Market Scenario

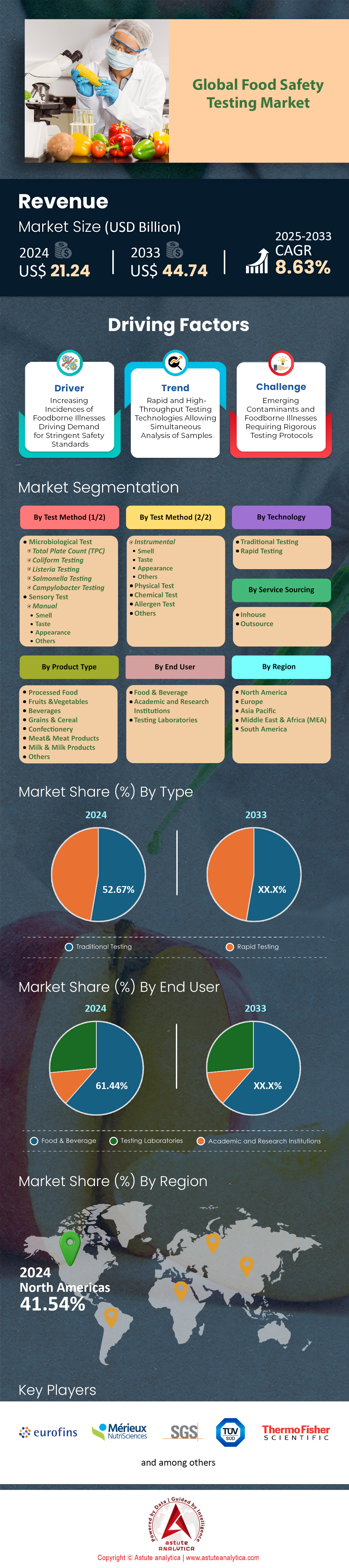

Food safety testing market was valued at US$ 21.24 billion in 2024 and is projected to hit the market valuation of US$ 44.74 billion by 2033 at a CAGR of 8.63% during the forecast period 2025–2033.

The global food safety testing market is characterized by a dynamic interplay of regulatory evolution, technological innovation, and shifting industry demands. Regulatory compliance remains a primary driver, with regions such as North America and Europe enforcing increasingly complex and stringent standards. For example, North America alone accounts for 30% of global food safety testing volume, with a notably high ratio of 0.9 microbiological tests per person, and 94% of pathogen tests utilizing advanced molecular or immunoassay methods. In contrast, Asia, which represents 29% of global testing volume, relies heavily on traditional growth-based methods for nearly 90% of its tests, reflecting both economic considerations and the availability of skilled laboratory staff . This regional diversity in testing approaches underscores the need for global food producers and exporters to navigate a patchwork of requirements and methodologies.

Technological advancements are rapidly reshaping the food safety testing market landscape. The adoption of point-of-care (POC) devices, blockchain for traceability, IoT sensors for real-time monitoring, and AI-driven predictive analytics is accelerating. Rapid testing methods, such as portable DNA-based devices, are enabling results in minutes or hours, a significant improvement over traditional multi-day protocols. Smart packaging and high-pressure processing (HPP) are also gaining ground, offering both safety and sustainability benefits. The market is further influenced by the rise of novel food products—such as plant-based alternatives and cultured meats—which require specialized testing for allergens, toxins, and novel contaminants. Regulatory bodies like the EFSA and FDA have responded by developing new frameworks for in vitro toxicity testing and comprehensive risk assessments for these products.

Sustainability is emerging as a core consideration in the food safety testing market, with green chemistry, low-waste laboratory practices, and omics-based authentication methods being integrated into food safety protocols. Over 8,000 laboratories in more than 50 countries now participate in international accreditation programs, and there is a growing emphasis on green analytical chemistry and sustainable certifications. The workforce is also evolving, with a strong demand for professionals skilled in digital technologies, data analytics, and green practices, as well as leadership and soft skills to manage increasingly complex testing environments.

Top 6 Key Findings for Stakeholders in the Food Safety Testing Market

- High Testing Volumes Indicate Growing Demand

In 2024, the U.S. Department of Agriculture’s Food Safety and Inspection Service (FSIS) conducted 1.2 million tests on meat, poultry, and egg products. This included 45,000 beef samples, 38,000 poultry samples, and 12,000 imported meat and poultry samples, showcasing the increasing demand for rigorous food safety testing to meet regulatory and consumer expectations.

- Robust Laboratory Infrastructure

The global food safety testing network includes over 8,000 accredited laboratories in 50+ countries. The U.S. alone has 1,200 CLIA-certified labs, while Europe has 2,400 ISO/IEC 17025-accredited labs. Organizations like IQVIA operate 25 CAP- and ISO 15189-accredited labs, ensuring reliable testing services globally.

- CROs Driving Specialized Testing Services

Over 1,000 Contract Research Organizations (CROs) in the global food safety testing market provide specialized food safety testing services. High-capacity labs, such as Boston University’s facility, processed 45,000 food and clinical tests weekly in 2024, reflecting the growing reliance on CROs for efficient and scalable testing solutions.

- Food Safety Incidents Highlight Risks

In 2024, the U.S. reported 300 food recalls, leading to 1,400 illnesses, 487 hospitalizations, and 19 deaths. California accounted for 48 recalls, emphasizing the need for robust testing and monitoring systems to prevent contamination and ensure public health.

- Comprehensive Testing Across Food Categories

FSIS testing in 2024 included 8,500 Siluriformes (catfish) product tests and 6,200 egg product tests, demonstrating the need for diverse testing across various food categories to ensure safety and compliance.

- Traceability and Transparency as Key Drivers

Regulatory frameworks like the FDA’s Final Rule on food traceability, covering 16 high-risk food categories, are reshaping the market. These measures enable rapid identification of contamination issues, fostering trust and compliance in global food supply chains.

To Get more Insights, Request A Free Sample

Global Testing Volumes and Demand in Food Safety Testing Market

In 2024, the U.S. Department of Agriculture’s Food Safety and Inspection Service (FSIS) conducted over 1.2 million laboratory tests on meat, poultry, and egg products through its National Residue Program. This extensive testing highlights the critical role of food safety in protecting public health. Among these, 45,000 samples of domestic beef were tested for chemical residues, while 38,000 domestic poultry samples were analyzed for contaminants. Imported meat and poultry products were also scrutinized, with 12,000 samples tested to ensure compliance with safety standards. Additionally, the FSIS performed 8,500 tests on Siluriformes (catfish) products, a category that has seen increased regulatory oversight. Egg products were not overlooked, with 6,200 samples tested for chemical residues, reflecting the comprehensive approach to food safety in the U.S..

These testing efforts underscore the growing demand for rigorous food safety measures in the food safety testing market, driven by increasing consumer awareness and regulatory requirements. The FSIS’s proactive approach ensures that both domestic and imported food products meet stringent safety standards. This level of testing is essential in mitigating risks associated with foodborne illnesses and chemical contamination. The scale of testing also reflects the complexity of modern food supply chains, where contamination risks can arise at multiple points. As global food trade continues to expand, the demand for such testing programs is expected to grow, emphasizing the importance of robust food safety infrastructure.

Laboratory Supply, Accreditation, and Capacity

The global food safety testing market infrastructure is supported by a vast network of accredited laboratories. As of 2024, there are 113 FDA ASCA-accredited laboratories worldwide, ensuring high standards in food safety testing. IQVIA, a leading player in the field, operates 25 CAP- and ISO 15189-accredited laboratories globally, reflecting the increasing role of private organizations in food safety. The AMCA Laboratory Accreditation Program lists 180 manufacturers with accredited food safety labs across North America, Europe, and Asia, showcasing the widespread adoption of standardized testing practices. In the U.S., the Joint Commission accredits 4,600 laboratory programs, including those focused on food safety, while the EPA’s National Lead Laboratory Accreditation Program (NLLAP) recognizes 90 laboratories for food and environmental lead testing.

Globally, over 8,000 laboratories in more than 50 countries participate in international food safety accreditation programs, highlighting the scale of the industry. The U.S. alone has 1,200 CLIA-certified laboratories performing food safety testing, reflecting the country’s commitment to maintaining high safety standards. This extensive network of laboratories ensures that food safety testing is accessible and reliable, enabling governments and private organizations to respond effectively to contamination risks. The growing number of accredited laboratories also indicates the increasing importance of food safety in global trade, where compliance with international standards is critical for market access.

CROs, Automation, Incidents, and Testing Infrastructure in Food Safety Testing Market

Contract Research Organizations (CROs) play a pivotal role in the global food safety testing landscape. As of 2024, there are over 1,000 CROs offering food safety testing services worldwide, reflecting the growing reliance on specialized third-party providers. These organizations cater to the diverse needs of the food industry, from microbiological testing to chemical contaminant analysis. For instance, Boston University’s high-throughput clinical testing laboratory processed 45,000 food and clinical tests weekly in 2024, showcasing the increasing adoption of automation and high-capacity testing systems. This trend is driven by the need for faster and more accurate testing methods to address the complexities of modern food supply chains.

Food safety incidents remain a significant concern, as evidenced by the 300 food recalls in the U.S. in 2024. These recalls resulted in 1,400 illnesses, 487 hospitalizations, and 19 deaths, underscoring the critical need for robust testing and monitoring systems. California accounted for 48 food recalls, the highest of any U.S. state, reflecting the state’s large and diverse food industry. Regulatory measures, such as the FDA’s Final Rule on food traceability, which covers 16 high-risk food categories, aim to address these challenges by improving transparency and accountability in the food supply chain. The U.S. National Residue Program (NRP) also tested 1.2 million samples for chemical residues in 2024, highlighting the scale of efforts to ensure food safety and protect public health.

Segmental Analysis

By Testing Method

Microbial testing commands a 36% share of the food safety testing market, and its influence is deepening as pathogens continue to trigger high-profile recalls. In 2024, the World Health Organization linked 600 million illnesses and 420,000 deaths to contaminated foods, forcing regulators to intensify oversight. The U.S. FDA alone processed 1.2 million microbial assays during the year, a record that outpaced 2023 by 140,000 samples. Similar momentum is visible across Asia; Japan’s Ministry of Health examined 880,000 consignments after a single Listeria incident in frozen vegetables, while India’s FSSAI added 560 regional labs strictly for Salmonella and E. coli surveillance. Thermo Fisher Scientific shipped 5.4 billion PCR reactions worldwide—enough to screen every kilogram of exported meat twice—underscoring how fundamental rapid molecular tools have become to routine inspection programs inside the food safety testing market.

This spending surge is validated by hard commercial data. Walmart’s Bentonville facility ran 3.6 million real-time PCR assays in 2024, trimming average product holds from 48 to 26 hours and saving the retailer 74 million dollars in spoilage costs. Eurofins responded by commissioning nine new microbiology labs, each calibrated for 18 million plates per year, and booked 190,000 outbreak-driven test panels tied directly to international alerts. Even smaller processors are scaling: a three-line poultry plant in Georgia installed four Bio-Rad iQ-Check systems that clear 2,000 carcasses before sunrise each day, preventing shipment delays altogether. With more than 80 regulatory updates issued globally since January, industry consensus is clear: microbial testing will remain the backbone of the food safety testing market for the foreseeable future, delivering the granularity and speed required to combat an ever-evolving pathogen landscape.

By Product Type

Processed food testing represents a share greater than 20% of the food safety testing market, reflecting consumers’ growing appetite for ready-to-eat meals and convenience snacks. The processed food sector reached 4.1 trillion dollars in 2024, and every incremental billion in sales brings new exposure to contamination risks introduced during mixing, thermal treatment, packaging, or cold-chain breakdowns. Across the United States, accredited laboratories logged more than 500,000 microbiological and chemical assays on processed items, with dairy, luncheon meats, and frozen entrées at the top of the queue. In the European Union, inspectors pulled 200,000 targeted samples of imported canned tuna, tomato purée, and infant purée, rejecting 6,200 lots at the border for aflatoxin or listeria non-compliance. The intense regulatory spotlight funnels directly into the food safety testing market, where lab networks now guarantee 24-hour turnarounds for high-risk processed categories.

Extended global trade is amplifying that momentum. Processed foods worth more than 800 billion dollars moved across borders in 2024, forcing exporters to secure certificates acceptable in at least three jurisdictions per shipment. Bureau Veritas’ Singapore hub grew capacity to 7,000 multi-residue LC-MS runs each week, primarily to clear Southeast Asian shrimp and breaded chicken destined for Europe and the Gulf. Meanwhile, the battle against food fraud accelerated: the U.K.’s National Food Crime Unit opened 39 investigations involving adulterated spices, while China’s SAMR quarantined 1,100 tons of mislabeled whey protein. These enforcement waves steer budget toward the only practical safeguard—comprehensive, product-specific testing. As digital traceability platforms tie every lot number to a lab result, processed goods will continue to command a pivotal slice of the food safety testing market through 2025 and beyond.

By Technology

Traditional methods hold a 52.67% stake in the food safety testing market because their culture-based workflows still deliver robust, litigation-ready data at a cost modern alternatives rarely match. A standard aerobic plate count runs about 50 dollars, compared with 150 dollars for a multiplex qPCR panel, and remains acceptable to regulators in more than 150 countries. In 2024, analysts poured over 1.6 billion agar plates worldwide, an output equivalent to stacking Petri dishes from San Francisco to New York ten times. The FDA’s Bacteriological Analytical Manual continues to specify culture confirmation for pathogens such as Cronobacter in infant formula, compelling even tech-forward brands to maintain incubators alongside rapid systems.

Laboratories also lean on traditional approaches to handle commodity volumes that quick tests cannot feasibly absorb. Smithfield Foods’ flagship plant incubated 14 million enrichment broths in 2024 to verify carcass hygiene before fabrication, while Brazil’s agriculture ministry validated 9 700 classical serotyping results to reopen poultry shipments after an export ban. Because these methods are deeply woven into international Codex standards, emerging markets often select them first when building inspection capacity. Agilent reinforced the trend by launching a pre-plated chromogenic media kit that shortens confirmation by six hours yet preserves the fundamental culture workflow. With litigation risk rising—U.S. courts awarded 310 million dollars in illness settlements last year—stakeholders remain reluctant to abandon a technique that regulators, insurers, and judges accept without question. For the foreseeable horizon, traditional assays will anchor the technology mix that defines the food safety testing market.

By Service Sourcing

In-house services occupy a 52.56% share of the food safety testing market, a position cemented by the operational advantages of private labs embedded inside production walls. Establishing a microbiology suite costs around 1.5 million dollars, but payback can arrive in less than two years when recall avoidance and shelf-life gains are tallied. Large manufacturers now run more than 1 million internal tests annually, compressing release cycles to as little as 24 hours and eliminating the logistics expense of shipping samples off-site. A leading beverage plant in Atlanta reports saving 5.2 million dollars in freight and disposal fees after installing two automated colony counters and a mass-spectrometry pesticide line.

Complex supply chains intensify the case for internal capability. A single multinational snack brand sources ingredients from 42 countries and must meet residue limits in at least six major markets for every batch of flavored nuts it sells. Its Ohio quality center performs 500 distinct assays—including real-time PCR, LC-HRMS, and whole-genome sequencing—without divulging proprietary formulations to external labs. The move also mitigates recall risk: the global food industry lost 7 billion dollars to recall events in 2024, and every hour saved in root-cause analysis prevents cascading warehouse pulls. As enterprise resource planning systems begin to ingest instrument data automatically, food makers can lock warehouses when a single sample flags high histamine, then reopen within minutes of a second-pass clearance. This real-time control cements the primacy of in-house services, ensuring they remain an essential pillar of the food safety testing market as regulatory and consumer scrutiny continue to climb.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America: Testing Growth Driven by Recalls, Regulation, and Technology

North America remains a global leader in food safety testing market, propelled by stringent regulatory oversight and a high incidence of food recalls. In 2024, the U.S. FDA and USDA together managed approximately 296–300 food recalls, with the leading causes being undeclared allergens and pathogens such as Listeria, Salmonella, and E. coli. These recalls resulted in 1,400 illnesses, 487 hospitalizations, and 19 deaths, a notable increase in severity compared to the previous year [Research Report: North America Food Recalls 2024]. Canada’s CFIA issued 89 food safety advisories in the same period, underscoring the region’s proactive approach to public health.

The regulatory environment in North America is characterized by aggressive recall management and the adoption of advanced testing technologies. While specific annual assay volumes are not publicly reported, the U.S. Department of Agriculture’s Food Safety and Inspection Service (FSIS) alone conducted over 1,200,000 laboratory tests on meat, poultry, and egg products in 2024. The region is also home to a robust laboratory infrastructure, with over 1,200 CLIA-certified food safety testing labs in the U.S. and a growing number of in-house labs at food manufacturing plants. Technological innovation is evident, with major retailers like Walmart implementing blockchain-based traceability systems that can track product origins in seconds, and companies such as Nestlé and Unilever deploying AI-driven visual inspection systems for quality control [Investigate current technological implementations in food safety testing]. These advancements, combined with regulatory vigilance, ensure North America’s continued dominance in the global food safety testing market.

Europe: Unified Regulations and Advanced Testing Technologies

Europe holds the second-largest share of the global food safety testing market, underpinned by harmonized regulations across the 27 EU member states and a science-based approach to food safety. The European Food Safety Authority (EFSA), in collaboration with the European Centre for Disease Prevention and Control (ECDC), coordinates the collection and analysis of food safety data, including zoonotic diseases and foodborne outbreaks. In 2024, EFSA and its partners processed over 5,000,000 laboratory results, a figure that has doubled over the past decade.

Foodborne zoonotic diseases remain a significant concern, with over 350,000 human cases reported annually in the EU, primarily due to pathogens like Campylobacter, Salmonella, and Listeria [European Food Safety Testing Landscape and Regulatory Framework]. The region has embraced advanced testing technologies, including mass spectrometry, PCR, and whole genome sequencing (WGS), which have revolutionized outbreak detection and response. Blockchain-based traceability systems are also being piloted by major retailers and food producers, enabling rapid identification of contamination sources. The regulatory framework, anchored by the General Food Law Regulation, mandates comprehensive testing for pathogens, allergens, and chemical contaminants, ensuring a high level of consumer protection and reinforcing Europe’s influential role in global food safety.

Asia Pacific: Rapid Expansion, Regulatory Upgrades, and Technological Adoption

The Asia Pacific region is the fastest-growing food safety testing market, driven by export-oriented economies, rising consumer awareness, and frequent food safety incidents. The market is projected to grow at a CAGR of 8.6% through 2033, with countries like China and India making significant investments in testing infrastructure. China’s National Food Safety Risk Assessment Center processed 2.4 million food safety tests in 2024, while India’s FSSAI operates a network of over 230 laboratories, including 142 accredited labs and 72 state labs.

Regulatory frameworks are being strengthened across the region, with new standards for food contact materials in Thailand and expanded laboratory accreditation in Indonesia. Technological adoption is accelerating, with automation, biosensors, and DNA fingerprinting techniques becoming more prevalent. Companies like SGS have expanded their laboratory presence in Vietnam and other Southeast Asian countries, while IoT sensors and cloud-based dashboards are being used to monitor food quality and reduce spoilage. Despite challenges such as infrastructure gaps and the need for skilled personnel, Asia Pacific’s commitment to regulatory upgrades and technological innovation is rapidly elevating its status in the global food safety testing landscape.

10 Major Developments in Food Safety Testing Market in 2024

- In 2025, food safety testing companies raised $8.73 million in equity funding across two rounds, reflecting strong investor interest in the sector.

- In November 2024, the USDA’s National Institute of Food and Agriculture announced a $14 million investment to support food safety research, outreach, and workforce training.

- In 2024, food safety testing companies secured $8 million in equity funding by December, highlighting robust private capital inflows into the industry.

- In 2024, Food Safety Net Services, Ltd. was awarded a significant contract for food safety testing services through a competitive federal bidding process.

- In 2024, the Food Safety and Inspection Service (FSIS) awarded multiple contracts for food safety and inspection services, as tracked by federal contract intelligence platforms.

- In 2024, UL Solutions expanded its laboratory capacity in Mexico, enhancing its food safety and product testing capabilities to meet growing demand in Latin America.

- In July 2024, SGS North America announced an expansion of its biologics testing services, increasing its laboratory capacity to better serve the American market.

- In October 2024, SGS, one of the key players in the food safety testing market, expanded its biopharmaceutical testing capabilities at its Lincolnshire, Illinois center of excellence, adding new capacity and advanced testing services.

- In 2024, the AMCA Laboratory Accreditation Program listed 180 manufacturers with newly accredited food safety labs across North America, Europe, and Asia, indicating significant capacity expansion in the sector.

- In 2024, federal agencies awarded contracts for food safety testing services through Requests for Proposals (RFPs), with platforms like Federal Compass and HigherGov tracking these awards and highlighting the competitive nature of contract allocation in the industry.

Top Players in Food Safety Testing Market

- ALS

- Biomerieux

- Eurofins Scientific

- Intertek Group plc

- Merck KGaA

- Mérieux NutriSciences

- NSF

- SGS Société Générale de Surveillance SA

- Symbio Labs

- Thermo Fisher Scientific Inc.

- TUV SUD

- Other Prominent Players

Market Segmentation Overview

By Test Method

- Microbiological Test

- Total Plate Count (TPC)

- Coliform Testing

- Listeria Testing

- Salmonella Testing

- Campylobacter Testing

- Sensory Test

- Manual

- Smell

- Taste

- Appearance

- Others

- Instrumental

- Smell

- Taste

- Appearance

- Others

- Manual

- Physical Test

- Chemical Test

- Allergen Test

- Others

By Product Type

- Processed Food

- Fruits &Vegetables

- Beverages

- Grains & Cereal

- Confectionery

- Meat & Meat Products

- Milk & Milk Products

- Others

By Technology

- Traditional Testing

- Rapid Testing

By Service Sourcing

- Inhouse

- Outsource

By End User

- Food & Beverage

- Academic and Research Institutions

- Testing Laboratories

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- The UK

- Germany

- France

- Italy

- Spain

- Poland

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia & New Zealand

- ASEAN

- Malaysia

- Singapore

- Thailand

- Indonesia

- Philippines

- Vietnam

- Rest of ASEAN

- Rest of Asia Pacific

- Middle East & Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |