Market Scenario

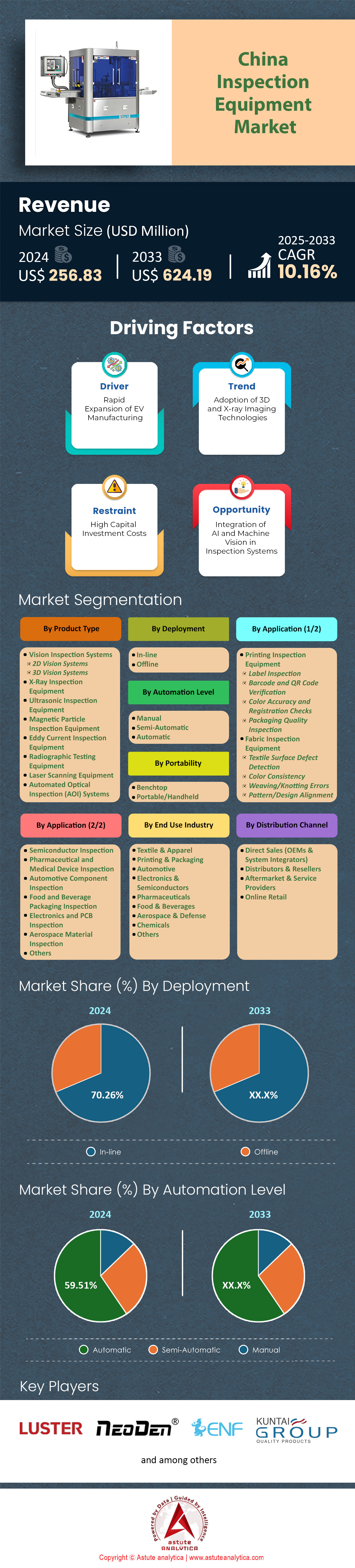

China inspection equipment market was valued at US$ 256.83 million in 2024 and is projected to hit the market valuation of US$ 624.19 million by 2033 at a CAGR of 10.16% during the forecast period 2025–2033.

China has emerged as the undisputed global leader in manufacturing quality control investment and infrastructure development, fundamentally reshaping the international landscape of inspection equipment and industrial automation. With semiconductor fab equipment spending reaching $49.55 billion in 2024 and industrial robot production hitting 556,000 units annually, China now commands both the scale and sophistication necessary to dominate global manufacturing quality standards. The remarkable achievement of 86% of "Made in China 2025" goals, coupled with the establishment of over 17,000 "5G+ Industrial Internet" projects across all 41 major industrial sectors, demonstrates that China's transformation from a low-cost manufacturer to a quality-focused industrial powerhouse is not merely aspirational but actively materializing at unprecedented speed.

The strategic shift from import dependence to domestic self-sufficiency represents a seismic change in global supply chains in the inspection equipment market. Chinese suppliers now control 85% of robot installations in the metal and machinery industry and 54% in electronics, while holding over 190,000 robot-related patents—two-thirds of the global total. This technological sovereignty extends beyond mere production capacity; it encompasses the entire innovation ecosystem, from R&D to implementation. The dramatic reduction in ASML's expected revenue share from China (from 50% to 20%) exemplifies how rapidly domestic capabilities are displacing foreign suppliers, particularly in critical sectors like semiconductor manufacturing equipment.

Looking forward, China's position in the global inspection equipment market appears unassailable in the medium term. The commitment to cultivate 15,000 new leading talents and 5 million high-skilled workers, combined with sustained investment momentum and regulatory harmonization with international standards, positions China not just as a manufacturing hub but as the global epicenter of quality control innovation. The convergence of AI, 5G, and advanced robotics within China's manufacturing ecosystem creates competitive advantages that will likely take other nations decades to replicate.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Government Mandates for Stringent Quality and Safety Standards

The Chinese government is a primary force driving the demand for inspection equipment market through a concerted push for higher quality, safety, and technological sovereignty. This is not merely a suggestion but is being enforced through a series of new mandatory national standards (GB standards) and strategic initiatives. These mandates compel manufacturers across all sectors to invest in more sophisticated inspection technologies to ensure compliance and avoid market exclusion.

- Broad Legislative Framework: In 2025, the State Council's legislative plan is set to revise and formulate numerous laws centered on high-quality development. The overarching "Made in China 2025" plan explicitly targets improving quality and efficiency as a central theme, pushing for the deep integration of new information technology and manufacturing.

- New and Updated Mandatory Standards (2024-2025):

- Electric Vehicle (EV) Chargers: As of March 1, 2025, a new rule (CNCA-C25-01:2024) will take effect, mandating CCC (China Compulsory Certification) for all electric vehicle supply equipment to ensure national safety and quality standards are met.

- Consumer Products: A wave of new mandatory standards for consumer goods will be implemented between 2024 and 2026. This includes GB/T 22849-2024 for knitted t-shirts (effective October 1, 2024), GB 44702-2024 limiting harmful substances in watch components (effective October 1, 2025), and GB 25038-2024 setting general safety requirements for footwear (effective June 1, 2025). An updated standard for woven children's clothing, GB/T 31900-2024, will become effective on December 1, 2026. It is likely to add fuel to the growth of China inspection equipment market.

- Food and Medical Devices: In March 2024, the government released 47 new national food safety standards (including GB 2760-2024). The medical device industry is also facing a transition period, with a compliance deadline of May 1, 2026, for most manufacturers to meet the GB 9706.1-2020 electrical safety standard.

- Strengthened Enforcement and Certification: Revisions to the "Regulation for Production and Filling Licensing of Special Equipment" (effective June 1, 2024) emphasize robust quality assurance systems and regular inspections by regulatory bodies. Furthermore, the China Quality Certification Center (CQC) is rolling out an updated "Certification Mark Use Approval" system, effective March 1, 2025, as part of a broader plan to build credibility in the quality certification industry. These measures create a powerful incentive for manufacturers to upgrade their inspection capabilities to secure and maintain necessary certifications.

Trend: Adoption of AI and Machine Learning in Inspection Systems

Artificial intelligence in the China inspection equipment market is rapidly moving from a buzzword to a practical and transformative tool in China's manufacturing sector, with quality inspection being a prime application. The "AI Plus" initiative, introduced in the 2024 government work report, is a strategic national push to integrate AI into industries to boost efficiency and quality.

- Market Growth and Investment: The China artificial intelligence in manufacturing market generated revenue of US$ 617.4 million in 2024 and is projected to skyrocket to US$ 5,724.1 million by 2030, growing at a CAGR of 47.2% from 2025. By 2025, China is expected to invest approximately $128 billion in AI technologies across various sectors, including manufacturing.

- Real-World Applications and Case Studies (2024-2025):

- Automotive and EV: AI-powered quality inspection robots have amassed a database of over 100 million defect samples for electric motor stators, helping to resolve post-assembly issues and bolster the reliability of China's new energy vehicles. One automaker, using Huawei's Industrial AI-powered Quality Inspection Solution, reduced defects per unit by 80%.

- Electronics and Textiles: Start-up Zhijing Technology has developed "miniature robots" with AI-empowered visual recognition that are integrated into weaving machines, enabling simultaneous weaving and flaw detection. In electronics manufacturing, companies like Foxconn are deploying deep learning algorithms for quality inspection to increase accuracy and reduce rework costs. AI-enabled vision systems from firms like Mech-Mind Robotics and SenseTime are identifying micro-defects in real-time on production lines.

- General Manufacturing: Across 18 cities in the China inspection equipment market, more than 2,700 factories have deployed intelligent robots for inspection, reducing the quality inspection workforce by over 10,000 people while improving consistency. Lenovo streamlined its production scheduling process from a 6-hour daily task to just 1.5 minutes using AI algorithms, leading to a 16% surge in production efficiency.

- AI for Government and Customs: China Customs is actively integrating AI into its inspection processes. An application known as Intelligent Customs Inspection (ICI) uses AI to review scanned images of cargo, improving regulatory efficiency and accuracy. This high-level government adoption signals the technology's maturity and encourages broader industrial use.

Challenge: Intense Competition from Established Foreign Equipment Providers

While China's domestic inspection equipment market is advancing rapidly, it faces formidable competition from established international giants, particularly from Japan, the U.S., and Germany. These foreign firms have long-standing reputations, extensive R&D, and a strong foothold in the high-end market.

- Dominant Market Share of Foreign Brands: In the broader industrial automation market, foreign firms like Siemens, Schneider Electric, Honeywell, and Emerson Electric are highly active and successful in China. In the Programmable Logic Controller (PLC) market, a core automation component, Siemens holds a commanding 40% market share. In machine vision, Japanese and American companies lead; in 2022, Keyence held a 38% share in China, while Cognex had 7%. Though these are not the latest figures, they illustrate the entrenched position of foreign leaders.

- Reliance on Imported High-End Equipment: China's imports of chipmaking equipment, which includes sophisticated inspection and metrology tools, reached a massive $38.5 billion in 2024. This highlights a continued dependence on non-Chinese suppliers for the most advanced technology, a key area where foreign providers maintain a competitive edge. The Asia Pacific region, with China as a dominant player, accounted for 54.7% of the global semiconductor metrology and inspection equipment market in 2024.

- Strategic Responses from Foreign Competitors (2025): Faced with growing local competition and a government push for domestic substitution, foreign firms are adapting their strategies in the inspection equipment market.

- Localization of R&D and Production: In March 2025, Siemens unveiled its "China Acceleration 2.0" strategy, launching 18 new products tailored to the Chinese market, 16 of which were developed entirely in China. This includes four new products for intelligent measurement and analysis.

- New Brands for the Chinese Market: Also in March 2025, Mitsubishi Electric Automation (China) launched a new brand, "Lingling," specifically to meet the needs of Chinese customers, signaling a shift away from its previous global product focus.

- The Price-Driven Rivalry: The Chinese industrial automation market saw a decline in 2024. In this environment, local players gained ground through competitive pricing. This is forcing international brands to further localize their strategies, innovate on cost-effective solutions, and even offer rapid services like "Half Day Delivery" to stay competitive in a market that is increasingly price-sensitive, yet still demands high quality.

Segmental Analysis

By Product Type

Automated Optical Inspection has achieved unprecedented dominance in the China inspection equipment market with over 48.06% market share by addressing the fundamental impossibility of human inspection in modern electronics manufacturing. The widespread adoption of ultra-miniature components like 0201 and 01005 packages has rendered manual inspection physically impossible, while production speeds continue to accelerate beyond human capability. This technological imperative has driven a massive upgrade cycle from 2D to 3D AOI systems, particularly as manufacturers increasingly utilize Ball Grid Array (BGA) and Quad-Flat No-leads (QFN) packages with hidden solder joints. The integration of AI and deep learning algorithms in 2024-2025 represents the key competitive advantage, dramatically reducing false call rates that previously plagued production lines and caused unnecessary rework.

The comprehensive capabilities of modern AOI systems extend throughout the entire production process, making them indispensable for the China inspection equipment market. Dedicated 3D Solder Paste Inspection (SPI) machines have become standard practice before component placement, while post-reflow AOI validates long-term reliability for devices subject to vibration or thermal stress. These systems excel at identifying critical defects including tombstoning, solder bridges, and open circuits, while providing permanent photographic and data records essential for automotive and medical device traceability requirements. The ability to rapidly reprogram for new board layouts enables high-mix, low-volume production models, directly supporting China's shift toward more customized manufacturing.

Key Findings:

- 3D AOI adoption is mandatory for detecting hidden solder joints in BGA/QFN packages, driving massive equipment upgrade cycles across China's electronics sector

- AI-powered false call reduction has become the primary competitive differentiator, with deep learning algorithms distinguishing true defects from cosmetic variations

- First-Pass Yield (FPY) improvement represents the single most important metric for factory managers, with AOI being the most effective tool for achieving it

- Complete traceability documentation through AOI systems is now contractually required for automotive and medical device manufacturing contracts

- Flexible production enablement through rapid reprogramming capabilities makes AOI essential for China's growing high-mix, low-volume production demands

By Deployment

In-line inspection equipment with over 70.26% market share has emerged as the architectural backbone of smart factories throughout the China inspection equipment market, fundamentally transforming quality control from reactive detection to proactive prevention. The ability to create closed-loop systems where defects trigger immediate upstream adjustments has revolutionized production efficiency—an in-line SPI machine detecting insufficient paste can automatically signal the printer to adjust squeegee pressure or halt production, preventing hundreds of faulty boards. This real-time feedback mechanism, combined with the elimination of production bottlenecks through continuous flow inspection at production line speeds, has made in-line systems indispensable for achieving zero-defect manufacturing goals.

The strategic deployment pattern in Surface-Mount Technology (SMT) lines demonstrates why in-line systems dominate the China inspection equipment market. Critical inspection points include post-solder paste printing (SPI), post-component placement (pre-reflow AOI), and post-reflow soldering (post-reflow AOI), with Tier 1 automotive suppliers and 5G base station manufacturers driving adoption through zero-tolerance field failure policies. The economic advantages are compelling—catching defects before the costly reflow oven process significantly reduces scrap and rework costs, while Statistical Process Control (SPC) integration enables real-time trend monitoring and predictive adjustments. Support for double-sided PCB inspection through automated flipping and re-inspection demonstrates clear logistical superiority over offline methods.

Key Findings:

- 100% in-line inspection has become a contractual requirement for automotive ADAS, infotainment, and 5G base station equipment manufacturing

- Real-time SPC integration allows process engineers to detect gradual shifts and make corrections before defects occur

- Immediate root cause analysis through exact defect location identification accelerates problem resolution and reduces downtime

- Reduced contamination risk through minimal human handling prevents ESD damage and physical shock to sensitive components

- Robotic sorting integration enables automatic defective board removal without human intervention, supporting lights-out factory operations

By Application

Electronics and PCB inspection with over 20.57% market share represents the highest concentration of quality control investment in the China inspection equipment market due to the exponential cost impact of undetected defects. A single microscopic flaw—whether a hairline crack in a solder joint or an internal short circuit—can render complex devices like smartphones or automotive ECUs completely inoperable, making comprehensive inspection economically imperative. The extreme component density in modern PCBs, particularly those featuring high-density interconnects (HDIs) for 5G devices and smartwatches, creates microscopic spacing between traces highly susceptible to solder bridging and shorts detectable only through advanced inspection systems. This technical reality drives heavy deployment across China's electronics manufacturing base.

The global supply chain's dependence on China-produced PCBs intensifies quality validation requirements throughout the China inspection equipment market. Companies worldwide rely on inspection data from Automated X-ray Inspection (AXI) systems to validate the internal structure and quality of sourced boards. The automotive industry's electrification push has created exceptional demand for automotive-grade PCBs capable of withstanding years of vibration, temperature extremes, and humidity—requiring inspection rigor far exceeding consumer electronics standards. Specialized challenges like flexible and rigid-flex PCB inspection for wearables demand dedicated systems addressing layer alignment, pad integrity, and delamination risks. The cost multiplier effect powerfully justifies investment: defects cost $1 to fix on bare boards, $10 after assembly, $100 in finished products, and potentially $1,000+ per unit in field failures and recalls.

Key Findings:

- PCBs represent single points of failure where microscopic defects can destroy entire high-value devices, making inspection investment critical

- AXI is essential for BGA inspection, providing the only method to analyze hundreds of hidden solder balls for voids, shorts, and defects

- Automotive reliability standards drive rigorous inspection requirements beyond consumer electronics for vibration and environmental resistance

- High-frequency 5G applications demand inspection verification of trace widths and impedance control for signal integrity

- Cost multiplier effect creates powerful ROI: $1 bare board fixes versus $1,000+ field failure costs justify heavy front-end inspection investment

By Automation Level

The explosive growth of automatic inspection equipment in the China inspection equipment market directly addresses the acute shortage of skilled inspection labor while delivering consistency impossible with human operators. It currently controls more than 59.51% market share. The challenge of recruiting and retaining inspectors capable of spotting microscopic defects for extended periods has made automation a necessity rather than a luxury. Modern automatic systems inspect the first unit and the millionth unit with identical criteria, eliminating the performance variations caused by fatigue, subjectivity, and human error that previously compromised quality control. This transformation extends beyond simple mechanization to sophisticated systems integrating robotic handling, where arms load PCBs into in-circuit testers or X-ray machines and sort them based on results, creating true lights-out inspection cells.

The data generation and operational capabilities of automatic inspection systems provide compelling advantages throughout the China inspection equipment market. Automatic Coordinate Measuring Machines (CMM) and 3D laser scanners execute complex measurement routines on high-value components like engine blocks or turbine blades with precision impossible to achieve manually. Every measurement is logged digitally, creating comprehensive databases for compliance auditing and long-term process improvement analysis. In hazardous environments like battery manufacturing, automatic visual inspection systems monitor for leaks or swelling where human presence would be unsafe. The emergence of collaborative robots (cobots) working alongside humans represents a hybrid approach, while accumulated inspection data feeds AI models for predictive maintenance—a cornerstone of Industry 4.0 implementation.

Key Findings:

- Skilled labor gap solution addresses the impossibility of finding sufficient human inspectors for microscopic defect detection at scale

- 100% consistency achievement ensures identical inspection criteria from first to last unit, eliminating human variability

- Higher throughput rates through elimination of manual handling time directly increases units inspected per hour

- Complete data integrity through automatic logging eliminates transcription errors while creating compliance audit trails

- Predictive maintenance enablement through AI analysis of inspection data forecasts equipment failures before they occur

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Key Players in China Inspection Equipment Market

- Kuntai Group

- ENF Ltd.

- Taymer International

- DGM

- Luster Inc.

- Neoden

- Jiangsu Yingyou Textile Machinery Co.,Ltd

- Shenzhen Jakange Technology Co., Ltd.

- Weigang Machinery

- Zhejiang Hongsheng Machinery Co., Ltd.

- Ngai Shing Development Limited

- Other Prominent Players

Market Segmentation Overview

By Product Type

- Vision Inspection Systems

- 2D Vision Systems

- 3D Vision Systems

- X-Ray Inspection Equipment

- Ultrasonic Inspection Equipment

- Magnetic Particle Inspection Equipment

- Eddy Current Inspection Equipment

- Radiographic Testing Equipment

- Laser Scanning Equipment

- Automated Optical Inspection (AOI) Systems

By Deployment

- In-line

- Offline

By Automation Level

- Manual

- Semi-Automatic

- Automatic

By Portability

- Benchtop

- Portable/Handheld

By Application

- Printing Inspection Equipment

- Label Inspection

- Barcode and QR Code Verification

- Color Accuracy and Registration Checks

- Packaging Quality Inspection

- Fabric Inspection Equipment

- Textile Surface Defect Detection

- Color Consistency

- Weaving/Knotting Errors

- Pattern/Design Alignment

- Semiconductor Inspection

- Pharmaceutical and Medical Device Inspection

- Automotive Component Inspection

- Food and Beverage Packaging Inspection

- Electronics and PCB Inspection

- Aerospace Material Inspection

- Others

By End Use Industry

- Textile & Apparel

- Printing & Packaging

- Automotive

- Electronics & Semiconductors

- Pharmaceuticals

- Food & Beverages

- Aerospace & Defense

- Chemicals

- Others

By Distribution Channel

- Direct Sales (OEMs & System Integrators)

- Distributors & Resellers

- Aftermarket & Service Providers

- Online Retail

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |