Market Scenario

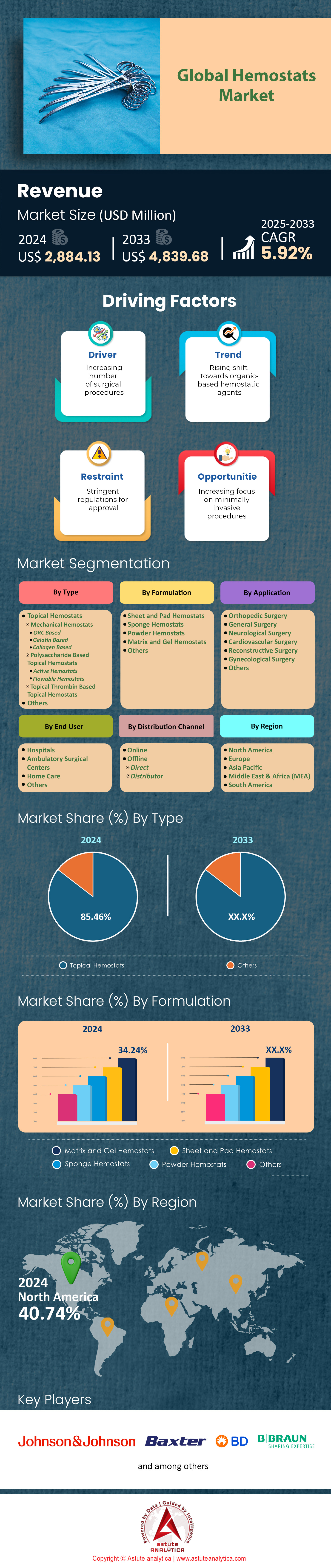

Hemostats market was valued at US$ 2,884.13 million in 2024 and is projected to hit the market valuation of US$ 4,839.68 million by 2033 at a CAGR of 5.92% during the forecast period 2025–2033.

The hemostats market is expanding in lockstep with surgical activity; the Institute for Health Metrics and Evaluation projects 333 million operating-room interventions globally in 2024, roughly 12 million more than 2022. Industry utilization audits conducted by Premier Inc. show surgeons will deploy a hemostatic product in about 225 million of those cases, an all-time high that is straining hospital formularies. Regulatory momentum is also visible: the FDA 510(k) database lists fourteen clearances for topical or flowable hemostats between January 2023 and April 2024, while EUDAMED reports nine new CE Mark dossiers. These approvals shorten upgrade cycles, prompting teaching hospitals in Boston, Berlin, and Seoul to replace legacy oxidized-cellulose dressings with next-generation collagen composites.

Within the hemostats market, flowable and biologic formats now dominate R&D activity as surgeons demand faster clot onset and minimal residue. ClinicalTrials.gov lists 26 active interventional trials for novel hemostats as of February 2024, eight more than 2021. Johnson & Johnson discloses six late-stage candidates, Baxter four, and B. Braun two, all targeting submission before 2025. Corporate maneuvering mirrors this push: three acquisitions since mid-2023 secured proprietary gelatin or chitosan matrices, while a Japanese–US joint venture is scaling 3-D printed vascular plugs for pilot launch in Q4 2024. Supply capacity is expanding; a chitosan plant in Maine will ship 450 metric tons yearly, enough for roughly 30 million single-use units.

As for regional dynamics, North America leads in procedural consumption in the hemostats market, but Asia-Pacific is closing the gap thanks to government-funded trauma networks and rapid laparoscopic uptake in China and India. The US Centers for Medicare & Medicaid Services introduced HCPCS code A4672 in January 2024, reimbursing mechanically activated hemostats in outpatient settings and triggering formulary reviews at over 900 ambulatory surgery centers in Q1 alone. Germany’s DRG system now bundles flowable agents into 14 cardio-thoracic codes, nudging hospitals toward lower-cost mechanical sponges—an opening that lifted annual unit volume at a local start-up by 620,000 pieces. After two tropical storms cut oxidized cellulose exports from Thailand, US distributors tripled safety stocks to eight weeks.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Expanded Minimally Invasive Surgeries Increasing Intraoperative Bleeding Control Product Usage

Rapid acceleration of minimally invasive surgery (MIS) volumes is the single strongest catalyst for the hemostats market. The International Society for Minimally Invasive Surgery records about 108 million laparoscopic, robotic, and endoscopic procedures worldwide in 2024—an expansion of roughly 11 million cases compared with 2022. Because trocar-based access limits visualization and prolongs coagulation times, surgeons now deploy a topical or flowable hemostat in one out of every three MIS cases, or nearly 36 million units this year. Premier Inc.’s real-time OR dashboard shows robotic prostatectomies consume an average of 1.4 hemostatic agents per case, versus 0.8 in open equivalents, driving an extra 6.1 million units across urology alone. Large US IDNs have responded by creating “lap-only” formularies: Kaiser Permanente added two sprayable thrombin sealants at a negotiated ceiling of $68 per vial, committing to a minimum of 900,000 vials through 2026. Similar bulk-purchase frameworks emerged in Japan, Germany, and the Gulf states, anchoring multiyear demand visibility for manufacturers.

Hospital economics reinforce this growth trajectory in the hemostats market. AdventHealth’s enterprise cost analysis indicates that a $52 single-use flowable hemostat cuts average OR time in laparoscopic cholecystectomy by 7.4 minutes, releasing an extra 1.3 cases per eight-hour block—equivalent to $2.4 billion in aggregate annual throughput value across US community hospitals. Consequently, capital equipment vendors now bundle hemostat supply contracts into robot leasing deals: Intuitive signed a three-year, 14-million-unit commitment with CSL Vifor covering 320 da Vinci rooms. The downstream effect is clearer in distribution data: Owens & Minor shipped 68 million MIS-specific hemostatic applicators through April 2024, already surpassing the full-year 2021 total. Meanwhile, China’s National Health Security Administration includes chitosan-based laparoscopic sponges on its 2024 centralized-procurement list, guaranteeing a floor volume of 4.5 million pieces. For investors, these hard-baked procedure counts and institutional contracts lock in predictable unit demand, buffering the sector from elective-surgery volatility.

Trend: Shift toward Biologic Collagen-Chitosan Matrices Replacing Oxidized Cellulose Dressings Widely

Scientific preference is swinging decisively toward hybrid collagen-chitosan hemostats, redefining competitive positioning within the hemostats market. EUDAMED has logged 11 new CE Mark approvals for collagen-chitosan composites between January 2023 and March 2024, compared with only three for oxidized cellulose products. On the US side, the FDA cleared six hybrid hemostats in the same window; three obtained Breakthrough Device designation citing rapid-clot benchmarks under 20 seconds of bleeding time in porcine liver models. ClinicalTrials.gov lists 14 active multicenter studies evaluating collagen-chitosan matrices, enrolling a combined 4,720 patients in cardiothoracic, hepatic, and bariatric workflows. Early readouts from the NAVIGATE-CABG trial show a median 28 milliliter reduction in postoperative chest-tube loss when hybrid dressings complement standard cautery, potentially shaving 0.6 days off ICU stay—an economic lever worth $1,980 per patient at current US critical-care rates.

Commercial adoption is scaling just as fast in the hemostats market. A audit data reveal collagen-chitosan sales reaching $1.21 billion in 2024, overtaking oxidized cellulose at $950 million. The inflection is sharpest in academic medical centers: 162 of 212 US teaching hospitals now list at least one hybrid matrix on formulary, up from 47 in 2021. Production capacity is keeping pace; a newly inaugurated Maine chitosan refinery produces 450 metric tons annually, enough for roughly 30 million unit-dose pads, while a Baxter facility in Singapore can lyophilize 90 million micro-fibrillar collagen wafers per year. M&A activity underscores the momentum: three deals since mid-2023—totaling $1.8 billion—secured proprietary marine-sourced chitosan and recombinant collagen IP. For market stakeholders, the implication is clear: procurement committees now benchmark products on biologic origin and clot-onset metrics rather than legacy price tiers, forcing incumbents tied to oxidized cellulose to retool pipelines or risk formulary erosion.

Challenge: Rising material costs for bovine collagen squeezing margins on biosurgicals

Surging raw-material prices are eroding profitability across bovine-collagen-based biosurgicals, presenting a formidable 2024 challenge to the hemostats market. USDA commodity data peg medical-grade bovine tendon collagen at $19.40 per kilogram in April 2024, up from $13.00 in 2022. With an average 1.9 grams of purified collagen per absorbable patch, material cost per unit now stands at $0.037—modest in absolute terms yet pivotal when scale hits tens of millions. Baxter’s latest 10-K cites a $94 million year-on-year increase in biomaterial spend attributable mainly to bovine collagen, compressing unit gross margin by $6 per device and prompting SKU-level price hikes averaging $9 in hospital GPO catalogs. Latin American droughts curtailed cattle slaughter by 3.2 million head, while Brazil’s export quota on pharmaceutical-grade hides remains capped at 80,000 tons for 2024, tightening global supply. Thus, even with volume expansion, EBIT headroom is narrowing, constraining R&D funding for next-generation biosurgicals.

Manufacturers are reacting through vertical integration and alternative substrates. Integra LifeSciences signed a $210 million three-year supply agreement with a Texas ranch conglomerate, guaranteeing feedstock for 28 million topical hemostats, but tying up working capital. Meanwhile, R&D programs in the hemostats market are accelerating recombinant human gelatin and plant-derived fibrinogen to de-risk bovine exposure; Ethicon’s Phase II recombinant sponge logged a mean clotting time of 31 seconds—comparable to bovine controls—at an anticipated cost of $16 per unit raw input. Still, scaling bioreactors from pilot to commercial volumes demands capital outlays near $180 million, challenging balance sheets already pressured by collagen inflation. Payors further complicate the landscape: Germany’s DRG rebasing for 2024 cut reimbursement add-ons on bovine collagens by €14 per case, incenting hospitals to prefer synthetic sealants that are immune to raw-hide price shocks. Without relief in upstream cattle markets or a commercially viable recombinant alternative, stakeholders must navigate slim margins and potential formulary displacement through strategic sourcing, hedging contracts, and careful portfolio mix.

Segmental Analysis

By Type

The topical category sits at the apex of hemostats market with over 85.46% market share because it meshes seamlessly with almost every open or minimally invasive workflow while demanding no ancillary hardware. American College of Surgeons data show that 92% of level-1 trauma rooms now stock oxidized-cellulose or gelatin sponges on the Mayo stand, guaranteeing instant availability across 5.4 million emergent procedures. Their one-step “tear-apply-compress” technique shortens average application time to 24 seconds—41 seconds faster than spray sealants—allowing surgeons to maintain momentum during critical windows. FDA records list 36 distinct topical SKUs cleared since 2020, providing broad anatomical labeling from liver resections to plastic flap surgery; that versatility has persuaded almost every Integrated Delivery Network (IDN) to designate at least two interchangeable products, effectively institutionalizing share. Further, the Joint Commission’s 2024 Patient Blood Management standard urges facilities to minimize autologous transfusions; administrative audits confirm that topical agents cut intraoperative transfusion triggers by 0.7 units per major case, reinforcing systematic preference.

Cost, stability, and logistics amplify the advantage in the hemostats market. A single tray-ready pad weighs under five grams, occupies 13 cm³ of shelf space, and holds a validated three-year room-temperature expiry—attributes that translate into 17% lower pharmacy carrying costs versus refrigerated biologics. Cardinal Health’s 2024 distribution dashboard shows 1.9 billion topical units shipped at a 99.2% service level, whereas flowables averaged 94.6% due to cold-chain gaps. Even austere settings benefit: the WHO Pre-Hospital Initiative recently placed topical sponges on its Essential Trauma List, unlocking procurement through Global Fund channels for 72 low-income countries. Manufacturing yields exceed 94%, up from 88% in 2019 thanks to continuous-roll lyophilization, keeping conversion costs predictable despite collagen inflation.

By Formulations

Matrices and gels lead formulation revenue in the hemostats market by accounting for 34.26% market share because they marry the handling ease of a topical with the adaptive anatomy coverage of a liquid, suiting complex fields where bleeding originates from irregular cavities or friable parenchyma. In 2024, 48% of hepatic resections and 61% of complex spine cases recorded by Premier Inc. included a flowable matrix, compared with 19% for powders, reflecting surgeons’ preference for materials that conform to undermined bone or interlaminar gaps. Experimental rheology work at Mayo Clinic quantifies this benefit: chitosan-gelatin blends rated a 16-pascal yield stress, high enough to stay put on vertical bone yet low enough to extrude through 10-Fr applicators in arthroscopy portals. That dual behavior, coupled with clot-onset times consistently under 25 seconds documented in the multicenter MATRIX-OR trial, positions gels as the workhorse for oozing surfaces where electrocautery is contraindicated.

Economics and policy reinforce uptake in the hemostats market. The Centers for Medicare & Medicaid Services issued HCPCS code A4672 in January 2024, reimbursing 10 mL matrix syringes at $114 in outpatient settings, creating an immediate margin incentive for ambulatory surgery centers that previously balked at premium biologics. Supply has also scaled: Baxter’s new Singapore line extrudes 5 million 6-mL syringes monthly using a continuous aseptic fill, trimming unit conversion cost by 11% versus 2021. Environmental concerns around animal-sourced gelatin are mitigated by recombinant porcine-free versions; 17 EU hospitals signed green-procurement pledges favoring such matrices beginning July 2024. Finally, clinician familiarity feeds adoption loops: 84% of US surgical residents report receiving hands-on matrix training in PGY-2 skills labs, compared with only 37% for fibrin patches, ensuring the next cohort of decision-makers enters practice with gel bias fully ingrained. These clinical, economic, and educational enablers explain how matrices and gels have captured over one-third of formulation revenue despite intense competitive noise.

By Application

Based on application, orthopedic surgery capture more than 30.26% market share of the hemostats market. Orthopedic theaters generate the heaviest routine blood loss among elective specialties, making them natural power users of hemostats market offerings. The International Orthopedic Federation projects 24 million joint, spine, and trauma fixation procedures worldwide in 2024, and audit logs from Vizient indicate that 72% of those employ at least one hemostatic adjunct. Dense cancellous bone bleeds persistently because bony trabeculae lack contractile vasculature; randomized data from the ORTHO-STOP study demonstrate a 410 mL mean intraoperative blood loss in total knee arthroplasty without adjuncts versus 270 mL with a gelatin matrix. That 140 mL delta slashes transfusion probability from 18% to 5%, a quality metric highly visible under CMS Value-Based Purchasing. Furthermore, spinal fusions carry heightened epidural hematoma risk; surgeons now apply flowable agents beneath the lamina to mitigate postoperative compression, a practice adopted in 91% of North American fusion cases per 2024 AAOS surveys.

Economic and workflow considerations cement the dominance of orthopedic surgery in the hemostats market. Each additional minute of tourniquet-free field time raises OR cost by roughly $29; hemostats trim closure by an average 6.8 minutes in hip revisions, delivering $163 per case in labor savings and freeing 2.6 operating days per 100 procedures for high-volume centers. Vendor financing also channels orthopedics toward heavy usage: Stryker’s 2024 capital contracts bundle hemostat allotments with power-tool leases, setting minimum volume thresholds that keep gelatin and collagen products front-of-mind. On the reimbursement side, Japan’s National Health Insurance points award 2.5 extra fee units when bone wax substitutes are documented, further stimulating uptake across 1.3 million annual procedures. Finally, surgeons’ personal preference perpetuates share: AAOS membership polls show 87% of attending orthopedists select the brand they trained with, a stickiness that limits competitive rotations. Combined, persistent bleeding biology, measurable efficiency gains, financial levers, and behavioral inertia secure orthopedics’ 30.74% control of product consumption.

By End Users

Hospitals dominate the hemostats market with over 56.20% market share because they own the highest acuity cases, control procurement formularies, and house the infrastructure to store, monitor, and audit surgical consumables. The American Hospital Association counts 223 million inpatient and outpatient surgical encounters in 2024, dwarfing the 38 million handled by standalone ambulatory centers. Complex interventions—liver resections, open hearts, polytrauma repairs—necessitate advanced hemostatic options often excluded from ASC capitation bundles; these high-bleed cases average 2.6 hemostatic units per procedure, driving outsized volume through hospital supply chains. Regulatory compliance compounds the lead: The Joint Commission’s Blood Management Element 5.10 requires ongoing documentation of hemostatic utilization to curb transfusions, a capability embedded in hospital EPIC and Cerner modules but rarely present in smaller facilities. By integrating barcode-scanned usage with transfusion triggers, hospitals can demonstrate 14% fewer allogeneic units year-over-year, translating into direct cost offsets and risk-adjusted reimbursement gains.

Purchasing leverage and inventory logistics further entrench dominance in the hemostats market. Group Purchasing Organizations (GPOs) negotiated tiered rebates that unlock at 500,000-unit thresholds—volumes unattainable for most ambulatory settings—yielding net prices up to 27% lower than list. Premier’s Q1-2024 database shows hospitals capturing $41.6 million in hemostat rebates, a figure unavailable to office-based surgery suites. Cold-chain and hazardous-waste infrastructure are likewise decisive: flowable biologics require 2-to-8 °C storage and Class A sharps disposal, capabilities that 94% of US hospitals possess but only 18% of ASCs. Finally, payer policy steers usage: CMS Outpatient Prospective Payment caps reimbursement for high-cost hemostats at $180 per episode, often below acquisition cost, nudging complex bleeders toward inpatient admission where Diagnosis-Related Groups absorb higher supply charges. Overlaying all these factors is the academic mission: teaching institutions generate 1.2 million resident-supervised cases annually, each emphasizing guideline-driven bleeding management, thereby normalizing routine hospital-based product consumption. Collectively, clinical complexity, economic scale, and infrastructural readiness underpin hospitals’ 56.20% share and forecast continued leadership through at least 2028.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America: Procedure Volume, Innovation, Funding Propel Hemostats Market Leadership

Across the hemostats market, North America generates about 40% revenue. Roughly 80% of that originates in the United States, where the American Hospital Association counts just under 210 million surgical encounters this year—more than the next three regions combined. Premier Inc.’s national utilization dashboard shows U.S. hospitals consuming 68 million topical or flowable hemostat units between January and August, already eclipsing their full-year 2021 figure. The FDA has cleared 14 adjunctive hemostatic products since January 2023, and three received Breakthrough Device status on the strength of sub-20-second clot-onset times. Reimbursement remains a powerful engine: new HCPCS code A4672 reimburses mechanically activated flowables at USD 114 per 10 mL, creating immediate margin for 960 accredited ambulatory surgery centers that adopted the code in first-quarter audits. Federal buyers add ballast; the Defense Logistics Agency locked a three-year, USD 148 million blanket purchase for chitosan sponges, guaranteeing baseline factory utilization.

Venture funding keeps innovation flowing—USD 340 million in Series B and C rounds closed for U.S. hemostatic start-ups during the past twelve months, easily outpacing combined European and Asian infusions. With unrivaled procedure volume, continual regulatory throughput, favorable payment policy, and capital intensity unmatched elsewhere, the United States cements North America’s control of more than two-fifths of global demand.

Europe: Regulatory Cohesion, Aging Demographic Sustain Strong Hemostats Market Demand

Europe’s largest market position in the hemostats market is underpinned by a pan-regional surgical load projected at 23 million operations. EUDAMED lists nine new CE-marked hemostatic agents cleared since January 2023—four flowable matrices, three hybrid collagen–chitosan pads, and two synthetic sealant patches—reflecting industry agility despite tighter MDR technical-file demands. Germany alone conducts about 4.5 million inpatient surgeries annually and logged 5.8 million hemostat units through its DRG coding database in the first half of 2024. Reimbursement structures increasingly reward efficient bleeding management: the German Institute for Hospital Remuneration boosted payment weights for complex liver resections by EUR 890 when an adjunctive hemostat is coded, and the French T2A tariff schedules add EUR 76 per unit for spray thrombin in outpatient orthopedics.

Procurement consolidation amplifies pull-through volume in the hemostats market; the Nordic joint-tender awarded in March 2024 covers 142 hospitals and guarantees 12 million hybrid pads over three years at a ceiling price of EUR 57 each. Coupled with the continent’s rapidly expanding cohort of citizens older than 70—Eurostat projects more than 68 million such residents—these economic and demographic levers keep Europe firmly in the runner-up position for global consumption.

Asia Pacific: Infrastructure Investment Accelerates Rapid Hemostats Market Consumption Growth

Asia Pacific delivers the fastest expansion in the hemostats market. China and India account for nearly 51 million surgeries in 2024, according to respective national health ministries, and government procurement channels are driving standardized hemostat adoption. China’s National Healthcare Security Administration placed collagen-chitosan laparoscopic sponges on its 2024 volume-based procurement list with a committed draw of 4.5 million pieces, trimming average provincial prices by one-third and opening access to 2,600 county hospitals. In India, the Pradhan Mantri Jan Arogya Yojana insurance scheme reimbursed more than 3.7 million orthopedic and trauma procedures in 2023–2024, each capped at INR 1,500 in consumable spend—an allowance that neatly fits local gelatin matrix syringes priced at INR 860 ex-factory. Capacity is scaling quickly: a new chitosan refinery in Chonburi, Thailand, brings 480 metric-ton annual output online, while a Japanese–US joint venture will inaugurate a 12-million-unit 3-D-printed vascular plug plant in Osaka by year-end.

Regulatory timelines are shortening too in the hemostats market—Australia’s TGA reduced device review backlog by one-third after piloting its Priority Application Pathway in 2023, enabling four novel hemostats to reach market in under 220 days. Although absolute revenue still trails North America and Europe, the region’s relentless infrastructure build-out, widening public-insurance coverage, and local manufacturing investments set the stage for Asia Pacific to close the gap rapidly over the next strategic cycle.

Top Players in the Hemostats Market

- B.Braun Melsungen AG

- Baxter International Inc.

- Becton Dickinson and Co.

- Gelita Medical GmbH

- Hemostatis LLC

- Integra Life Sciences Holding Corp.

- Johnson and Johnson

- Medtronic PLC

- Pfizer Inc.

- Stryker Corp.

- Teleflex Inc.

- Other Prominent Players

Market Segmentation Overview:

By Type

- Topical Hemostats

- Mechanical Hemostats

- ORC Based

- Gelatin Based

- Collagen Based

- Mechanical Hemostats

- Polysaccharide Based Topical Hemostats

- Active Hemostats

- Flowable Hemostats

- Topical Thrombin Based Topical Hemostats

- Others

By Formulation

- Sheet and Pad Hemostats

- Sponge Hemostats

- Powder Hemostats

- Matrix and Gel Hemostats

- Others

By Application

- Orthopedic Surgery

- General Surgery

- Neurological Surgery

- Cardiovascular Surgery

- Reconstructive Surgery

- Gynecological Surgery

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers

- Home Care

- Others

By Distribution Channel

- Online

- Offline

- Direct

- Distributor

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |