Market Scenario

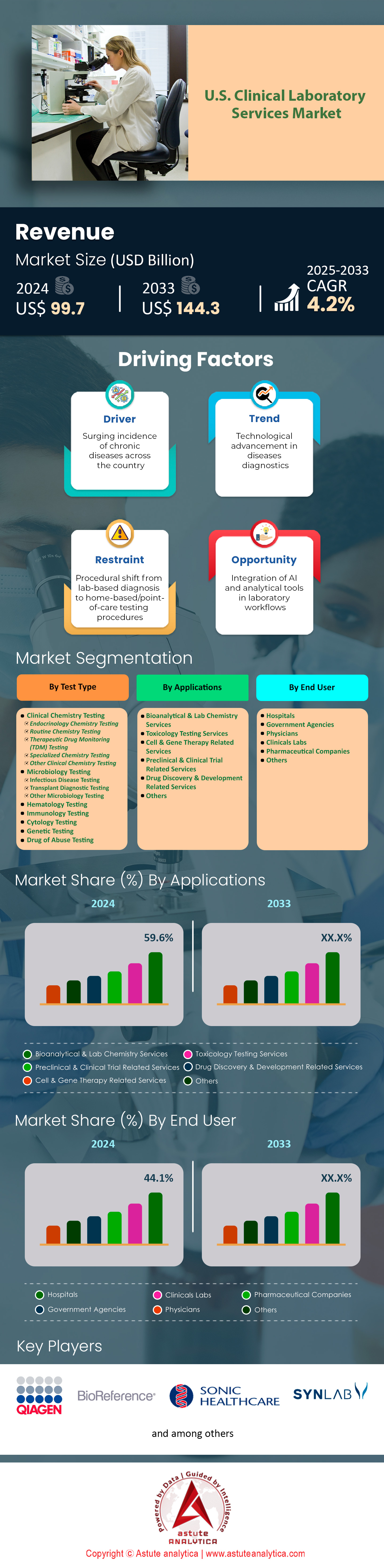

U.S. clinical laboratory services market was valued at US$ 99.7 billion in 2024 and is projected to hit the market valuation of US$ 144.3 billion by 2033 at a CAGR of 4.2% during the forecast period 2025–2033.

The US clinical laboratory services market is experiencing unprecedented transformation in 2024, driven by the integration of artificial intelligence and molecular diagnostics across major laboratory networks. Quest Diagnostics has deployed AI-powered diagnostic algorithms across 2,300 patient service centers, reducing turnaround times from 48 hours to 12 hours for complex genetic panels. Laboratory Corporation of America (LabCorp) invested US$ 450 million in automated specimen processing systems, enabling their facilities to handle 175,000 additional tests daily. The consolidation wave continues as regional laboratories merge to achieve economies of scale, with Sonic Healthcare acquiring 18 independent laboratories for US$ 1.2 billion, creating a network serving 42 million patients annually. Point-of-care testing expansion has led to the installation of 85,000 new diagnostic devices in urgent care centers and retail clinics, shifting routine testing away from centralized facilities.

Digital pathology adoption in the U.S. clinical laboratory services market accelerated dramatically as PathAI's platform now processes 2.5 million tissue samples monthly across 150 hospital systems, while Proscia's cloud-based solution analyzes 800,000 slides daily for cancer detection. The workforce dynamics shifted significantly with laboratories hiring 35,000 molecular technologists and bioinformaticians to support advanced genomic testing capabilities. Reimbursement pressures intensified as Medicare implemented new fee schedules affecting 4,200 diagnostic codes, prompting laboratories to optimize test utilization through AI-driven ordering systems. The US clinical laboratory services market witnessed the launch of 120 new liquid biopsy tests for early cancer detection, with Guardant Health processing 450,000 samples quarterly through their automated facilities in California and North Carolina.

Supply chain resilience became paramount in the U.S. clinical laboratory services market as laboratories stockpiled US$ 2.8 billion worth of critical reagents and consumables following global disruptions. Major players like BioReference Laboratories established 12 new regional distribution centers, ensuring 24-hour delivery capabilities to 8,500 healthcare facilities. The integration of laboratory information systems with electronic health records reached new heights, with Epic and Cerner platforms now seamlessly connected to 3,200 laboratory facilities, facilitating real-time result reporting for 180 million patients. The US market continues evolving through strategic partnerships, as evidenced by Mayo Clinic Laboratories collaborating with 45 health systems to provide specialized testing services, processing 22 million tests annually through their reference laboratory network.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Growing aging population increasing demand for diagnostic laboratory testing services

The demographic shift toward an aging population is fundamentally reshaping the U.S. clinical laboratory services market in 2024, with 73 million Americans now aged 65 and older requiring frequent diagnostic monitoring. Medicare beneficiaries generate an average of 14 laboratory tests annually, compared to 4 tests for individuals under 40, creating unprecedented testing volumes across major laboratory networks. Quest Diagnostics reported processing 89 million tests for Medicare patients in 2024, while LabCorp handled 76 million geriatric-specific panels including comprehensive metabolic profiles and cardiac biomarkers. The concentration of elderly populations in states like Florida and Arizona has prompted laboratory companies to establish 45 new patient service centers specifically designed for senior accessibility, featuring extended hours and specialized phlebotomy teams trained in geriatric care.

This demographic pressure intensifies as chronic disease management requires continuous laboratory monitoring, with diabetic patients alone generating 52 million HbA1c tests annually through the U.S. clinical laboratory services market infrastructure. Major health systems like Kaiser Permanente have responded by integrating 2,800 point-of-care testing devices in senior living facilities, enabling on-site diagnostic capabilities for 450,000 residents. The economic impact reaches US$ 18.5 billion in annual Medicare laboratory spending, prompting innovative service delivery models including mobile phlebotomy units that collected 12 million samples from homebound seniors in 2024. Specialized geriatric testing panels now comprise 38 million annual orders, encompassing vitamin D assessments, thyroid function tests, and cognitive biomarkers specifically tailored for aging populations requiring regular health monitoring.

Trend: Automation transforming pre analytical and post analytical laboratory workflow processes

Advanced robotics revolutionized specimen handling across the U.S. clinical laboratory services market in 2024, with Siemens Healthineers' Atellica systems processing 95 million tubes through 120 integrated laboratory networks nationwide. Pre-analytical automation investments focused on artificial intelligence-powered sample sorting, where machine vision systems identify 48 different tube types and route specimens to appropriate analyzers at speeds of 3,600 samples hourly. Massachusetts General Hospital's implementation of total laboratory automation reduced specimen processing time from 180 minutes to 45 minutes, handling 28,000 daily samples through interconnected track systems spanning 12,000 square feet. Automated aliquoting stations now prepare 65 million daughter tubes annually, eliminating manual pipetting errors and preserving primary specimens for additional testing requirements. These technological advances enabled laboratories to process 4.2 million COVID-19 surveillance samples monthly while maintaining routine testing operations.

Post-analytical automation transformed result management within the U.S. clinical laboratory services market through sophisticated middleware platforms connecting 8,500 instruments across 2,100 facilities nationwide. Auto-verification algorithms now release 142 million results directly to electronic health records without manual review, utilizing 850 customizable rules per test type. Stanford Health Care's laboratory automated critical value notification system contacts 18,000 providers daily through integrated communication platforms, reducing response time from 35 minutes to 8 minutes. Digital image analysis for urinalysis microscopy examines 75 million specimens annually, with artificial intelligence identifying cellular elements and bacteria in 2.8 million samples daily. Investment in post-analytical automation reached US$ 3.8 billion as laboratories deployed advanced analytics platforms monitoring quality metrics across 450 million annual test results.

Challenge: Severe laboratory workforce shortage causing operational disruptions and testing delays

Critical staffing deficits plague the U.S. clinical laboratory services market throughout 2024, forcing 2,400 hospitals to operate laboratories at reduced capacity while managing 185 million annual test requests. The shortage spans all specialties, with histotechnology facing 6,800 vacant positions nationally, causing surgical pathology backlogs affecting 4.2 million cancer diagnoses annually. Blood banks report 3,500 unfilled positions, jeopardizing transfusion services for 1.8 million surgical procedures and trauma cases requiring immediate blood product availability. Commercial laboratories increased recruitment spending to US$ 850 million, implementing international hiring programs that brought 4,200 foreign-trained technologists through visa sponsorship initiatives. Regional laboratory networks consolidated operations, closing 380 smaller facilities and centralizing testing in 85 mega-laboratories processing 500,000 daily specimens to maximize limited workforce efficiency.

Educational institutions struggle to expand training capacity within the U.S. clinical laboratory services market infrastructure, with only 142 accredited programs graduating 4,800 new professionals annually against industry demand for 15,000 entry-level positions. Hospital laboratories report 28 million delayed non-urgent test results as skeleton crews prioritize emergency and inpatient testing, creating backlogs worth US$ 6.4 billion in deferred revenue. Traveling laboratory professionals command premium rates of US$ 3,500 weekly, with agencies placing 12,000 temporary workers across facilities experiencing acute shortages. The workforce crisis forced innovation in service delivery models, with 850 hospitals implementing cross-training programs enabling 35,000 nurses and respiratory therapists to perform waived testing. Major health systems allocated US$ 2.1 billion toward retention bonuses, tuition reimbursement, and career ladder programs attempting to stabilize their laboratory workforce amid unprecedented turnover rates.

Segmental Analysis

By Test Type

Clinical chemistry testing commands 35.70% market share of the clinical laboratory services market due to its fundamental role in routine health assessments and disease monitoring, with laboratories nationwide performing 1.4 billion chemistry panels annually. These tests form the cornerstone of preventive medicine, with comprehensive metabolic panels alone accounting for 485 million orders yearly, followed by 380 million lipid profiles and 295 million liver function tests. Every hospital admission requires baseline chemistry testing, generating 180 million test orders from 36 million annual hospitalizations. The ubiquitous nature of chemistry testing spans all healthcare settings, from 225,000 primary care offices ordering basic metabolic panels for annual physicals to emergency departments running 145 million stat chemistry tests for critical care decisions. The U.S. clinical laboratory services market benefits from chemistry testing's broad clinical utility, diagnosing conditions ranging from diabetes to kidney disease through standardized, automated platforms. The dominance stems from technological advantages enabling high-volume processing, with modern chemistry analyzers handling 10,000 tests hourly at costs under US$ 2 per test. Major laboratories invested US$ 4.8 billion in chemistry automation, with facilities like Quest Diagnostics' Clifton laboratory processing 8 million chemistry tests monthly through integrated track systems. Clinical chemistry serves as the gateway for disease detection, with 65 million Americans receiving diabetes diagnoses through glucose testing and 48 million identified with chronic kidney disease via creatinine measurements. The US market infrastructure supports chemistry testing through 8,500 automated analyzers installed nationwide, operated by 45,000 certified technologists maintaining continuous operations across 4,200 hospital laboratories and 2,800 independent facilities.

By End Users

Hospitals maintain their position as dominant end users with 44.10% market share in the U.S. clinical laboratory services market due to their comprehensive testing requirements spanning emergency, inpatient, and outpatient services. These 6,090 facilities generate 2.8 billion annual laboratory tests supporting 36 million admissions, 145 million emergency department visits, and 485 million outpatient encounters. Hospital laboratories operate 24/7 capabilities processing 450 million stat tests with turnaround times under 60 minutes, critical for emergency medical decisions. Major health systems like HCA Healthcare invested US$ 3.2 billion in laboratory infrastructure, establishing 185 core laboratories serving their 180-hospital network processing 285 million tests annually.

The hospital dominance reflects integrated care delivery models requiring immediate access to diagnostic results within the U.S. clinical laboratory services market ecosystem. Academic medical centers alone account for 680 million complex tests including 125 million molecular diagnostics, 95 million flow cytometry analyses, and 85 million specialized coagulation studies supporting tertiary care services. Hospital laboratories employ 285,000 professionals operating sophisticated instrumentation worth US$ 18.5 billion, enabling on-site testing capabilities from routine chemistry to advanced genomic sequencing. Strategic advantages include seamless electronic health record integration facilitating real-time clinical decision support, direct specimen collection from 2.4 million hospital beds, and quality assurance programs maintaining accreditation standards across 4,800 hospital laboratory facilities nationwide.

By Application

Bioanalytical and lab chemistry services command an impressive 59.6% market share in the U.S. clinical laboratory services market, driven by their fundamental role in routine health assessments and chronic disease management. This dominance originates from the universal requirement for chemistry panels in virtually every clinical encounter, with laboratories performing 850 million comprehensive metabolic panels, 620 million lipid profiles, and 480 million glucose tests annually. The integration of advanced mass spectrometry platforms enabled 3,200 laboratories to expand therapeutic drug monitoring services, processing 125 million tests for medication optimization. Clinical chemistry automation reached unprecedented levels with 1,850 facilities operating integrated analyzer systems producing 50,000 results hourly.

The demand surge reflects multiple factors including preventive care initiatives requiring 380 million annual wellness panels and chronic disease monitoring necessitating 295 million diabetes-related tests within the U.S. clinical laboratory services market framework. Primary end users encompass 225,000 primary care physicians ordering chemistry tests for 165 million patients, specialty clinics managing 85 million chronic disease patients requiring quarterly monitoring, and 7,500 dialysis centers performing 145 million renal function assessments. Corporate wellness programs drive 65 million employee health screenings annually, while insurance requirements mandate 185 million pre-enrollment chemistry panels, solidifying bioanalytical services as the cornerstone of modern healthcare delivery.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Competitive Landscape

The competitive landscape remains highly consolidated with two giants, Laboratory Corporation of America (LabCorp) and Quest Diagnostics, collectively processing 1.2 billion tests annually through their combined network of 4,500 patient service centers and 85 specialized laboratories. These industry leaders invest US$ 2.8 billion yearly in technology upgrades and geographic expansion, maintaining competitive advantages through economies of scale. Regional players including Sonic Healthcare, BioReference Laboratories, and Mayo Clinic Laboratories compete by specializing in complex testing portfolios, with Sonic operating 45 facilities processing 185 million tests annually. The U.S. clinical laboratory services market witnesses intense competition in hospital outreach programs, where independent laboratories vie for exclusive contracts worth US$ 12.5 billion across 3,200 health systems nationwide.

Competitive strategies focus on vertical integration and digital transformation, with LabCorp acquiring 28 specialty testing companies for US$ 4.6 billion since 2022, expanding capabilities in oncology and rare disease diagnostics. Quest Diagnostics invested US$ 850 million in consumer-initiated testing platforms, capturing 35 million direct-to-consumer orders annually through retail partnerships with Walmart and CVS Health. Emerging competitors like Labcorp Drug Development leverage clinical trial testing expertise, managing 2,800 studies generating US$ 3.2 billion revenue. The U.S. clinical laboratory services market experiences disruption from technology companies, with Amazon entering through acquisition of One Medical's laboratory operations, while Walgreens expanded VillageMD clinics to include 185 on-site laboratories, intensifying competition for routine testing volumes.

Top Companies in the U.S. Clinical Laboratory Services Market

- Qiagen Inc.

- Opko Health, Inc.

- Abbott Laboratories

- Charles River Laboratories

- Johnson & Johnson

- Roche Laboratories

- Pfizer Inc

- Eli Lilly

- Novartis Laboratories

- Merck Inc.

- Astrazeneca

- Arup Laboratories

- Davita, Inc.

- Siemens Healthcare Limited

- Viapath Group Llp

- Almac Group

- Neogenomics Laborateries

- Eurofins Scientific

- UNILABS, SYNLAB International GmbH

- H.U. Groups Holdings, Inc.

- Sonic Healthcare

- ACM Global Laboratories

- Amedes Holding GmbH

- BioReference Laboratories, Inc.

- Other Prominent Players

Market Segmentation Overview

By Test Type

- Clinical Chemistry Testing

- Endocrinology Chemistry Testing

- Routine Chemistry Testing

- Therapeutic Drug Monitoring (TDM) Testing

- Specialized Chemistry Testing

- Other Clinical Chemistry Testing

- Microbiology Testing

- Infectious Disease Testing

- Transplant Diagnostic Testing

- Other Microbiology Testing

- Hematology Testing

- Immunology Testing

- Cytology Testing

- Genetic Testing

- Drug of Abuse Testing

By Application

- Bioanalytical & Lab Chemistry Services

- Toxicology Testing Services

- Cell & Gene Therapy Related Services

- Preclinical & Clinical Trial Related Services

- Drug Discovery & Development Related Services

- Others

By End User

- Hospitals

- Government Agencies

- Physicians

- Clinicals Labs

- Pharmaceutical Companies

- Others

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 99.7 Billion |

| Expected Revenue in 2033 | US$ 144.3 Billion |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Bn) |

| CAGR | 4.2% |

| Segments covered | By Test Type, By Application, By End-User |

| Key Companies | Qiagen Inc., Opko Health, Inc., Abbott Laboratories, Charles River Laboratories, Johnson & Johnson, Roche Laboratories, Pfizer Inc, Eli Lilly, Novartis Laboratories, Merck Inc., Astrazeneca, Arup Laboratories, Davita, Inc., Siemens Healthcare Limited, Viapath Group Llp, Almac Group, Neogenomics Laborateries, Eurofins Scientific, UNILABS, SYNLAB International GmbH, H.U. Groups Holdings, Inc., Sonic Healthcare, ACM Global Laboratories, Amedes Holding GmbH, BioReference Laboratories, Inc., Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |