Underwater Wireless Communication Market: By Type (Acoustic Communications, Optical Communications, RF Communications, Others); Technology (Sensor Technology and Vehicular Technology); Application (Environmental Monitoring, Pollution Monitoring, Seismic Monitoring, Ocean Current Monitoring, Climate Recording, Marine Archaeology, Search and Rescue Mission, Others); Industry (Oil and Gas, Military & Defense, Marine, Scientific Research & Development, Civil, Commercial, Others); Region—Market Forecast and Analysis for 2026–2035

- Last Updated: 11-Dec-2025 | | Report ID: AA0723536

Market Snapshot

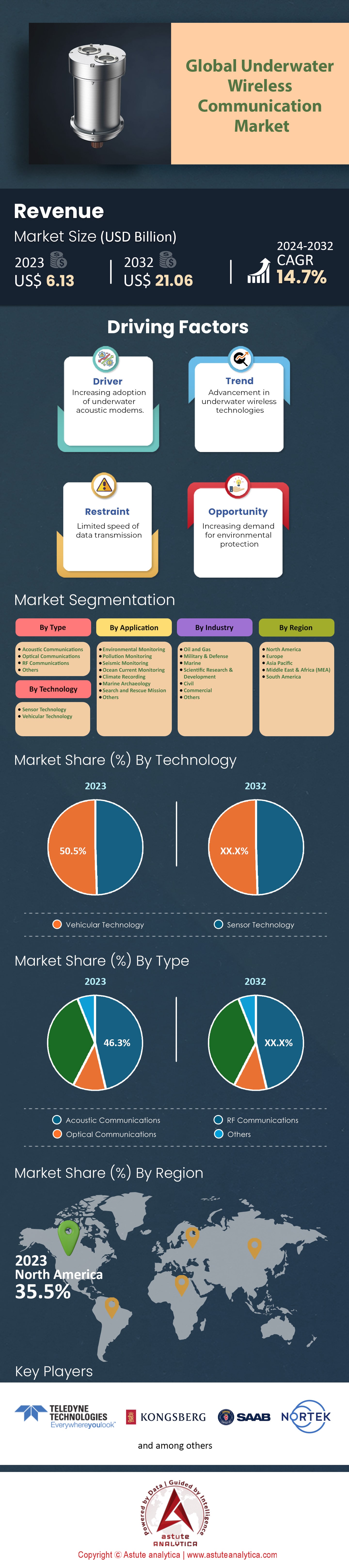

Underwater wireless communication market was valued at US$ 7.36 billion in 2025 and is projected to surpass market size of US$ 25.29 billion by 2035 at a CAGR of 14.7% during the forecast period 2026–2035.

Key Findings

- By type, the market is segmented into acoustic communication and radio frequency (RF) communication. Among these, the acoustic communication is projected to grow fastest CAGR of 15.6% and hold the largest market share of 46.3%.

- By technology, vehicular technology is projected to continue dominating the global market, holding over 50.5% of the revenue share.

- By application, environmental monitoring is anticipated to account for the highest market share of 25.9%

- By industry, the scientific research and development segment is expected to hold a significant market share of 37.2%.

- North America controls the largest 35.50% market share.

As of 2025, the demand for underwater wireless communication market is accelerating rapidly in 2025, primarily driven by the strategic shift toward autonomous naval interoperability. Defense agencies are no longer merely testing concepts but are actively deploying massive fleets, evidenced by the REPMUS 2025 exercise which coordinated over 2,000 personnel and 260 unmanned systems across 22 nations. Consequently, procurement cycles are lengthening to ensure operational stability; for instance, the UK MoD solidified a 3-year support contract with Teledyne Marine extending through 2028. This surge in defense spending validates the immediate transition from wired to wireless architectures to maintain superiority in contested environments.

Parallel to defense, the commercial sector is fueling growth of the underwater wireless communication market through the Internet of Underwater Things (IoUT), which is projected to expand at a 14.2% CAGR between 2025 and 2033. Offshore energy operators now demand infrastructure that functions autonomously for months without human intervention, necessitating robust data loggers like the 1 Terabyte capacity found in Sonardyne’s latest 2025 systems. Furthermore, the push for deep-water resource extraction requires hardware rated for extreme environments, with new ADCPs certified for depths of 4,100 meters. These specifications indicate a market rapidly moving toward permanent, wireless subsea residency rather than temporary, cabled expeditions.

The demand is being unlocked by breakthroughs in data throughput and range that were previously deemed impossible. Operators across the global underwater wireless communication market require high-speed video offloading, a need met by Kyocera’s November 2025 demonstration of 5.2 Gbps optical links. Simultaneously, long-range surveillance needs are being addressed by acoustic advancements achieving transmission distances of 30 kilometers while maintaining 4,000 bps. Even in deep waters, optical links have proven stable at 1,650 meters, proving to stakeholders that wireless technologies can now reliably handle the complex, high-bandwidth data requirements of modern oceanography.

To Get more Insights, Request A Free Sample

Trend Analysis: High Speed Optical Links and IoUT Integration Define Future Market Trajectories

Technological convergence is currently steering the Underwater wireless communication market toward unprecedented data rates and network density. In November 2025, Kyocera reset industry expectations by demonstrating optical link speeds of 5.2 Gbps, a figure approximately 2.5 times higher than legacy systems. Such throughput is essential for real-time video, pushing the industry beyond simple telemetry. Future-proofing is also evident in 6G research, which is now targeting the 0.1 to 10 THz spectrum to reduce latency to under 0.1 milliseconds. Furthermore, the IEEE 802.15.3d standard is opening the 252–322 GHz band, supporting channel bandwidths of 69 GHz. These advancements indicate a clear trend where data capacity is becoming the primary differentiator for commercial viability.

Network expansion is simultaneously driving demand for smarter, longer-lasting nodes. The Internet of Underwater Things (IoUT) sector is forecasted to surge with a 14.2% CAGR from 2025 to 2033, necessitating energy-efficient designs. Modern blue-laser systems recently achieved 135 Mbps over 10 meters with a robust Bit Error Rate of 5.9 × 10⁻³, proving reliable connectivity for sensor meshes. Power conservation is equally critical; MIT’s retrodirective backscatter innovation extended communication ranges by 15 times without increasing battery load. Stakeholders in the Underwater wireless communication market are rapidly adopting these technologies to create permanent, autonomous subsea digital twins.

Competitive Analysis: Leading Manufacturers Prioritize Miniaturization and Long Range Reliability To Secure Market Share

Key players within the Underwater wireless communication market are competing aggressively on hardware size and acoustic efficiency. Teledyne Marine has dominated the micro-sector in 2025 with its OEM Ultra Compact Modem, weighing just 55 grams and measuring 60 x 50 mm. This miniaturization allows integration into micro-AUVs without sacrificing depth ratings, which remain at 6,000 meters. Additionally, Teledyne's BlueStreamX2 update doubled legacy throughput to 4,800 bps using a 10 kHz bandwidth. Competitor EvoLogics is countering with raw speed, offering the S2CM-HS mini-modem that delivers 62.5 kbps for rapid data bursts. These innovations highlight a competitive landscape focused on maximizing performance-per-gram for autonomous fleets.

Conversely, long-duration reliability remains the battleground for infrastructure monitoring. Sonardyne solidified its position in late 2025 by successfully concluding an 18-month sensor deployment in the Gulf of Mexico. Their Origin 65 ADCP features 1 Terabyte of onboard storage, vastly outperforming standard competitors. Subnero is challenging the distance sector, with October 2024 launches exceeding 10 km in range. Meanwhile, Teledyne secured a 3-year contract with the UK MoD, locking in revenue through 2028. Defense and energy clients in the Underwater wireless communication market are favoring these manufacturers who can prove multi-year endurance and interoperability in deep-sea environments.

North Atlantic Defense Pacts And Asian Innovation Drive Global Market Expansion

The Underwater wireless communication market is expanding rapidly across the North Atlantic and Asia, fueled by distinct regional priorities. Portugal is now a critical hub for naval interoperability, recently hosting the massive REPMUS 2025 exercise. During this event, 22 nations coordinated over 260 unmanned systems to test coalition readiness. Building on this momentum, the United Kingdom solidified its defense posture through strategic long-term agreements. The UK MoD signed a 3-year support contract with Teledyne Marine that extends operations through 2028. Meanwhile, China is redefining long-distance capabilities in the Pacific. Researchers there achieved a record-breaking 30-kilometer transmission link in 2024. These combined efforts create a competitive global landscape where national security directly dictates technological procurement.

Application trends are simultaneously shifting from passive monitoring to active autonomous defense. Security needs are driving the Underwater wireless communication market forward by funding projects like "U-SHIELD," which operationalized new tech in August 2025. Commercial sectors are also leveraging European funding through the "VesselAI" project to build maritime digital twins. Such initiatives support the Internet of Underwater Things (IoUT), which is projected to grow at a CAGR of 14.2%. At last, offshore energy requires robust deep-sea tools. Operators are deploying ADCPs rated for 4,100 meters to profile currents. These diverse use cases prove that industrial wireless adoption is becoming the global standard for asset protection.

European Defense Alliances and Asian R&D Breakthroughs Dominate Market Expansion

Europe is currently establishing the operational blueprint for the Underwater wireless communication market, driven by urgent NATO interoperability mandates. Portugal served as the epicenter in 2025, hosting the massive REPMUS exercises where 22 nations successfully coordinated 260 unmanned assets. Such collaboration is bolstering investor confidence across the continent. The United Kingdom is equally aggressive, securing a 3-year defense contract with Teledyne Marine that runs through 2028. Innovation is shifting eastward as well. Chinese entities set a new global benchmark in 2024 by achieving a massive 30-kilometer acoustic transmission range. These distinct regional efforts are creating a competitive landscape defined by NATO's standardization versus Asia's raw distance capabilities.

Defense applications remain the primary revenue generator within the Underwater wireless communication market, specifically for infrastructure protection. Security initiatives like the U-SHIELD project, operationalized in August 2025, are actively deploying wireless tech to protect subsea perimeters. Beyond defense, commercial sectors are scaling rapidly. The Internet of Underwater Things (IoUT) is projected to grow at a 14.2% CAGR, supported by EU-funded initiatives like VesselAI which utilize wireless data to create maritime digital twins. Deep-sea energy operators are also adopting these tools, deploying ADCPs rated for 4,100 meters to monitor billion-dollar assets. Market leaders are witnessing a clear migration from experimental pilots to essential industrial and military utility.

Segmental Analysis

Acoustic Innovations Driving Reliability And Standardization In Complex Deep Sea Operations

Acoustic communication systems act as the primary backbone for subsea connectivity. As a result, the segment is projected to grow fastest CAGR of 15.6% and hold the largest market share of 46.3% of the underwater wireless communication market. Physics dictates that sound waves propagate far more efficiently through water than electromagnetic signals, making acoustic technology indispensable for long-range transmission in defense and energy sectors. A major leap toward market maturity occurred when NATO fleets formally adopted the JANUS standard, ensuring that diverse acoustic devices from different manufacturers can finally interoperate during joint exercises.

Additionally, commercial innovation is accelerating, with companies like Teledyne Marine releasing compact acoustic modems specifically designed to enable swarm behavior in micro-AUVs. These advancements suggest the Underwater wireless communication market is moving away from bespoke, isolated systems toward a standardized, networked future that supports increasingly complex operations.

- Researchers successfully demonstrated multi-kilometer acoustic data transmission in the Arctic to overcome ice-cover interference.

- Oil majors deployed acoustic trigger systems for remote control of subsea valves, removing the need for hydraulic umbilicals.

- EvoLogics demonstrated a new acoustic networking protocol that facilitates simultaneous communication between multiple underwater drones.

Strategic investments in national security further solidify the dominance of acoustic technology in the underwater wireless communication market. The US Navy recently awarded multi-million dollar contracts for acoustic-based mine countermeasure systems, prioritizing diver safety and reliable data links in high-noise littoral waters. In the commercial energy sector, Sonardyne introduced advanced acoustic telemetry nodes capable of retrieving data from deep-water wells without surface vessels, a capability that significantly reduces operational expenditures for oil and gas operators. Subsea 7 has also implemented these positioning systems to monitor pipeline bundle installations. Such widespread adoption across critical industries ensures that acoustic solutions remain the primary revenue generator within the Underwater wireless communication market, driving sustained growth through both military defense upgrades and offshore energy efficiency programs.

Autonomous Underwater Vehicles Fueling Massive Demand For Robust Wireless Data Links

Vehicular technology is projected to continue dominating the underwater wireless communication market, holding over 50.5% of the revenue share. This commanding position is largely driven by the industry-wide transition from tethered Remotely Operated Vehicles (ROVs) to fully Autonomous Underwater Vehicles (AUVs), which require sophisticated wireless command capabilities. Kongsberg Maritime, for instance, secured record orders for their HUGIN AUVs equipped with proprietary wireless data links, signaling a decisive shift toward untethered pipeline inspection. Similarly, Saab Seaeye successfully integrated wireless command controls into their e-robotic systems, allowing operators to reduce dependence on costly support vessels. As these vehicles become the standard for subsea intervention, the Underwater wireless communication market is witnessing a surge in demand for high-bandwidth modems that can support autonomous decision-making and real-time path correction.

- L3Harris developed specialized wireless nodes for unmanned undersea gliders to support long-endurance surveillance missions.

- Fugro transitioned several operations to remote onshore centers, controlling wireless ROVs via satellite-linked subsea modems.

- Kawasaki Heavy Industries demonstrated an AUV capable of wireless docking and charging at subsea stations.

Commercial entities are aggressively scaling their fleets to offer data-centric services, further boosting the vehicular segment. Ocean Infinity expanded its Armada fleet, a move that necessitates advanced wireless data transfer systems to maintain over-the-horizon control of uncrewed vessels. Innovation is also visible in startups like Terradepth, which launched autonomous submarines offering data-as-a-service; these units rely entirely on high-speed wireless uploads upon surfacing to deliver client data. Furthermore, Nauticus Robotics successfully tested tether-less manipulation on subsea structures using wireless real-time video feedback. These developments confirm that the vehicular segment captures the majority of revenue because the Underwater wireless communication market provides the essential "nervous system" that allows these next-generation robots to function autonomously and efficiently.

Real Time Ocean Observation Networks Boosting Adoption Of Advanced Sensor Arrays

Environmental monitoring is anticipated to account for the highest market share of 25.9% among applications, driven by the urgent global need to track climate change indicators and mitigate natural disasters. Governments are heavily investing in permanent infrastructure, such as the DART Tsunami Warning System, which NOAA expanded with improved acoustic data uplinks to ensure faster threat detection. Simultaneously, the Smart Ocean Buoy network has integrated underwater modems to transmit real-time salinity and temperature data to surface gateways, replacing sporadic logging with continuous intelligence. These large-scale deployments are critical for the Underwater wireless communication market, as they represent stable, long-term contracts rather than one-off project sales. The shift from passive data collection to active, real-time monitoring is compelling agencies to upgrade their entire sensor architectures with wireless capabilities.

- China launched a commercial underwater data center featuring environmental sensor arrays linked via wireless optical-acoustic hybrids.

- Japan deployed wireless monitoring grids to assess the environmental impact of deep-sea mineral extraction trials.

- Offshore wind developers mandated wireless noise monitoring systems to ensure construction remains within marine mammal safety limits.

Conservation efforts are also leveraging advanced connectivity to protect fragile ecosystems. The Great Barrier Reef Foundation deployed wireless sensor arrays to send immediate alerts regarding coral bleaching events, allowing for rapid response measures. Similarly, European marine observatories have installed wireless seafloor nodes to track seismic activity and underwater volcanic eruptions, safeguarding coastal communities. Plymouth Marine Laboratory is utilizing wirelessly connected gliders to study plankton blooms without disturbing the water column. As environmental regulations tighten, industrial stakeholders are forced to adopt these monitoring solutions, thereby reinforcing the segment's leadership position in the Underwater wireless communication market. The ability to remotely monitor deep-sea environments without human presence is proving to be the most valuable application of wireless subsea technology today.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Government Funding and Deep Sea Exploration Projects Accelerating Wireless Communication Research

The scientific research and development segment is expected to hold a significant market share of 37.2%, fueled by massive capital injections aiming to conquer the "final frontier" of the deep ocean. Institutions like Scripps Institution of Oceanography have received federal grants to develop "underwater Wi-Fi" for real-time video streaming, a project that pushes the boundaries of current bandwidth physics. Defense agencies are also major contributors; DARPA funded the "Trace" program to advance wireless undersea surveillance capabilities using novel signal processing techniques. These high-budget initiatives sustain the Underwater wireless communication market by procuring experimental, high-value systems that are not yet commercially viable for the mass market. The European Union Horizon program has further allocated funds for developing 6G concepts specifically for underwater environments, indicating a long-term commitment to foundational research.

- MIT researchers developed battery-free underwater communication prototypes that harvest energy from sound waves.

- South Korea invested in "Digital Ocean" infrastructure, funding R&D for a nationwide underwater wireless IoT network.

- National Oceanography Centre UK trialed swarm autonomy algorithms dependent on inter-vehicle wireless sharing.

Space exploration agencies are utilizing Earth’s oceans as testing grounds, adding another layer of demand to this segment. NASA conducted underwater wireless communication tests to simulate future missions exploring the subsurface oceans of Europa, requiring extremely robust and autonomous data links. Meanwhile, China State Shipbuilding Corporation is advancing research into quantum underwater communication to secure data against interception. On the academic front, Woods Hole Oceanographic Institution tested optical-acoustic hybrid modems to solve bandwidth limitations during research expeditions. Such diverse and well-funded projects ensure that the R&D segment remains a dominant force, driving the technological breakthroughs that eventually trickle down to commercial sectors of the underwater wireless communication market.

To Understand More About this Research: Request A Free Sample

Regional Analysis

The Global Underwater Wireless Communication market is witnessing a shift in the dynamics of regional dominance. North America, with its advanced technological infrastructure and significant investments in defense and exploration sectors, currently holds sway, accounting for over 35.5% of the global market revenue in 2025. The region's visionary approach towards the use of underwater robotic technologies has played a key role in this. Unmanned underwater vehicles, also known as underwater robots, offer considerable advantages such as negating the need for human divers, thus making offshore operations more feasible and less risky.

The high demand for these technologies in North America is primarily driven by the need for enhanced security and surveillance systems, which makes underwater acoustic communication a vital component. This trend is expected to fuel the growth of the underwater wireless communication market in North America at a fast pace during the forecast period.

However, the dynamics of the global UWC market are changing, with the Asia Pacific region expected to emerge as a key player. In 2025, the Asia Pacific region projected the highest Compound Annual Growth Rate (CAGR) of 16.5%. The increase in the deployment of autonomous underwater vehicles in the defense sector is the primary reason behind this surge. The region's escalating tension and increasing defense budgets are directly contributing to this rise.

Furthermore, in the Asia Pacific region, the growing economies such as China and India are showing an increased focus on maritime security and exploration, thus driving the demand for UWC. As these economies continue to invest in their defense sectors, the demand for advanced technologies such as underwater wireless communication systems is expected to rise, potentially making the Asia Pacific region a major market for UWC in the near future.

Europe, although trailing behind North America and Asia Pacific in terms of market growth, is showing promise for the underwater wireless communication market. Advanced countries in Europe are progressively acknowledging the benefits of autonomous underwater vehicles, which in turn, is creating a rising demand for UWC. Therefore, Europe is predicted to follow the growth trajectory of the Asia Pacific and North American markets in the future.

Recent Developments in Underwater Wireless Communication Market

L3Harris Iver4 900 AUV Delivery: L3Harris delivered the first production Iver4 900 AUVs with Lithium-ion Passive Propagation Resistant (Li-ion PPR) batteries to the U.S. Navy around November 12, 2024. These units double endurance for submarine-launched missions and mark the first Navy-approved Li-ion AUVs for submarine use.

Subnero L12L Series Launch: Subnero launched the L12L series acoustic smart modems on October 5, 2024, achieving over 10 km range in tropical waters and up to 8 kbps data rates for coastal networks and AUV tracking.

Sonardyne Gulf of Mexico Monitoring: Sonardyne partnered with SeaTrac in October 2024 (announced around September-October) to deploy Origin 65 ADCPs in the Gulf of Mexico, using a solar-powered USV for remote, low-carbon data harvesting from the Loop Current System.

Hydromea US Market Expansion: Hydromea appointed Crestone as its official U.S. partner on October 3, 2024 (formalized November), targeting LUMA/EXRAY optical tech for Gulf of Mexico oil/gas "drive-by" data offloading.

Seaber Micro-AUVs for SEAMAP: Seaber, with CNRS-LEMAR, mobilized micro-AUV swarms (YUCO models with eDNA samplers and sonars) for the SEAMAP project under France 2030 around July 15, 2024, enabling low-cost seabed biodiversity mapping.

Seaber and Marine Sonic Partnership: Seaber integrated Marine Sonic Technology's dual-frequency side-scan sonars into micro-AUVs on May 30, 2024, enabling high-resolution imaging for compact wireless surveys.

Teledyne Slocum Sentinel Glider: Teledyne Marine debuted the Slocum Sentinel Glider at Oceanology International on March 4-14, 2024, featuring an acoustic trigger for ropeless fishing to prevent whale entanglements.

u-blox Antarctic Penguin Tracking: u-blox partnered with Cellular Tracking Technologies (CTT) on March 12, 2024, using CloudLocate for low-power IoUT tracking of Adélie penguins via surface bursts in Antarctica.

Subnero S40H High-Speed Modems: Subnero unveiled the S40H series on March 1, 2024 (announced March 11 at Oceanology), offering up to 33 kbps in 25-50 kHz band for shallow-water visual telemetry.

EvoLogics S2C "Tiny" Series Update: EvoLogics featured updated S2C T-Series ("Tiny") modems in its 2024 portfolio (ongoing from prior models), with ~20% size reduction, JANUS compatibility, and micro-ROV optimization.

Top Players in Global Underwater Wireless Communication Market

- Benthowave Instrument Inc

- Bruel and Kjar

- DSPComm

- EvoLogics GmbH

- Fugro

- Kongsberg Gruppen

- Nortek AS

- Ocean Technology Systems

- RJE International, Inc

- SAAB AB

- SONARDYNE

- Subnero Pte Ltd

- Teledyne Technologies Incorporated

- Ultra Electronics Maritime Systems

- Wilcoxon Sensing Technologies

- Other Prominent Players

Market Segmentation Overview:

By Type:

- Acoustic Communications

- Optical Communications

- RF Communications

- Others

By Technology

- Sensor Technology

- Vehicular Technology

By Application

- Environmental Monitoring

- Pollution Monitoring

- Seismic Monitoring

- Ocean Current Monitoring

- Climate Recording

- Marine Archaeology

- Search and Rescue Mission

- Others

By Industry

- Oil and Gas

- Military & Defense

- Marine

- Scientific Research & Development

- Civil

- Commercial

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2025 | US$ 7.36 Billion |

| Expected Revenue in 2035 | US$ 25.29 Billion |

| Historic Data | 2020-2024 |

| Base Year | 2025 |

| Forecast Period | 2025-2035 |

| Unit | Value (USD Bn) |

| CAGR | 14.7% |

| Segments covered | By Type, By Technology, By Application, By Industry, By Region |

| Key Companies | Benthowave Instrument Inc, Bruel and Kjar, DSPComm, EvoLogics GmbH, Fugro, Kongsberg Gruppen, Nortek AS, Ocean Technology Systems, RJE International, Inc, SAAB AB, SONARDYNE, Subnero Pte Ltd, Teledyne Technologies Incorporated, Ultra Electronics Maritime Systems, Wilcoxon Sensing Technologies, Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |