Market Snapshot

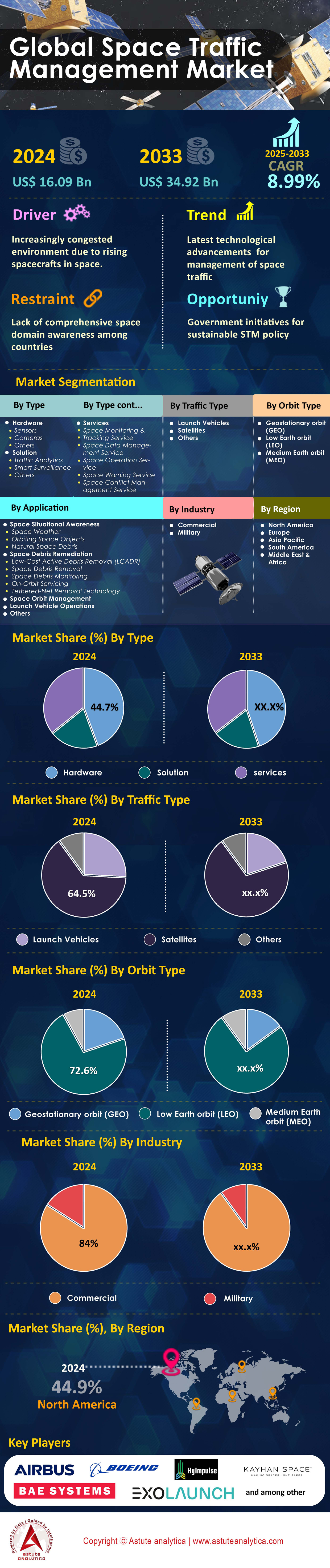

Space traffic management market was valued at US$ 16.09 billion in 2024 and is set to attain valuation of over US$ 34.92 billion by 2033 at a CAGR of 8.99% during the forecast period 2025–2033.

The space traffic management market in 2024 operates through sophisticated radar systems, optical telescopes, and radio frequency sensors tracking over 34,000 orbital objects daily. LeoLabs deployed 12 new phased-array radars across Alaska, Costa Rica, and the Azores, each capable of tracking objects as small as 2 centimeters in low Earth orbit. Ground-based systems from companies like Numerica Corporation process 4 million observations daily, while space-based sensors aboard satellites like Privateer's Pono constellation detect 850 unique conjunction events every 24 hours. These systems feed data to centralized command centers where artificial intelligence algorithms analyze trajectory patterns, with SpaceX's Starlink constellation alone requiring 25,000 automated collision avoidance maneuvers annually.

Commercial satellite operators emerged as primary consumers in space traffic management market, with Amazon's Project Kuiper, OneWeb, and SpaceX collectively managing 8,400 operational satellites requiring continuous monitoring. Government agencies including the U.S. Space Force's 18th Space Defense Squadron process 400 high-interest conjunction warnings daily, while the European Space Agency's Space Debris Office coordinates tracking for 2,800 active payloads. Insurance companies now mandate space traffic management services for all launches exceeding US$ 500 million in value, driving demand from 47 new constellation operators who launched 2,100 satellites through Q3 2024. Universities and research institutions consume tracking data for 175 CubeSat missions monthly, requiring precision orbital determination within 50-meter accuracy thresholds.

Major players in the space traffic management market including Kayhan Space, Slingshot Aerospace, and COMSPOC Corporation expanded operations significantly, with Kayhan Space's Pathfinder platform now autonomously managing flight paths for 1,200 satellites across 15 operators. Lockheed Martin's iSpace command and control system processes 750 gigabytes of sensor data hourly from 27 ground stations worldwide, while Ansys' orbital debris simulation software models 18 million fragment trajectories for mission planning. The Chinese National Space Administration deployed 8 new tracking stations along the Belt and Road corridor, enhancing coverage for 650 Chinese commercial satellites. These developments reflect growing recognition that every kilometer of altitude between 400 and 1,200 kilometers now contains approximately 2,500 trackable objects, necessitating real-time coordination among 92 countries operating space assets.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Twenty-five thousand satellites projected joining orbit by year 2030

The exponential growth trajectory toward 25,000 satellites by 2030 fundamentally transforms space traffic management requirements, with current orbital population standing at 9,800 active satellites as of October 2024. Amazon's Project Kuiper secured 83 launch contracts to deploy 3,236 satellites, while China's GuoWang constellation plans 13,000 satellites across 500 orbital planes. This surge necessitates advanced tracking infrastructure, with LeoLabs expanding from 6 to 19 ground-based radars by 2025, each monitoring 15,000 objects simultaneously. The U.S. Space Surveillance Network now processes 2.4 million observations daily, compared to 600,000 in 2020. Commercial operators including SpaceX perform 1,100 collision avoidance maneuvers monthly for their 5,500 Starlink satellites, requiring automated decision-making systems processing 180 terabytes of orbital data every 24 hours.

The proliferation in the space traffic management market drives unprecedented demand for space traffic management services, with satellite operators spending US$ 4.2 million annually on collision avoidance operations per 1,000 satellites. Astroscale's ELSA-M servicer targets removing 5 defunct satellites annually starting 2026, addressing the 3,400 dead satellites currently orbiting Earth. Insurance premiums for constellation operators now include mandatory STM service subscriptions costing US$ 850,000 per year for fleets exceeding 100 satellites. The European Space Agency allocated 340 million euros for developing automated space traffic coordination systems through 2027. Ground station networks expanded to 847 facilities worldwide, with each station tracking 8,500 objects per pass. This infrastructure investment reflects the reality that every new satellite launch creates 120 additional conjunction assessment events monthly, requiring continuous monitoring and coordination among 147 satellite operators globally.

Trend: Private companies launching dedicated STM service platforms and solutions

Private sector innovation dominates space traffic management market evolution in 2024, with 43 companies offering specialized STM platforms compared to 12 in 2020. Kayhan Space's Pathfinder platform autonomously manages 1,200 satellites across 15 operators, processing 50,000 conjunction data messages daily and recommending 340 collision avoidance maneuvers monthly. Slingshot Aerospace's Beacon system tracks 27,000 objects using machine learning algorithms that predict orbital trajectories 30 days ahead with 50-meter accuracy. COMSPOC Corporation's commercial space operations center monitors 9,000 active payloads, generating 2,500 automated alerts daily for operators. These platforms integrate data from 127 sensors globally, including 34 optical telescopes and 93 radar installations. LeoLabs' subscription service costs operators US$ 180,000 annually for comprehensive tracking of objects larger than 10 centimeters.

The commercialization accelerates through venture capital investments in the space traffic management market totaling US$ 2.3 billion in STM companies during 2024, enabling rapid technology deployment. Privateer Space launched 3 Pono satellites equipped with edge computing capabilities processing 400 gigabytes of imagery daily for real-time debris detection. Neuraspace's AI-powered platform reduces false collision warnings by analyzing 18 million historical conjunction events, saving operators 72 unnecessary maneuvers monthly. ExoAnalytic Solutions expanded its global telescope network to 350 sensors, capturing 4 million observations nightly. These companies serve 185 commercial satellite operators, 27 government agencies, and 42 insurance providers. The shift toward commercial solutions reflects growing recognition that government systems alone cannot manage the 850 new satellites launching quarterly. Platform capabilities now include automated maneuver planning, regulatory compliance reporting, and integration with 23 different ground control systems used by satellite operators worldwide.

Challenge: Satellite operating costs increasing five to ten percent annually

Rising operational expenses fundamentally challenge space traffic management market sustainability, with satellite operators allocating US$ 2.8 million annually for collision avoidance activities per 100 satellites in 2024. Ground station time costs US$ 3,500 per hour for emergency maneuver coordination, while dedicated STM analyst teams require 6 full-time engineers earning US$ 140,000 annually each. Fuel consumption for collision avoidance maneuvers reduces satellite operational lifetime by 3 months per 50 maneuvers executed, translating to US$ 18 million in lost revenue for communication satellites. Insurance premiums increased from US$ 12 million to 19 million annually for mega-constellation operators, directly linked to debris proliferation risks. OneWeb spends US$ 4.1 million yearly on enhanced tracking services for its 634 satellites, while maintaining 24/7 operations centers in London and Virginia costing US$ 8.2 million combined.

The cost escalation forces operators to balance safety requirements against profitability in the space traffic management market, with smaller companies particularly strained. STM software licensing fees reach US$ 450,000 annually for enterprise platforms capable of managing 500-plus satellites. Regulatory compliance costs add US$ 1.2 million yearly, including mandatory reporting to 12 different national space agencies. Data storage for conjunction analysis histories requires 850 terabytes annually, costing US$ 180,000 in cloud infrastructure. Operators now budget US$ 15 million over satellite lifetime for STM-related expenses, compared to US$ 4 million in 2019. The financial pressure drives consolidation, with 8 small satellite operators merging operations in 2024 to share STM costs. This trend threatens market diversity, as only companies operating 200-plus satellites achieve economies of scale in STM operations, potentially limiting new entrants and innovation in the commercial space sector.

Segmental Analysis

By Component

The hardware segment, commanding 44.7% market share in space traffic management market, encompasses sophisticated tracking infrastructure with LeoLabs deploying 19 phased-array radars globally by 2024, each costing US$ 12 million to construct. These installations track objects as small as 2 centimeters, processing 400,000 observations daily per radar facility. Optical telescope networks expanded to 350 units worldwide, with ExoAnalytic Solutions operating 175 sensors across 30 countries. Ground station antennas increased to 847 facilities, each requiring US$ 3.5 million in annual maintenance. The segment experiences rapid technological advancement with next-generation sensors incorporating artificial intelligence processors capable of real-time object classification.

Software solutions revolutionize space traffic management operations, with platforms like Kayhan Space's Pathfinder managing 1,200 satellites autonomously. These systems process 50,000 conjunction data messages daily, utilizing machine learning algorithms trained on 18 million historical events. COMSPOC's commercial operations center software analyzes 2.4 million observations every 24 hours, generating 2,500 automated alerts. Services encompass comprehensive monitoring packages costing operators US$ 180,000 to US$ 450,000 annually, depending on fleet size. The projected 8.3% CAGR reflects growing demand for integrated solutions, with 43 companies now offering specialized STM platforms compared to 12 in 2020, serving 185 commercial operators globally.

By Orbit Type

Low Earth orbit's 72.6% market dominance in space traffic management market intensified by 2024, with 6,000 tons of debris concentrated between 400 and 1,200 kilometers altitude. This region hosts 7,500 active satellites, requiring 25,000 automated collision avoidance maneuvers annually. The U.S. Space Surveillance Network tracks 27,000 objects larger than 10 centimeters in LEO, processing 2.4 million observations daily. Mega-constellations operate primarily in LEO, with Starlink satellites at 550 kilometers, OneWeb at 1,200 kilometers, and Amazon Kuiper planned for 590-630 kilometers. Each orbital shell requires dedicated tracking resources, with ground stations performing 8,500 object observations per pass.

Geostationary orbit maintains 565 active satellites in 2024, each occupying specific longitude slots requiring precise station-keeping in the space traffic management market. MEO hosts navigation constellations including 31 GPS satellites, 24 GLONASS satellites, and 30 Galileo satellites, demanding centimeter-level position accuracy. Debris mitigation efforts focus on LEO, where Astroscale's ELSA-M servicer targets removing 5 defunct satellites annually starting 2026. The 6,000 tons of LEO debris translate to 34,000 trackable objects, with collision risk assessments performed every 8 hours for operational satellites. Space agencies mandate end-of-life disposal plans, requiring satellites to deorbit within 25 years, driving demand for enhanced tracking services.

By Application

Space situational awareness commanded the highest application segment share in space traffic management market, with operators investing US$ 2.8 million annually per 100 satellites for comprehensive SSA services. The orbiting space object tracking sub-segment processes 4 million observations nightly through optical telescope networks. LeoLabs' subscription services provide conjunction alerts with 30-day advance warning, enabling operators to plan fuel-efficient avoidance maneuvers. Real-time tracking systems monitor 27,000 cataloged objects, generating 400 high-interest warnings daily for satellite operators. SSA platforms integrate data from 127 sensors globally, providing position accuracy within 50 meters for active satellites.

Space debris remediation emerges as a critical application, with 8 active debris removal missions planned through 2026. Launch vehicle operations require coordinating with 92 countries operating space assets, processing 750 gigabytes of trajectory data hourly. Space orbit management systems autonomously calculate optimal paths for 1,200 commercial satellites, reducing fuel consumption by planning efficient station-keeping maneuvers. Insurance companies mandate SSA services for policies exceeding US$ 500 million, driving adoption across 47 new constellation operators in 2024. The application landscape expands with cislunar space monitoring, as 12 missions target lunar vicinity operations by 2026, requiring new tracking capabilities beyond traditional Earth orbit.

By Industry

Commercial operators dominated space traffic management market with 84.0% market share in 2024, reflecting space commercialization's acceleration with 185 private companies operating satellites in 2024. SpaceX, Amazon, OneWeb, and emerging constellation operators collectively manage 8,400 commercial satellites, spending US$ 4.2 million annually per 1,000 satellites on STM services. Private launch providers conducted 198 of 223 total orbital launches in 2023, coordinating trajectories through commercial STM platforms. Venture capital invested US$ 2.3 billion in STM companies during 2024, enabling 43 private firms to offer specialized tracking services. Commercial insurance providers mandate continuous monitoring for 1,750 insured satellites valued at US$ 875 billion collectively.

Military agencies operate 1,200 dedicated defense satellites across 18 nations, with the U.S. Space Force's 18th Space Defense Squadron processing 400 high-priority conjunction warnings daily. Military STM requirements include tracking 850 classified satellites, monitoring adversary spacecraft activities, and protecting 340 critical national security assets. Defense budgets allocate US$ 4.7 billion globally for space situational awareness capabilities, supporting 27 military space operations centers. The commercial-military interface strengthens through dual-use technologies, with military agencies purchasing data from commercial SSA providers for US$ 180 million annually. This public-private partnership model enables comprehensive space domain awareness while leveraging commercial innovation and infrastructure investments.

By Traffic Type

Satellites dominated with 64.84% market share in space traffic management market, reflecting the 9,800 active satellites currently orbiting Earth as of 2024. SpaceX alone operates 5,500 Starlink satellites, performing 1,100 collision avoidance maneuvers monthly. Amazon's Project Kuiper secured 83 launch contracts to deploy 3,236 satellites through 2029, while China's GuoWang constellation plans 13,000 satellites across 500 orbital planes. The anticipated 25,000 satellites by 2030 drives unprecedented tracking requirements, with each satellite generating 120 conjunction assessment events monthly. Launch vehicle tracking intensified with 223 orbital launches in 2023, creating 1,890 upper stages requiring continuous monitoring.

The Russian ASAT test's 2,000 debris fragments continue posing risks in space traffic management market, with tracking systems detecting 850 high-risk conjunctions involving these fragments quarterly. Launch vehicles contribute significantly to congestion, with 3,400 defunct rocket bodies orbiting Earth, each tracked continuously by ground stations. Commercial launch providers including SpaceX, Blue Origin, and Rocket Lab coordinate 47 launches quarterly, requiring precise trajectory planning to avoid existing debris fields. The segment's growth reflects increasing launch frequency, with 2024 averaging 18 orbital launches monthly compared to 8 in 2021. Space agencies worldwide allocate 340 million euros collectively for enhanced tracking capabilities addressing this multi-faceted traffic challenge.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America Dominates Global Space Traffic Management Market Through Advanced Infrastructure

North America's leadership in the space traffic management market stems from operating 4,200 active satellites and maintaining 312 ground tracking stations across the continent. The region processes 1.8 million space object observations daily through facilities including the Space Surveillance Network's 28 sensors and LeoLabs' 7 phased-array radars. Commercial operators headquartered in North America manage 3,500 satellites, with SpaceX alone conducting 1,100 collision avoidance maneuvers monthly. The region hosts 23 dedicated STM companies offering services to 147 global satellite operators, generating US$ 8.7 billion in annual revenue.

Investment in STM infrastructure across the global space traffic management market reached US$ 1.9 billion in 2024, supporting development of next-generation tracking systems. NORAD's Cheyenne Mountain operations center coordinates with 43 civilian facilities, sharing 50,000 conjunction warnings annually. Canadian Space Agency operates 4 tracking stations contributing 120,000 observations daily to the continental network. Mexico's emerging space program added 2 ground stations in 2024, enhancing coverage for 89 satellites traversing North American airspace. The region's 847 space technology companies drive innovation in automated collision avoidance systems.

United States Leads Through Military and Commercial Space Traffic Coordination

The United States operates 2,800 active satellites in the space traffic management market, requiring continuous monitoring by 18th Space Defense Squadron's 24/7 operations center processing 400 high-priority conjunction assessments daily. U.S. Space Force maintains 19 dedicated tracking facilities, including powerful radars at Kwajalein Atoll capable of detecting 2-centimeter objects at 1,000 kilometers altitude. Commercial entities like LeoLabs, Slingshot Aerospace, and COMSPOC Corporation serve 112 international customers from U.S. headquarters, processing 2.4 million observations every 24 hours. The nation's 156 licensed launch sites conducted 108 orbital missions in 2023.

Federal investment totaling US$ 4.2 billion supports STM infrastructure development through 2027 in the space traffic management market, including upgrading Space Fence radar capabilities. American universities operate 234 CubeSats requiring precision tracking within 50-meter accuracy. Insurance companies based in the U.S. cover 1,200 satellites valued at US$ 600 billion, mandating comprehensive STM services. The Commercial Space Operations Center in Colorado Springs coordinates activities for 89 satellite operators globally. U.S.-developed STM software platforms manage 6,500 satellites worldwide, demonstrating technological leadership through AI-powered collision prediction algorithms processing 180 terabytes of orbital data daily.

Europe Advances Space Traffic Management Through Multinational Collaboration and Innovation

Europe tracks 2,100 active satellites through 67 ground stations distributed across 22 member nations in the space traffic management market, with ESA's Space Debris Office coordinating observations from Darmstadt, Germany. The continent invested 340 million euros in automated space traffic coordination systems, supporting 31 European satellite operators managing 1,450 spacecraft. French space agency CNES operates 8 tracking telescopes generating 280,000 observations nightly, while Germany's TIRA radar detects objects smaller than 5 centimeters. European STM companies including GMV, Neuraspace, and Iceye serve 73 commercial operators globally, pioneering AI-driven collision avoidance technologies.

The European Union Space Surveillance and Tracking consortium combines resources from 7 nations, maintaining continuous coverage of 11,000 space objects. Italy's BIRALES radar system monitors 1,200 objects simultaneously, contributing 150,000 daily measurements. UK Space Agency's 5 tracking facilities support OneWeb's 634-satellite constellation operations from London. European insurers covering 450 satellites worth 225 billion euros require quarterly STM compliance reports. The region's 18 spaceports planned through 2026 integrate STM considerations from design phase, establishing Europe as a regulatory leader.

Asia Pacific Rapidly Expands Space Traffic Management Capabilities Across Region

Asia Pacific space traffic management market operate 1,700 active satellites, with China managing 650 commercial spacecraft through 8 new tracking stations along the Belt and Road corridor. Japan's space agency JAXA maintains 6 optical telescopes and 3 radar facilities tracking 8,500 objects, sharing 200,000 observations daily with international partners. India's NETRA system monitors 1,500 satellites from Bengaluru, supporting ISRO's 42 active missions. Australia's space industry expanded to 117 companies in 2024, with Electro Optic Systems operating 12 tracking sensors across the continent generating 350,000 nightly observations.

Regional cooperation in the regional space traffic management market strengthened through the Asia-Pacific Space Cooperation Organization, coordinating STM activities among 12 member nations. South Korea's 4 tracking facilities support 28 domestic satellites, investing US$ 890 million in enhanced capabilities through 2027. Singapore emerged as a regional STM hub, hosting 8 international operators managing 234 satellites. New Zealand's Rocket Lab conducted 19 launches in 2023, demonstrating regional launch capabilities. The region's combined tracking network processes 1.1 million observations daily, supporting safe operations for 3,200 satellites regularly transiting Asia Pacific airspace.

List of Key Companies Profiled:

- Airbus Group

- BAE Systems plc

- Boeing Company

- Exolaunch

- HyImpulse Technologies

- Kayhan Space Corp.

- L3Harris Technologies, Inc.

- Lockheed Martin

- Northrop Grumman

- Raytheon Technologies

- Saab AB

- Thales Group

- The Aerospace Corporation

- Other Prominent Players

Market Segmentation Overview

By Component

- Hardware

- Sensors

- Cameras

- Others

- Solution

- Traffic Analytics

- Smart Surveillance

- Others

- Services

- Space Monitoring & Tracking Service

- Space Data Management Service

- Space Operation Service

- Space Warning Service

- Space Conflict Management Service

By Traffic Type

- Launch Vehicles

- Satellites

- Others

By Orbit Type

- Geostationary orbit (GEO)

- Low Earth orbit (LEO)

- Medium Earth orbit (MEO)

By Application

- Space Situational Awareness

- Space Weather

- Orbiting Space Objects

- Natural Space Debris

- Space Debris Remediation

- Low-Cost Active Debris Removal (LCADR)

- Space Debris Removal

- Space Debris Monitoring

- On-Orbit Servicing

- Tethered-Net Removal Technology

- Space Orbit Management

- Launch Vehicle Operations

- Others

By Industry

- Commercial

- Military

By Region

- North America

- Europe

- Asia Pacific

- Middle East

- Saudi Arabia

- Iran

- Israel

- Jordan

- Iraq

- Kuwait

- Qatar

- UAE

- Turkey

- Rest of Middle East

- South America

- North Africa

- Algeria

- Egypt

- Libya

- Morocco

- Rest of North Africa

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 16.09 Billion |

| Expected Revenue in 2033 | US$ 34.92 Billion |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Bn) |

| CAGR | 8.99% |

| Segments covered | By Component, By Traffic Type, By Orbit Type, By Application, By Industry, By Region |

| Key Companies | Airbus Group, BAE Systems plc, Boeing Company, Exolaunch, HyImpulse Technologies, Kayhan Space Corp., L3Harris Technologies, Inc., Lockheed Martin, Northrop Grumman, Raytheon Technologies, Saab AB, Thales Group, The Aerospace Corporation, Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |