Industrial Robotics Market Revenue to Attain USD 235.38 Billion By 2033

Industrial Robotics Market Revenue and Trends 2025 to 2033

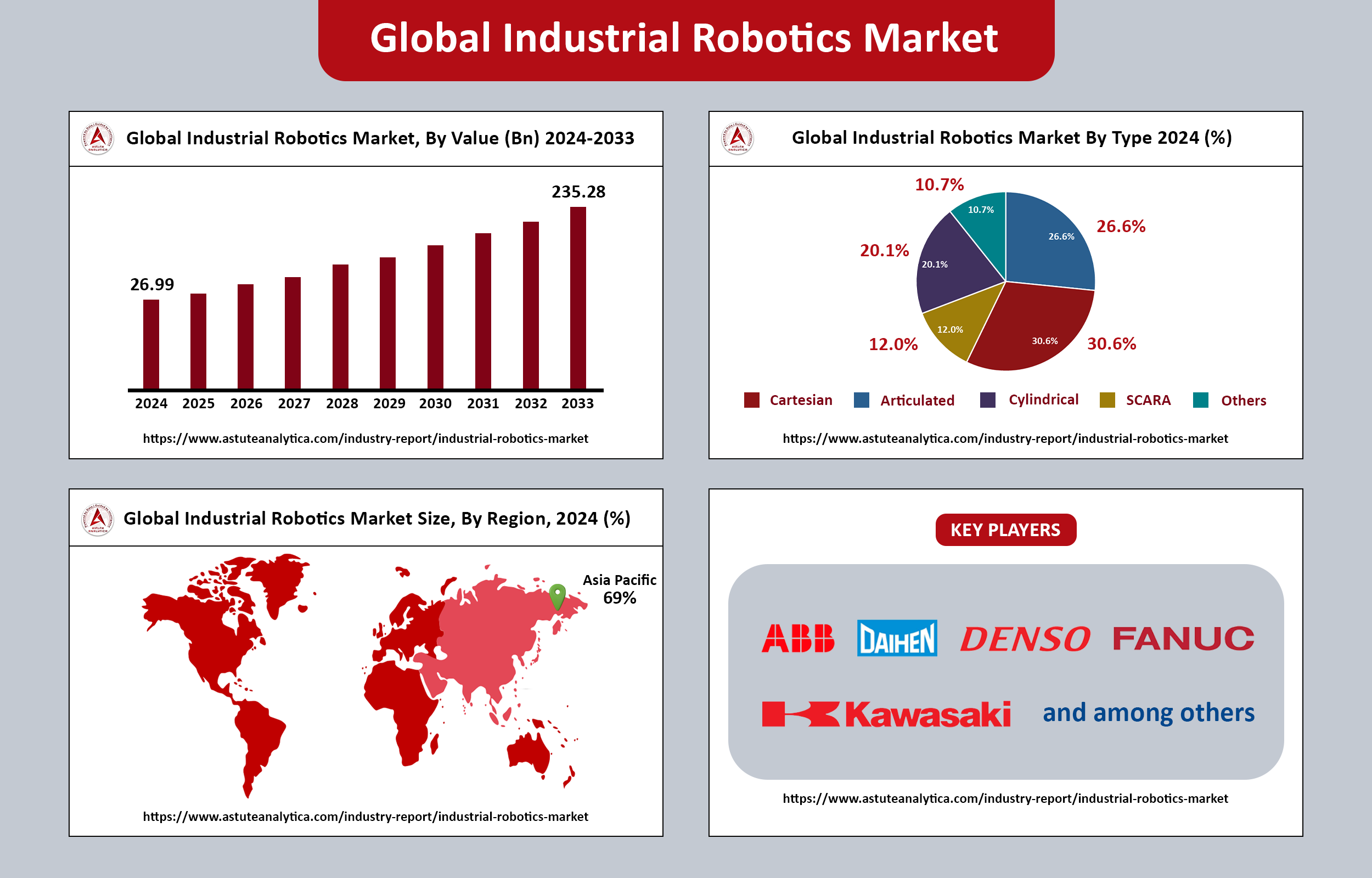

The global industrial robotics market revenue surpassed US$ 26.99 billion in 2024 and is predicted to attain around US$ 235.28 billion by 2033, growing at a CAGR of 27.2% during the forecast period from 2025 to 2033.

Industrial robotics refers to the deployment of robots within manufacturing environments to automate various tasks, including assembly, welding, and material handling. According to the latest World Robotics report, there are now 4,281,585 units operating in factories globally, marking a 10% increase. For the third consecutive year, annual installations have surpassed half a million units, reflecting a robust demand for robotic automation.

Moreover, articulated robotic platforms are transforming, evolving from being dedicated single-task machines to becoming versatile multi-purpose workhorses. Modern end-users now have heightened expectations for these robotic systems, seeking features such as fast tool-change couplers, integrated vision cabling, and native OPC UA connectors as standard offerings. This shift indicates a broader trend towards flexibility and adaptability in robotics, enabling manufacturers to optimize their production processes and respond more effectively to varying operational demands.

Industrial Robotics Market Key Takeaways

- The industrial robotics market is projected to achieve a valuation of US$ 235.28 billion by 2033, growing at a remarkable CAGR of 27.2% during the forecast period from 2025 to 2033.

- In terms of robot type, Cartesian robots hold the largest market share, commanding approximately 30.60% of the total. Their linear architecture is particularly well-suited for the rectangular work envelopes prevalent in modern production cells, making them a preferred choice for many manufacturers.

- When examining the market by function, material handling emerges as the dominant category, accounting for over 43% of the market share. This is largely due to the necessity for continuous movement of parts between different process steps in virtually every production environment, from heavy-duty steel mills to agile micro-fulfillment centers.

- The automotive industry remains the powerhouse of the industrial robotics market, representing over 25.40% of the total market share. The unique demands of vehicle assembly, which require a complex mix of welding, sealing, painting, and final inspection processes, necessitate high-speed operations with zero defects.

Regional Analysis

The Asia Pacific region dominates the industrial robotics market, accounting for over 69.0% of installations worldwide, representing nearly seven out of every ten new robots installed globally. This leading position is further solidified as regional governments intensify their support for capacity expansion through grants and incentives aimed at boosting automation.

China stands out as the largest market for industrial robots globally. In 2023, the country saw the installation of 276,288 industrial robots, which translates to a staggering 51% of all global installations. This figure marks the second-highest level recorded in history, following the peak of 290,144 units in 2022. The consistent investment in automation reflects China's commitment to enhancing its manufacturing capabilities and maintaining its competitive edge in the global market.

Following China, Japan retains its status as the second-largest market for industrial robots. In 2023, robot installations in Japan totaled 46,106 units, representing a 9% decline from the previous year. This decrease follows two consecutive years of strong growth, with installations peaking at 50,435 units in 2022, marking the second-best result in the country's history after the record of 55,240 units in 2018. The decline in installations may indicate market saturation or a temporary recalibration as manufacturers assess their automation needs.

Market Overview

The market for industrial robots has experienced a remarkable surge in growth, driven primarily by their capability to automate labor-intensive production processes, especially in fast-paced assembly lines. The increasing adoption of robotic technology within the manufacturing industry can be attributed to several key factors.

Favorable government policies promoting automation and technological advancement have played a significant role in encouraging manufacturers to integrate robots into their operations. These policies often include incentives for companies that invest in automation, grants for research and development, and support for workforce training programs.

Additionally, the proliferation of small and medium-sized enterprises (SMEs) globally is contributing to the growth of the industrial robotics market. SMEs are increasingly recognizing the benefits of automation, as it allows them to compete with larger firms on a more level playing field. With advancements in technology, robotic systems have become more accessible and affordable for smaller businesses, enabling them to streamline operations and improve productivity.

Access a free sample copy or review the report summary :

Market Growth Factors

Driver

Chronic Skilled Labor Shortages Driving Automation: The persistent skilled labor shortages faced by manufacturers worldwide are increasingly pushing companies toward automation-intensive solutions. This trend is significantly influencing the growth of the industrial robotics market as businesses seek to maintain productivity and efficiency in the face of workforce challenges.

Expansion in EV and Semiconductor Industries: The rapid growth of the electric vehicle (EV) and semiconductor sectors is creating a pressing demand for precise, high-volume robot-enabled production capacity. This surge is further propelling the industrial robotics market as manufacturers seek advanced robotic solutions to meet these emerging needs.

Restraint

Supply Chain Constraints: The industrial robotics market is currently facing significant challenges due to supply chain constraints affecting critical components such as servomotors and chips. These constraints are prolonging lead times considerably, which could hinder the market growth.

Challenges Faced by SMEs in Robotics Integration: Small and Medium Enterprises (SMEs) are encountering several barriers that complicate their efforts to integrate robotics into their operations. Issues such as integration complexity, programming expertise, and change-management barriers are significant obstacles that can impede the growth of the industrial robotics market.

Top Trends

Collaborative Robots and Advanced Vision: The integration of collaborative robots (cobots) equipped with advanced vision systems is revolutionizing the landscape of industrial robotics. These technologies facilitate flexible human-robot shared workspaces, allowing robots to work alongside human operators safely and efficiently.

Digital Twins and Edge AI: The advent of digital twins combined with edge AI technology is further propelling advancements in robotic systems. Digital twins, which are virtual replicas of physical systems, allow for autonomous robotic path optimization, enhancing efficiency and performance.

Recent Developments

- In May 2025, Epson Robots expanded its SCARA lineup with the introduction of the GX-C Series. This new series is powered by the RC800A controller, which features SafeSense technology. The lineup includes the models GX4C, GX8C, GX10C, and GX20C.

- In May 2025, Novarc Technologies Inc., a full-stack AI robotics company known for its automated welding solutions, announced the launch of NovAI™. This innovative AI-powered system enhances articulated robotic and mechanized welding by incorporating vision and real-time adaptation. The announcement was made at Automate 2025.

- In May 2025, Standard Bots unveiled a new robot and announced the expansion of its production facility in Glen Cove, N.Y. The American robotics company revealed that the new factory, spanning 16,000 square feet (approximately 1486.4 square meters), effectively doubles the size of its previous Long Island location.

Top Companies in the Industrial Robotics Market:

- ABB Limited

- DAIHEN Corporation

- Denso Corporation

- Epson America Incorporated

- Fanuc Corporation

- Kawasaki Heavy Industries Limited

- Kobe Steel, Limited

- Kuka AG

- Mitsubishi Electric Corporation

- Yaskawa Electric Corporation

- Other Prominent Players

Market Segmentation Overview

By Type

- Articulated

- Cartesian

- SCARA

- Cylindrical

- Others

By Industry

- Automotive

- Electrical & Electronics

- Chemical Rubber & Plastics

- Machinery

- Food & Beverages

- Others

By Function

- Soldering & Welding

- Materials Handling

- Assembling & Disassembling

- Painting & Dispensing

- Milling, Cutting, & Processing

- Others

By Geography

- North America

- Europe

- Asia Pacific

- South America

- Middle East & Africa (MEA)