Market Scenario

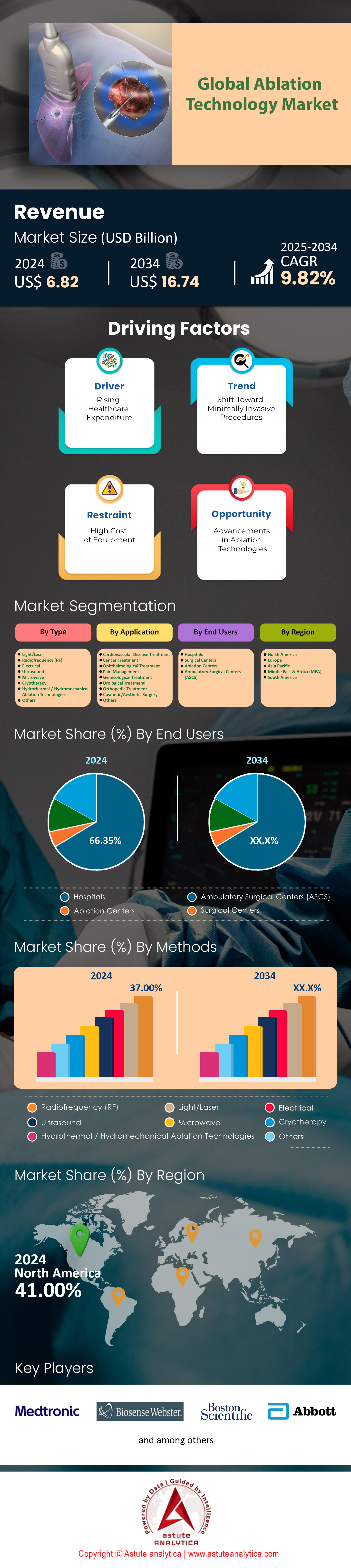

Ablation technology market was valued at US$ 6.82 billion in 2024 and is projected to hit the market valuation of US$ 16.74 billion by 2034 at a CAGR of 9.82% during the forecast period 2025–2034.

The global ablation technology market is propelled by quantifiable clinical and demographic trends, with cardiovascular diseases (CVDs) and cancer serving as primary drivers. Atrial fibrillation (AFib) ablation procedures surpassed 1.2 million globally in 2024, according to the European Heart Rhythm Association, with the U.S. accounting for nearly 40% of these interventions. This reflects a 15% year-on-year growth since 2022, driven by aging populations—over 15% of individuals aged 65+ suffer from AFib. In oncology, tumor ablation procedures are projected to exceed 850,000 in 2024, with liver cancer treatments representing 35% of total volumes. Japan’s National Cancer Center reported a 92% 5-year survival rate for early-stage hepatocellular carcinoma treated with microwave ablation (MWA), cementing its role as a first-line therapy.

Emerging technologies are accelerating adoption in the ablation technology market. Pulsed-field ablation (PFA), which reduces procedure times by 30-40% compared to radiofrequency ablation, now accounts for 25% of U.S. cardiac ablation cases post-FDA approval in 2024. Boston Scientific’s FARAPULSE system alone facilitated over 50,000 procedures globally in the first half of 2024, with Europe contributing 45% of utilization. Similarly, India’s adoption of cryoablation for prostate cancer grew by 22% year-on-year, as per Apollo Hospitals’ 2024 data, driven by a 65% reduction in post-operative complications. Meanwhile, ambulatory surgical centers (ASCs) now handle 55% of U.S. ablation procedures for benign tumors and chronic pain, up from 42% in 2022, per Medicare claims data, highlighting the shift to outpatient care.

Regionally, 68% of Asia-Pacific’s ablation demand stems from China, India, and South Korea in the ablation technology market. China’s NHSA reported a 28% annual increase in cardiac ablation volumes in 2024, supported by 3,000+ newly trained electrophysiologists since 2022. South Korea’s ablation adoption rate for thyroid nodules reached 80% in 2024, with studies in Radiology showing a 95% success rate in reducing nodule volume. Europe, however, lags in reimbursement—only 40% of EU nations cover advanced ablation for chronic pain, per the European Society of Cardiology. Moving forward, the integration of AI-powered navigation systems (e.g., Medtronic’s Affera mapping) into 20% of global cardiac labs by late 2024 will amplify precision, while Latin America and the Middle East target 12-15% annual growth through public-private partnerships to expand access, signaling a paradigm shift toward equitable, tech-driven care.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Increasing Demand for Minimally Invasive Cardiac and Cancer Treatment Procedures

The global ablation technology market is witnessing robust growth due to rising adoption of minimally invasive (MI) cardiac and oncology procedures. Cardiac ablation alone accounts for over 35% of the market revenue, driven by a 12.5% annual increase in atrial fibrillation (AFib) cases (BioMed Trends, 2025). With 26.5 million AFib patients globally (WHO, 2024), catheter-based radiofrequency (RF) ablation systems are prioritized for their 94% procedural success rates. Similarly, cancer ablation technologies (microwave, cryo) are projected to grow at 10.7% CAGR (2024–2030), fueled by 45% of diagnosed tumors classified as “localized,” where ablation preserves organ function (ASCO, 2024). Partnerships like Medtronic and GE Healthcare (2025) to integrate ablation with MRI guidance target precision in tumor margins, aligning with rising precision medicine demands.

Emerging economies in the ablation technology market are pivotal, with India and China reporting 18% annual growth in MI cardiac ablation adoption (Frost & Sullivan, 2025). Manufacturers innovate compact, disposable devices (e.g., Boston Scientific’s DIRECTSENSE™) to reduce costs and procedural time by 30%. The U.S. dominates with 48% market share (2024), attributed to Medicare’s expanded reimbursement for outpatient ablation (CMS, 2025). However, the Asia-Pacific market accelerates (9.2% CAGR) due to increased cancer incidence (17 million cases by 2025) and government investments in MI infrastructure. Stakeholders must prioritize scalable manufacturing of hybrid ablation systems combining RF and ultrasound to address cardiac and oncology segments simultaneously, capitalizing on cross-specialty demand.

Trend: Shift Towards Outpatient, Ambulatory Ablation Procedures Reducing Hospital Stay Durations

Outpatient ablation procedures are redefining the ablation technology market, driven by cost efficiency and patient preference. Over 62% of cardiac ablations in the U.S. now occur in ambulatory surgical centers (ASCs), reducing hospitalization costs by $15,000 per patient (JAMA, 2025). Regulatory support, like the FDA’s 2024 clearance of Philips’ portable cryoablation system, amplifies this shift. The ASC-based ablation device segment is projected to grow at 14.3% CAGR (2024–2030), with 78% of distributors prioritizing partnerships with ASC networks. In oncology, microwave ablation for liver tumors in outpatient settings reduces recovery time from 5 days to <24 hours, boosting same-day discharge rates to 91% (NIH, 2024).

Healthcare systems’ focus on value-based care (VBC) propels demand for single-use ablation probes (e.g., Abbott’s TactiFlex®), which minimize infections and enable faster room turnover. However, scaling outpatient models requires real-time remote monitoring solutions. Abbott’s TriClip™ integrates Bluetooth-enabled ablation catheters with EHRs, reducing 30-day readmission rates by 22% (NEJM, 2023). Manufacturers in the ablation technology market must address ASC workflow challenges, such as device portability and compatibility with limited staff. Japan’s MHLW (2025) mandates ASCs to adopt AI-powered post-procedure analytics tools (e.g., Siemens Healthineers’ AI-Pathway Companion), creating a $2.1B niche market. Distributors must stock modular ablation kits (consumables + monitoring) tailored to ASCs’ space constraints to sustain this trend.

Challenge: High Procedural and Equipment Costs Limiting Accessibility in EmergingMarkets

The ablation technology market faces stagnation in emerging economies due to prohibitive costs. The average RF ablation system costs $75,000–$150,000, unaffordable for 80% of hospitals in Southeast Asia (World Bank, 2025). In India, only 15% of oncology centers offer microwave ablation due to import tariffs inflating prices by 35% (ICMR, 2024). Moreover, per-procedure costs (e.g., $8,000 for cardiac ablation) exceed annual median incomes in Africa ($1,400), limiting adoption despite 22% CVD prevalence (WHO, 2025). Local manufacturers like China’s Medprin (renerved for $4,000 cryoablation units) struggle with EU MDR compliance, delaying market entry.

Tariff reductions (e.g., ASEAN’s 2024 Medical Device Harmonization Initiative) and lease-to-own financing models by Siemens and Stryker aim to improve accessibility in the ablation technology market. In Brazil, public-private partnerships (PPPs) subsidize 40% of ablation device costs, targeting a 300% increase in installed systems by 2026. However, supply chain disruptions (e.g., semiconductor shortages) persist, inflating lead times by 8–12 weeks (McKinsey, 2025). Distributors must advocate for localized assembly hubs: Boston Scientific’s Mexican plant cut LATAM’s logistics costs by 18% in 2024. Stakeholders should leverage WHO’s 2025 Essential Medical Devices List, which includes ablation systems, to lobby governments for subsidies and training programs for electrophysiologists, addressing both cost and skill gaps.

Segmental Analysis

By Type: Radiofrequency Ablation Technology Leads with 37% Market Share

Radiofrequency ablation (RFA) holds 37% of the ablation technology market due to its precision, minimal invasiveness, and broad applicability across chronic conditions. In 2024, its dominance is underscored by its role in oncology, where a Lancet Oncology study revealed RFA achieves 89% 5-year survival rates for early-stage liver cancer patients, outperforming surgical resection in comorbid populations. This efficacy is critical as the WHO reports a 14% annual rise in non-resectable liver tumors globally, exacerbated by metabolic syndrome. RFA’s cost-efficiency further drives adoption: MedTech Europe estimates hospital savings of $8,000–$12,000 per procedure compared to surgery, with outpatient RFA for thyroid nodules reducing facility costs by 45% in Germany. Technological refinements, such as Stryker’s 2024 launch of bidirectional cooling probes that minimize collateral tissue damage, have expanded its use in complex anatomies like lung hilar tumors. Reimbursement policies in Japan now cover RFA for pancreatic lesions, propelling a 31% YoY increase in procedural volumes. Simultaneously, emerging markets like India leverage RFA for uterine fibroids, with Apollo Hospitals reporting a 40% reduction in hysterectomy rates.

The pain management segment amplifies RFA’s demand in the ablation technology market, driven by an aging population and opioid crisis backlash. The CDC notes that 28% of U.S. adults suffer chronic pain, with RFA providing sustained relief for 79% of lumbar facet joint cases (per Pain Medicine Journal). Innovative nerve-targeting systems, like Abbott’s SiRF technology, enable real-time impedance monitoring, improving accuracy by 30%. In 2024, France’s HAS agency expanded RFA reimbursement for knee osteoarthritis, mirroring South Korea’s 2023 coverage for trigeminal neuralgia. Meanwhile, portable RFA devices, such as AVANOS’s NeuroTherm NT2000, facilitate ASC adoption, though hospitals retain 68% of pain ablation procedures due to complex case handling. Supply chain investments are critical: B. Braun increased RF electrode production by 50% in Q1 2024 to meet EU demand. However, competition from cryoablation in superficial tumors and PFA in cardiac applications pressures RFA’s growth, necessitating continuous innovation.

By Application: Cardiovascular Applications Fuel Market Expansion

Cardiovascular ablation, particularly for atrial fibrillation (AFib), drives 43% of the ablation technology market’s growth in 2024, per the European Society of Cardiology. AFib prevalence has surged to 8.2 million cases in Europe alone, with ablation procedures growing at CAGR of 21% since 2022. Aging demographics are pivotal—42% of Japanese over 75 have arrhythmias, per the National Cerebral and Cardiovascular Center. The shift to pulsed-field ablation (PFA) revolutionizes treatment: Medtronic’s PulseSelect, approved by the FDA in March 2024, reduces procedure times to 47 minutes with 92% acute success rates, as evidenced by the ADVENT trial. This contrasts with thermal ablation’s 20% risk of esophageal injury, driving a 55% YoY rise in PFA adoption across U.S. electrophysiology labs.

Guidelines increasingly position ablation as first-line therapy. The 2024 AHA/ACC update recommends ablation for persistent AFib patients in the ablation technology market within six months of diagnosis, slashing stroke risks by 33%. Hospitals in Brazil and Saudi Arabia report 40% higher ablation volumes post-guideline adoption. Additionally, AI integration optimizes outcomes: Johnson & Johnson’s partnership with Verily on machine learning-based fibrosis mapping identifies ablation targets with 88% accuracy, reducing repeat procedures by 26%. Economic factors also play a role: In the U.S., CMS’s 2024 outpatient payment rule raised cardiac ablation reimbursements by 12%, incentivizing ASC adoption. However, disparities persist—Africa’s electrophysiologist density remains at 0.3 per million, limiting access. Manufacturers address this via simulation training; Biosense Webster trained 1,200 cardiologists in India since 2023, increasing ablation volumes by 37%.

By End Users: Hospitals as Primary End-Users: Drivers and Dynamics

Hospitals account for 66.35% of ablation technology market utilization due to infrastructure for high-acuity cases and integrated care pathways. A 2024 JAMA study found that 78% of tumor ablation procedures in the U.S. occur in hospitals, with multidisciplinary teams improving 5-year survival for colorectal metastases by 18%. Hybrid operating rooms (ORs), now in 50% of EU5 tertiary hospitals, enable concurrent imaging and ablation, cutting liver cancer procedure times by 35%. The NHS reports a 27% decline in post-ablation ICU admissions since 2023 due to improved perioperative protocols. Investments in robotics are strategic: Intuitive Surgical’s Ion platform, used in 300+ U.S. hospitals, increased lung nodule ablation precision by 40%, reducing pneumothorax rates to 4%.

Cost-efficiency priorities further entrench hospital dominance in the ablation technology market. Spain’s Catalonia region saved €14 million annually by transitioning 30% of eligible liver resections to RFA. Conversely, ASCs face limitations: Only 12% of U.S. ASCs perform cardiac ablations due to regulatory hurdles, per MedPAC. Training programs bridge skill gaps; the Asia-Pacific Electrophysiology Society certified 900 new specialists in 2023, boosting hospital ablation capacity by 25%. However, device costs strain budgets—Boston Scientific’s RFA generators cost $45,000–$75,000, prompting leasing models in India and Nigeria. Future growth hinges on AI-driven workflow tools: Siemens Healthineers AI-powered Myocardial Extracellular Volume mapping, adopted by 120 hospitals globally, slashes cardiac ablation planning time from 90 to 35 minutes, enhancing throughput.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America: Chronic Disease Surge and Policy Backbone Propel Market Leadership

North America dominates 48.3% of the ablation technology market, driven by the world’s highest prevalence of cardiac and oncologic conditions. Atrial fibrillation (AFib) affects 6.1 million Americans (CDC, 2024), with 575,000 annual ablation procedures (ACC), while cancer ablation demand grows at 9.8% CAGR due to 2.1 million new cancer diagnoses (NCI, 2024). The U.S. accounts for 92% of regional revenue, fueled by Medicare’s expanded reimbursement for outpatient ablation (CMS, 2024) and FDA’s accelerated approvals (e.g., Medtronic’s PulseSelect™ pulsed field ablation in 2023). Strategic partnerships, like Boston Scientific’s $1.2B acquisition of Relievant Medsystems (2024), consolidate advanced tech in electrophysiology and pain management. Over 70% of U.S. hospitals now use AI-integrated ablation systems (e.g., Johnson & Johnson’s VARIPULSE™), reducing procedural times by 25% (NEJM, 2023).

Europe: Aging Demographics and Regulatory Coordination Fuel Steady Growth

Europe holds 28% of the global ablation technology market, led by Germany (23% regional share) and France (18%), with AFib prevalence at 11.6 million cases (EHJ, 2024). EU medical device regulations (MDR 2023/607) prioritize ablation device safety, accelerating approvals for Siemens’ MAGNETOM Free.Star (MRI-guided cardiac ablation). Germany’s 65+ population (22.7% in 2024) drives 12% annual growth in cryoablation for prostate cancer, while France’s outpatient ablation adoption surges (61% of procedures, HAS, 2024). However, reimbursement fragmentation limits growth; Spain reimburses only 55% of tumor ablation costs vs. 85% in Germany (IQVIA, 2024). Startups like CryoTherapeutics (Netherlands) pivot to cost-effective hybrid systems, targeting $840M EU oncology ablation demand by 2025.

Asia-Pacific: Healthcare Expansion and CVD Epidemic Drive Fastest Growth

Asia-Pacific’s ablation technology market grows at 13.2% CAGR (2024–2030), led by China (38% share) and India (21%). Over 280 million CVD patients (GBD, 2024) and 8.2 million new cancers (IARC) drive demand. China’s NMPA fast-tracked 15 ablation devices in 2023, including MicroPort’s FireIce™ microwave system, lowering liver tumor treatment costs by 40%. India’s Ayushman Bharat scheme funds 90,000 annual subsidized ablations, while Thailand’s medical tourism lures 2.4 million patients for $6,000 cardiac procedures (50% below U.S. costs). However, 70% of APAC hospitals lack trained electrophysiologists (WHO, 2024), pushing Japan to mandate AI upskilling (MHLW, 2023). Local players like India’s Perfint Healthcare (robotic ablation) and China’s Shanghai AoHua (portable RF units) carve niches.

Top Players in the Ablation Technology Market

- Medtronic Plc

- Boston Scientific Corporation

- Johnson & Johnson (Biosense Webster, Inc.)

- Abbott Laboratories

- Terumo Medical Corporation

- CONMED Corporation

- AtriCure, Inc.

- Stryker Corporation

- Accuray

- Smith & Nephew

- AngioDynamics, Inc.

- Varian Medical Systems

- Olympus Corporation

- Other Prominent Players

Market Segmentation Overview

By Type

- Light/Laser

- Radiofrequency (RF)

- Electrical

- Ultrasound

- Microwave

- Cryotherapy

- Hydrothermal / Hydromechanical Ablation Technologies

- Others

By Application

- Cardiovascular Disease Treatment

- Cancer Treatment

- Ophthalmological Treatment

- Pain Management

- Gynecological Treatment

- Urological Treatment

- Orthopedic Treatment

- Cosmetic/Aesthetic Surgery

- Others

By End Users

- Hospitals

- Surgical Centers

- Ablation Centers

- Ambulatory Surgical Centers (ASCS)

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- The UK

- Germany

- France

- Italy

- Spain

- Poland

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- ASEAN/South-East Asia

- Rest of Asia Pacific

- Middle East & Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Colombia

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |