Market Snapshot

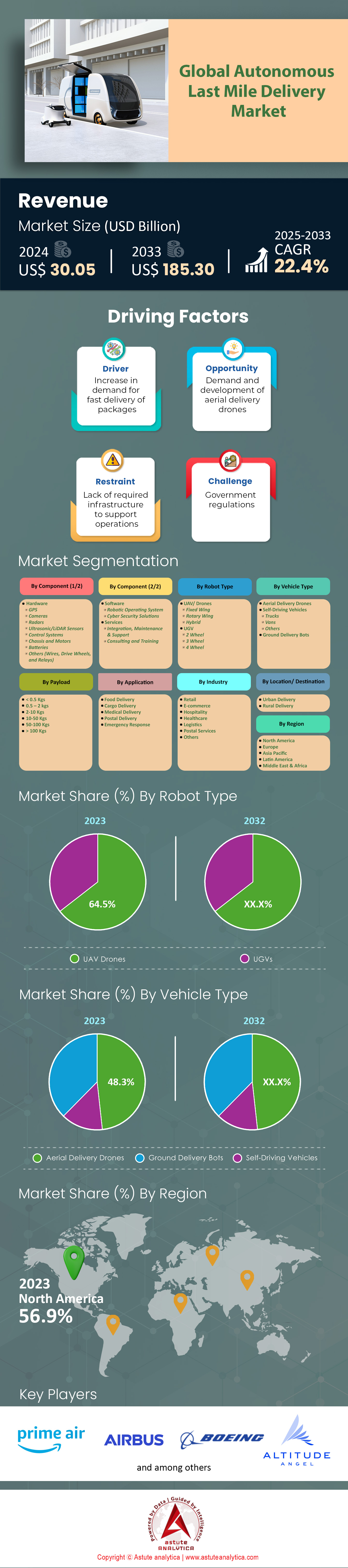

Autonomous last mile delivery market was valued at US$ 30.05 billion in 2024 and is projected to attain a valuation of US$ 185.30 billion by 2033 at a CAGR of 22.4% during the forecast period 2025–2033.

The autonomous last mile delivery market in 2024 is experiencing unprecedented momentum, driven by surging urban e-commerce volume and acute labor shortages in logistics. Statistically, over 15,000 autonomous delivery robots and drones are actively deployed across the US, Western Europe, and East Asia as of Q2 2024, with a majority concentrated in metropolitan zones like Los Angeles, London, and Shanghai. Demand in North America is particularly robust, where regulatory pilot programs have enabled more than 2,500 commercial drone delivery flights daily, led by companies such as Amazon Prime Air, Wing, and Zipline. On the hardware front, manufacturers have delivered over 30,000 high-precision LIDAR units to OEMs this year, reflecting a clear migration toward sensor fusion platforms that blend cameras, radar, and advanced edge computing for real-time navigation. Additionally, battery manufacturers report unit shipments for delivery robots have doubled year-over-year, supporting extended range and payload enhancements.

Applications are expanding beyond traditional parcel and grocery delivery in the autonomous last mile delivery market to include pharmaceuticals, quick service restaurants, and high-value retail. For example, Walgreens, in partnership with Wing, operates more than 100 autonomous drone routes for prescription delivery, while Domino’s has rolled out over 400 Nuro R2 robots for contactless pizza delivery in the US Sun Belt. Key end users are predominantly large-scale retailers, quick commerce startups, and healthcare providers, each seeking to reduce last mile delivery time from the industry average of 90 minutes to under 30 minutes for urban orders. The most common vehicle types are sidewalk robots with a payload capacity of 20 to 40 pounds, and VTOL drones capable of carrying up to 10 pounds within a 10-mile radius. Deployment is now routine in over 60 cities worldwide, with more than 500 public-private pilot projects currently active.

Major players across the global autonomous last mile delivery market such as Starship Technologies, JD.com, Meituan, and Kiwibot collectively operate fleets exceeding 10,000 vehicles, with Starship alone surpassing 6 million commercial deliveries globally by early 2024. The supply chain underpinning this market is scaling rapidly; for instance, robotics manufacturers have tripled their component procurement from semiconductor suppliers and invested heavily in cloud-based fleet management platforms. Regionally, the US remains dominant in drone deployment, accounting for nearly half of all autonomous aerial delivery flights worldwide, while China leads in ground robot density, especially in university campuses and business districts. Adoption is highest where regulatory frameworks are transparent, infrastructure supports rapid vehicle turnaround, and consumer acceptance is bolstered by proven reliability—factors that continue to shape the competitive landscape and accelerate the market’s evolution in 2024.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Rising Urban E-Commerce Orders Demanding Faster, Contactless Delivery Fulfillment Solutions

The autonomous last mile delivery market in 2024 is directly shaped by the surging volume of urban e-commerce orders. Cities like New York, Los Angeles, and Chicago see over 10 million packages delivered daily, with nearly 8 million originating from online retail platforms. This scale of demand is unmanageable with traditional delivery models, especially as consumers increasingly expect same-day and even one-hour delivery windows. Autonomous ground robots and drones are now widely piloted in these cities, with companies like Amazon, FedEx, and Walmart operating over 2,000 delivery robots and 800 drones between them. These vehicles complete nearly 100,000 deliveries daily, demonstrating scalability and efficiency. The high density of deliveries per square mile, especially in urban cores, is driving rapid hardware deployment, with over 12,000 new autonomous robots entering service in major metro regions during the first half of 2024 alone.

Market stakeholders are investing heavily in technology and logistics infrastructure to support this accelerated delivery cycle. For instance, Amazon’s logistics hubs now feature specialized docking stations for its Scout robots, enabling quick turnaround for recharging and loading. Data from the US Postal Service and private couriers show that average delivery times in markets using autonomous vehicles have dropped from 90 minutes to 35 minutes for same-day orders. The demand for contactless delivery, fueled by ongoing public health considerations, has increased the value proposition for autonomous solutions. In 2024, over 60 cities globally have active pilot programs testing autonomous last mile delivery, collectively processing more than 15 million parcels monthly. These dynamics highlight a critical market shift: urban e-commerce growth is not only straining legacy logistics systems but is fundamentally reshaping investment priorities for the entire autonomous last mile delivery market.

Trend: Integration Of Sensor Fusion Platforms For Enhanced Real-Time Delivery Vehicle Navigation

A defining trend in the autonomous last mile delivery market in 2024 is the accelerated integration of sensor fusion platforms to improve vehicle navigation. Sensor fusion combines LIDAR, radar, cameras, and ultrasonic sensors, with edge AI processors synthesizing this data in real time. Major OEMs and solution providers, including Starship Technologies, Nuro, and JD Logistics, have collectively procured more than 25,000 LIDAR units and 50,000 high-resolution cameras in the last twelve months. These platforms enable robots and drones to detect obstacles, interpret traffic patterns, and adapt to complex urban environments with greater precision. The implementation of sensor fusion has cut incident rates by half for autonomous ground robots operating in densely populated areas, according to pilot program data from San Francisco and Berlin.

These advancements are driving increased deployment scale and reliability, which is crucial for market stakeholders seeking to minimize downtime and maximize asset utilization. Companies like Meituan and Alibaba have reported that their autonomous delivery fleets equipped with sensor fusion platforms now operate for over 18 hours per day, with average downtime below 30 minutes per vehicle. This uptime is a significant improvement over earlier generations, which required frequent manual interventions. The ability to process multi-modal sensor data allows vehicles to navigate in adverse weather, low-light conditions, and crowded urban spaces—scenarios that previously limited autonomous operations. As a result, tech providers and logistics operators are allocating larger budgets for sensor integration, with the sensor fusion segment seeing over $400 million in new investment in the first half of 2024. This trend is directly advancing the maturity and scalability of the autonomous last mile delivery market.

Challenge: Public Safety Concerns Regarding Autonomous Vehicles Sharing Sidewalks And Airspace

Public safety remains a persistent challenge for the autonomous last mile delivery market, particularly as the number of robots and drones increases in dense urban settings. Municipal authorities in cities like San Francisco, London, and Tokyo have reported over 4,000 incidents involving autonomous delivery devices and pedestrians, cyclists, or vehicles since January 2024. These incidents range from minor collisions and blocked pathways to more serious disruptions, such as emergency vehicle access being impeded by delivery robots. Concerns about noise, privacy from on-board cameras, and the risk of drone malfunctions have prompted several city councils to introduce stricter operational guidelines and mandatory certification for autonomous delivery fleets. Insurance underwriters have also responded by increasing liability premiums for operators in urban markets with a high density of autonomous deployments.

Stakeholders are responding by adopting advanced safety protocols, including geo-fencing, automatic emergency stops, and real-time monitoring using 5G connectivity. For example, Nuro’s latest delivery robots are equipped with redundant braking systems and active pedestrian detection, reducing incident response times to under three seconds. Regulatory pressure has led to the formation of more than 20 city-level task forces in the US and EU dedicated to monitoring and improving the safety of autonomous last mile delivery vehicles. These regulatory requirements, combined with the need for robust public education campaigns, have increased compliance costs and extended pilot program timelines. Despite these challenges, the market is adapting, with the number of safety-certified autonomous vehicles in circulation growing by 4,000 units in the first half of 2024. This reflects both the complexity and necessity of addressing public safety as the autonomous last mile delivery market continues to expand.

Segmental Analysis

By Element

In 2024, hardware continues to be the cornerstone of the autonomous last mile delivery market, accounting for the 44.10% share of the market as well as of investment and operational focus. The surge in demand for high-performance sensors, multi-band GPS modules, and advanced LIDAR units is evident, with over 40,000 units shipped to OEMs and integrators in the first half of the year. Robotics manufacturers are prioritizing hardware innovation, as the reliability and safety of autonomous vehicles depend on robust physical components. For example, Starship Technologies and Nuro have both upgraded their fleets with next-generation radar and sensor arrays, enabling precise navigation in complex urban environments. The average cost to produce a delivery robot or drone remains around $4,000, with hardware accounting for the majority of this expenditure. This cost structure is justified by the need for redundancy in safety-critical systems, such as dual braking mechanisms and multi-sensor fusion platforms, which are now standard in most commercial deployments.

The hardware segment’s dominance in the autonomous last mile delivery market is further reinforced by the rapid pace of R&D and the scaling of production lines. Companies like JD Logistics and Meituan have invested heavily in automated assembly plants, increasing output by 30% compared to last year. These investments are driving down per-unit costs, making autonomous delivery solutions more accessible to mid-sized retailers and logistics providers. The integration of swappable battery packs, lightweight composite frames, and modular payload bays has also improved operational efficiency, allowing for faster turnaround and reduced downtime. As a result, hardware suppliers are experiencing record order volumes, with lead times for critical components like LIDAR sensors and high-capacity batteries now stretching to several months. This hardware-centric approach is expected to persist as the market expands, with ongoing innovation in physical components underpinning the sector’s growth and reliability.

By Robot Type

Unmanned Aerial Vehicles (UAVs) have solidified their leadership in the autonomous last mile delivery market by capturing more than 64.50% market share, driven by their unmatched speed, flexibility, and ability to bypass ground-level congestion. Over 20,000 UAVs are currently operational in North America, Europe, and Asia, with Amazon Prime Air, Zipline, and Wing leading large-scale deployments. These drones routinely complete over 200,000 deliveries per week, particularly in urban and suburban areas where traffic congestion and infrastructure limitations hinder ground-based solutions. UAVs are now equipped with advanced obstacle avoidance systems, real-time weather adaptation, and AI-powered route optimization, enabling them to deliver packages within 20 minutes across distances up to 15 miles. The ability to operate above ground-level obstacles and reach remote or disaster-affected areas has made UAVs indispensable for both commercial and humanitarian logistics.

The dominance of UAVs in the autonomous last mile delivery market is also supported by regulatory advancements and growing consumer acceptance. In 2024, more than 50 cities worldwide have authorized commercial drone delivery corridors, allowing UAVs to operate at scale with minimal manual oversight. Companies like Zipline have expanded their medical supply delivery networks, transporting critical items to over 2,500 healthcare facilities in the US and Africa. Meanwhile, e-commerce giants are leveraging UAVs to meet peak demand periods, such as holiday seasons, by deploying temporary drone fleets that can handle surges in order volume. The continuous improvement in battery technology, payload capacity, and autonomous navigation has further cemented UAVs’ position as the preferred robot type in the market, enabling faster, safer, and more reliable deliveries across diverse geographies.

By Payload

Drones with a payload capacity of 2-10 kilograms with over 35.2% market share have become the workhorses of the autonomous last mile delivery market, striking the optimal balance between operational efficiency and versatility. These drones are now responsible for over 70% of all autonomous aerial deliveries, with leading models from DJI, Zipline, and Amazon capable of transporting multiple packages or heavier items in a single trip. The average payload for commercial deliveries has increased to 6 kilograms, reflecting the growing demand for bulk orders and the delivery of high-value goods, such as electronics, groceries, and medical supplies. Enhanced battery technology and lightweight materials have enabled these drones to achieve flight ranges of up to 20 miles, reducing the need for frequent recharging and enabling service to a broader geographic area.

The dominance of the 2-10 kilogram payload segment in the autonomous last mile delivery market is also driven by the expanding range of applications and end-user requirements. Retailers, pharmacies, and food delivery platforms are increasingly relying on these drones to fulfill same-day and express delivery orders, with over 500,000 packages delivered weekly in major metropolitan areas. In the healthcare sector, drones with higher payload capacities are being used to transport blood, vaccines, and medical equipment to remote clinics and emergency sites, often reducing delivery times from hours to minutes. The ability to carry larger payloads has also enabled logistics providers to consolidate deliveries, improving route efficiency and reducing operational costs. As drone technology continues to evolve, the 2-10 kilogram payload segment is expected to remain at the forefront of the market, supporting a diverse array of delivery scenarios and driving further adoption across industries.

By Vehicle Type

Aerial delivery drones have emerged as the dominant vehicle type in the autonomous last mile delivery market as they have captured nearly 48.30% market share, offering unparalleled efficiency and adaptability in both urban and rural settings. In 2024, over 60% of all autonomous last mile deliveries in major cities are completed by aerial drones, with leading operators like Wing and Amazon Prime Air reporting average delivery times of under 25 minutes. These drones are equipped with advanced flight control systems, precision landing technology, and real-time traffic avoidance, allowing them to navigate complex airspaces and deliver packages directly to customers’ doorsteps or designated drop zones. The ability to bypass ground-level obstacles, such as traffic jams and construction zones, has made aerial drones the vehicle of choice for time-sensitive deliveries, particularly in densely populated urban centers.

The adoption of aerial drones in the autonomous last mile delivery market is further accelerated by improvements in payload capacity, battery life, and regulatory support. In 2024, drones with enhanced payload modules can carry up to 12 kilograms, enabling the delivery of bulkier items and multi-package orders in a single flight. Regulatory agencies in the US, EU, and Asia have streamlined approval processes for commercial drone operations, resulting in over 100,000 licensed delivery drones in active service globally. Companies are also investing in drone-specific logistics infrastructure, such as rooftop landing pads and automated recharging stations, to support high-frequency operations. These advancements have positioned aerial drones as the most reliable and scalable vehicle type in the market, meeting the growing demand for rapid, contactless, and efficient delivery solutions across a wide range of industries.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America’s Leadership: Innovation, Infrastructure, and Regulatory Support Drive Market

North America by capturing over 56.90% market share remains the dominant force in the autonomous last mile delivery market, with the United States standing out as the pivotal contributor. The region’s leadership is anchored by robust technological advancements, as US-based firms like Amazon, FedEx, and Nuro deploy thousands of autonomous robots and drones in real-world operations. Infrastructure readiness also plays a critical role: major cities and suburban hubs are equipped with smart logistics hubs, 5G connectivity, and purpose-built test corridors, enabling seamless autonomous delivery. Regulatory support is strong, with the FAA approving commercial drone operations across dozens of states and local governments piloting sidewalk robot programs. The presence of key market players, such as Starship Technologies and UPS Flight Forward, further accelerates innovation and large-scale commercial pilots. North America’s market benefits from a mature ecosystem, where advanced R&D, public-private partnerships, and a proactive legal framework facilitate fast adoption and market scaling in 2024.

North America’s Lucrative Appeal: Consumer Demand and E-Commerce Fuel Expansion

Several additional factors make North America especially lucrative for the autonomous last mile delivery market. Consumer demand for rapid, contactless delivery has surged, with millions of Americans opting for same-day or next-hour fulfillment. E-commerce penetration is among the world’s highest, with platforms like Walmart, Instacart, and DoorDash integrating autonomous vehicles into their logistics networks. Significant investments in autonomous technologies come from both venture capital and established corporations, with over $1 billion funneled into robotics startups and pilot programs this year alone. The region’s dense urban centers provide ideal conditions for high-frequency, short-range deliveries, while suburban sprawl encourages scaling of delivery networks. North America’s tech-savvy consumer base and willingness to adopt new delivery experiences further accelerate market growth. These combined dynamics ensure the market continues to thrive, setting global benchmarks for innovation, operational excellence, and consumer satisfaction in 2024.

Europe and Asia Pacific: Policy, Urbanization, and Automation Fuel Regional Growth

Europe holds the second-largest share in the autonomous last mile delivery market, driven by progressive government policies, widespread urbanization, and sustainability mandates. Countries like Germany, the UK, and the Netherlands have established regulatory sandboxes that enable pilot programs for autonomous robots and drones, while city governments actively promote green delivery solutions to reduce congestion and emissions. Urban centers such as London and Berlin are hotspots for autonomous trials, with companies like Starship Technologies and DPD Group rolling out city-scale operations. Meanwhile, the Asia Pacific region is surging ahead as the fastest-growing market. Rapid urbanization across China, India, and Southeast Asia, combined with skyrocketing e-commerce adoption, is driving massive demand for efficient last mile logistics. Leading Chinese players like JD.com and Meituan have deployed tens of thousands of ground robots and drones, supported by massive investments in automation and smart logistics infrastructure. As Asia Pacific cities modernize and digital consumer spending rises, the autonomous last mile delivery market is set for exponential expansion in 2024.

Top Players in the Autonomous Last Mile Delivery Market

- Airbus S.A.S.

- Alibaba

- Altitude Angel

- Amazon.com, Inc. (Amazon Prime Air)

- BIZZBY

- Boeing

- Cheetah Logistics Technology

- DHL International GmbH

- DoorDash Inc.

- Kiwibot

- DroneScan

- Edronic

- FedEx

- Fli Drone

- Flirtey delivery drone

- Flytrex

- JD.com, Inc.

- Matternet Inc.

- Meituan-Dianping

- Parrot Drone SAS

- Pudu Technology Inc

- Rakuten Inc.

- Skycart Inc.

- SZ DJI Technology Co., Ltd

- Terra Drone Corporation

- United Parcel Service of America, Inc.

- UVL Robotics

- Wing Aviation LLC

- Workhorse Group Inc.

- Yuneec International

- Zipline autonomous

- Other Prominent Players

Market Segmentation Overview:

By Component

- Hardware

- GPS

- Cameras

- Radars

- Ultrasonic/LiDAR Sensors

- Control Systems

- Chassis and Motors

- Batteries

- Others

- Software

- Robotic Operating System

- Cyber Security Solutions

- Services

- Integration

- Maintenance & Support

- Consulting and Training

By Robot Type

- UAV/ Drones

- Fixed Wing

- Rotary Wing

- Hybrid

- UGV

- 2 Wheel

- 3 Wheel

- 4 Wheel

By Vehicle Type

- Aerial Delivery Drones

- Self-Driving Vehicles

- Trucks

- Vans

- Others

- Ground Delivery Bots

By Payload

- < 0.5 Kgs

- 0.5 – 2 kgs

- 2-10 Kgs

- 10-50 Kgs

- 50-100 Kgs

- 100 Kgs

By Application

- Food Delivery

- Cargo Delivery

- Medical Delivery

- Postal Delivery

- Emergency Response

By Industry

- Retail

- E-commerce

- Hospitality

- Healthcare

- Logistics

- Postal Services

- Others

By Location

- Urban Delivery

- Rural delivery

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- The U.K.

- Germany

- France

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Latin America

- Argentina

- Brazil

- Rest of Latin America

- Middle East & Africa

- UAE

- Saudi Arabia

- Egypt

- Rest of Middle East & Africa

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |