA02251192 | Delivery: Immediate Access

![pdf]()

![powerpoint]()

![excel]()

Market Scenario

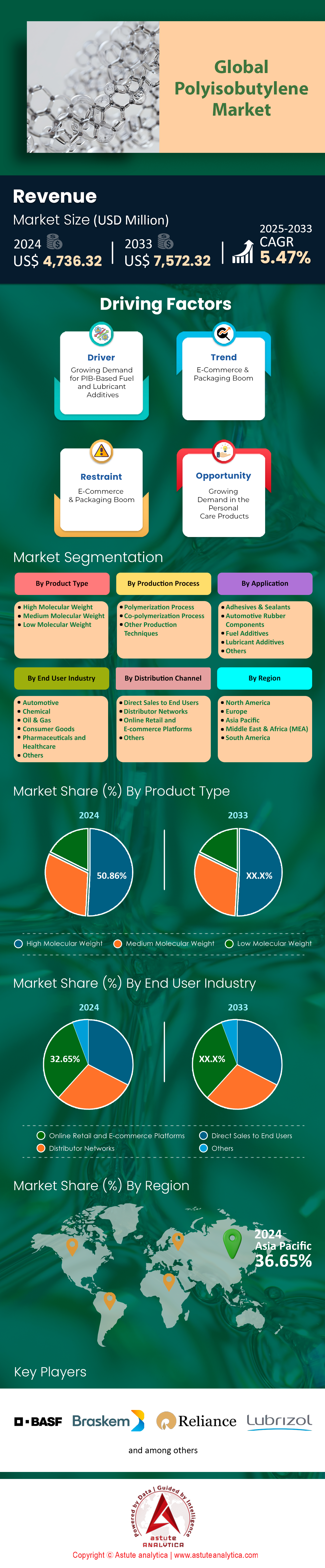

Polyisobutylene market was valued at US$ 4,736.32 million in 2024 and is projected to hit the market valuation of US$ 7,572.32 million by 2033 at a CAGR of 5.47% during the forecast period 2025–2033.

The global polyisobutylene market is positioned for robust and accelerated growth, underpinned by strong fundamentals and strategic industry expansions. With a market size estimated at 1.23 million tons in 2024 against a capacity of 1.48 million tons, the sector is well-balanced to meet current demand. Projections indicate a steady climb to 1.31 million tons in 2025 and a significant leap to 1.76 million tons by 2030. This trajectory represents an acceleration from the 0.9% average annual growth of the past decade to a forecasted 2.6% average rate, signaling renewed dynamism and expanding opportunities within the polyisobutylene market.

This growth is overwhelmingly driven by the automotive and industrial sectors. Lubricant additives alone constitute nearly half of all PIB consumption, and when combined with fuel additives and adhesives & sealants, these applications command three-fourths of the global p market. Geographically, demand is concentrated in established industrial hubs, with North America, Western Europe, and Asia Pacific collectively accounting for nearly 95% of global consumption. The health of the automotive industry, particularly in China and India where production figures continue to break records, serves as a direct and powerful engine for future PIB demand.

In response to this bright outlook, key producers in the polyisobutylene market are making significant investments. Nearly 0.1 million tons of new supply is expected in the near term from ventures by Saudi Aramco, TotalEnergies, and Daelim. This is complemented by Daelim’s own expansion to a total capacity of 0.33 million tons and BASF’s targeted increase of its medium-molecular-weight PIB capacity. These proactive capacity enhancements demonstrate strong industry confidence and ensure the market is prepared to support the needs of its diverse and growing customer base worldwide.

To Get more Insights, Request A Free Sample

Unpacking Global Supply: Strategic Capacity Expansions Redefining the Polyisobutylene Market

A granular analysis of the global supply chain reveals a period of strategic and substantial capacity expansion, critical for stakeholders evaluating the future competitive landscape of the market. Major producers are executing multi-faceted growth strategies to meet anticipated demand. Daelim Industrial is a prime example, embarking on a greenfield project to construct a new 80,000 metric ton per year plant in Saudi Arabia, set for a 2024 launch. This is complemented by a brownfield expansion at its Yeosu, South Korea facility, which will add another 50,000 tons, bringing Daelim's total polybutene capacity goal to an impressive 330,000 tons per year.

Similarly, BASF is surgically enhancing its capabilities in the polyisobutylene market, with an expansion at its Ludwigshafen site adding a specific 10,000 metric tons per year to its medium-molecular-weight PIB capacity by mid-2025, which will elevate the plant's total capacity for medium and high-MW PIB to 16,000 metric tons annually. Beyond individual efforts, collaborative ventures are set to make a significant impact, with a joint venture between Saudi Aramco, TotalEnergies, and Daelim poised to inject nearly 100,000 tons of new supply. This large-scale industrial activity contrasts with the operational scale of traders like Shanghai Qixi International Trade Co., Ltd., which handles a capacity of 1,000 tons per month, illustrating the tiered structure of the global supply network.

Decoding End-Use Demand: Pinpointing Key Growth Verticals for Polyisobutylene Consumption

For stakeholders, understanding application-specific consumption is paramount to capitalizing on the most lucrative segments of the polyisobutylene market. The automotive sector remains a cornerstone of demand, consuming over 14 million tons of plastics annually in passenger vehicles and driving tire shipments in key markets like the U.S. to volumes of 342.1 million units. However, the construction sector presents a powerful growth story; consumption of sealants is forecast to exceed 2.4 million metric tons in 2025 and continue its climb to a projected 4.1 million metric tons by 2030, making it a vital end-market for PIB.

A crucial insight for strategic planning in the polyisobutylene market is the highly consolidated nature of the high-value additives segment, where key suppliers like Chevron Oronite, Lubrizol, and Infinium consume over 90% of the volume of specialized grades like Daelim's highly reactive polybutene (HRPB). Looking forward, stakeholders must also monitor the evolving materials landscape. The projected rise in the automotive use of recycled plastics to 2,567 kilotons and bioplastics to 513 kilotons by 2035 will introduce new competitive and complementary dynamics that will shape long-term demand for virgin polymers like polyisobutylene.

Segmental Analysis

By Product Type: High Molecular Weight Polyisobutylene Commanding Market Dominance Through Superior Properties

The high molecular weight (HMW) segment’s control of over 50.86% of the polyisobutylene market is a direct consequence of its unparalleled physical characteristics, which make it indispensable for high-stakes applications. Unlike its liquid, lower-weight counterparts, HMW PIB is a solid, transparent, rubber-like elastomer defined by an ultra-high viscosity and molecular weights reaching into the millions. This structure imparts exceptional elasticity, allowing the material to stretch multiple times its length and recover, a critical feature for advanced rubber goods. However, its most valued attribute is its superior gas impermeability, which establishes it as the premier barrier material in numerous industries. The continuous global demand for high-performance lubricants and industrial sealants, where durability is non-negotiable, serves as the primary growth driver for the HMW segment, cementing its market leadership.

This dominance in the polyisobutylene market is further reinforced by HMW PIB’s resilience in harsh operational environments. The polymer exhibits outstanding chemical resistance against acids, bases, and various organic solvents, ensuring reliability and longevity. Its impressive thermal stability allows it to maintain structural integrity across a wide temperature range, a vital trait for applications exposed to fluctuating conditions. The long polymer chains inherent to HMW grades provide excellent structural integrity and durability. Furthermore, its compatibility with other polymers like polypropylene and synthetic resins makes it a versatile and valuable additive. As rapid industrialization and infrastructure projects accelerate in emerging economies, the demand for this robust grade of PIB is set to expand, solidifying its majority share in the global market.

By Production Method: Polymerization is Unrivaled Production Backbone of the Industry

The overwhelming dominance of polymerization, specifically cationic polymerization, as the primary production method for polyisobutylene market stems from its unique ability to exert precise control over the final polymer's architecture. The segment is currently accounting for over 47.34% market share. It stands as the only commercially viable method to synthesize this unique synthetic elastomer. This process allows manufacturers to meticulously tailor molecular weight, producing everything from viscous liquids to rubbery solids. This control is achieved through the careful selection of catalysts, with BF₃/ROH systems typically used for low MW PIB and AlCl₃/ROH systems for medium MW grades. Temperature is another critical variable; synthesizing HMW PIB requires cryogenic temperatures between -100 to -90 °C, whereas low MW PIB is produced in a much warmer range of -40 to 10 °C. This procedural precision enables the synthesis of highly reactive polyisobutylene (HRPIB), a critical precursor for high-performance additives.

The sophistication of cationic polymerization in the polyisobutylene market extends to controlling the polymer's end-groups, a feature that drives significant value in the additives sector. By employing Catalytic Chain Transfer Polymerization (CCTP), producers can achieve a yield of 70–90% of chain ends with a highly desirable exo-olefin group, essential for subsequent chemical reactions. At very low temperatures, from -80°C down to -25°C, the process can become a "living" polymerization, enabling the creation of advanced block copolymers with novel properties. The choice of solvent, such as polar dichloromethane or non-polar hexane, also profoundly influences the reaction and final structure. Reflecting broader industry trends, a key focus for producers is now on optimizing this energy-intensive process to enhance efficiency and sustainability, ensuring its continued dominance as the production standard.

Adhesives & Sealants: The Unshakeable Foundation Driving Nearly 30% Demand

The adhesives and sealants sector's consumption of nearly 30% of all polyisobutylene produced in the world is a testament to the polymer's irreplaceable combination of properties. A key driver for this demand is PIB’s permanent tackiness, which makes it a foundational component in pressure-sensitive adhesives (PSAs) used in everything from industrial tapes to labels. Unlike natural rubber, it boasts superior aging resistance and is highly resistant to chemical attack, ensuring long-term performance in the polyisobutylene market. This durability is complemented by its amorphous nature and an extremely low glass transition temperature of -62°C, which imparts exceptional flexibility and prevents adhesives from becoming brittle in cold environments. This combination of permanent stickiness and flexibility allows for excellent adhesion to a wide variety of substrates, including glass, metal, and plastic films, making it a highly versatile and reliable choice for formulators.

Beyond adhesives, PIB’s role in high-performance sealants is equally critical. Its excellent moisture and gas barrier properties are vital for applications like insulating glass windows, where it creates a hermetic seal to prevent fogging and improve energy efficiency. This is enhanced by the material’s "cold flow" characteristic, which allows it to seep into microscopic imperfections on a surface to create a perfect, self-healing seal in the polyisobutylene market. In hot melt adhesive formulations, specific PIB grades with a viscosity between 30,000 to 60,000 cps at 177°C are used to control flow and bonding characteristics. Its non-irritating nature makes it a choice material for medical adhesives, and its role as a modifier improves the tack and toughness of other polymers. Furthermore, using PIB can reduce the need for volatile organic compounds (VOCs), aligning with the market's growing demand for more environmentally friendly solvent-free formulations.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Automotive Sector: The Undisputed Engine Powering Global PIB Consumption

The automotive industry's position as the largest consumer with over 34.22% market share in the polyisobutylene market is anchored by the material’s multifaceted contributions to vehicle efficiency, durability, and performance. Its most significant and high-volume application is in the inner liners of tires. Here, PIB's unmatched air retention capabilities, far superior to other elastomers, prevent air leakage, which helps maintain correct tire pressure. This directly reduces rolling resistance, leading to improved vehicle fuel efficiency and enhanced safety. The ongoing shift to electric vehicles (EVs), which require robust and highly durable tires to manage higher torque and weight, is further accelerating the demand for PIB in this application. Beyond tires, the material's excellent flexibility and chemical resistance make it an ideal choice for manufacturing long-lasting automotive seals and gaskets that prevent fluid leaks and protect components from the elements.

The polymer's influence extends deep into the vehicle's powertrain through its use in advanced additives. In engine oils, PIB functions as a highly effective viscosity index improver, ensuring the lubricant maintains optimal thickness and protective qualities across the engine’s wide operating temperature range. As a key component in fuel additives, it helps keep engines clean by preventing deposit formation on critical parts, giving a strong momentum to the polyisobutylene market growth in this sector. Highly Reactive PIB is the essential precursor for producing ashless dispersants, which are primary components in modern engine oils responsible for managing soot and sludge, thereby extending engine life. This versatility is further demonstrated in its widespread use in two-stroke engine oils to improve lubrication and eliminate smoke. Its effectiveness is so pronounced that even in adjacent sectors like marine transport, PIB additives at just 1-25 mass % are proven to reduce deposit formation in large diesel engines, showcasing its critical role across the transportation landscape.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific's Reign: Unrivaled Growth Forges the Global Polyisobutylene Market Epicenter

The Asia Pacific region with over 36.65% market share stands as the undisputed engine of global growth, with staggering production and consumption figures that solidify its control of the polyisobutylene market. China’s economic indicators provide a powerful forecast for demand, with early 2025 figures showing 7% year-over-year growth in manufacturing production and a 5.5% rise in retail sales. This is buttressed by a colossal construction sector with output near 25 trillion Yuan and an automotive industry that consistently produces and sells over 31 million vehicles annually.

Meanwhile, India’s market is not just growing, it is accelerating at a breathtaking pace. In 2024, India’s automobile production surpassed 6 million units for the first time, reaching 6,014,548 units, with total annual vehicle production hitting 30,610,778 units. Passenger vehicle sales alone reached 4,274,793 units. The momentum is sustained, with the April-December 2024 period seeing 23,214,969 vehicles produced and 3,139,288 passenger vehicles sold. This explosive regional demand is being met by local supply expansions, such as Daelim's plan to increase its Yeosu plant's capacity to 250,000 tons, contributing to a massive future company-wide capacity of 330,000 tons.

US Market: Automotive Vigor Creates a Bedrock of Consistent PIB Demand

The United States presents a landscape of robust and stable demand in the North American region, firmly anchored by its automotive sector, creating a highly predictable environment for the polyisobutylene market. Tire shipments, a direct proxy for PIB consumption in inner liners, are projected to reach between 335.7 and 337.4 million units in 2024. This demand is multifaceted, with replacement passenger tires forecasted at 220.2 to 222 million units and Original Equipment (OE) shipments expected to hit 46.3 million units.

The light truck segment adds to this, with replacement demand projected at 35.2 to 36.7 million units and OE shipments at 6.0 to 6.7 million units, while medium truck/bus replacement tires will account for another 22 to 23.4 million units. This is supported by strong vehicle production in North America, expected to total 15.97 million units in 2024, and a forecast for U.S. light vehicle sales to reach 16.1 million units in 2025. With U.S. motor vehicle production hitting 10,611,555 units in 2023 and projected monthly sales of 1.27 million units for June 2025, the demand for lubricant additives—a 1.4 million ton market in North America in 2024—remains solid.

Europe's Duality: Production Strength Navigates Shifting Consumer and Industrial Tides

Europe’s polyisobutylene market is defined by a compelling duality: world-class production capabilities facing a complex and evolving demand landscape. On the supply side, the region is a cornerstone of global production. BASF's strategic expansion at its Ludwigshafen, Germany facility, which will add 10,000 metric tons per year to bring its medium and high-molecular-weight PIB capacity to 16,000 tons by mid-2025, underscores this strength. However, end-markets are mixed. The construction sector, a key PIB consumer in sealants, is projected to decline across 19 countries in 2024 before a modest recovery in 2025, with forecasted growth of just 0.4% in Western Europe versus 3.5% in Eastern Europe.

Conversely, the automotive sector provides a resilient demand base in the polyisobutylene market. The European new car market is expected to reach nearly 13 million registrations in 2024, with major players like the Volkswagen Group selling 3,407,242 vehicles and SUVs alone accounting for 6.92 million registrations. This activity directly fuels the European industrial lubricants market, estimated to be valued at USD 5,128.6 million in 2025, with Germany remaining the continent's largest consumer.

Top 10 Recent and Upcoming Developments In the Polyisobutylene Market Focusing On Expansions, Investments, and Strategic Projects

- BASF's European Capacity Boost (Scheduled for H1 2025): BASF is on track to complete a major expansion of its medium-molecular-weight polyisobutene (PIB) capacity at its Ludwigshafen, Germany, site. The project, officially announced in May 2024, will be finalized in the first half of 2025, adding 10,000 metric tons of annual production.

- Aramco-TotalEnergies-Daelim JV Progress (Announced Q1 2024): The strategic joint venture between Saudi Aramco, TotalEnergies, and Daelim for the "Amiral" complex, which includes a new polyisobutylene unit, saw major contracts awarded in March 2024. This signals the start of the primary construction phase for the project that will add nearly 100,000 tons of new supply.

- Daelim's Saudi Greenfield Project Commissioning (Q3 2024): Daelim Industrial's new 80,000-ton-per-year polyisobutylene plant in Saudi Arabia, a cornerstone of its global expansion, is scheduled to begin commercial operations in the third quarter of 2024, following its construction announcement.

- Daelim's South Korean Expansion Finalization (Q2 2024): The project to increase the annual capacity of Daelim's Yeosu plant in South Korea from 200,000 tons to 250,000 tons reached its final investment decision and implementation stages in the second quarter of 2024.

- TotalEnergies' Grandpuits Circularity Investment (February 2024): TotalEnergies announced a new investment phase in February 2024 to build a circular polymer production unit at its Grandpuits, France, zero-crude platform, influencing the market by increasing the focus on advanced recycling.

- Petronas Chemicals Group's Capex Allocation (February 2024): In its financial reporting in February 2024, Petronas Chemicals Group detailed its capital expenditure allocation for the year, prioritizing the growth of its specialty chemicals portfolio, which includes the value chain supporting polyisobutylene.

- Sibur's Modernization Investment Disclosure (April 2024): Sibur confirmed its ongoing investment program for modernizing its production facilities, including those for elastomers and polymers, in its sustainability and operational reports released in April 2024.

- Braskem's Strategic Investment Announcement (May 2024): During its Q1 2024 results call in May 2024, Braskem outlined its investment strategy to enhance polyolefins capacity, which is crucial for the feedstock streams required for polyisobutylene production.

- INEOS Olefins & Polymers Investment Update (June 2024): INEOS provided updates in June 2024 on its ongoing, multi-year investment plan to upgrade its European crackers, which are fundamental for supplying the raw materials needed for the polyisobutylene market.

- Reliance's Petrochemical Expansion Funding (Q4 2024): Reliance Industries is expected to finalize the next phase of funding and planning for its massive Jamnagar petrochemical expansion in the fourth quarter of 2024, with project timelines extending through 2025 and beyond.

Key Players in Polyisobutylene Market

- BASF SE

- Braskem

- Chevron Oronite Company LLC

- Dowpol Corp.

- Eneos Materials Corp.

- INEOS

- Kothari Petrochemicals

- Zhejiang Shunda New Material Co., Ltd

- Reliance Industries

- Shandong Hongrui New Material Technology Co., Ltd.

- The Lubrizol Corporation

- TPC Group

- Other Prominent Players

Market Segmentation Overview

By Product Type

- High Molecular Weight

- Medium Molecular Weight

- Low Molecular Weight

By Production Process

- Polymerization Process

- Co-polymerization Process

- Other Production Techniques

By Application

- Adhesives & Sealants

- Automotive Rubber Components

- Fuel Additives

- Lubricant Additives

- Others

By End User Industry

- Automotive

- Chemical

- Oil & Gas

- Consumer Goods

- Pharmaceuticals and Healthcare

- Others

By Distribution Channel

- Direct Sales to End Users

- Distributor Networks

- Online Retail and E-commerce Platforms

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Choose License Type

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |