Composite Reverse Osmosis Membrane Market: Type (Thin Film Composite Membrane and Cellulose Acetate Membrane); Product Form (Standard Membranes and Customizable Membranes); Flow Configuration (Spiral Wound Membranes, Hollow Fiber Membranes, Flat Sheet Membranes); Application (Desalination, Water & Wastewater Treatment, Food & Beverage Processing, Pharmaceutical, Residential, Others); End Users (Municipal, Industrial, Commercial, Residential, Others); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 28-Aug-2025 | | Report ID: AA08251476

Market Scenario

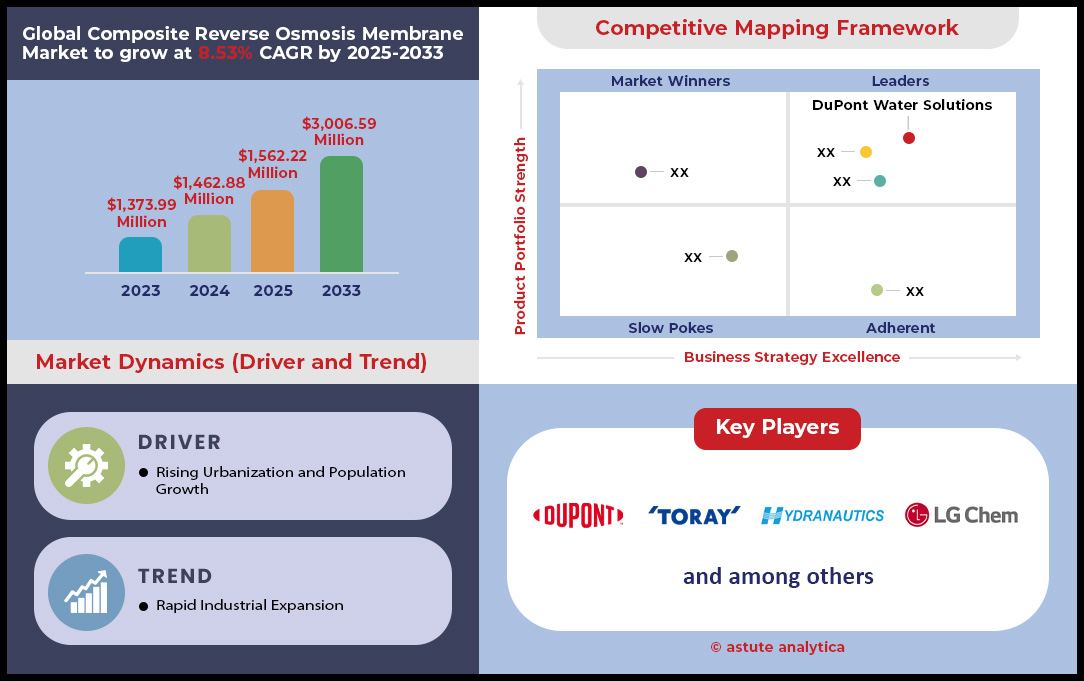

Composite reverse osmosis membrane market was valued at US$ 1,462.88 million in 2024 and is projected to hit the market valuation of US$ 3,006.59 million by 2033 at a CAGR of 8.53% during the forecast period 2025–2033.

Key Findings in Global Composite Reverse Osmosis Membrane Market

- Based on type, thin film composite membrane is projected to continue dominating the composite reverse osmosis membrane market by capturing more than 92.20% market share.

- Based on product form, Standard Membranes accounts the largest 76.31% market share.

Based on flow configuration, spiral would membrane holds the highest 84.72% market share. - When it comes to application, more than 36.02% of the composite reverse osmosis membrane is sold and consumed for desalination application.

- Asia pacific is the largest market by capturing over 38% market share

- Composite reverse osmosis membrane market is poised to reach US$ 3 billion by 2033.

Recent analysis of the composite reverse osmosis membrane market reveals that demand is solidifying around large-scale industrial and municipal projects. The push for water reuse is a significant driver, with new industrial projects in the Asia-Pacific region alone adding a combined treatment capacity of 1,500,000 cubic meters per day in 2024. High-tech sectors are contributing heavily; a single semiconductor plant in Arizona scheduled for 2025 completion will require 35,000 individual membrane elements. Desalination mega-projects remain foundational, evidenced by the Shoaiba 5 plant's use of over 80,000 membranes and the Taweelah plant processing 909,200 cubic meters of seawater daily. Future municipal tenders in 2025 signal a continued demand for 250,000 membrane elements, with new installations targeting an energy consumption benchmark at or below 3.0 kilowatt-hours per cubic meter.

The intense demand across the composite reverse osmosis membrane market is directly fueling aggressive production scaling and highlighting key regional hotspots. Top manufacturers are responding swiftly; DuPont increased its global production capacity by 1,000,000 membrane elements annually in early 2024, while Toray is investing 20 billion yen in a new facility. The market's urgency is reflected in the 120-day average lead time for bulk orders of standard membranes. Geographically, the MENA region is a focal point, installing approximately 400,000 new seawater RO membranes in 2024. Similarly, California's water projects slated for 2025 will require an estimated 60,000 new membrane elements, confirming North America as a critical market.

Beyond these core areas, demand is diversifying into high-value, specialized applications, creating new revenue streams for the composite reverse osmosis membrane market. Emerging industries are creating significant needs; the lithium extraction sector is projected to require 25,000 specialized RO elements by the end of 2025. The pharmaceutical industry also represents a key growth vector, with a forecasted 2025 need for 50,000 small-diameter, sanitary-grade elements for high-purity water systems. Technological pull is also shaping demand, as new membranes capable of tolerating 1,000 ppm-hours of chlorine exposure and offering a 7-year operational lifespan attract customers seeking greater durability and performance.

To Get more Insights, Request A Free Sample

Advanced Materials and Molecular Science Forge New Competitive Market Advantages

Tremendous opportunities await innovators within the composite reverse osmosis membrane market, extending beyond current demand drivers. Two powerful trends are shaping the next generation of products, offering pathways to premium positioning and significant operational savings for end-users. These developments are centered on fundamentally new approaches to membrane construction and surface chemistry.

- A primary opportunity lies in the commercialization of biomimetic membranes. Aquaporin-based platforms, which mimic biological channels for highly efficient water transport, are moving from research to reality. These membranes offer unparalleled permeability and selectivity. Companies mastering their production can command premium prices in high-purity applications, such as semiconductor manufacturing and pharmaceuticals, where superior water quality and lower energy use provide a compelling value proposition.

- A second major trend is the application of zwitterionic polymer coatings. By grafting these polymers onto a membrane's surface, a super-hydrophilic layer is created, offering extreme resistance to biofouling. The opportunity for membrane manufacturers is enormous. Offering a product that dramatically extends operational cycles and reduces the frequency of chemical cleaning provides a distinct competitive edge, especially in fouling-prone sectors like industrial wastewater treatment and food processing.

Green Energy and Critical Minerals Sector Propels Specialized Membrane Innovation

A powerful demand shift is occurring within the composite reverse osmosis membrane market, driven by the global transition to green energy and sustainable resource extraction. New high-tech industries require vast quantities of ultrapure water and specialized brine concentration capabilities, creating a significant new customer base. For instance, a new green hydrogen hub planned for Texas in 2025 will require a water treatment capacity of 50,000 cubic meters per day. Similarly, the burgeoning Direct Lithium Extraction (DLE) sector saw pilot plants in Nevada procure 15,000 specialized membrane elements in 2024 to process mineral-rich brines. To meet these needs, venture capital investment in RO technologies for battery material refining reached US$ 80 million in 2024.

The emerging demand in the composite reverse osmosis membrane market is characterized by stringent technical requirements. A major electric vehicle gigafactory opening in 2025 will feature an onsite water recycling plant utilizing 8,000 RO elements designed to produce water with a final resistivity of 18 megaohm-cm. The process is critical, as an estimated 9 tons of ultrapure water are required to produce just one ton of green hydrogen. New 2025 tenders for DLE projects now specify a boron rejection of 99.8% for membranes. Furthermore, new carbon capture facilities planned for 2025 are sourcing RO systems capable of handling influent with a total dissolved solids count of 5,000. This trend also extends to recycling, with new battery recycling facilities projected to require 500 new small-scale RO skids globally in 2025.

Demand for Operational Efficiency Drives Adoption of Advanced Low-Fouling Membranes

A second defining aspect of demand is the intense focus on reducing operational expenditure (OPEX) through the adoption of advanced low-fouling and high-durability membranes. End-users are increasingly prioritizing long-term performance and reduced maintenance over initial capital cost. In response, LG Chem’s new 2024 fouling-resistant (FR) line promises a 500-hour extended run time between cleaning cycles. This directly addresses a major pain point, as the annual cost of cleaning chemicals for a standard industrial RO system is estimated at US$ 30,000. A major dairy processor in Wisconsin is acting on this value proposition by retrofitting its plant with 3,000 new FR elements in 2024.

The specifications for these next-generation products reflect the market's demand for resilience. The acceptable pressure increase before a cleaning cycle is initiated for new FR membranes is now set at a higher tolerance of 20 psi. New membranes designed for municipal wastewater reuse can now handle a chemical oxygen demand (COD) of up to 75 mg/L. Reflecting this durability, a leading supplier extended the warranty period for its top-tier low-fouling membranes to 5 years in 2024. This innovation is backed by significant funding, with R&D in zwitterionic anti-fouling coatings attracting US$ 40 million in venture capital in 2024. Ultimately, the goal is uninterrupted operation; new textile industry plants in India are specifying RO systems that can run for 3,000 continuous hours, a key driver for the composite reverse osmosis membrane market.

Segmental Analysis

Superior Performance Drives Thin Film Composite Membrane Dominance

The remarkable dominance of thin film composite membranes, which capture over 92.20% of the market, is a direct result of their unparalleled separation efficiency and operational robustness. This technology's key advantage lies in its unique layered construction, which features an ultra-thin polyamide active layer responsible for salt rejection, supported by a more porous and durable substrate. This design enables independent optimization of permeability and strength, allowing these membranes to deliver exceptionally high water quality (with rejection rates often over 99%) while maintaining high flow rates. Their superior chemical and mechanical stability makes them the standard for the vast composite reverse osmosis membrane market, capable of handling diverse and challenging water sources where older technologies would fail. Continuous innovation, such as the development of nanocomposites that boost permeability, further cements their leading position.

The commercial success of thin film composite membranes is also built on their versatility and reliability across a wide array of applications, from large-scale desalination to high-purity industrial water production. With an active layer less than 200 nanometers thick and average pore sizes of just 1 nanometer, these membranes provide a formidable barrier against dissolved salts, organic compounds, and microorganisms. The consistent research and development in this area, evidenced by hundreds of annual publications, ensures a steady stream of enhancements in performance, fouling resistance, and lifespan. As global demands for purified water intensify, the fundamental advantages of this technology ensure it will continue to be the cornerstone of modern separation processes in the composite reverse osmosis membrane market.

- New thin-film nanocomposite (TFN) variants can double water permeability without compromising salt rejection by embedding nanoparticles like zeolites.

- The technology is now so advanced that freshwater recovery from challenging sources can surpass 60%, enhancing water-use efficiency.

- Ongoing material science research is focused on improving TFC resistance to chlorine and other oxidants, which is a key operational challenge.

Standard Form Membranes A Testament To Efficiency And Economy

Standard membranes command the largest product form share at 76.31% due to the powerful market benefits of standardization: interoperability and cost-effectiveness. This widespread adoption is driven by the fact that standardized elements can be easily interchanged between systems, regardless of the original manufacturer. Such uniformity simplifies procurement, inventory management, and maintenance for plant operators, significantly reducing operational complexity and downtime. This has fostered a highly competitive and stable supply chain, where economies of scale in manufacturing lead to lower costs for end-users. The reliability and proven performance of standard elements make them the go-to choice for the composite reverse osmosis membrane market, ensuring predictable results and operational ease for the vast majority of water treatment facilities worldwide.

The dominance of the standard form is not just about convenience; it is a foundation for process optimization and scalability. The modular design of these membranes allows for straightforward system scaling, enabling treatment plants to expand their capacity with minimal engineering adjustments. This inherent flexibility is invaluable for municipalities and industries facing growing water demands. Furthermore, the massive installed base of systems built around standard dimensions encourages continuous innovation within this format, such as the development of more efficient feed spacers and anti-fouling coatings. The result is a self-reinforcing cycle where widespread use drives both cost reduction and incremental technological improvement, securing the standard membrane's position as the industry benchmark in the composite reverse osmosis membrane market.

- The modular nature of standard elements allows for precise and easy scalability of water treatment capacity to meet growing demand.

- Automated manufacturing processes, made possible by standardized dimensions, significantly increase production yield and product consistency.

- The global supply chain for standard membranes is highly mature, ensuring parts are readily available for routine replacement and emergency repairs.

Spiral Wound Design The Industry Standard For Maximizing Output

Holding an impressive 84.72% of the market, the spiral wound configuration is the undisputed leader due to its exceptionally efficient design that maximizes filtration surface area within a compact, cost-effective module. The genius of the spiral wound element lies in its ability to pack a vast amount of membrane into a small cylindrical space, a feature known as high packing density. This allows for the construction of smaller, more space-efficient water treatment systems that can produce large volumes of purified water, making it the ideal choice for large-scale applications like municipal water treatment and desalination. This design is also inherently robust, built to withstand the high pressures of reverse osmosis while its internal feed spacers create turbulent flow, which helps mitigate membrane fouling and extend operational life.

The economic advantages of the spiral wound design are as significant as its technical merits. The configuration lends itself to highly automated and efficient manufacturing processes, which lowers production costs and makes the technology accessible for a broad range of applications. Its modular nature simplifies system design, maintenance, and expansion, offering flexibility that is highly valued by plant operators. The combination of high performance, durability, fouling resistance, and manufacturing efficiency has made the spiral wound element the core component of the global composite reverse osmosis membrane market. Its proven reliability and versatility across different filtration types, from reverse osmosis to ultrafiltration, ensure its continued dominance for the foreseeable future.

- The design's turbulent crossflow provides a continuous scouring action that dislodges potential foulants, reducing the need for chemical cleaning.

- Its leak-free, robust construction allows it to operate reliably under extreme conditions, including high pressures, temperatures, and pH levels.

- The spiral configuration is the most economical way to package membranes, a key reason for its widespread adoption since the 1970s.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Desalination An Essential Application Driving Membrane Demand

The desalination sector's position as the largest application, consuming over 36.02% of membranes in the composite reverse osmosis membrane market, is driven by the critical and growing global need for fresh water. Facing unprecedented water stress from population growth and climate change, coastal nations are increasingly reliant on the ocean as a stable source of potable water. Reverse osmosis technology is the dominant desalination method because it is significantly more energy-efficient and cost-effective than older thermal-based processes. This efficiency has made large-scale seawater conversion economically feasible, transforming it from a niche solution to a mainstream component of national water security strategies in many parts of the world. The continuous innovation in the is central to this trend.

Ongoing advancements in membrane technology have been a primary catalyst for the growth of RO desalination. Modern composite membranes feature higher salt rejection and greater water flux, allowing plants to produce more fresh water with less energy. Innovations such as advanced anti-fouling coatings and energy recovery devices have drastically cut operational costs and improved system reliability, further accelerating adoption. With global freshwater resources becoming ever more precarious, the demand for desalination is set to rise. This ensures that it will remain the largest and most critical application in the composite reverse osmosis membrane market for high-performance reverse osmosis membranes, directly linking water security to advancements in membrane science.

- Modern RO desalination plants can reduce seawater salt content from 36,000 mg/L down to drinking water standards of about 200 mg/L.

- The energy required for RO desalination has been reduced to as low as 1.8 kWh per cubic meter of water produced.

- Maintenance costs for RO systems are significantly lower than thermal alternatives, representing only 10-15% of total operational expenses.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific Industrial and Urban Growth Drives Dominant Market Demand

The Asia Pacific region, commanding a formidable 38.39% of the composite reverse osmosis membrane market, is defined by massive industrial undertakings and urgent municipal water projects. China's ambitious 14th Five-Year Plan targets a national desalination capacity of 3.5 million cubic meters per day by 2025. Specific projects underscore this scale, such as the new Shandong Yantai Penglai plant, which will provide 108 million tons of freshwater annually upon completion. India is also making significant strides; the newly inaugurated Nemmeli Water Desalination Plant in Tamil Nadu adds a capacity of 150 million liters per day as of February 2024, addressing critical water shortages. Industrial demand is equally robust. In South Korea, Samsung's Hwaseong semiconductor plant plans to treat and reuse 400 million liters of wastewater per day, converting it into ultrapure water for chip manufacturing.

The sheer scale of investment and development solidifies the region's top position in the global composite reverse osmosis membrane market. India, under its National Mission for Clean Ganga, has already completed 222 sewage treatment projects as of July 2024. The government also allocated 2 billion rupees for the Chandrawal Water Treatment Plant in its 2024-25 budget. In China, the government is backing a state fund to raise approximately 40 billion USD for its semiconductor sector, directly boosting demand for related ultrapure water systems. To meet industrial needs in Penglai Industrial Park, a new plant is being built for Wanhua Chemical, which will be the largest industrial membrane-based seawater desalination facility in the country. Further signaling growth, a new technical center and RO membrane production facility is set to begin operations in Saudi Arabia in 2026. The NMDC steel plant in Nagarnar, India, commissioned a 4,320 cubic meters per day Zero Liquid Discharge plant in 2024.

European Regulatory Rigor and Sustainability Investments Reshape Membrane Demand

Europe’s composite reverse osmosis membrane market is increasingly shaped by stringent environmental regulations and targeted investments in water resilience and green technology. The EU's Water Reuse Regulation, which came into full effect in 2024, is a primary driver, aiming to increase the annual use of reclaimed water to 6.6 billion cubic meters. In response to severe droughts, Spain is investing heavily, with a €467 million fund allocated in February 2024 for two new desalination plants near Barcelona. The country already produces around 5,000,000 cubic meters of desalinated water daily. Further projects include a new floating desalination plant for Barcelona with a capacity of 40,000 cubic meters per day. In Italy, major infrastructure upgrades are underway; a project in Vicenza, the largest of its kind in a decade, will serve approximately 300,000 people.

Additionally, a €30 million loan from the European Investment Bank will support Pescara's water and wastewater investment program for 2024-2026. The green energy sector is also a key demand driver; the United Kingdom's push for green hydrogen requires significant water resources, with new studies in 2024 mapping the specific water demands for electrolysis.

North America's High-Tech and Water Reuse Projects Drive Sophisticated Demand

In North America, demand for the composite reverse osmosis membrane market is characterized by high-tech industrial needs and large-scale water management in resource-intensive sectors. The oil and gas industry in Texas is a major consumer; the Permian Basin alone generates approximately 24 million barrels of produced water daily as of 2025, creating a huge market for treatment and reuse. Companies are actively seeking permits for discharge, with one application from NGL Water Solutions seeking to discharge up to 16.9 million gallons per day of treated water into the Pecos River.

The U.S. CHIPS Act is also a significant factor, expected to drive a capacity increase for ultrapure water systems of up to 50% over the next five years to support new semiconductor fabs. Water reuse for agriculture is another critical area for the composite reverse osmosis membrane market; California’s Central Valley is seeing new projects in 2024 designed to treat agricultural runoff, with initial systems targeting a capacity of 5,000 acre-feet per year. Municipal water reuse is also expanding, with Florida planning 15 new water recycling projects to be commissioned by the end of 2025. Canada’s mining sector plans to install 50 new containerized RO systems in 2025 for remote site water treatment.

Top 10 Investments and Acquisitions Shape Tomorrows Competitive Composite Reverse Osmosis Membrane Market

- Gradiant Secures Major Funding to Expand Water Technology Solutions (2024): Gradiant, a leader in advanced water and wastewater treatment, raised significant new funding to accelerate its growth, impacting the deployment of advanced membrane technologies globally.

- Suez Finalizes Acquisition of Veolia's UK Waste Business (2024): Suez completed its acquisition of Veolia's former UK waste business, a move that strengthens its portfolio and creates synergies for water and waste management solutions, including membrane-based treatments.

- Toray Announces Major Investment in New RO Membrane Production Facility (2024): Toray Industries revealed plans for a substantial investment to construct a new production facility for reverse osmosis membranes, aiming to meet surging global demand in the composite reverse osmosis membrane market.

- Xylem Acquires Idrica to Enhance Smart Water Management Capabilities (2024): Global water technology leader Xylem acquired Idrica, a smart water management specialist, to bolster its digital offerings, which are crucial for optimizing RO system performance.

- Grundfos Acquires Metasphere to Boost Smart Water Network Solutions (2024): Grundfos acquired Metasphere, enhancing its capabilities in telemetry and data analytics for water networks, a critical component for managing large-scale RO installations efficiently.

- DuPont Invests in New Biopharma Tubing Manufacturing Line (2024): DuPont invested in a new manufacturing line for biopharmaceutical tubing, a strategic move that complements its high-purity water solutions, including sanitary RO membranes used in pharma.

- Kurita Water Industries Acquires US-Based Water Treatment Company (2024): Kurita acquired a US water treatment chemicals and services company, expanding its footprint in North America and strengthening its ability to service industrial clients using RO systems.

- Membrion Raises Funding for Ceramic Desalination Membranes (2024): Membrion, a startup developing innovative ceramic membranes for harsh water environments, secured new funding to scale its technology, representing a potential future competitor or partner in the desalination space.

- KKR Invests in Indian Environmental Services Company SMS Envocare (2024): Global investment firm KKR invested in SMS Envocare, an Indian environmental services provider, signaling strong investor confidence in India's water and waste management sectors, key markets for RO membranes.

- Aliaxis Acquires Klenk to Strengthen Position in Water Management (2024): Aliaxis, a leader in fluid management solutions, acquired Klenk, a German specialist, to expand its portfolio and enhance its offerings for integrated water systems that often incorporate RO technology.

Top Companies in the Composite Reverse Osmosis Membrane Market

- DuPont

- Hydranautics

- Toray Industries

- LG Chem

- SUEZ Water Technologies & Solution

- Dow Water & Process Solutions

- Veolia

- Pentair

- Membrana (A division of Celgard)

- Aquatech International

- 3M Purification

- Axium Process

- Beijing OriginWater Membrane Technology Co., Ltd.

- Vontron Membrane Technology Co. Ltd.

- Bluewater

- Hunan KeenSen Technology Co., Ltd.

- Freudenberg SE

- Wenzhou Aowei Machinery Co., Ltd

- Parker Hannifin Corporation

- Membrane Solutions

- Wave Cyber (Shanghai) Co., Ltd.

- Wanhua Chemical Group Co., Ltd.

- AROMEM PTE. LTD. (SURO)

- Nitto Denko Corporation

- Culligan Water

- MANN+HUMMEL

- Other Prominent Players

Market Segmentation Overview

By Type

- Thin Film Composite Membrane

- Cellulose Acetate Membrane

By Product Form

- Standard Membranes

- Customizable Membranes

By Flow Configuration

- Spiral Wound Membranes

- Hollow Fiber Membranes

- Flat Sheet Membranes

By Application

- Desalination

- Water & Wastewater Treatment

- Food & Beverage Processing

- Pharmaceutical

- Residential

- Others

By End User

- Municipal

- Industrial

- Commercial

- Residential

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

FREQUENTLY ASKED QUESTIONS

The global market was valued at US$ 1,462.88 million in 2024 and is projected to reach US$ 3,006.59 million by 2033, growing at a CAGR of 8.53%.

Thin film composite membranes lead with over 92.20% share, driven by superior salt rejection, durability, and wide adoption in desalination and industrial water treatment.

Standard membranes account for 76.31% of the market, preferred for their cost efficiency, reliability, and compatibility across treatment systems.

Desalination accounts for more than 36.02% share, as coastal regions increasingly rely on RO technology to meet fresh water needs.

Asia Pacific holds over 38% share, supported by rapid urbanization, mega-desalination projects, and growing industrial water reuse initiatives.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |