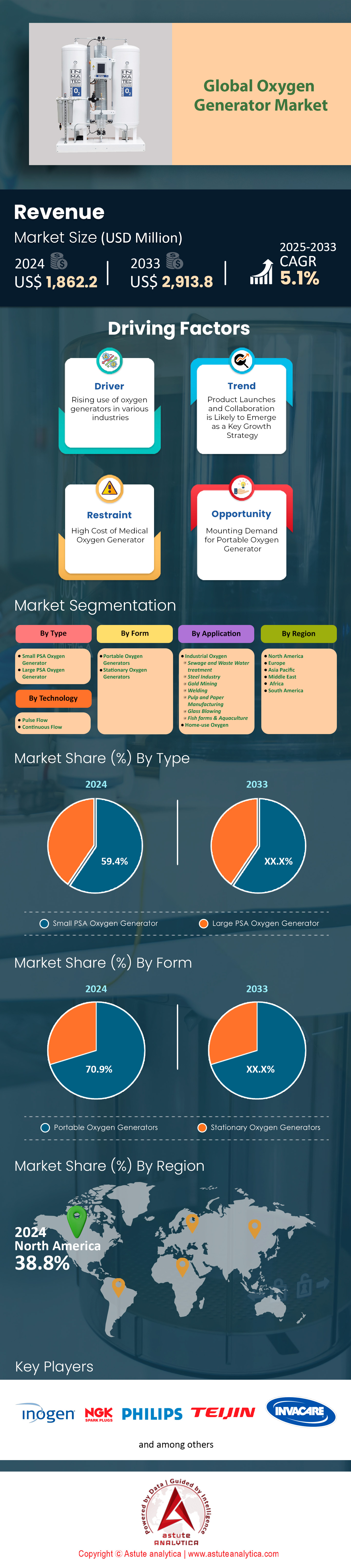

Market Snapshot

Oxygen generator market is estimated to witness a rise in revenue from US$ 1,862.2 million in 2024 to US$ 2,913.8 million by 2033 at a CAGR of 5.1% during the forecast period 2025-2033.

Key Findings

- Based on type, the small PSA oxygen generator takes the lead with over 59.4% market share.

- Based on form, the portable oxygen generators takes the lead with over 70.9% market share.

- In terms of technology, the pulse flow segment contributed the highest revenue (64.8%) to global market in 2024.

- Based on application, home-use to remain at the epicenter.

- North America holds the lion’s share of over 38.9% in the global market.

A structural shift toward home-based healthcare is creating a substantial and predictable demand stream for oxygen generators. The foundation of this demand is a large patient population, exemplified by the over 800,000 U.S. patients on home oxygen therapy in the first quarter of 2025. Consequently, high user engagement, with an average daily portable concentrator wear-time of 7.5 hours in 2024, translates into a need for durable and reliable devices. The oxygen generator market's stability is further reinforced by a 28-month average prescription length for new patients, which ensures a long-term revenue cycle. Moreover, demand for next-generation products is actively being shaped by users; a 2025 survey showed 58 of every 100 patients desire lighter models, driving a robust replacement and upgrade market.

In parallel, industrial sectors are generating significant demand based on clear financial and operational advantages. The rapid return on investment, with a typical payback period for on-site systems ranging from just 18 to 24 months, is a powerful incentive. For instance, a wastewater treatment plant can cut annual energy costs by 20,000 EUR, creating a compelling business case. In heavy industry, steelmakers can reduce coke consumption by 50 kilograms per ton of metal produced, directly impacting profitability. The demand across the oxygen generator market is also emerging from specialized sectors like aquaculture, where on-site oxygen can increase fish stocking density by 100 kilograms per cubic meter. These tangible benefits are fueling major capital investments, evidenced by Chart Industries securing an order for 2 large on-site plants in July 2024.

Future growth in the oxygen generator market is expected to be heavily influenced by technological sophistication and geographic expansion. Evolving consumer preferences are a leading indicator; online searches for "lightweight" models hit a peak interest value of 88 in January 2025, while travel needs drove 40,000 searches for "FAA approved" concentrators in 2024. Furthermore, international markets are becoming major demand centers. India's issuance of tenders for over 5,000 PSA plants in 2024 represents a massive public health investment. Similarly, Brazil's private healthcare sector experienced a 12-fold increase in demand, while Mexico's plan to equip 500 rural clinics in 2025 highlights growing adoption in new regions.

To Get more Insights, Request A Free Sample

Untapped Niche Markets Offer Significant Avenues for Strategic Market Expansion

The oxygen generator market holds promising opportunities in non-traditional sectors ripe for penetration. These emerging niches provide avenues for diversification away from the competitive mainstream medical and industrial fields.

- Veterinary Medicine Integration: A significant growth frontier exists within veterinary care. Advanced veterinary hospitals and clinics are increasingly adopting on-site oxygen generators. They use these systems for critical applications like anesthesia delivery during surgery and life support in intensive care units for small animals. This specialized B2B segment demands robust, smaller-scale systems. It offers a new revenue stream with distinct product requirements and a less saturated competitive landscape for manufacturers to explore.

- The High-Growth Wellness and Biohacking Sector: The burgeoning consumer wellness industry presents another lucrative opportunity for the oxygen generator market. Boutique wellness centers, anti-aging clinics, and athletic training facilities are creating demand for commercial-grade oxygen generators. These are used for offerings like oxygen bars, hyperbaric oxygen therapy (HBOT) for athletic recovery, and high-altitude simulation training. This trend allows manufacturers to tap into a direct-to-business, private-pay market. It is driven by consumer health trends rather than medical necessity, providing a hedge against regulatory changes in healthcare.

Demand Analysis

Hyperbaric Oxygen Therapy Creates Demand for High-Purity Medical Oxygen Systems

A key driver defining the medical oxygen generator market is the expansion of Hyperbaric Oxygen Therapy (HBOT). This specialized medical treatment created significant demand, with 150 new standalone HBOT clinics opening in the US in 2024 alone. The therapy's oxygen requirements are substantial. An average monoplace HBOT session in 2025 consumes 7,000 liters of oxygen, necessitating a reliable on-site supply. The required oxygen purity for these medical-grade chambers is a stringent 99.5%, mandating high-performance generator technology. Growth is supported by a solid clinical foundation, with 14 FDA-approved conditions for HBOT as of 2024.

The infrastructure and professional community around HBOT are also growing in the oxygen generator market. In 2024, 25 new multi-place HBOT chambers were installed in North American hospitals. A new large-scale HBOT center opened in Florida in 2025 with a 12-person capacity chamber. The professional base expanded to over 1,200 credentialed hyperbaric technologists in the U.S. in 2025. With treatment protocols for conditions like diabetic foot ulcers requiring 30 sessions, patient throughput is high. Even with an installation cost for a clinical monoplace chamber reaching US$ 100,000 in 2024 and a private-pay session costing US$ 450 in 2025, the market continues its upward trajectory.

Remote and Hostile Industrial Environments Mandate On-Site Oxygen Generation

Demand in the industrial oxygen generator market is being shaped by the needs of remote and challenging operations, particularly in mining. The logistical impossibility of transporting liquid oxygen to these sites makes on-site generation essential. In 2024, 300 containerized, mobile oxygen plants were deployed to remote mining locations globally. The scale of demand is significant; a gold mine processing 5,000 tons of ore requires 10 tons of on-site oxygen daily for leaching processes, which need an oxygen purity of 93%. The financial incentive is powerful, with cost savings at a remote mine reaching US$ 200,000 annually per plant in 2025.

Technological advancements are meeting these harsh environmental demands. Specialized high-altitude PSA oxygen generators in 2024 now have an operational ceiling of 5,000 meters. The utility of the oxygen generator market extends beyond mineral processing. A single PSA plant can support breathing air for up to 50 miners in a refuge chamber. On-site oxygen is also used to enrich diesel engine intake, reducing fuel consumption by 5 liters per hour. This demand has spurred a support economy, with the average service contract for a remote plant valued at US$ 30,000 per year in 2025. The trend is expanding, with 15 oil and gas platforms in the Gulf of Mexico installing PSA units in 2024, despite a deployment lead time of 20 weeks for custom systems.

Segmental Analysis

On-Site PSA Systems Revolutionize Industrial and Healthcare Oxygen Supply

An in-depth market analysis reveals that the small PSA (Pressure Swing Adsorption) oxygen generator segment is estimated to hold the highest revenue share of the oxygen generator market. This dominance is quantitatively supported by the global installation of over 650,000 PSA units across various sectors by 2024. A significant growth vector is emerging economies, which commissioned over 110,000 new PSA generators in 2023, with South Asia alone accounting for 38,000 of these installations. The healthcare sector remains a primary adopter, with a remarkable 140,000 PSA units installed globally between 2023 and early 2024. Demand is particularly strong for small-scale generators offering 5 to 50 liters per minute, evidenced by the deployment of over 63,000 such units worldwide in 2023. These units are valued for their compact footprint, often occupying less than 2 square meters. The industrial sector is also a key consumer, utilizing over 68,000 PSA generators in 2023. This market expansion is fueled by continuous innovation, with over 50 new PSA models introduced globally in 2023, and further underscored by the filing of over 1,200 patents related to PSA oxygen systems during the same year.

- The strategic allocation of infrastructure budgets by hospitals towards on-site PSA systems signals a long-term commitment to operational self-sufficiency and cost control.

- Intense research and development activity, reflected in the high number of new patents, indicates a highly competitive landscape focused on efficiency and performance enhancements.

- Government-led public health initiatives, such as the deployment of 29,000 healthcare PSA units in India, are creating significant regional market opportunities and setting new standards for medical infrastructure.

This strategic shift towards on-site generation is fundamentally altering the supply chain dynamics within the oxygen generator market. By enabling facilities to produce their own medical-grade oxygen, PSA technology reduces the logistical complexities and recurring costs associated with traditional oxygen cylinders. A prime example is India's National Health Mission, which installed 29,000 PSA units, thereby strengthening the nation's healthcare resilience. This move towards self-sufficiency is critical for providing uninterrupted oxygen supply, especially in remote or underserved areas. The versatility of these systems allows for market penetration into diverse industrial applications, including aquaculture and water treatment, creating new revenue streams. The continuous technological evolution, focusing on improved energy efficiency and intelligent control systems, ensures that small PSA technology will maintain its leading position in the ever-evolving oxygen generator market.

Patient Mobility and Advanced Technology Fuel Portable Oxygen Generator Dominance

The portable oxygen generators segment has captured the major share in the global oxygen generator market, a position achieved by directly addressing patient demand for greater mobility and lifestyle freedom. A key market enabler is the growing number of FAA-approved portable oxygen concentrator models, which facilitates air travel for patients. Manufacturers are competing on critical performance metrics; for instance, advancements in 2024 and 2025 have pushed battery longevity, with models like the CAIRE Freestyle Comfort offering up to 16 hours of operation. Concurrently, device weight has been drastically reduced, with some of the latest 2024 models weighing less than 3 pounds, such as the Inogen Rove 4. Specific product examples illustrate this competitive landscape: the popular Inogen One G5 weighs 4.7 pounds and provides up to 13 hours of battery life, while the CAIRE Freestyle Comfort, at 5 pounds, sets a high bar for endurance. Furthermore, user experience is enhanced through noise reduction, with leading devices operating at a quiet 37 to 39 decibels.

- The competitive dynamic in the portable segment is characterized by a clear trade-off between device weight, oxygen output, and battery duration, creating distinct product categories.

- Regulatory milestones, particularly FAA approvals, function as crucial market access gateways, significantly expanding the addressable market for manufacturers.

- Acoustic performance, measured in decibels, has become a key marketing and differentiation point, directly impacting patient comfort and compliance with therapy.

For patients with higher clinical needs, the market offers robust solutions like the CAIRE SeQual Eclipse 5, which provides both continuous and pulse flow options at a weight of 18.4 pounds, and the Oxlife Independence at 16.7 pounds. The market also includes models like the Inogen Rove 6, weighing 4.8 pounds with over 6 hours of battery life, and the Philips SimplyGo Mini at 5 pounds with up to 9 hours of operation. Another notable device is the GCE Zen-O, which weighs 10.25 pounds and delivers both flow types. This patient-centric product development, focusing on miniaturization and extended battery performance, has been instrumental. The segment's leadership within the oxygen generator market is a direct result of successfully translating technological innovation into tangible improvements in patient quality of life and independence.

Smart Pulse Flow Technology Commands the Oxygen Concentrator Market Share

Within the technology landscape of the oxygen generator market, the pulse flow segment contributes the major share, a leadership position rooted in its superior efficiency and intelligent oxygen delivery. This technology conserves oxygen by delivering it in metered bursts synchronized with patient inhalation, a critical feature for extending the battery life of portable units. The market in 2024 and 2025 is characterized by devices with a wide array of settings; for example, the CAIRE SeQual Eclipse 5 offers nine pulse dose settings, delivering up to 192 ml per pulse. Other leading products like the Inogen One G5 and Rove 6 feature six settings with a maximum output of 1260 ml/min. The Philips Respironics SimplyGo Mini provides five settings up to 1,000 ml/min, while the CAIRE Freestyle Comfort has five settings delivering up to 1050 ml/breath. Even ultra-lightweight models like the Inogen One G4, weighing under 3 pounds, offer three distinct pulse flow settings, demonstrating the scalability of the technology.

- The integration of sensitive breath detection sensors, such as CAIRE's UltraSense technology, represents a key technological differentiator that enhances clinical efficacy and patient comfort.

- Auto-adjusting dosage systems, like the SmartDose Technology in the Drive DevilBiss iGo2, are an emerging trend, signaling a move towards more personalized and responsive respiratory therapy.

- The wide variance in pulse dose settings across models, from three to nine, allows manufacturers to segment the market and target patient populations with different levels of respiratory impairment.

The sophistication of this technology is further exemplified by the Drive DevilBiss iGo2, which features SmartDose Auto-Adjusting Technology to match oxygen delivery to the user's real-time breathing rate. Similarly, the VARON 5L Pulse Flow Portable Oxygen Concentrator VP-2 offers an adjustable pulse flow of 1 to 5 liters. The market also features versatile devices like the O2 Concepts OxLife Liberty with nine settings and the Respironics SimplyGo with six pulse dose options in addition to continuous flow. The Inogen One Rove 4, a newer model, comes with four settings. This focus on precise, adaptable, and efficient oxygen delivery has firmly established pulse flow as the dominant technology, shaping product development and competition across the oxygen generator market.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Home-Use Oxygen Therapy Spearheads Market Expansion and Patient Care

An analytical review confirms the home-use oxygen segment contributed the major share in the global oxygen generator market. A primary driver is the growing global patient population requiring long-term oxygen therapy, which exceeded 15 million individuals in 2024. This trend is reflected in the over 1.2 million new home oxygen concentrator units shipped globally in 2023 alone. The demographic shift towards an aging population, particularly in North America and Europe, has substantially increased prescriptions for at-home oxygen. Consequently, providers are transitioning patients from cumbersome oxygen tanks to more convenient stationary and portable concentrators, with reimbursement policies from entities like Medicare now strongly favoring these modern devices for their long-term cost-effectiveness.

- The rise of telehealth platforms has streamlined the process for prescribing and monitoring home oxygen therapy, boosting patient compliance and segment growth.

- Direct-to-consumer online sales channels have disrupted traditional distribution models, providing patients with greater choice and competitive pricing for home concentrators.

- The "aging-in-place" movement, a strong socioeconomic trend, directly fuels demand as more seniors opt for receiving long-term care within their residences.

The segment's leadership in the oxygen generator market is further cemented by its clear value proposition in modern healthcare. Home-based oxygen therapy significantly improves patient quality of life and is a cost-effective alternative to prolonged hospital stays, a key factor for healthcare payers seeking to reduce expenditures. Devices like the Philips Respironics SimplyGo Mini and the Inogen One series exemplify the innovation that empowers patients, blurring the lines between stationary home care and an active lifestyle. This enhancement of patient autonomy directly supports clinical goals of reducing hospital readmission rates for chronic respiratory conditions, solidifying the home-use segment's foundational importance to the entire oxygen generator market.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America's Advanced Healthcare Infrastructure Powers Its Market Dominance

North America's leadership in the oxygen generator market is anchored by its vast and sophisticated healthcare system. Hospitals are aggressively adopting on-site generation to improve efficiency, with facilities in 2025 reporting savings of US$ 0.45 per 100 cubic feet by replacing delivered liquid oxygen. The long-term care sector represents a massive consumer base, with 250 new assisted living facilities opening in 2024, each a potential site for new oxygen systems. Canada’s market shows similar depth, with over 400 long-term care homes in Ontario alone utilizing on-site generation. Investment is following this strong demand, evidenced by a US$ 50 million expansion of a key production facility in Georgia announced in 2024.

A mature distribution network of over 7,000 durable medical equipment providers in the U.S. oxygen generator market ensures deep market penetration for home oxygen concentrators. The direct-to-consumer channel is booming, with leading manufacturers selling over 60,000 portable units directly to patients in 2024. Government procurement provides a stable demand floor, highlighted by a 2025 Department of Veterans Affairs contract for 5,000 stationary oxygen concentrators. Niche applications for oxygen generators are also expanding rapidly; over 1,500 veterinary hospitals are now equipped with surgical-grade systems. Furthermore, the 2,700 accredited sleep centers across the U.S. represent another key and growing user base.

Asia Pacific Emerges as The Epicenter of Rapid Market Growth

The Asia Pacific oxygen generator market is defined by explosive, dual-engine growth from industrialization and healthcare modernization. On the industrial front, China's steel sector commissioned 25 new large-scale VPSA plants in 2024, creating substantial demand. South Korea's high-tech industry followed suit, with semiconductor fabs contracting for 15 new on-site oxygen systems. The region's burgeoning aquaculture industry is another key driver; Vietnam alone saw the installation of over 1,000 PSA systems in 2025 to increase productivity and yields.

Parallel to industrial demand is a rapid expansion of healthcare infrastructure. India’s national health mission in 2024 initiated projects to equip 800 district hospitals with their own PSA oxygen plants. To meet surging regional needs, Indonesia began the domestic manufacturing of 500 hospital-grade oxygen generator units in 2025. Even mature markets are growing in specialized areas; over 3,000 veterinary clinics in Japan now use medical oxygen generators. Singapore's advanced biotech sector also contributed, with 200 labs upgrading to on-site generation in 2024.

Europe’s Market Matures With a Focus on Efficiency and Niche Verticals

Europe's mature oxygen generator market is driven by system upgrades and a deep-rooted healthcare network. The region’s large geriatric population creates consistent demand, with the United Kingdom's private long-term care sector comprising over 450,000 beds in early 2025. Government-backed efficiency projects are also significant. A 2024 German initiative, for example, supported the upgrade of over 100 municipal wastewater treatment plants with modern oxygenation systems, a core application for industrial generators.

Growth is particularly pronounced in high-value industrial and wellness verticals. Italy’s artisanal glass manufacturing industry saw 50 factories convert to on-site oxygen in 2024 for superior furnace control. France’s aquaculture sector expanded with 70 new land-based fish farms utilizing PSA technology. The wellness trend is another powerful driver, with over 300 high-end clinics across Europe adding hyperbaric oxygen therapy in 2024. Further demand comes from the continent's expanding biotech industry, which required over 2,000 new laboratory-grade oxygen concentrators in 2025.

Strategic Investments and Acquisitions Shape the Competitive Landscape of Oxygen Generator Market

- Chart Industries Deepens Cryogenic Portfolio: In early 2024, Chart Industries completed its acquisition of Howden for US$ 4.4 billion, significantly expanding its portfolio in cryogenic gas handling and compression, essential for large-scale oxygen production and transport.

- Atlas Copco Acquires Compressor Technology: In 2024, Atlas Copco acquired a specialized compressor technology company, strengthening its core component supply chain for its VPSA and PSA oxygen generator product lines.

- Private Equity Buys Major DME Provider: A leading private equity firm completed the buyout of a major US-based durable medical equipment (DME) provider in early 2025, consolidating a key distribution channel for home and portable oxygen concentrators.

- Japanese Conglomerate Invests in Indian Market: A major Japanese conglomerate announced a joint venture in 2024, investing US$ 100 million to build a new manufacturing facility for medical devices in India, including oxygen concentrators.

Top Companies in the Oxygen Generator Market

- Atlas Copco

- AVIC Jianghang

- Beijing Shenlu

- Airsep

- Caire

- DeVilbiss Healthcare

- Drive Medical

- Foshan Kaiya

- GCE Group

- Inmatec

- Inogen

- Inova Labs

- Nidek Medical

- NGK Spark Plug

- Novair Medical

- O2 Concepts

- Oxymat A/S

- Philips Respironics

- Precision Medical

- ResMed

- SeQual Technologies

- Teijin Pharma

- Yuwell

- Other Prominent Players

Market Segmentation Overview

By Type

- Small PSA Oxygen Generator

- Large PSA Oxygen Generator

By Form

- Portable Oxygen Generators

- Stationary Oxygen Generators

By Technology

- Pulse Flow

- Continuous Flow

By Application

- Industrial Oxygen

- Sewage and Waste Water treatment

- Steel Industry

- Gold Mining

- Welding

- Pulp and Paper Manufacturing

- Glass Blowing

- Fish farms & Aquaculture

- Home-use Oxygen

By Region

- North America

- The US

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia and New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 1,862.2 Mn |

| Expected Revenue in 2033 | US$ 2,913.8 Mn |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Mn) |

| CAGR | 5.1% |

| Segments covered | By type, form, technology, applications, and Region |

| Leading players | Atlas Copco, AVIC Jianghang, Beijing Shenlu, Airsep, Caire, DeVilbiss Healthcare, Drive Medical, Foshan Kaiya, GCE Group, Inmatec, Inogen, Inova Labs, Nidek Medical, NGK Spark Plug, Novair Medical, O2 Concepts, Oxymat A/S, Philips Respironics, Precision Medical, ResMed, SeQual Technologies, Teijin Pharma, Yuwell, Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |