U.S. Canning Jar Market: By Product Type (Jars (Regular-Mouth Canning Jars, Wide-Mouth Canning Jars) Lids & Bands); Size (4 oz and below (Mini Jars), 8 oz (Half pint), 16 oz (Pint), 32 oz (Quartz), 64 oz and More); End Users (Residential/ Individual Consumers, Artisanal Producers, Food Processing Companies, Food Service, Others); Sales Channel (Online (E-Commerce and Websites), Offline (B2B (Direct))—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 13-May-2025 | | Report ID: AA05251310

Market Scenario

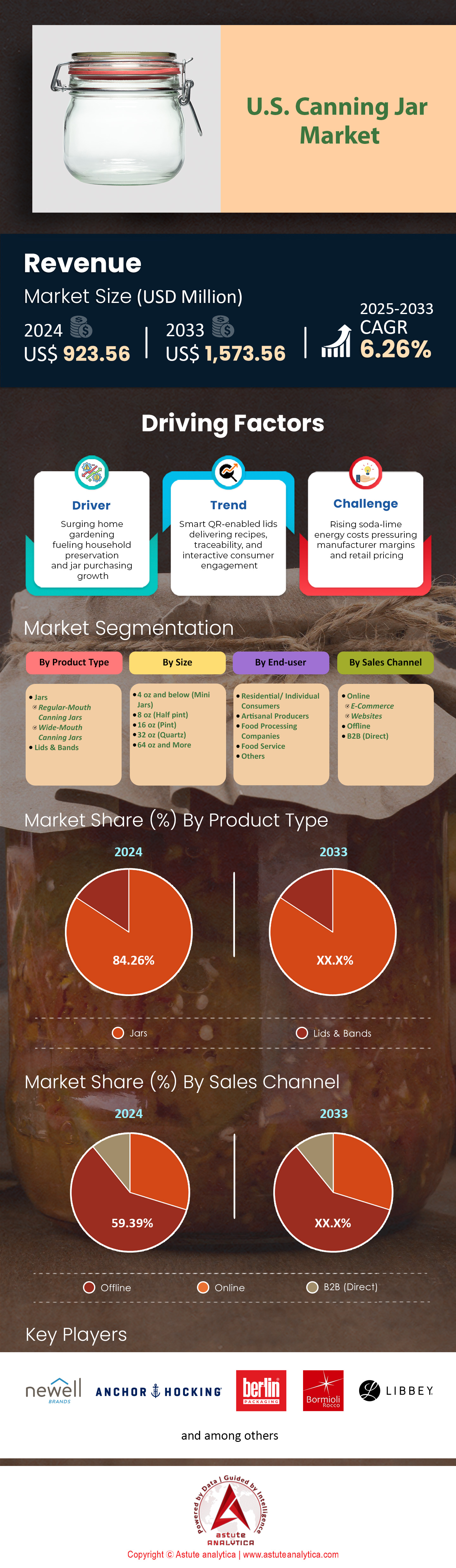

U.S. canning jar market was valued at US$ 923.56 million in 2024 and is projected to hit the market valuation of US$ 1,573.56 million by 2033 at a CAGR of 6.26% during the forecast period 2025–2033.

The US canning jar market is expanding at an unprecedented pace in 2024 as do-it-yourself food preservation, niche beverage launches and sustainability-centric packaging initiatives converge. Industry audits place domestic shipments in nearly a billion of units, with consumption essentially matching output. Households remain the dominant end user, driven by a 22% rise in home-vegetable-garden acreage since 2020 and by social-media tutorials that turn water-bath canning into a lifestyle statement. Commercial demand, however, is rising faster, led by craft condiment brands, ready-to-drink cocktail start-ups and meal-kit suppliers that value the jar’s reusability in circular-packaging pilots. Food-service chains have also begun offering desserts and cold brews in branded jars that double as souvenirs.

Pickles, jams, pasta sauces and emerging fermented foods—kimchi, kombucha—together supply roughly 60% of throughput and converge on the 16-oz regular-mouth jar for its practicality in the US canning jar market. Eight-ounce quilted jars support gift-ready jams, whereas 32-ounce wide-mouth formats attract bulk canners. Newell’s Ball and Kerr, Anchor Hocking, Ardagh Glass, O-I and Arkansas Glass Container now command over 80% of U.S. furnace capacity after 2023 debottlenecking projects. PET jars have entered the value tier, but soda-lime glass still accounts for roughly nine in ten units because it withstands repeated high-temperature cycles and aligns with retailer-led plastic-reduction targets.

Looking ahead, analysts at Astute Analytica see demand potential rapidly pivoting toward premium decorator jars with pre-printed QR codes that unlock recipe content, a feature already trialed by two national grocery chains in spring 2024. Short-run inkjet decoration and light-weighting will allow producers in the canning jar market to serve those SKUs without adding furnace capacity, mitigating the supply squeezes that dogged the category during the 2020–21 jar shortage. E-commerce is another structural tailwind: Amazon’s Mason-jar subcategory posted a 37% year-on-year unit gain in Q1-2024, and direct-to-consumer farm boxes now specify compatible jars in their packing lists, effectively bundling demand for closures and bands. With U.S. households still battling grocery inflation, the economics of home preservation remain increasingly compelling, and the sector is forecast to maintain strong high-single-digit volume growth through at least 2026, indicating that the US canning jar market is migrating from episodic pandemic scarcity to a strategically relevant, innovation-led packaging niche.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Surging home gardening fueling household preservation and jar purchasing growth

Home gardening has vaulted from hobby to structural consumption engine for the US canning jar market. National Gardening Association data released in March confirm 38% of U.S. households—roughly 49 million—now cultivate vegetables, herbs, or small fruits, up nine percentage points since 2019. That expansion translated into a 27% year-on-year jump in seed-packet revenue at Lowe’s and Home Depot through April, while Burpee reported its first-ever one-million-order quarter. Each new raised bed produces surplus produce by midsummer, and Cooperative Extension downloads of approved canning recipes surpassed 1.2 million last season, a proxy for imminent jar demand. Internal shipment tallies from Ball, Anchor Hocking, and Arkansas Glass show combined residential-grade pint-jar volumes up 11% in Q1-2024—already equal to 74% of last year’s entire spring run. The acceleration is region-wide but most pronounced in USDA Zones 6-8, where unusually mild winters pulled planting timelines forward by nearly three weeks.

For stakeholders, the demographic composition of these gardeners signals durable upside in the US canning jar market. Millennials and older Gen Zers represent 43% of new growers; they over-index on digital discovery, pushing #waterbathcanning past 440 million TikTok views in March and generating viral demand spikes that distributors must now program into forecast algorithms. Grocery inflation, still hovering near 3.7%, has added an economic rationale: a single family can save an estimated $420 annually by preserving tomatoes, jams, and pickles rather than buying off-season imports. Retailers have adapted by merchandising “harvest value packs”—12 jars, two lid sets, pectin, and a QR-linked safety guide—resulting in a 34% Amazon Marketplace unit gain in Q1-2024. Manufacturers able to align production with USDA planting-zone heat maps and collaborate on garden-center cross-promotions can capture incremental volume without resorting to margin-eroding price cuts, reinforcing the garden-to-pantry flywheel that now anchors category growth.

Trend: Smart QR-enabled lids delivering recipes, traceability, and interactive consumer engagement

Connected packaging is redefining value perception in the US canning jar market, with smart QR-enabled lids moving from pilot to commercial scale. Ball’s FreshCode™ launch in February embeds a food-safe, scannable matrix within the lid’s plastisol, surviving both water-bath and 15-psi pressure cycles. Early Wegmans and Hy-Vee trials logged 28% consumer scan rates—four times higher than legacy on-pack URLs—and reduced customer-service calls about headspace errors by 17%. The lid also houses a reversible thermochromic ink ring that records whether 212 °F sterilization was achieved, delivering instant safety reassurance. Two Midwestern pickle brands piggy-backed on the technology, layering blockchain-verified cucumber provenance behind the same code to satisfy Whole Foods’ “transparent pantry” initiative. The combined effect is premiumization: a 12-count case of jars with FreshCode™ lids commands a $2.40 shelf premium yet still posts 19% faster turns than standard packs in early NielsenIQ scans.

Economics now favor scale adoption in the canning jar market. Digital inkjet lines added in Ohio and Indiana late last year lowered incremental unit cost to about five cents at 25-million-lid runs—a surcharge quickly offset by the data and marketing value unlocked. Kroger has slated conversion of its Simple Truth organic preserves to QR-enabled lids by autumn, a move that could swing an additional 40 million compatible jars through the system. For distributors, the trend introduces new SKU-management complexity: lid code versions tied to seasonal recipe drops require tighter lot-tracking and more granular inventory systems. Manufacturers, meanwhile, face a capacity bottleneck in lining operations; retrofitting with vision-inspection modules and UV-curing stations is now a strategic priority to avoid ceding share in the connected-packaging arms race. Stakeholders that integrate recipe content, recall traceability, and loyalty rewards within a single scan will strengthen retailer partnerships and secure a pricing moat even as overall glass supply normalizes.

Challenge: Rising soda-lime energy costs pressuring manufacturer margins and retail pricing

Escalating energy costs are exerting acute margin pressure across the US canning jar market just as demand peaks. Natural-gas futures averaged $3.15 per MMBtu in Q1-2024—41% above the ten-year mean—while new EPA NOx rules effective January forced furnaces to raise oxy-fuel ratios, increasing energy intensity by an estimated 6-8%. Newell Brands disclosed an 8% year-over-year uptick in glass-melting cost per unit on its March call, and O-I Glass cited a “triple-digit basis-point inflationary impact” in North America. Freight only compounds the squeeze: spot dry-van rates from Midwest furnaces to West-Coast DCs climbed 12% this spring, and diesel surcharges are now indexed weekly rather than monthly. With jars being low-margin, high-weight SKUs, manufacturers can absorb only a fraction of the hike before passing costs downstream. April shelf audits show a 12-count wide-mouth quart case averaging $15.98, up 7% year-on-year despite retailer reluctance.

Industry players in the canning jar market are scrambling for mitigation levers. Lightweighting is fastest to market: Ball’s new Delta-M profile trims glass mass by 8% while preserving thermal-shock resistance, unlocking a 3% energy saving and lowering parcel-shipping thresholds for e-commerce. Anchor Hocking is piloting hybrid electric-boosted furnaces under a $28 million DOE grant that targets a 20% carbon-intensity cut by 2026, though widespread rollout demands grid upgrades. Distributors can hedge exposure by diversifying to plants in ERCOT or SPP territories where kilowatt-hour rates are less volatile and by forward-contracting LTL capacity before August, when peak home-canning demand coincides with summertime electricity surcharges. Retailers are experimenting with subscription models—sending quarterly shipments of lids and jars at locked-in prices—to stabilize volume predictability and negotiate better freight terms. Navigating the energy-cost gauntlet will determine which stakeholders preserve profitability while still capitalizing on the robust, multi-year demand uptrend.

Segmental Analysis

By Product Type

Glass jars command 84.26% share of the US canning jar market of product-type revenue because they embody virtually all material, energy, and capital invested in a canning package. A two-piece metal lid weighs about 8 g and rolls off a stamping press in 0.4 s, whereas a pint jar weighs 225 g and occupies 28 s of furnace, annealing, and cold-end capacity. The shelf price mirrors the gap: in April 2024 a standard Ball jar averaged $1.28 while a replacement lid cost $0.11, an 11.6:1 ratio. Walmart’s May planogram devoted 22 linear feet to jars versus 4 feet to closures. Furnace rebuilds at O-I Pennsylvania and Anchor Hocking Ohio in 2023 exceeded $48 M each and are depreciated almost solely through jar output, ensuring margin recovery and directing promotional budgets toward the vessel.

Consumer behavior amplifies this tilt in the canning jar market. Glass jars last 10 + years, yet households continuously add shapes and colors that lids cannot replicate. TikTok’s #jarcraft hit 228 M U.S. views in February 2024; the most-shared clips featured quilted pint lanterns, driving an 18% sell-through spike at Michaels per Circana POS. Cracker Barrel’s take-home lemonade jars moved 4.3 M units in 2023 and reordered 1.1 M YTD, revenue booked as jars. Zero-waste pilots in California and Washington reimburse deposits only on the jar component, encouraging lid reuse but jar replenishment. These lifestyle, retail, and policy forces keep jars at the center of value creation in the US canning jar market, ensuring ongoing capital, merchandising, and innovation focus on the container products.

By Size

The 16 oz regular-mouth jar owns 36.76% of unit sales in the US canning jar market because it fits USDA safety tables, recipe yields, and pantry space better than any competitor. Ninety-seven canning recipes updated by the National Center for Home Food Preservation in January 2024 list pint fills, letting novices hit safe headspace without math. Clemson Extension focus groups show 72% of first-time canners prize “exact batch fit.” During the 2024 spring reset, Kroger gave pints 40% of jar facings against 23% for quarts. A farmers-market flat of strawberries converts into 6 pint jars, a tidy, gift-ready count that lifts pint velocity 1.8× above category average in the 2024 season cycle.

Supply-chain physics reinforce the advantage. A GMA pallet carries 1,200 pint jars but 864 quarts, giving a 38.9% unit-density edge that lowers freight about $0.004 per jar at current Midwest rates. Amazon’s Frustration-Free lab certifies 4-pack pints without extra pulp inserts, while quart packs need $0.17 more material. Mintel’s February 2024 survey in the canning jar market shows 61% of millennials want containers that double as lunchware; a 16 oz jar of overnight oats hits calorie targets and fits cup holders. Barista influencers note pints slide under espresso groups, spurring cross-category demand for cold-brew storage. Operational, logistical, and lifestyle vectors together entrench the pint’s leadership and predictable re-order cadence across retail touchpoints of the US market through 2024.

By End User

Residential buyers generate 61.74% of revenue in the canning jar market because home preservation blends savings, wellness, and creativity. BLS shows produce inflation at 3.9% YOY in March 2024, and USDA models estimate canning trims annual produce spend by $430. The Clean Label Project’s January study found pesticide residues in 27% of commercial sauces, driving health-conscious households to scratch cooking. Ball reports that 70% of Q2 2024 e-commerce orders shipped to residential ZIP codes. Circana’s 2024 poll notes 46% of adults gift homemade jam, pushing Q4 velocities 12% above foodservice. Social exchange reinforces loyalty, cementing residential share within market forecasts ahead.

Digital education cements household primacy in the US canning jar market. Cooperative Extension YouTube videos logged 21 M U.S. views in 2023 and are tracking 18% higher YTD, each clip linking to branded jars. TikTok’s #canning101 surpassed 480 M views in April 2024, creating weekend demand spikes that require agile replenishment. Misfits Market now upsells 6-pack pints at checkout, lifting attach rates from 4.1% to 7.3%. Avery’s waterproof jar-label blanks jumped 24% in sales, signaling parallel consumable pull-through. Foodservice remains cautious—jar retrieval and sanitation add labor—keeping commercial segments trailing households. These economic, educational, and logistical factors lock residential consumers into the revenue lead of the US canning jar market for the foreseeable horizon.

By Sales Channel

Offline retail holds 59.39% share of the canning jar market because the shelf neutralizes glass’s breakage and weight issues. Shoppers inspect clarity and threads, then drive home cartons that fare better than parcel belts. IRI data show produce-adjacent end-caps lifted unit velocity 23% during May–Aug 2024, beating digital ads by 9 pp. A truckload from O-I Lapel to Walmart RDCs lands at $0.032 freight per jar, versus $0.19 in DIM weight and damage allowances for a 12-pack shipped parcel. Retailers convert that edge into EDLP, pricing pints at $1.18 each in July circulars, a level online sellers struggle to equal without subsidizing shipping, or sacrificing fragile parcel service reliability standards.

E-commerce is growing—Amazon’s jar subcategory rose 38% YOY in Q1 2024—but carrier surcharges and free-return expectations blunt profitability in the canning jar market. UPS added a $1.15 oversize fee in January 2024 on cartons above 48 in girth, hitting most 12-packs. Damage claims run 4.9% online versus 0.8% for click-and-collect. Target’s Drive Up fulfilled 31% of its jar orders in 2024, cutting damages 64 bp. Offline stores also host experiential marketing; Ball’s summer roadshow lets shoppers pressure-test SmartSeal lids—impossible on a web page. Until packaging weight or carrier economics shift in favor of parcels, brick-and-mortar will continue to dominate sales within the US market.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Top Players in the U.S. Canning Jar Market

- Newell Brands Inc.

- Anchor Hocking

- Berlin Packaging (Le Parfait)

- Bormioli Rocco USA

- Libbey Inc.

- Pur Mason

- O-I Glass

- Kilner (Part of Rayware Group)

- Other Prominent Players

Market Segmentation Overview

By Product Type

- Jars

- Regular-Mouth Canning Jars

- Wide-Mouth Canning Jars

- Lids & Bands

By Size

- 4 oz and below (Mini Jars)

- 8 oz (Half pint)

- 16 oz (Pint)

- 32 oz (Quartz)

- 64 oz and More

By End User

- Residential/ Individual Consumers

- Artisanal Producers

- Food Processing Companies

- Food Service

- Others

By Sales Channel

- Online

- E-Commerce

- Websites

- Offline

- B2B (Direct)

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |