Japan Temporary Scaffolding Market: By Model (Independent tobi (own materials + labor), Rental company (owns materials, outsources labor), Rental company (owns materials + in-house labor)); Scale (Small Scale Projects, Mid-to- Large Scale Projects); Region (Kyushu, Tohoku, Hokkaido, Chugoku, Shikoku, Okinawa)—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2035

- Last Updated: 16-Oct-2025 | | Report ID: AA10251543

Market Scenario

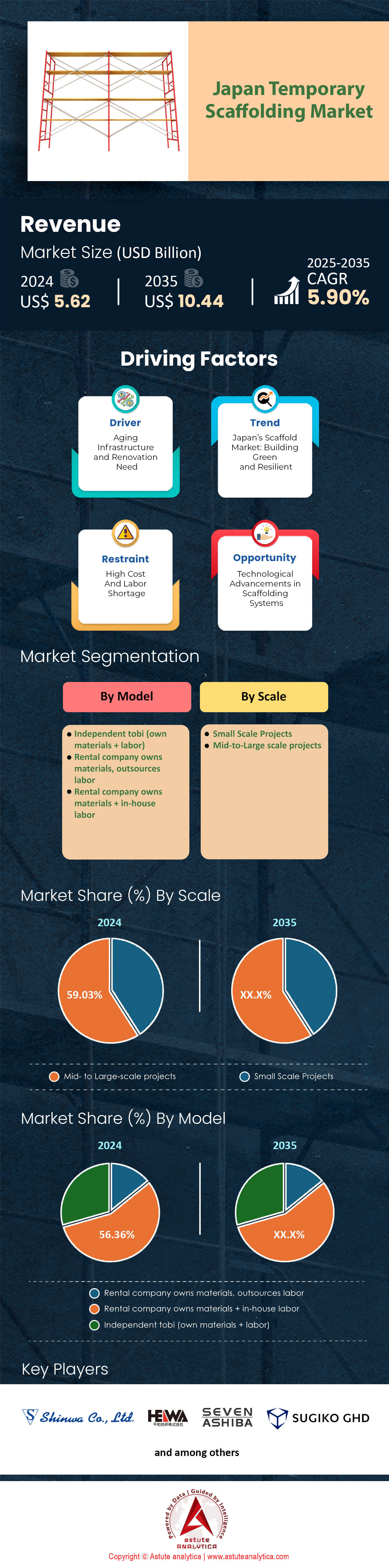

Japan temporary scaffolding market size was valued at US$ 5.62 billion in 2024 and is projected to hit the market valuation of US$ 10.44 billion by 2035 at a CAGR of 5.90% during the forecast period 2025–2035.

A powerful combination of public investment and labor dynamics is fundamentally shaping the Japan temporary scaffolding market. A predictable project pipeline is assured by the government's JPY 20 trillion (USD 137.9 billion) National Resilience Plan and a 6 trillion yen allocation for public works. This capital infusion is funding mega-projects like the Uchisaiwaicho 1-Chome Redevelopment, with its massive 1,100,000m² floor area, and the 85-kilometer Tokyo Outer Ring Road expansion, creating sustained, large-scale demand. These enormous undertakings guarantee a high baseline requirement for scaffolding solutions nationwide.

Simultaneously, the construction sector faces a critical labor crisis influencing purchasing decisions. The industry's workforce shrank by 60,000 people in 2024, now standing at only 4.77 million. An overtime cap of 720 hours per year, effective April 2024, further constrains labor availability. This shortage is underscored by a rise in related bankruptcies, which reached 180 in 2024. Consequently, contractors are increasingly driven to adopt advanced, efficient scaffolding systems that reduce assembly time and manpower requirements.

Demand across the temporary scaffolding market in Japan is also being shaped by specialized construction booms. Amazon's $15.5 billion and Microsoft's $2.9 billion investments in data centers create a lucrative niche for scaffolding providers. Projects like the 16,500m² AirTrunk OSK1 Data Center and the 19,693m² CyrusOne KEP OSK1 facility require sophisticated temporary structures. Furthermore, preparations for Expo 2025, with a total investment of ¥280 billion, create concentrated, time-sensitive demand. A focus on resilience, spurred by events like the 2024 Noto Peninsula earthquake that caused over 240 deaths, will also drive long-term demand for retrofitting and reconstruction projects, solidifying the market's robust future.

To Get more Insights, Request A Free Sample

Unlocking New Revenue Streams in Japan's Evolving Scaffolding Market

- The integration of Building Information Modeling (BIM) with scaffolding design creates a significant service-based opportunity: Companies across temporary scaffolding market can now offer precise digital planning and simulation services. In 2024, Japan's Ministry of Land, Infrastructure, Transport and Tourism (MLIT) mandated BIM for all its public works projects. A move projected to involve over 300 major projects annually. Providing BIM-compatible scaffolding models and consultation can create a new revenue stream. It allows for clash detection and optimized logistics planning before on-site work begins. A service that reduces material waste and assembly time directly addresses industry-wide labor shortages and efficiency goals.

- A growing focus on sustainability and the circular economy is opening a market for eco-friendly scaffolding solutions: In 2025, new government procurement policies will favor suppliers using recycled materials. A policy that includes scaffolding made from high-strength, recycled steel or aluminum alloys. Companies across the Japan temporary scaffolding market offering certified "green" scaffolding with lower carbon footprints can gain a competitive edge. The Tokyo Metropolitan Government's "Zero Emission Tokyo" strategy, updated in 2024, sets specific emissions reduction targets for construction sites. Offering scaffolding systems that contribute to these goals presents a powerful value proposition for contractors bidding on public and private projects.

Renewable Energy Infrastructure Boom Creates Unprecedented Vertical Scaffolding Demand

Japan's accelerated push towards renewable energy is creating a new, specialized, and highly lucrative demand segment for the temporary scaffolding market. The government’s latest Strategic Energy Plan, updated for 2024, targets the installation of 10 gigawatts of offshore wind capacity by 2030. Fulfilling this requires the construction of approximately 800 to 1,000 large-scale offshore wind turbines, each demanding complex scaffolding for assembly and maintenance. In 2025, construction will begin on 3 major offshore wind farms in the Akita and Chiba prefectures. These projects alone will utilize over 200,000 tons of specialized marine-grade steel for their foundations.

Furthermore, the expansion of solar energy contributes to the trend. In 2024, the government approved subsidies for the installation of solar panels on 50,000 public buildings. An initiative that requires extensive scaffolding for safe rooftop access. The development of large-scale solar farms, like the 70-megawatt project in Kagoshima starting in 2025, also needs temporary structures for panel installation and maintenance sheds. Moreover, the country is investing in 5 new large-scale biomass power plants, with construction commencing in 2024 and 2025. Each of these industrial facilities has complex boiler and turbine halls requiring intricate scaffolding solutions, adding another layer of demand to the burgeoning Japan temporary scaffolding market.

Logistics and Warehouse Construction Surge Redefines Scaffolding Market Needs

A revolution in logistics and e-commerce is driving a massive wave of warehouse construction. In 2024, investments in new logistics facilities in Japan temporary scaffolding market are projected to exceed 1 trillion yen. A surge fueled by the need to modernize supply chains. For example, ESR Group is developing a 4-story, 150,000 square meter logistics park near Tokyo, with a completion date in 2025. Prologis is also expanding its footprint with 3 new large-scale distribution centers in the Greater Nagoya area, adding over 300,000 square meters of floor space by the end of 2025.

These modern logistics centers in the temporary scaffolding market are not simple structures; they are multi-story giants. The average height of new warehouses built in 2024 increased to 4 stories. These facilities require extensive and robust scaffolding for their construction, especially for installing high ceilings, advanced sorting systems, and mezzanine levels. In 2025, an estimated 250 new multi-story warehouses will be under construction across the country. The demand for automated retrieval systems within these centers has also led to the construction of over 500 specialized high-rack systems in 2024 alone. Each of these systems requires precise scaffolding for installation. A sustained boom that presents a consistent and high-volume demand driver for the Japan temporary scaffolding market.

Segmental Analysis

Rental and Labor Outsourcing Model Secures Market Leadership

The rental company model, which owns materials and outsources labor, commands a dominant 56.36% of the market as of 2024. This leadership is propelled by significant financial and operational advantages. Companies utilizing rentals can treat scaffolding costs as fully deductible expenses, offering a clear tax benefit over outright purchasing. Furthermore, this model eradicates the need for substantial upfront capital investment and eliminates ongoing costs related to storage and maintenance in the temporary scaffolding market. The operational strain is further eased by a severe construction labor gap, evidenced by a high 5.60 jobs-to-applicants ratio, making the outsourcing of skilled labor a necessity.

This trend is supported by Japan's increasing reliance on foreign labor, with the workforce hitting a record 2.3 million by October 2024, employed by a record 342,000 businesses. Leading rental firms such as SUGIKO, which holds the second-largest industry revenue share, provide immediate access to the latest scaffolding technologies and professional setup services. A national jobs-to-applicants ratio of 1.25 further underscores the tight labor market, reinforcing the efficiency of the rental and outsourcing strategy in the Japan temporary scaffolding market. Consequently, a flexible approach provides the resource management crucial for navigating the complexities of the modern construction landscape.

- Rental providers handle all equipment maintenance and repairs, saving construction firms significant time and operational costs.

- The government's plan to raise the annual recruitment quota for foreign workers to 33,500 will further support the labor outsourcing model.

- Access to specialized and the latest scaffolding systems is available immediately through rental fleets without the high cost of ownership.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Mid to Large-Scale Projects Command Overwhelming Market Share

Mid to large-scale projects consistently capture more than 59.03% of the temporary scaffolding market, driven by massive government investment and ambitious urban redevelopment. The Japanese government has allocated over 6 trillion yen for public works, fueling a pipeline of large-scale endeavors. In Tokyo alone, more than 100 new high-rise buildings are currently planned or under construction, including the 330-meter-tall Mori JP Tower and the expansive Takanawa Gateway City project. These complex structures demand sophisticated and extensive scaffolding solutions that only well-equipped providers can supply.

The preference for advanced systems on major projects is clear, with leading firms like Obayashi Corporation reporting a 30% reduction in assembly times by using modular scaffolding. Furthermore, productivity gains of up to 20% are achieved on large projects that leverage modern scaffolding technology. The upcoming Osaka Expo 2025 and a rapid expansion in data center construction contribute significantly to this segment's dominance within the Japan temporary scaffolding market. The government’s Fundamental Plan for National Resilience also mandates large-scale repairs to aging infrastructure, ensuring a steady stream of major projects for the foreseeable future.

- A majority of Japan's premier construction firms now integrate Building Information Modeling (BIM) software for precise planning of large, complex scaffolding deployments.

- The Uchisaiwaicho 1-Chome Redevelopment in Tokyo is a massive project covering a floor area of 1,100,000 square meters.

- Major national projects like the Chuo Shinkansen maglev line require extensive and specialized scaffolding over long durations.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Kanto Region's Unrivaled Dominance in Scaffolding Demand

The Kanto region, with Tokyo at its core, holds the largest market share at over 37.60% in the temporary scaffolding market and is projected to maintain its top position. Dominance is a direct result of its status as Japan's primary economic and construction hub. Construction costs in Tokyo are among the highest globally, with an average of US$4,467 per square meter, reflecting the high value and complexity of projects undertaken. The sheer volume of activity is immense, with numerous "once-in-a-century" redevelopment projects transforming entire districts like Shibuya, Yaesu, and Toranomon simultaneously.

An intense concentration of high-value construction ensures that scaffolding rental companies experience their peak equipment utilization rates in the Tokyo metropolitan area. To meet demand, major suppliers strategically locate their main product management centers in the Kanto and Kansai regions. The Kanto region also has the highest concentration of the 342,000 businesses that employ foreign labor, a critical component of the construction workforce. The continuous launch of new commercial towers, residential complexes, and infrastructure upgrades solidifies the Kanto region's premier position in the Japan temporary scaffolding market.

- The Tokyo Metropolitan Government has noted a significant rise in the issuance of permits for suspended scaffolding, indicating a high volume of building maintenance and facade work.

- A significant portion of the government's 6 trillion yen public works budget is allocated to projects within the densely populated and economically vital Kanto region.

- The region is home to a dense network of supplier bases, with companies like Sankyo operating 24 directly-managed sites to service the high demand.

Competitive Landscape: Titans of the Trade Dominate Japan's Temporary Scaffolding Market

The competitive landscape of the Japan temporary scaffolding market is highly concentrated, with a few key players commanding significant influence through extensive distribution networks, robust manufacturing capabilities, and strategic growth initiatives. Shinwa Co., Ltd. stands as the undisputed market leader, capturing the largest individual share at an impressive 27.80%. The company leverages its first-class production capability and a strong reputation for its mainstay wedge-binding type scaffolds to maintain its dominant position. For fiscal year 2025, Shinwa forecasts a substantial 35.4% increase in revenue from its scaffolding equipment segment, driven by strategic acquisitions like the YAGUMI Group, a major scaffolding construction operator.

Following Shinwa, Heiwa Giken Co., Ltd. asserts itself as another dominant force in the temporary scaffolding market, recognized as a top brand with a formidable market presence. While specific market share percentages fluctuate, Heiwa's strength lies in its vast product range and brand recognition. The market, though fragmented beyond these leaders, sees significant contributions from other major players like Sankyo Corporation and Sugiko Group. Sankyo has a long history of innovation, including the development of specialized scaffolding cleaning machines and a focus on rental and installation services. The Sugiko Group differentiates itself by integrating digital technology like BIM assistance and VR safety education with its traditional rental services, addressing modern demands for efficiency and safety.

These industry giants continuously reinforce their positions through strategic growth. Shinwa's midterm plan for fiscal years 2025 to 2029 targets a minimum revenue CAGR of 9.5%, signaling aggressive expansion. The competitive environment is characterized by a push towards next-generation scaffolding systems, an emphasis on value-added services like digital integration, and strategic acquisitions to consolidate market power. As construction demand remains robust, the dominance of these key players is expected to continue, shaping the direction of the entire Japan temporary scaffolding market.

Top Players in Japan Temporary Scaffolding Market

- SANKYO Corporation / SEVEN ASHIBA

- KYC Machine Industry

- Shinwa

- Sugiko Group Holdings Co., Ltd .

- Daisan Co. Ltd .

- Heiwa Giken Co., Ltd.

- Other Prominent Players

Market Segmentation Overview

By Model

- Independent tobi (own materials + labor)

- Rental company owns materials, outsources labor

- Rental company owns materials + in-house labor

By Scale

- Small Scale Projects

- Mid- to Large-scale projects

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |