Market Scenario

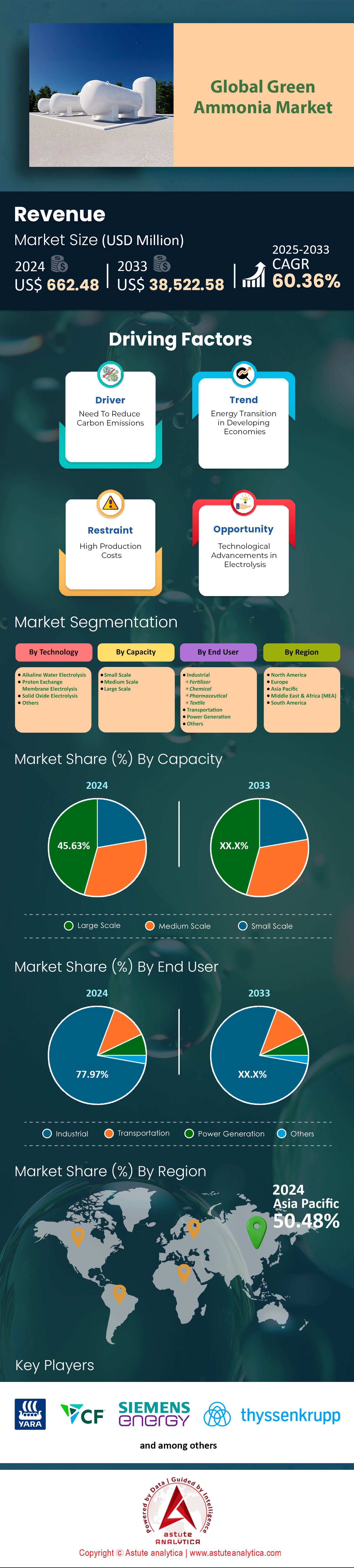

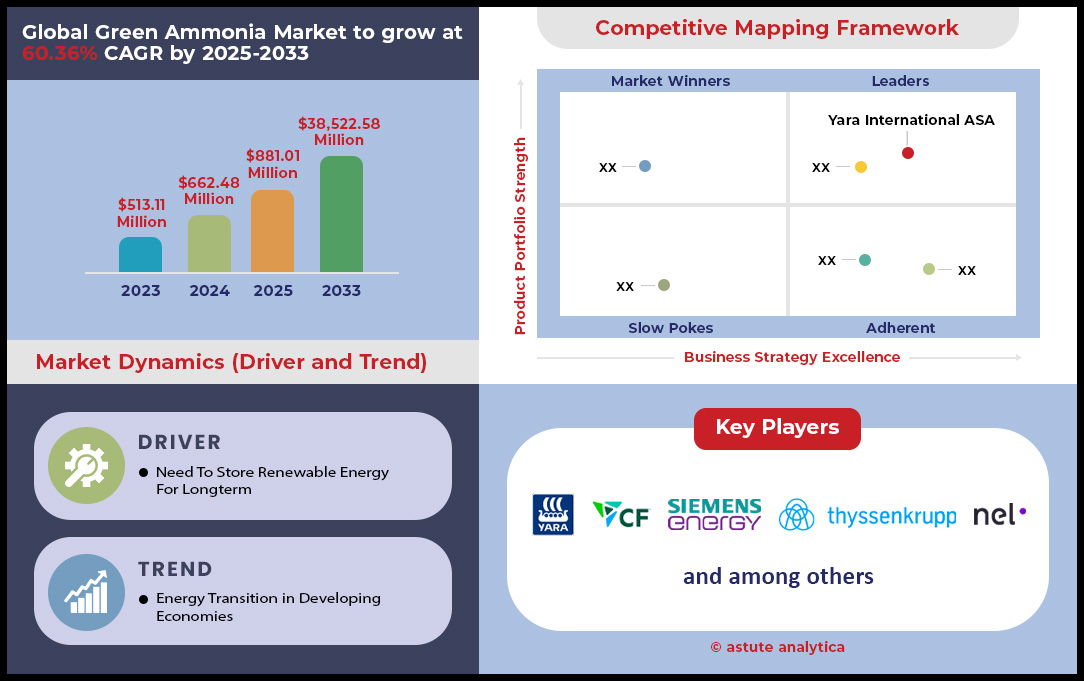

Green ammonia market was valued at US$ 662.48 million in 2024 and is projected to hit the market valuation of US$ 38,522.58 million by 2033 at a CAGR of 60.36% during the forecast period 2025–2033.

Key Findings Shaping the Green Ammonia Market

- Based on technology, alkaline water electrolysis technology with over 63.19% market share and has emerged as the production technology for green ammonia.

- Based on capacity, large scale units are currently dominating the green ammonia market with over 45.63% market share.

- Based on end users, industrial consumers are primary end users of the green ammonia as they accounts for over 77.97% revenue share.

- Asia Pacific is set to remain the key contributor with over 50% revenue to come from the region alone by 2033

- Global green ammonia market is poised to reach US$ 38,522.58 million by 2033.

A tangible shift in the green ammonia market from potential to practice is accelerating as binding offtake agreements and firm commitments from key end-use sectors take hold. Governments are actively creating the market certainty through targeted procurement. A prime example is India, where authorities floated tenders in 2024 for a combined 1,200,000 tons of green ammonia. This was split between a primary tender for 750,000 tons and a surplus capacity tender for an additional 450,000 tons. Such decisive actions provide a clear demand signal to producers, encouraging investment in new capacity by guaranteeing a market for the output.

The scale of commercial agreements is a primary indicator of demand maturation in the global green ammonia market. A landmark term sheet was finalized in January 2024 between ACME Group and IHI Corporation for the supply of 1.2 MMTPA to Japan. Further, a non-binding letter of intent was signed in October 2024 between BASF and AM Green for 100,000 metric tons per year. Yara Clean Ammonia also signed a heads of terms agreement in July 2024 for 150,000 mt/year from a plant in Egypt. Competitive auctions in India during August 2025 resulted in offtake commitments for 85,000 tons by Jakson Green and 50,000 tons by ACME, both for 10-year terms.

Specific end-use projects quantify the emerging demand profile. A floating production plant announced in October 2024 is designed to produce nearly 300,000 tons annually, an output specifically targeted at the maritime sector. In agriculture, Yara's European plant, inaugurated in June 2024, will produce 20,500 tons of ammonia, which will be converted into as much as 80,000 tons of green fertilizer. A smaller, modular system launched in February 2025 can produce 20 tons of ammonia per day for local farm use, showcasing demand at a distributed level.

To Get more Insights, Request A Free Sample

Strategic Opportunities Unfolding in Power Generation and Hydrogen Logistics

- Growing use of green ammonia for co-firing in thermal power plants: Nations like Japan and South Korea are pioneering this application. In early 2025, Japan's JERA began preparations for a large-scale demonstration at a 1 GW coal-fired unit, requiring an initial 500,000 tons of ammonia annually. By 2025, South Korea aims to have 24 coal power units co-firing ammonia. Lotte Chemical is investing 600 billion won ($450 million) into a clean ammonia plant by 2025 to supply this domestic power sector demand, targeting an initial output of 150,000 tons.

- Development of efficient, industrial-scale ammonia cracking technology presents a major opportunity: It is positioning green ammonia as the preferred carrier for transporting hydrogen globally. Several companies are advancing toward commercial readiness. In late 2024, Syzygy Plasmonics secured $78 million in new funding to scale its cracker technology, which can produce hydrogen from ammonia at a single production site. Also in 2024, a consortium including Equinor and BP launched a study for a 200,000-tonne-per-annum low-carbon ammonia cracking facility in the UK. Fortescue announced in early 2025 the successful operation of its first prototype membrane-based ammonia cracker at a facility in Perth.

Maritime Fuel Transition Creates Unprecedented Demand for Bunkering Infrastructure

The maritime industry's decarbonization drive is a primary demand catalyst for the green ammonia market, extending beyond fuel supply to the build-out of new bunkering infrastructure. In 2024, orders for ammonia-capable vessels accelerated, with Clarksons Research noting 25 new vessel orders. Engine manufacturer MAN Energy Solutions confirmed in early 2025 it had secured over 200 orders for its dual-fuel ammonia engines. The Port of Singapore, a key global shipping hub, announced in 2024 its plan to facilitate the first ammonia bunkering pilot by 2025, with an initial handling capacity target of 500,000 tons per year. This project alone carries an initial infrastructure investment of $50 million from a private consortium.

These developments create a tangible demand for both green ammonia volumes and the associated port-side assets. In Northern European green ammonia market, the Port of Rotterdam initiated a pre-feasibility study in late 2024 for an ammonia import and cracking terminal with a planned throughput of 1 million tons annually. Yara and Azane Fuel Solutions installed the first ammonia bunkering unit in Norway in 2024, a system with a storage capacity of 400 cubic meters. Additionally, a 2025 joint development project between several Japanese firms aims to put the first 80,000 cubic meter ammonia-fueled gas carrier into service. The world's first ammonia bunkering vessel, with a capacity of 2,500 cubic meters, was ordered in January 2025. Finally, a new green ammonia production facility in Texas, announced in 2024, has already allocated 300,000 tons of its future annual output specifically for maritime fuel offtake.

Green Ammonia Emerges as a Key Solution for Grid Stability

Emerging role of green ammonia as a long-duration energy storage medium and a dispatchable power source for stabilizing renewable-heavy electricity grids have become integral part behind the green ammonia market growth. In 2024, the UK government awarded £4 million in funding to eight different ammonia-to-power projects as part of its innovation portfolio. One of these projects aims to develop a 50 MW ammonia-fueled gas turbine demonstrator by 2025. In the United States, a Department of Energy project initiated in 2025 is developing a solid oxide fuel cell system capable of generating 100 kW of power directly from ammonia for grid support applications.

The application is creating a new demand vertical for large-scale ammonia storage and conversion facilities. In Japan green ammonia market, IHI Corporation began testing a 2 MW gas turbine running on 100% liquid ammonia in early 2025. The company plans to commercialize a 70 MW class turbine by 2028. In Australia, a solar-to-ammonia pilot project that became fully operational in 2024 includes a storage capacity of 3 tons of green ammonia, enough to provide 1.5 MWh of dispatchable electricity. Furthermore, a 2025 feasibility study for a project in Germany is assessing a 500,000-tonne salt cavern for seasonal ammonia storage. Another project in South Korea, announced in late 2024, plans to construct a 50,000-tonne ammonia receiving terminal dedicated to supplying co-firing power plants. An additional 10,000-tonne storage tank for power generation was commissioned in Japan in 2024.

Segmental Analysis

Alkaline Electrolysis Technology Spearheads Green Ammonia Production Capabilities

Alkaline water electrolysis, a mature and cost-effective method, commands the green ammonia market with a dominant 63.19% share. Its leadership stems from inherent advantages in durability and lower capital costs compared to newer technologies. The technology's established supply chains, particularly robust in China, contribute to its economic viability. Chinese manufacturers, for instance, offer alkaline systems at prices around $167/kW for a 5 MW system in 2024, a significant cost advantage. Further innovations are enhancing efficiency; advancements in electrode surface area and zero-gap cell designs are boosting performance and reducing energy losses. Developers are now targeting operational pressures of up to 30 bar, which reduces the need for downstream compression and saves significant energy, approximately 0.1-0.2 kWh per cubic meter of hydrogen. These factors collectively reinforce the technology's position as the go-to choice for large-scale green ammonia production.

The widespread adoption of alkaline electrolysis is evident in the scale of recent projects in the green ammonia market. In January 2025, a partnership was announced to deploy a massive 3 GW electrolyzer system in Australia, one of the world's largest planned green hydrogen projects. The total installed capacity of electrolyzers is projected to reach 35.77 GW by the end of 2024, an increase of 1-2 GW from the previous year. The cost of these electrolyzer systems is also on a downward trend, with projections showing a potential 30% drop by 2025 due to economies of scale and manufacturing improvements.

- Projected System Advancements: Advanced alkaline electrolyzers are being designed to achieve a minimum load of just 10% when operating at 8 bar, enhancing flexibility for integration with intermittent renewable energy sources.

- Growing Model Sizes: While 1,000Nm³/h models dominated 2024 shipments, the delivery of larger 1,200Nm³/h and 2,000Nm³/h units signifies a market shift towards greater production capacities.

- Global Manufacturing Dominance: China controls approximately 85% of the global manufacturing capacity for alkaline electrolyzers, a key factor in their cost-competitiveness.

This continued innovation and cost reduction solidify alkaline electrolysis as the cornerstone of the burgeoning green ammonia market. The technology's proven reliability and improving performance metrics ensure its dominance will persist as the industry scales up to meet global decarbonization goals. With annual shipments reaching over 1,044 MW in 2024, the momentum is clearly established. Furthermore, the development of new electrode materials and coatings promises to further enhance the electrochemical surface area, leading to even greater efficiency in future deployments.

Large-Scale Production Units Underpin Market Expansion and Investment Confidence

The green ammonia market is characterized by the prevalence of large-scale production units, which hold a commanding 45.63% market share. This dominance is a direct result of the economies of scale they offer, making the production of green ammonia more economically competitive against conventional methods. Large projects attract significant multi-billion dollar investments, enabling the development of extensive infrastructure required for high-volume output. For example, a newly announced project in South Africa involves a $5.8 billion investment to produce 1 million tons of green ammonia annually by 2029. Similarly, a facility planned for Saudi Arabia, backed by a $5 billion investment, is expected to produce 1.2 million tons per year starting in 2025. These massive undertakings are essential for meeting the anticipated global demand.

The scale of these projects is a critical factor in de-risking investments and securing long-term offtake agreements, which are vital for financial viability. As of August 2024, the total announced global capacity for low-emission ammonia projects reached an impressive 372.5 million tons across 428 projects. While many are in early stages, the pipeline demonstrates robust confidence in the future of the green ammonia market. Projections indicate that by 2030, 30.6 million tons of this capacity is expected to be operational, a significant increase from the 3.7 million tons in operation as of the third quarter of 2024.

- Substantial Project Investments: A single green ammonia project in Louisiana, announced in April 2025, carries a $4 billion price tag and is designed to produce 1.4 million metric tons annually.

- Significant Capacity Growth: In Denmark, a plant expected to be completed in 2026 will have the capacity to produce approximately 600,000 tons of green ammonia per year.

- Renewable Power Integration: AM Green in India signed an agreement in May 2025 to be supplied with 4,500 MW of renewable energy to support its goal of producing 5 million tons of green ammonia a year by 2030.

The trend towards large-scale facilities across the green ammonia market is also driven by the need to integrate with massive renewable energy sources. One Texas project, for instance, will utilize an 800 MW solar power facility. The sheer volume produced by these plants is necessary to make a meaningful impact on decarbonizing heavy industries and to establish new global trade routes for green energy. It is estimated that a plant producing 2,250 short tons per day requires approximately 1.25 million gallons of water daily, highlighting the resource intensity that necessitates large-scale, efficient operations.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Industrial Consumers Drive Demand and Define Green Ammonia's Primary Role

Industrial consumers are the primary drivers of the green ammonia market, accounting for an overwhelming 77.97% of the revenue share. This is largely because green ammonia serves as a direct, decarbonized replacement for conventional ammonia, a critical feedstock in numerous industrial processes. The fertilizer industry is the most significant of these consumers, traditionally relying on ammonia for nitrogen-based fertilizers. The transition to green ammonia allows this sector to dramatically reduce its carbon footprint, a pressing goal for sustainable agriculture. Projects like ATOME's planned $630 million facility in Paraguay are set to produce 260,000 tons of green fertilizer, directly targeting this demand.

Beyond fertilizers, green ammonia market is gaining traction as a vital energy carrier and a clean fuel for hard-to-abate sectors. The maritime industry, for example, is increasingly looking to green ammonia to meet stringent emissions reduction targets set by the International Maritime Organization. In a significant move, BHP Group contracted two ammonia-fueled bulk carriers in July 2025, which are projected to cut voyage emissions by up to 95%. The chemical industry also utilizes ammonia extensively, and the availability of a green alternative is crucial for decarbonizing manufacturing processes.

- Secured Offtake Agreements: Major industrial players are entering into significant purchase agreements, with one project in Oman securing an offtake deal for 100,000 tons per year with Yara Clean Ammonia.

- High-Volume Industrial Use: A single industrial complex in Spain is slated to be a primary consumer for a green ammonia project that will feature 7.4 GW of electrolyzer capacity.

- Premium on Green Products: Green ammonia is already commanding a price premium of between $100 and $150 per metric ton in industrial markets, reflecting its value in meeting sustainability targets.

The strong demand from these industrial end-users provides the financial stability and market certainty needed for the capital-intensive development of green ammonia projects. Governments and industry consortia in the green ammonia market are actively fostering these relationships, with India's National Green Hydrogen Mission, for example, creating incentives to accelerate adoption within its domestic fertilizer sector. This symbiotic relationship between producers and industrial consumers is foundational to the growth of the global green ammonia market, ensuring that the vast quantities of green ammonia produced by large-scale facilities have dedicated and reliable end markets.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific Commands Global Green Ammonia Market Leadership Position

The Asia Pacific (APAC) region is definitively positioned as the global epicenter of the green ammonia market, projected to command an overwhelming 50.48% market share by 2033. This dominance is underpinned by a massive project pipeline, substantial investment commitments, and strong governmental support, particularly in India, China, and Australia. In India, prominent companies like Avaada Group are developing a 1.1 million-tonne-per-annum plant in Odisha, while Ocior Energy is advancing a 1 million-tonne project in Gujarat with a $4 billion investment. Similarly, YamnaCo signed an MoU in July 2025 for a 1 million-tonne-per-annum facility in Andhra Pradesh, backed by a $1.9 billion investment.

The regional momentum across the green ammonia market is further evidenced by strategic infrastructure and offtake developments. Australia's Gibson Island project, despite delays, is backed by a AUD$13.7 million grant from ARENA for its front-end engineering and design (FEED) study, targeting 400,000 tons of green ammonia production. To meet rising demand from power and industrial sectors, Japan’s Mitsubishi Heavy Industries launched a study in 2025 to create a logistics plan for importing green ammonia from India. In the UAE, construction began in June 2024 on a facility aiming to produce 1 million tons of lower-emission ammonia annually starting in 2027. South Korea is also driving demand through its co-firing initiatives, aiming to have 24 coal power units utilizing ammonia by 2025.

Europe Strategically Builds Import Infrastructure to Secure Future Supply

Europe is aggressively positioning itself as a primary demand center for green ammonia market, focusing on developing large-scale import and distribution infrastructure to meet its ambitious decarbonization targets. The Port of Rotterdam is central to this strategy, with OCI's terminal expansion set to increase throughput capacity to 1.2 million tons per year. In a further move, VTTI launched an open season in December 2024 to gauge market interest for ammonia storage and cracking facilities at its terminals in both Rotterdam and Antwerp. These developments are crucial for receiving future imports and converting ammonia back to hydrogen for industrial use.

To secure these future supplies, Germany has taken a proactive role through its H2Global import scheme. In July 2024, the program awarded its first contract to Fertiglobe for a cumulative supply of up to 397,000 tons of green ammonia between 2027 and 2033. The initial delivery of 19,500 tons is scheduled for 2027 from a production facility in Egypt green ammonia market. The German government has allocated a substantial €4.43 billion to the H2Global 'double-auction' mechanism to underwrite these long-term purchase agreements. These coordinated efforts between port authorities and government bodies underscore Europe’s strategic approach to building a resilient green ammonia import market.

North America Focuses on Large-Scale Production for Export Markets

North America, particularly the US Gulf Coast and Atlantic Canada, is rapidly emerging as a major production hub for the green ammonia market, with a clear focus on serving international export demand. In the US, CF Industries is developing a green ammonia plant in Louisiana, expected to start production in 2025 with an initial capacity of 18,144 tons of hydrogen for ammonia synthesis. The Port of Corpus Christi is also preparing for a massive 10 million-tons-per-year clean ammonia export project scheduled to begin operations in 2030. These projects are heavily supported by government incentives, including a $1.6 billion loan guarantee from the US Department of Energy for the Wabash Valley Resources ammonia project.

Canada is concurrently developing world-scale export-oriented projects further supporting the green ammonia market. World Energy GH2's Project Nujio'qonik in Newfoundland is a notable example, planning to use 4 GW of wind power to produce approximately 1.6 million tons of green ammonia per year. The project, which expects its first production phase of 400,000 tons per year to reach a final investment decision in 2025, has already secured a $95 million credit facility from the federal government. These large-scale production facilities, backed by significant public and private investment, are positioning North America as a key future supplier to Europe and Asia.

Strategic Investments and Funding Fuel Global Green Ammonia Market Expansion

- Hygenco Secures $280 Million for Odisha Project (September 2024): Hygenco Green Energies signed an MOU with REC Limited to finance its green ammonia project in Gopalpur, Odisha, with funding of up to $280 million.

- Amogy Expands Funding Round to $80 Million (July 2025): Ammonia-to-power technology firm Amogy raised an additional $23 million, bringing its total recent venture financing round to $80 million to accelerate commercialization and expansion into Asian markets.

- SA-H2 Fund Invests $20 Million in Coega Project (July 2025): The Coega renewable ammonia project in South Africa received $20 million in development funding from the SA-H2 Fund, which also secured rights to participate in construction funding for up to $200 million.

- Mitsui Finalizes Loan for UAE Ammonia Plant (June 2024): Mitsui & Co. signed a loan agreement with the Japan Bank for International Cooperation (JBIC) to help finance the construction of a 1 million-ton-per-year low-emission ammonia facility in the UAE.

- Hygenco Plans $100 Million+ Fundraise (March 2024): Following an initial $25 million funding round, Hygenco announced plans to raise over $100 million by September 2024 to support its project pipeline and capital expenditure plans.

- Hygenco Announces $2.5 Billion Three-Year Investment (February 2024): Hygenco Green Energies committed to a total capital expenditure of approximately $2.5 billion in India over the next three years to develop its green hydrogen and ammonia project pipeline supporting the green ammonia market growth.

- Amogy Raises $56 Million in Venture Financing (January 2025): In the initial phase of its funding round, Amogy secured $56 million co-led by Aramco Ventures and SV Investment to commercialize its technology for maritime and power generation markets.

- US DOE Provides $1.5 Million for Pre-FEED Study (January 2025): The US Department of Energy awarded $1.5 million to GTI Energy to lead a pre-FEED study for applying carbon capture technology at an ammonia facility in Louisiana.

- Canada Commits $300 Million to H2Global (2024): The Canadian federal government committed $300 million to Germany's H2Global auction mechanism to facilitate offtake agreements for green ammonia, supporting Canadian export projects.

- OCI Invests $20 Million in Rotterdam Terminal Expansion (2024): OCI N.V. made a final investment decision for the initial phase of its Rotterdam ammonia import terminal expansion, committing under $20 million to increase throughput capacity.

Top Companies in the Green Ammonia Market

- CF Industries Holdings, Inc.

- Yara International ASA

- ThyssenKrupp AG

- ACME Group

- Air Products

- Siemens

- Socemo

- Other prominent players

Market Segmentation Overview

By Technology

- Alkaline Water Electrolysis

- Proton Exchange Membrane Electrolysis

- Solid Oxide Electrolysis

- Others

By Capacity

- Small Scale

- Medium Scale

- Large Scale

By End User

- Industrial

- Fertilizer

- Chemical

- Pharmaceutical

- Textile

- Transportation

- Power Generation

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |