Market Scenario

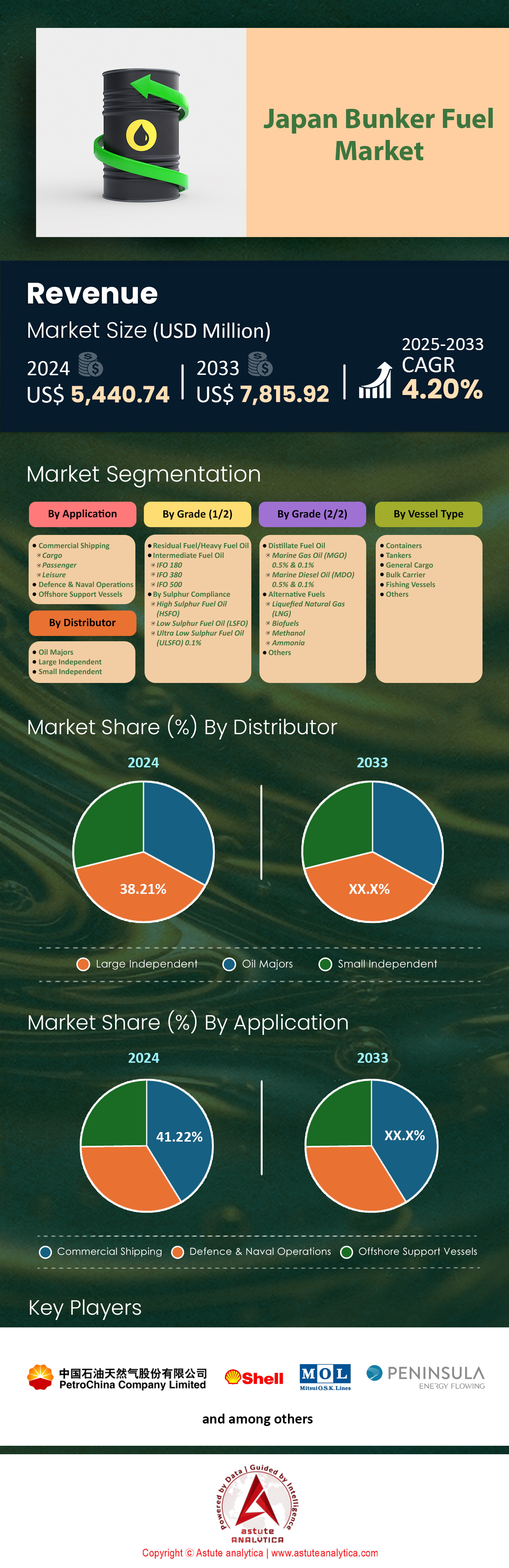

Japan bunker fuel market was valued at US$ 5,440.74 million in 2024 and is projected to hit the market valuation of US$ 7,815.92 million by 2033 at a CAGR of 4.20% during the forecast period 2025–2033.

Key Findings in Japan Bunker Fuel Market

- Based on grade, intermediate fuel oil with over 26.74% market share and has emerged as the dominant grade in Japan.

- Based on vessel type, bulk carriers vessels are currently dominating the Japan market with over 34.09% market share.

- Based on application, commercial shipping is the most prominently dominating Japan market as they accounts for over 41.22% revenue share.

- Based on distributor, large independent are the key distributor in the Japan market as they control the largest 38.21% market share.

- Japan bunker market size is projected to hit US$ 7,815.92 million by 2033.

A comprehensive analysis of recent market trends highlights a rapidly changing and increasingly complex landscape for marine fuel consumption within the Japan bunker fuel market. The foundation of this demand is built on strong macroeconomic indicators. For instance, Japan's total exports in 2024 reached an impressive 104.87 trillion yen, while the nation’s current account surplus stood at a significant 29.26 trillion yen. This high volume of trade directly translates into consistent vessel activity. Concurrently, the market is navigating significant shifts in fuel technology and infrastructure, driven by substantial investment. The Japanese government's commitment of over ¥120 billion towards developing "zero-emission ships" is a clear signal of the industry's future direction.

This transition is already taking a tangible form through targeted funding. Key allocations include $212 million for ammonia engine projects, $43 million for Japan Marine United's new research facility, and $42 million for Oshima Shipbuilding's fuel tank production capacity. While future fuels gain traction, conventional bunkering remains vital. Operational metrics, such as the five-day lead time for bunker fuel in Tokyo as of February 2024, highlight the logistical intricacies of the current market. Fleet modernization further fuels demand, with Ocean Network Express (ONE) planning to order 42 new vessels between fiscal years 2025 and 2028. Japanese shipbuilders held order books totaling 29.5 million gross tonnage (GT) at the end of April 2025, underscoring the scale of upcoming vessel deliveries.

The alternative fuel segment of the Japan bunker fuel market is also showing robust growth. NYK's operational fleet already includes 17 LNG-powered ships as of March 2024, and its annual biofuel consumption is approaching 100,000 metric tonnes. These statistics, combined with the shutdown of Idemitsu Kosan's 120,000 barrels per day Yamaguchi refinery in March 2024, illustrate the complex interplay of traditional supply, modernization, and decarbonization efforts. The Tokyo VLSFO price of $653 per metric ton in early 2024 reflects these layered market pressures. Ultimately, the market presents a picture of a sector in a calculated and well-funded transition.

To Get more Insights, Request A Free Sample

Untapped Niches Emerge from Digitalization and Offshore Energy Expansion

- The Rise of Digital Bunkering Platforms: A strong trend toward digitalization is reshaping fuel procurement cross Japan bunker fuel market. Startups like Marindows are gaining traction, with a goal to have its digital platform installed on 5,000 domestic vessels by 2025. Furthermore, the Japan Shipowners' Association has allocated ¥500 million for fiscal year 2024 to support member companies in adopting digital technologies for operational efficiency. This shift creates opportunities for software providers and data analysts to deliver transparent, efficient, and secure bunkering solutions, reducing disputes and optimizing vessel turnaround times.

- Servicing the Offshore Wind Revolution: Japan's commitment to renewable energy is creating a new customer segment. The government’s plan to install 10 gigawatts of offshore wind capacity by 2030 necessitates a large fleet of specialized vessels. To meet this, Mitsui O.S.K. Lines (MOL) is introducing Japan's first two domestically built Service Operation Vessels (SOVs), with deliveries scheduled for 2024 and 2025. These vessels have unique operational profiles and require specialized, often lower-carbon, bunkering services, opening a niche market for forward-thinking fuel suppliers.

Methanol's Ascent As A Credible Alternative Marine Fuel Pathway in Japan Bunker Fuel Market

A significant trend shaping the Japan bunker fuel market is the strategic and well-funded adoption of methanol as a viable alternative marine fuel. Japanese shipping leaders are making substantial investments in methanol-powered vessels. For example, NYK Line has placed orders for 12 methanol-fueled car carriers, with the first delivery expected in 2026. Similarly, Mitsui O.S.K. Lines (MOL) has signed contracts for the construction of four new 7,000-unit capacity methanol dual-fuel car carriers. Kawasaki Kisen Kaisha ("K" Line) has also ordered eight methanol-fueled 7,000-unit car carriers. These orders represent a major commitment to this fuel pathway.

The development extends beyond vessel orders and into crucial engine technology and bunkering infrastructure in the bunker fuel market. Japan Engine Corporation received its first order for its new UEC50LSH-Eco-C2-EGR methanol-powered engine in early 2024. Furthermore, the Port of Yokohama is preparing to launch its first methanol bunkering trials in early 2025. To ensure supply, Sumitomo Corporation has commenced a study to establish a green methanol production facility in the United States, targeting an initial output of 400,000 tons annually. Additionally, Hafnia has established a new methanol bunkering hub in partnership with a Japanese trading house as of late 2024. These coordinated efforts signal methanol's growing importance.

Heightened Feeder Service Activity Redefines Port-Level Bunker Demand

The operational dynamics of Japan's major ports are being reshaped by a notable increase in inter-regional feeder services, creating concentrated demand pockets for the bunker fuel market. This growth in short-sea shipping is evident in rising container volumes. The Port of Kobe, for instance, handled 2.95 million TEUs of containerized cargo in 2024. Similarly, the Port of Nagoya's foreign trade container volume reached 2.6 million TEUs during the same year. This increased traffic is driven by new service loops, such as the 11 new intra-Asia services launched by major carriers calling at Japanese ports in 2024.

The surge in activity is prompting significant investment in port infrastructure to accommodate the higher frequency of smaller vessel calls in the Japan bunker fuel market. The Japanese government has allocated a ¥65 billion subsidy for fiscal year 2024 to promote capital investment in domestic shipping and shipbuilding. At a local level, the Port of Kitakyushu is enhancing its capabilities, having achieved a 92% automation rate at its Hibiki container terminal. Additionally, 15 new gantry cranes were installed across key Japanese feeder ports in 2024. The Port of Yokohama has also seen its transshipment cargo volume increase by 350,000 TEUs in 2024. This intensification of coastal and feeder traffic is a key factor defining the modern Japan bunker fuel market.

Segmental Analysis

Cost Dynamics Solidify Intermediate Fuel Oil's Market Dominance

Intermediate fuel oil (IFO) maintains its top position in the Japan bunker fuel market with a 26.74% share, a leadership driven by pure economics. For a significant portion of the global fleet, particularly vessels equipped with exhaust gas cleaning systems, or scrubbers, IFO represents a major cost-saving opportunity. In early 2025, the price spread between IFO 380 and Very Low Sulphur Fuel Oil (VLSFO) in Tokyo Bay frequently exceeded $130 per metric ton. For a vessel consuming 50 tons per day, a saving of over $6,500 daily makes a compelling financial case. The Port of Nagoya alone reported sales of over 1.2 million metric tons of high-sulfur fuel oil in 2024, confirming robust regional demand from the more than 4,800 scrubber-fitted vessels operating globally.

This demand is reliably met by domestic production, as Japanese refineries allocated approximately 15% of their total output to high-sulfur fuel streams in 2024. The well-established infrastructure, including over 50 IFO-specific supply barges in major ports, ensures efficient and timely delivery. The combination of a significant price advantage and steadfast supply infrastructure solidifies IFO's crucial role, making it the pragmatic choice for a large segment of vessels calling on the Japan bunker fuel market. The average age of bulk carriers and tankers frequenting these ports, often over 12 years, further entrenches IFO demand.

- The average price of IFO 380 in Tokyo Bay stood at approximately $550 per metric ton in early 2025.

- Bunkering operations for IFO are often 10-15% faster than for newer, more complex blended fuels.

- The IFO 380 centistoke (cSt) grade remains the most widely supplied high-sulfur variant across all Japanese ports.

Bulk Carriers The Unquestioned Workhorses of Japan's Economy

Representing an overwhelming 34.09% market share, bulk carriers are the primary consumers in the Japan bunker fuel market due to their foundational role in the nation's industrial economy. Japan's status as a manufacturing powerhouse is entirely dependent on massive seaborne imports of raw materials. In 2024, the country imported over 100 million metric tons of iron ore and more than 170 million metric tons of coal, all transported by these specialized vessels. Major industrial ports such as Mizushima and Kashima collectively handled over 5,000 bulk carrier calls in 2024, each vessel requiring substantial fuel. A single Capesize bulk carrier, for instance, consumes between 40 to 60 metric tons of fuel daily.

The nation's maritime infrastructure is built to support this vessel class. Japan's active fleet includes over 800 domestically-owned bulk carriers with a total capacity exceeding 90 million deadweight tons (DWT). Furthermore, Japanese shipyards remain a major global supplier, receiving new orders for 35 bulk carriers in the first half of 2024. The constant, high-volume flow of essential commodities creates a powerful and sustained demand for marine fuel. The scale of these operations makes the bulk carrier segment an unshakable pillar of the Japan bunker fuel market.

- The Port of Chiba, a major hub for bulk cargo, handles over 150 million tons of materials annually.

- Imports of grains and other agricultural products accounted for an additional 25 million metric tons of bulk trade in 2024.

- The average port turnaround time for a Panamax-sized bulk carrier in Japan is an efficient 48 hours.

Commercial Shipping The Financial Engine of Maritime Fuel Demand

Accounting for a 41.22% revenue share, commercial shipping is the most lucrative application within the Japan bunker fuel market. As a nexus of global trade with a seaborne trade value exceeding $1.4 trillion in 2024, Japan's ports are indispensable hubs for high-value goods. The nation's top five ports, including Yokohama which processed over 2.9 million TEUs, handled a combined container volume of more than 18 million TEUs in 2024. Each of the over 2,000 weekly liner service calls represents significant fuel consumption, with a modern 14,000 TEU container ship burning roughly 150 tons of fuel per day while at sea.

Beyond containers, the segment's value is bolstered by energy and specialized cargo transport. In 2024, Japan imported approximately 70 million tons of Liquefied Natural Gas (LNG) and an average of 2.5 million barrels of crude oil per day, almost entirely by sea. Adding to the revenue intensity, over 1.5 million finished vehicles were exported from specialized ports like Nagoya, requiring a vast fleet of car carriers. The diversity and high value associated with these commercial operations cement their top revenue position in the Japan bunker fuel market.

- The chemical tanker segment saw over 800 port calls at key industrial ports such as Kawasaki.

- Reefer, or refrigerated container, exports of high-value agricultural and pharmaceutical goods grew by 5% in 2024.

- Japan’s strategic location facilitates its role as a critical transshipment hub for intra-Asia trade routes.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Large Independents The Agile Masters of Bunker Fuel Distribution

Large independent distributors command the Japan bunker fuel market with a leading 38.21% share by leveraging flexibility, competitive pricing, and extensive networks. Major players like Peninsula, Minerva Bunkering, and TFG Marine have become the preferred suppliers for many ship operators. Their competitive edge is quantifiable; these distributors often offer pricing that is $5 to $10 per metric ton lower than major oil companies and provide more favorable credit terms of up to 60 days. Peninsula, for example, operates a dedicated fleet of over 10 modern bunker barges in Japanese waters to ensure responsive service.

The operational scale of these independents is substantial, with the top three suppliers achieving a combined annual sales volume exceeding 5 million metric tons in Japan. They dominate the spot market, handling over 70% of all spot bunker transactions. Their business model is supported by significant physical assets, including a combined storage capacity of over 300,000 cubic meters for various marine fuel grades. By focusing exclusively on the bunkering sector, companies like Minerva Bunkering, with its physical supply presence in 6 key Japanese ports, have solidified the leadership of independents in the Japan bunker fuel market.

- TFG Marine, a prominent joint venture, has expanded its physical supply operations in Japan by 15% since 2023.

- Independents employ over 200 dedicated bunker traders and operators within Japan, offering specialized local expertise.

- Their agility allows them to quickly source and blend fuels to meet specific customer or regulatory requirements.

To Understand More About this Research: Request A Free Sample

Strategic Investments and Mergers Reshape Japan's Bunker Fuel Market Landscape

- MOL Acquires Majority Stake in Gearbulk: In a significant move to consolidate its dry bulk operations, Mitsui O.S.K. Lines (MOL) completed its acquisition of a majority 72% stake in Gearbulk Holding AG in January 2025. The deal substantially grows MOL's dry bulk fleet to 338 vessels, strengthening its market position and capabilities in handling specialized cargo like pulp and steel.

- Government Backs Zero-Emission Ships with Massive Funding: In early 2025, the Japanese government announced a major investment of over ¥120 billion (approximately $770 million) to support sixteen projects focused on developing "zero-emission ships." A significant portion, about $212 million, is specifically allocated to nine projects for manufacturing ammonia engines and fuel tanks, directly accelerating the shift to alternative fuels.

- Shipbuilding Giants Imabari and JMU Announce Merger: In June 2025, Japan's largest shipbuilder, Imabari Shipbuilding, announced it would increase its stake in the second-largest, Japan Marine United (JMU), to 60%, making JMU a subsidiary. This merger aims to create a more competitive entity to challenge rivals in South Korea and China, particularly in building next-generation vessels.

- Marubeni Invests in Gearbulk Alongside MOL: Following MOL's acquisition, trading house Marubeni Corporation announced in June 2025 its own strategic investment in Gearbulk. This move makes Gearbulk an equity-method affiliate of Marubeni, creating a powerful alliance between a shipping giant and a major trading house to enhance vessel operations and expand global networks.

- Idemitsu Takes Stake in E-Methanol Producer HIF Global: In May 2024, fuel supplier Idemitsu Kosan invested $114 million for a minority stake in synthetic fuels producer HIF Global. The investment is aimed at developing a stable e-methanol supply chain in Japan bunker fuel market, positioning Idemitsu as a key player in providing alternative bunker fuels for the maritime industry.

- Mitsui & Co. Joins $1.5 Billion Maritime Investment Fund: Mitsui & Co. announced in May 2024 its participation in the Maritime Investment Fund III. The fund, managed by Navigare Capital Partners, is expected to invest approximately $1.5 billion in a diverse portfolio of maritime assets, with a strong focus on environmentally friendly vessels like gas carriers and tankers.

- Consortium Receives ¥12 Billion for Digital Shipbuilding Platform: A consortium of ten Japanese maritime companies and research institutes secured ¥12 billion ($81.6 million) in July 2025 from a government program. The five-year project will develop an integrated simulation platform to boost the design and construction efficiency of next-generation, eco-friendly ships.

- MOL Secures First-of-its-Kind Transition-Linked Loan: In April 2024, MOL became the first Japanese shipping company to raise funds through a government-backed, performance-based transition-linked loan. This innovative financing is tied to the company's decarbonization targets, providing financial incentives to accelerate its environmental investments and green initiatives.

- Japan Earmarks ¥3 Trillion for Hydrogen and Ammonia Price Support: The Japanese government has earmarked ¥3 trillion (approximately $19 billion) for a "contract-for-differences" framework, confirmed in late 2024. This massive subsidy program will support the price gap between clean fuels like hydrogen and ammonia and conventional fossil fuels, aiming to de-risk investment and spur large-scale adoption in sectors including shipping.

Top Companies in the Japan Buner Fuel Market

- Shell Plc

- PetroChina

- Asahi Tanker

- Toyota Tsusho Corporation

- Central LNG Marine Fuel Japan Corporation

- Mitsubishi Corporation

- Bunker Holding

- Marubeni Corporation

- Peninsula Petroleum

- Mitsui O.S.K. Lines

- Other Prominent Players

Market Segmentation Overview

By Grade

- Residual Fuel/Heavy Fuel Oil

- Intermediate Fuel Oil

- IFO 180

- IFO 380

- IFO 500

- By Sulphur Compliance

- High Sulphur Fuel Oil (HSFO)

- Low Sulphur Fuel Oil (LSFO)

- Ultra Low Sulphur Fuel Oil (ULSFO) 0.1%

- Distillate Fuel Oil

- Marine Gas Oil (MGO) 0.5% & 0.1%

- Marine Diesel Oil (MDO) 0.5% & 0.1%

- Alternative Fuels

- Liquefied Natural Gas (LNG)

- Biofuels

- Methanol

- Ammonia

- Others

By Vessel Type

- Containers

- Tankers

- General Cargo

- Bulk Carrier

- Fishing Vessels

- Others

By Application

- Commercial Shipping

- Cargo

- Passenger

- Leisure

- Defence & Naval Operations

- Offshore Support Vessels

By Distributor

- Oil Majors

- Large Independent

- Small Independent

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |