Marktübersicht

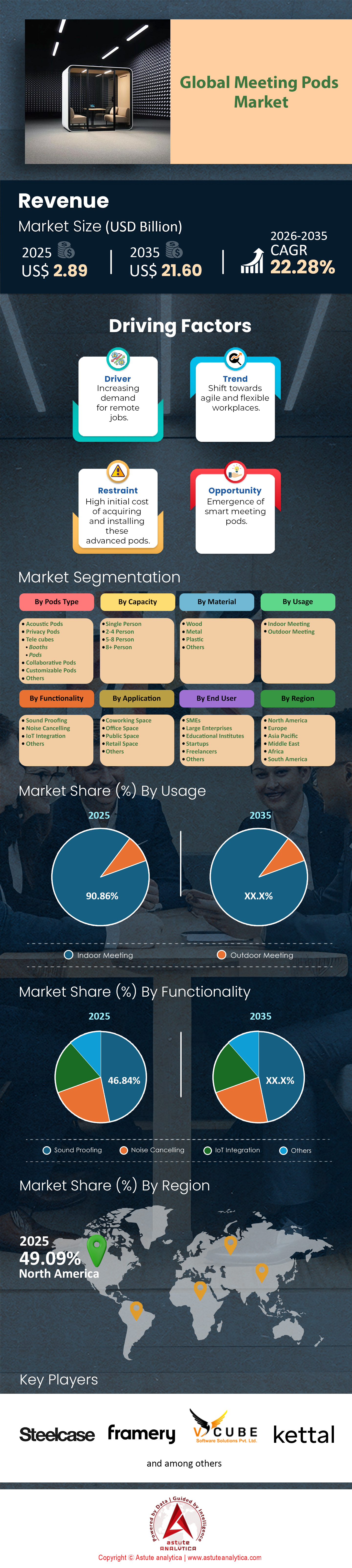

Der Markt für Meeting-Pods wurde im Jahr 2025 auf 2,89 Milliarden US-Dollar geschätzt und soll bis 2035 einen Marktwert von 21,60 Milliarden US-Dollar erreichen, was einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von 22,28 % im Prognosezeitraum 2026–2035 entspricht.

Wichtigste Erkenntnisse

- Basierend auf dem Kabinentyp haben Akustikkabinen den Markt für Besprechungskabinen maßgeblich verändert und einen beachtlichen Marktanteil von über 36,09 % erreicht.

- Gemessen an der Kapazität dominieren Meeting-Pods für 2-4 Personen den globalen Markt für Meeting-Pods mit einem Marktanteil von 42,53%.

- Nach Anwendungsbereich werden Meeting-Pods hauptsächlich in Büroräumen eingesetzt, und dieser Anwendungsbereich beherrscht über 41% Marktanteil.

- Gemessen am Material hat sich Holz zum führenden Material für den Bau von Meeting-Pods entwickelt und wird im Jahr 2025 fast 39,67 % aller gebauten und verkauften Einheiten ausmachen.

- Nordamerika hält mit 50 % den Löwenanteil am Weltmarkt.

Besprechungskabinen haben sich von einfachen Möbelstücken zu ausgeklügelten, modularen Akustikräumen entwickelt, die der Lärmbelastung in Großraumbüros entgegenwirken sollen. Technisch gesehen handelt es sich um in sich geschlossene, belüftete und schallgedämmte Einheiten, die von Einzeltelefonzellen bis hin zu großen Konferenzräumen reichen und ohne bauliche Veränderungen installiert werden können. Hauptgrund für den jüngsten Nachfrageanstieg ist die „Datenschutzkrise“, mit der die Arbeitnehmer nach der Pandemie konfrontiert sind.

Da laut Daten aus dem Jahr 2025 Lärm die Hauptursache für Unzufriedenheit am Arbeitsplatz ist – 70 % der Beschäftigten nennen dies –, suchen Unternehmen händeringend nach Lösungen. Die wirtschaftlichen Folgen sind gravierend: Der Gallup-Bericht „State of the Global Workplace 2025“ schätzt, dass Produktivitätsverluste durch unmotivierte und abgelenkte Mitarbeiter die Weltwirtschaft jährlich sage und schreibe 438 Milliarden US-Dollar kosten. Daher haben sich Besprechungskabinen von optionalen Zusatzleistungen zu einer unverzichtbaren Infrastruktur für konzentriertes und effizientes Arbeiten entwickelt.

Für weitere Einblicke fordern Sie ein kostenloses Muster an.

Welche wirtschaftlichen Triebkräfte und strategischen Faktoren treiben das Wachstum des Marktes für Meeting-Pods an?

Neben dem reinen Komfort bietet die Nutzung von Meeting-Pods überzeugende finanzielle Vorteile für Facility Manager und Investoren. Die Kosten für den Bau fester Besprechungsräume sind rasant gestiegen, wobei traditionelle Trockenbaukonstruktionen aufgrund von Lohn- und Materialpreissteigerungen oft über 29.000 US-Dollar pro Raum kosten. Modulare Lösungen hingegen bieten eine kapitaleffiziente Alternative: Hochwertige 4-Personen-Pods kosten in der Regel zwischen 13.500 und 22.500 US-Dollar. Diese Möglichkeit zur Kostenersparnis erlaubt es Unternehmen, flexible Ressourcen einzusetzen, die bei einem Umzug des Büros – im Gegensatz zu fixen Baukosten – einfach mitgenommen werden können.

Darüber hinaus zeigen aktuelle Erkenntnisse, dass sich die Investition schnell amortisiert. Die Marktanalyse für Meeting-Pods legt nahe, dass sich eine 10.000 US-Dollar teure Kabine bereits nach weniger als zwölf Monaten amortisiert, wenn sie zwei Mitarbeitern täglich nur 30 Minuten weniger Ablenkung erspart. Diese spürbare finanzielle Effizienz ist der Hauptgrund für das starke Marktwachstum bis 2025.

Welche Produktkonfigurationen dominieren die Auftragsbücher?

Der Markt für Meeting-Pods ist aktuell in zwei wachstumsstarke Segmente unterteilt: den „Focus Pod“ für individuelle Videokonferenzen und den „Collab Pod“ für kleine Teams. Der Trend zu hybriden Arbeitsmodellen hat Videokonferenzen allgegenwärtig gemacht und eine enorme Nachfrage nach Einzelplatzlösungen wie dem Framery One Compact geschaffen, der nur 1,03 Quadratmeter Stellfläche benötigt. Gleichzeitig treibt der Bedarf an ungestörter physischer Zusammenarbeit den Absatz von Einheiten für 4 bis 6 Personen an.

Diese größeren Kabinen sind für intensive Nutzung konzipiert. Hochleistungsmodelle bieten Luftdurchsatzraten von bis zu 100 Litern pro Sekunde (l/s), um auch bei stundenlangen Strategiebesprechungen eine optimale Luftqualität zu gewährleisten. Der Markt verzeichnet zudem eine wachsende Nachfrage nach barrierefreien Kabinen. Hersteller bringen ADA-konforme Modelle mit extrem niedrigen Einstiegshöhen von 1,25 cm und breiteren Türen auf den Markt, um die Inklusionsrichtlinien von 2025 zu erfüllen.

Wer sind die Schwergewichte und prominenten Marken, die die Marktlandschaft der Meeting-Pods prägen?

Die Wettbewerbslandschaft ist geprägt von europäischer Ingenieurskunst, wobei Framery seine unangefochtene Marktführerschaft behauptet. Das finnische Unternehmen erzielte 2024 einen Jahresumsatz von 162 Millionen Euro und übertraf die Marke von 110.000 weltweit ausgelieferten Kabinen. Seine Vormachtstellung wird jedoch von starken Konkurrenten wie Silen, einer estnischen Marke, die sich durch ihre robuste Akustiktechnik und eine nachweisliche Produktlebensdauer von über 20 Jahren einen Namen macht.

Hushoffice ist ein weiterer wichtiger Akteur im Markt für Meeting-Pods und positioniert sich mit seiner HushFree.S-Produktlinie aggressiv im mittleren Preissegment. In Nordamerika halten Marken wie Room und Zenbooth weiterhin bedeutende Marktanteile, insbesondere im Einsteiger- und Mittelklassebereich. Diese Hersteller differenzieren sich nicht nur über den Preis, sondern auch durch validierte ISO 23351-1 Klasse-A-Akustikzertifizierungen, die für Käufer zum Goldstandard geworden sind.

Welche neuen Umsatzpotenziale und wichtigsten Trends beeinflussen den Markt?

Der Markt für Meeting-Pods wandelt sich hin zu „Smart Pods“ mit IoT-Funktionen und generiert so neue Einnahmen durch Datenanalyse und Software-Abonnements. Moderne Pods sind keine passiven Möbelstücke mehr, sondern aktive Technologiegeräte. Premium-Pods verfügen beispielsweise über integrierte 4G-LTE-Verbindungen und Millimeterwellen-Radarsensoren zur Belegungserkennung, ohne die Privatsphäre zu beeinträchtigen. Facility Manager erhalten dadurch Zugriff auf Nutzungsdaten in Echtzeit – ein Service, der über den reinen Hardware-Verkauf hinaus einen Mehrwert bietet.

Nachhaltigkeit ist ein weiterer dominanter Trend, der die Beschaffung im Markt für Meeting-Pods grundlegend verändert. Unternehmenskäufer fordern im Jahr 2025 Transparenz und drängen die Hersteller damit, ihre Umweltbelastung zu reduzieren. Framery beispielsweise konnte den CO₂-Fußabdruck seiner Produkte im Jahr 2024 um 19 % senken und die Emissionen seiner Fabrik um 58 % reduzieren. Der Trend geht hin zu Prinzipien der Kreislaufwirtschaft: Materialien wie Sperrholz werden durch Stahl ersetzt, um die Recyclingfähigkeit zu verbessern und das Gewicht um bis zu 23 % zu reduzieren. Darüber hinaus entspricht die Integration fortschrittlicher Ergonomie, wie beispielsweise höhenverstellbare Steh-Sitz-Schreibtische (74 cm bis 116 cm), den Wellness-Trends, die sich im Unternehmenssektor immer stärker durchsetzen.

Welche strukturellen und wirtschaftlichen Herausforderungen behindern die Einführung?

Trotz der positiven Prognose steht der Markt für Meeting-Pods vor einigen Herausforderungen. Die größte Hürde sind die hohen Investitionskosten. Da hochwertige Smart-Pods für eine Person zwischen 9.500 und 12.500 US-Dollar kosten, zögern kleine und mittlere Unternehmen oft, in diese zu investieren, da günstigere, wenn auch weniger effektive Alternativen bevorzugt werden. Zudem stellen die Gewichtsbeschränkungen eine Herausforderung für die Nachrüstung älterer Gebäude dar. Ein hochleistungsfähiger Akustik-Pod wie der Silen Space 2 wiegt aufgrund seiner dichten Sandwichpaneel-Konstruktion etwa 670 Kilogramm, wodurch die Böden eine hohe Tragfähigkeit aufweisen müssen. Auch die Wahrnehmung der Belüftung ist eine Herausforderung: Hersteller müssen ständig nachweisen, dass ihre Systeme das gesamte Luftvolumen alle 40 bis 60 Sekunden austauschen können, um Klaustrophobie und CO₂-Bedenken der Nutzer zu minimieren.

Wer repräsentiert die Kernkäufergruppe im Jahr 2025?

Das Käuferprofil im globalen Markt für Meeting-Pods hat sich über Tech-Startups hinaus erweitert und umfasst nun auch traditionelle multinationale Konzerne, Flughäfen und Universitäten. Allein Framery betreut über 11.000 Unternehmenskunden, was auf eine breite institutionelle Akzeptanz hindeutet. Auch die „Coworking 2.0“-Welle stellt ein bedeutendes Käufersegment dar, da Betreiber flexibler Arbeitsräume Pods installieren, um höhere Mitgliedsbeiträge zu rechtfertigen. Öffentliche Räume sind das nächste Wachstumsfeld: Flughäfen und Bahnhöfe bieten nutzungsbasierte Pods für Geschäftsreisende an.

Diese Käufer legen Wert auf Langlebigkeit und Plug-and-Play-Funktionalität und bevorzugen Geräte, die mit Standard-Wechselstrom von 100–240 V betrieben werden können und nur minimalen Wartungsaufwand erfordern.

Segmentanalyse

Akustische Innovationen treiben die Nachfrage nach Schallschutzlösungen im Jahr 2025 an

Der Markt für Besprechungskabinen verzeichnet einen starken Anstieg der Nachfrage nach Akustikkabinen, die einen beachtlichen Marktanteil von über 36,09 % erreichen. Diese Dominanz ist maßgeblich auf die Einführung der ISO-Norm 23351-1 im Jahr 2024 zurückzuführen, die Kabinen mit einer Schalldämmung von über 30 Dezibel als Klasse A einstuft. Hersteller wie Framery reagierten darauf mit der Integration von 4G-LTE-fähigen Sensoren zur aktiven Anpassung der Geräuschmaskierung und verbesserten so die Echtzeit-Isolierung. Aktuelle Studien aus dem Jahr 2025 bestätigen, dass Hintergrundgeräusche weiterhin die Hauptursache für Ablenkung im Büro sind und zu einem Leistungsabfall von 66 % führen. Daher installieren Unternehmen diese Kabinen verstärkt, um neurodiverse Mitarbeiter vor sensorischer Überlastung zu schützen. Hochwertige Materialien wie Akustikfilz und doppelt verglastes Sicherheitsglas gewährleisten, dass Gespräche selbst in einem Meter Entfernung unverständlich bleiben.

Diese Eigenschaften haben den Markt für Besprechungskabinen unverzichtbar gemacht, um in dicht besiedelten Arbeitsumgebungen die Vertraulichkeit zu wahren. Daten von Anwesenheitssensoren aus dem Jahr 2024 zeigen, dass akustische Privatsphäre für Mitarbeiter die wichtigste Voraussetzung für einen angenehmen Arbeitsplatz ist – noch vor der Beleuchtung. Rechts- und Finanzinstitute beschaffen diese Kabinen nun, um strenge Vertraulichkeitsauflagen gegenüber ihren Mandanten zu erfüllen, ohne teure Trockenbauwände finanzieren zu müssen. Aktive Geräuschunterdrückung in Premiummodellen hat das Interesse der Verbraucher zusätzlich verstärkt. Letztendlich liegt der Fokus nun auf der Schaffung von „Sprachprivatsphäre“-Zonen, in denen offene Büros lebendig bleiben, ohne konzentriertes Arbeiten in der Kabine zu stören.

Zusammenarbeit in kleinen Gruppen treibt den Absatz kompakter Besprechungseinheiten an

Meeting-Pods für 2–4 Personen haben sich zum Rückgrat der Branche entwickelt und dominieren den globalen Markt mit einem Marktanteil von 42,53 %. Unternehmensdaten aus dem Jahr 2024 zeigen, dass sich die durchschnittliche Teilnehmerzahl bei Präsenzmeetings bei drei Personen stabilisiert hat, wodurch große Konferenzräume überflüssig werden. Da mittlerweile 86 % der Interaktionen mit virtuellen Teilnehmern stattfinden, eignen sich diese kompakten Einheiten ideal als „hybride Besprechungsräume“. Framery hat kürzlich die „Four“-Serie speziell für diesen effizienten Markt eingeführt. Immobilienanalysen belegen, dass die Aufstellung von 4er-Pods die Fläche 40 % effizienter nutzt als herkömmliche Konferenzräume.

Zu den Hauptabnehmern von Meeting-Pods zählen agile Technologieunternehmen und Coworking-Anbieter. Diese nutzen die Kapazität von zwei bis vier Personen für Einzelgespräche und schnelle Brainstorming-Sitzungen. Startups bevorzugen diese Größe aufgrund ihrer Skalierbarkeit, die es Teams ermöglicht, ihre Kapazität ohne Bauverzögerungen zu erweitern. Auch die Einhaltung von Vorschriften ist einfacher, da diese Größe problemlos den Brandschutz- und Belüftungsstandards für geschlossene Räume entspricht. Darüber hinaus zeigen Belegungsstatistiken aus dem Jahr 2024, dass Vier-Personen-Pods höhere stündliche Auslastungsraten erzielen als Einzelkabinen oder große Räume.

Unternehmenszentralen priorisieren flexible Datenschutzlösungen für höhere Mitarbeiterproduktivität

Büroflächen bleiben der Haupteinsatzbereich und tragen dazu bei, dass diese Anwendung einen Marktanteil von über 41 % hält. Die strengen Vorgaben zur Rückkehr ins Büro ab 2024 haben einen kritischen Mangel an privaten Bereichen in Großraumbüros offengelegt. Facility Manager entscheiden sich zunehmend für flexible Meeting-Pods anstelle von festen Bauten, da diese als Möbel gelten und somit Vorteile bei der beschleunigten Abschreibung bieten. Ein JLL-Bericht aus dem Jahr 2025 stellte fest, dass flexible Büroflächen zehnmal schneller wachsen als feste Neubauten. Unternehmen nutzen die Pods auch, um separate „Bereiche“ zu schaffen, die visuelle Monotonie aufzubrechen und gleichzeitig die Lärmbelastung über große Etagen zu reduzieren.

Die Installationen zielen gezielt auf ungenutzte Bereiche wie Flure ab und verwandeln ungenutzte Flächen in produktive Arbeitsbereiche. Technologiekonzerne bestellen mittlerweile ganze Flotten von Meeting-Pods, die mit Tablets ausgestattet sind, welche sich nahtlos mit Microsoft Outlook und Google Kalender synchronisieren lassen. Da die Büroauslastung 2024 durchschnittlich bei 50 % liegen wird, nutzen Unternehmen diese flexiblen Einheiten, um die Größe ihrer Arbeitsbereiche an die tägliche Anwesenheit anzupassen. Die Möglichkeit zum Abbau und zur Versetzung ist für Mieter mit kurzfristigen Mietverträgen unerlässlich, um Wiederherstellungskosten zu vermeiden. Umfragen im Jahr 2025 werden private Arbeitsbereiche auf Abruf weiterhin als eine der drei wichtigsten Anforderungen von Mitarbeitern werten, was das Wachstum des Marktes für Meeting-Pods weiter ankurbeln wird.

Diesen Bericht anpassen + von einem Experten validieren

Greifen Sie nur auf die Abschnitte zu, die Sie benötigen – regionsspezifisch, unternehmensbezogen oder nach Anwendungsfall.

Beinhaltet eine kostenlose Beratung mit einem Domain-Experten, der Sie bei Ihrer Entscheidung unterstützt.

Holzdesigns dominieren die Ästhetik moderner Büromöbelarchitektur

Holz hat sich als führendes Material etabliert und wird 2025 fast 39,67 % aller gebauten und verkauften Einheiten ausmachen. Diese Präferenz im Markt für Meeting-Pods wird durch biophile Trends befeuert, da natürliche Eichenholzoberflächen nachweislich den Cortisolspiegel der Mitarbeiter senken. Akustische Tests aus dem Jahr 2024 zeigten, dass Massivholzkonstruktionen Schallfrequenzen besser absorbieren als Glasalternativen und so für eine wärmere Raumakustik sorgen. Hersteller setzen zunehmend auf Brettsperrholz (CLT) für Rahmenkonstruktionen, das eine stahlähnliche Stabilität bei reduziertem CO₂-Fußabdruck bietet. Die Verwendung von FSC-zertifiziertem Holz ist mittlerweile Standard, um die ESG-Kriterien großer Unternehmen zu erfüllen.

Verbraucher verbinden Holzfassaden mit wohnlichem Komfort und mildern so die sterile Atmosphäre moderner Arbeitsplätze. Skandinavische Prinzipien prägen die Ästhetik von 2025, und Marken wie Taiga Concept nutzen Holz, um Technologie und Natur zu vereinen. Thermische Studien belegen, dass Holz im Innenbereich die Luftfeuchtigkeit effektiver reguliert als synthetische Materialien und so für ein angenehmes Raumklima sorgt. Renommierte Anwaltskanzleien bevorzugen Furniere, die zu maßgefertigten Möbeln passen und so den Umsatz im Luxussegment ankurbeln. Dank der natürlichen Langlebigkeit von Holz können Unternehmen im Bereich der Besprechungskabinen Produkte anbieten, die starker Beanspruchung besser standhalten als lackiertes Metall.

Um mehr über diese Studie zu erfahren: Fordern Sie ein kostenloses Muster an

Regionalanalyse

Nordamerika dominiert den Markt für Meeting-Pods durch Investitionen in die Büromodernisierung

Nordamerika erzielt derzeit einen beeindruckenden Anteil von 50 % am weltweiten Umsatz – eine Dominanz, die vor allem auf die aggressive Rückkehr ins Büro in den USA zurückzuführen ist. Da die durchschnittlichen Mieten für Büroflächen der Klasse A in Metropolen wie New York und San Francisco im Jahr 2025 voraussichtlich über 80 US-Dollar pro Quadratfuß liegen werden, verzichten Mieter verstärkt auf teure, feste Trockenbaukonstruktionen. Stattdessen investieren US-Unternehmen in modulare Gebäude, wobei das Beschaffungsvolumen für Modulbüros im Vergleich zum Vorjahr um 35 % gestiegen ist.

Die Nachfrage konzentriert sich stark auf die Technologie- und Finanzbranche, wo Datenschutz von größter Bedeutung ist, was dazu führt, dass bis Ende 2025 schätzungsweise 150.000 Einheiten auf dem gesamten Kontinent installiert werden. Folglich haben die Umsätze der Marktführer in den USA alle anderen Regionen zusammen übertroffen, da Unternehmen steuerlich begünstigten Möbelanlagen den Vorrang vor dauerhaften Gebäudeveränderungen einräumen.

Der Markt für Meeting-Pods im asiatisch-pazifischen Raum expandiert dank rasanter Entwicklung der kommerziellen Infrastruktur

Nach den USA hat sich die Region Asien-Pazifik dank des massiven Ausbaus der Global Capability Centers (GCCs) in Indien und der zunehmenden Verbreitung von Büroflächen in Japan den zweiten Platz gesichert. Bis 2025 wird für die Region eine durchschnittliche jährliche Wachstumsrate (CAGR) von über 25 % prognostiziert – die höchste weltweit. Allein in Indien überstieg die Nettobüroflächennachfrage 2024 60 Millionen Quadratfuß, wodurch ein unmittelbarer Bedarf an skalierbaren Lösungen für mehr Privatsphäre, wie beispielsweise Telefonzellen, für Videokonferenzen mit hohem Teilnehmeraufkommen entstand.

Darüber hinaus treibt die in Japan kulturell tief verwurzelte Vorliebe für Schalldämmung weiterhin Großbestellungen an, da multinationale Unternehmen ihre Großraumbüros mit hochverdichteten Arbeitsplatzinseln ausstatten. Der Markt ist hier volumengetrieben, wobei sich mittelgroße Arbeitsplatzinseln um die 6.000 US-Dollar am schnellsten durchsetzen, um der hohen Belegschaftsdichte gerecht zu werden.

Europäischer Markt für Meeting-Pods: Nachhaltigkeit und Einhaltung der Datenschutzbestimmungen stehen im Vordergrund

Europa bleibt trotz seines dritten Platzes im Hinblick auf das Produktionsvolumen ein wichtiger Innovationsstandort. Die Region bildet das technische Rückgrat des Marktes für Meeting-Pods und ist Heimat von Branchenriesen wie Framery und Silen. Die Nachfrage konzentriert sich hier weniger auf reine Expansion als vielmehr auf die Modernisierung hin zu „intelligenten“ und nachhaltigen Einheiten, um die Anforderungen des EU Green Deals zu erfüllen. Deutschland und Großbritannien sind weiterhin führend bei der Einführung von Meeting-Pods. Dort treiben die strengen DSGVO-Bestimmungen zum Schutz der Vertraulichkeit von Gesprächen in Gemeinschaftsräumen die Installation von nach ISO 23351-1 Klasse A zertifizierten Einheiten voran.

Während das Mengenwachstum im Vergleich zur Explosion in Asien stetiger ausfällt, weist Europa weiterhin den höchsten durchschnittlichen Verkaufspreis (ASP) auf. Der Anteil der Premium-Einheiten am regionalen Absatzmix liegt bei 40 %, was auf Unternehmensvorgaben für Netto-Null-zertifizierte Möbel zurückzuführen ist.

Aktuelle Entwicklungen auf dem Markt für Meeting-Pods

- Einführung der Framery Smart Pods: Framery hat seine Smart Pods der nächsten Generation vorgestellt, die über adaptive Luftzirkulation, mmWave-Sensoren zur Anwesenheitserkennung, voreingestellte Videoanrufbeleuchtung und 100%ige Recyclingfähigkeit bei reduzierten Kosten verfügen.

- PrivacyPod-Produktpalette 2025: PrivacyPod hat anpassbare Kabinen für 2-8 Personen auf den Markt gebracht, die über eine 30-dB-Schalldämmung, verstellbare Schreibtische, WLAN-fähige Tablets und wetterfeste Modelle für den Außenbereich verfügen.

- Einsatz von Evolution Dome bei Konferenzveranstaltungen: Evolution Dome lieferte 137 Konferenzkabinen für eine große US-amerikanische Gesundheitskonferenz und präsentierte damit skalierbare, aufblasbare Lösungen.

- Framery Building Growth Award: Framery erhielt den finnischen Building Growth Award 2025 für die erfolgreiche Entwicklung vom Startup zum globalen Marktführer im Bereich Pods.

- PrivacyPod Smart Pod vorgestellt: PrivacyPod hat intelligente, schalldichte Kabinen für Unternehmen auf den Markt gebracht, die auf Rentabilität und fortschrittliche Funktionen setzen.

Führende Anbieter im Markt für Meeting-Pods

- Dapapod

- Framery Oy

- Kettal

- MEAVO Limited

- Pod Space

- Stille

- Silent Labs

- Specistor

- Steelcase

- Taiga-Konzept

- The Meeting Pod Company Ltd

- V Cube.com

- Welltek

- Weitere prominente Spieler

Marktsegmentierungsübersicht:

Nach Kapseltyp

- Akustikkapseln

- Sichtschutzkabinen

- Tele Cubes

- Stände

- Kapseln

- Kollaborative Pods

- Anpassbare Kapseln

- Andere

Nach Kapazität

- Einzelperson

- 2-4 Personen

- 5-8 Personen

- 8+ Personen

Nach Material

- Holz

- Metall

- Plastik

- Andere

Nach Verwendung

- Indoor-Meeting

- Treffen im Freien

Nach Funktionalität

- Schalldämmung

- Geräuschunterdrückung

- IoT-Integration

- Andere

Durch Bewerbung

- Coworking-Space

- Büroflächen

- Öffentlicher Raum

- Einzelhandelsfläche

- Andere

Vom Endbenutzer

- KMU

- Großunternehmen

- Bildungseinrichtungen

- Startups

- Freiberufler

- Andere

Nach Region

- Nordamerika

- Die USA.

- Kanada

- Mexiko

- Europa

- Westeuropa

- Großbritannien

- Deutschland

- Frankreich

- Italien

- Spanien

- Übriges Westeuropa

- Osteuropa

- Polen

- Russland

- Übriges Osteuropa

- Westeuropa

- Asien-Pazifik

- China

- Indien

- Japan

- Südkorea

- Australien und Neuseeland

- ASEAN

- Indonesien

- Thailand

- Malaysia

- Philippinen

- Singapur

- Rest der ASEAN

- Übriges Asien-Pazifik

- Naher Osten

- Saudi-Arabien

- Kuwait

- VAE

- Katar

- Oman

- Bahrain

- Übriger Naher Osten

- Südamerika

- Argentinien

- Brasilien

- Restliches Südamerika

SIE SUCHEN UMFASSENDES MARKTWISSEN? KONTAKTIEREN SIE UNSERE EXPERTEN.

SPRECHEN SIE MIT EINEM ANALYSTEN

.svg)

Merkmale | Lizenzart | ||||

Datenbuch | Einzelbenutzer |   Mehrere Benutzer | Unternehmen | ||

| E-Zugang | ✓ | ✓ | ✓ | ✓ | |

Benutzerfreigabe | Nur für 1 Benutzer | Nur für 1 Benutzer | Bis zu 7 Benutzer | Unbegrenzter Benutzerzugriff | |

⨉ | ⨉ | ⨉ | ✓ | ||

Kostenlose Anpassung | Keine kostenlose Anpassung | Bis zu 30 Stunden Arbeit | Bis zu 60 Stunden Arbeit | Bis zu 80 Arbeitsstunden | |

Lieferformat |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analystenunterstützung | 2 Monate Analystenunterstützung | 4 Monate Analystenunterstützung | 7 Monate Analystenunterstützung | Ein Jahr Analystenbetreuung | |

Kostenloses Bericht-Update im nächsten Aktualisierungszyklus | ⨉ | ⨉ | ⨉ | ✓ | |

Kostenloses Branchen-Update (Innerhalb von 180 Tagen) | ⨉ | ⨉ | ⨉ | ✓ | |

Nutzen | Bis zu 10 % Rabatt nach dem Kauf | Bis zu 20 % Rabatt nach dem Kauf | Bis zu 30 % Rabatt nach dem Kauf | Bis zu 40 % Rabatt nach dem Kauf | |