Utility Poles Market: By Type (Transmission Poles, Distribution Poles, Light Poles); Material Type (Wooden Utility Poles, Steel Utility Poles,[ Stepped poles (ISTPs), Swaged poles (ISWPs)], Concrete Utility Poles, Fiber Reinforced Polymer (FRP) Composites); Pole Size (Below 40ft, Between 40 & 70ft, Above 70ft); Application (Energy Transmission & Distribution, Telecommunication, Street Lighting, Heavy Power Lines, Sub Transmission Lines, Others); Region— Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 03-Nov-2025 | | Report ID: AA0523444

Market Snapshot

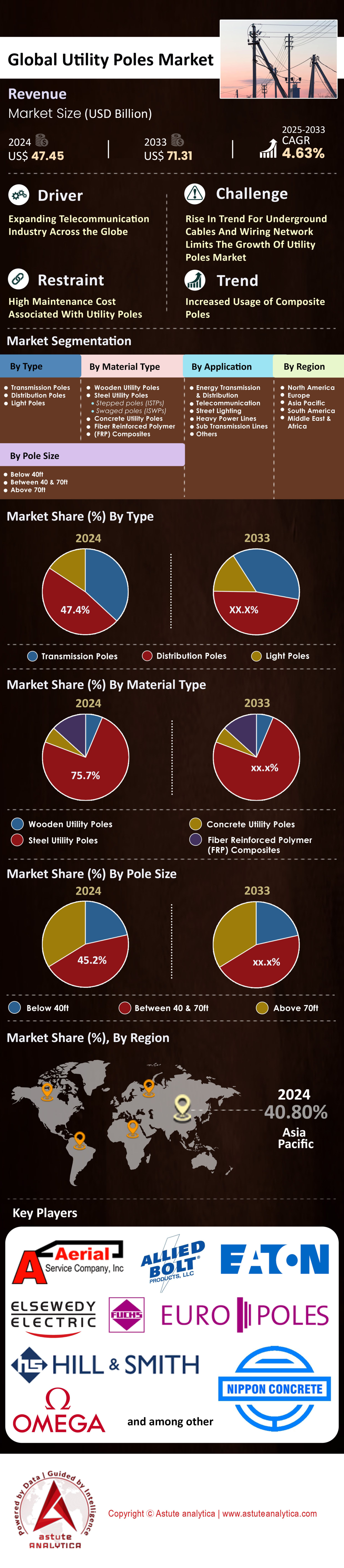

Utility poles market size was pegged at US$ 47.45 billion in 2024 and is projected to reach a valuation of US$ 71.31 billion by 2033, exhibiting a CAGR of 4.63% during the forecast period from 2025 to 2033.

Key Findings

- Based on type, power distribution poles generated over 47.4% revenue in the global utility poles market.

- Based on material type, steel is the dominant material used in the production of utility poles and the material accounted for over 74.4% market share.

- Based on size, the demand for utility poles between 40 and 70 feet in height are more dominant with 44.7% market share than other size.

- When it comes to application, utility poles are heavily deployed for energy transmission and distribution. This application represented more than 79.4% market share in terms of revenue.

- Asia Pacific to remain the key contributor to the global market thanks to rapid infrastructural growth in China and India.

An unprecedented wave of capital expenditure is fundamentally reshaping demand within the utility poles market. Stakeholders should note the sheer scale of grid modernization investments, such as the projected US$ 1.4 trillion planned by U.S. utilities between 2025 and 2030. Immediate demand is underscored by nearly US$ 208 billion in planned U.S. grid upgrades for 2024 alone. This trend is global, evidenced by Europe's EUR 584 billion electricity-infrastructure plan and China's 2024 grid budget, which surpassed 600 billion yuan. Furthermore, climate resilience is a key driver, with the U.S. GRIP Program allocating US$ 7.6 billion across 105 projects as of 2024, directly fueling the need for durable pole infrastructure.

The green energy transition and widespread electrification are creating powerful, long-term demand channels for the utility poles market. The integration of renewables requires massive infrastructure build-outs, exemplified by Dominion Energy Virginia's 2024 plan for approximately 12,000 megawatts (MW) of new solar capacity. Supporting this shift, a U.S. Department of Energy investment of US$ 2.2 billion announced in August 2024 is set to add nearly 13 gigawatts (GW) of grid capacity. Simultaneously, the electric vehicle boom creates immense new load requirements. China added an astounding 4,222,000 EV charging points in 2024, while the U.S. deployed over 40,000 new non-home chargers during the same year, each installation expanding the distribution network.

For industry players in the utility poles market, these drivers translate into robust and geographically diverse project pipelines. The global 5G rollout, with estimated infrastructure investments reaching up to US$ 650 billion by 2025, creates parallel demand for poles to support new fiber and hardware. The U.S. cellular industry's investment of over US$ 10.8 billion in 2024 on network capacity is a strong indicator of this activity. The health of the market is reflected in the order books of major contractors like KEC International, which saw its year-to-date order intake reach approximately ₹14,000 crores as of October 2025. The anticipated creation of at least 5,000 jobs from a single US$ 2.2 billion U.S. grid investment further signals the large scale of deployment shaping near-term market dynamics.

To Get more Insights, Request A Free Sample

Unlocking New Revenue Streams and Enhancing Community Value Through Pole Innovation

- A significant opportunity is emerging from the transformation of standard poles into smart, multi-functional assets: Specifically, the global smart pole market is forecast to involve the installation of over 2.8 million units by 2025. These intelligent structures in the utility poles market can seamlessly integrate 5G small cells, LED lighting, public Wi-Fi, and security cameras. A key driver, for instance, is the need for dense 5G networks; operators are expected to deploy over 6.5 million 5G small cells globally by 2025, with many being pole-mounted. Furthermore, these poles can host Level 2 EV chargers, thereby tapping into the growing electric vehicle market and creating new revenue streams.

- Another major opportunity lies in developing circular economy models for pole lifecycle management: With millions of aging wood poles being decommissioned annually, for example, a growing market for recycling and repurposing is taking shape. Advanced chemical extraction can now recover valuable preservatives from treated wood, significantly reducing environmental impact. In addition, decommissioned composite and steel poles have high recyclability rates. Consequently, companies that develop efficient, scalable solutions for collecting and remarketing these materials can capture a new value segment. A single large utility might decommission over 50,000 poles in a single year, representing a substantial material stream.

Strategic Undergrounding Initiatives are Reshaping Grid Infrastructure Investment Priorities in Utility Poles Market

A growing movement toward undergrounding power lines is creating a distinct demand dynamic within the utility poles market. Increasingly, utilities are investing in burying electrical infrastructure to enhance resilience and improve aesthetics. In California, for instance, a major utility announced plans in 2024 to underground 1,000 miles of power lines, with a projected total program cost of US$ 20 billion to bury 10,000 miles over the next decade. Similarly, a utility in Florida has a storm protection plan that includes burying approximately 1,300 miles of overhead lines by 2025. The cost of these projects is substantial, often estimated at US$ 3 million per mile for distribution lines.

Ultimately, these initiatives represent a long-term shift away from overhead infrastructure in targeted areas. Underscoring this trend, a 2024 federal grant allocated US$ 50 million to a single undergrounding project in Oregon to mitigate wildfire risk. Furthermore, one Midwest utility plans to invest US$ 1.1 billion through 2025 to move more than 400 miles of lines underground. A project in North Carolina is likewise set to bury 15 miles of transmission lines at a cost of US$ 150 million in the utility poles market. Notably, even smaller-scale projects have significant budgets; a community in Arizona approved a US$ 48 million plan in 2024 to bury power lines along a 4-mile corridor, while a US$ 25 million pilot program in Virginia is converting 5 miles of lines. Finally, a municipal utility in Colorado is undertaking a 20-year project to underground 300 miles of its system.

Supply Chain Pressures and Material Costs Define Market Availability and Pricing

Critical supply chain dynamics are heavily influencing the utility poles market by defining lead times and project costs. The price of hot-rolled coil steel, for example, a key component for steel poles, fluctuated significantly in 2024, at times exceeding US$ 800 per short ton. In addition, lead times for some specialized composite transmission poles extended to over 52 weeks in 2024 due to high demand and manufacturing constraints. Meanwhile, the cost of pentachlorophenol, a major wood preservative, saw a price increase of over US$ 0.15 per pound in early 2025. As a result, one major North American wood pole producer reported a backlog of over 300,000 poles entering 2025.

These factors consequently create a challenging procurement environment for utilities and contractors in the utility poles market. Specifically, freight costs for delivering poles also rose, with some routes seeing surcharges increase by US$ 500 per truckload in 2024. In response to these pressures, a key fiberglass supplier for composite poles announced a US$ 40 million investment to expand its manufacturing capacity by 20,000 tons annually, aiming to alleviate bottlenecks by late 2025. At the same time, a major steel pole fabricator reported running its facilities at 95% capacity throughout 2024. Exacerbating the issue, a transportation bottleneck at a major U.S. port in 2024 delayed a shipment of 5,000 imported steel poles for over 6 weeks. Ultimately for buyers, one utility reported a cost variance of US$ 1,200 per pole on a large 2025 order due to material price escalations, while the cost to galvanize a standard steel distribution pole also increased to over US$ 350 in 2024.

Segmental Analysis

Distribution Poles Fueling Growth Through Last-Mile Network Expansion

Power distribution poles command a 47.4% share of global utility poles market revenue, reflecting their essential role in delivering electricity to end users. The scale of this segment continues to expand, with utilities’ spending on distribution networks rising by 160% between 2003 and 2023. Looking forward, the Utilities for Net Zero Alliance (UNEZA) has pledged $117 billion annually toward grid projects, dedicating a major portion to distribution infrastructure. Storm events repeatedly underline the need for replacements, as one U.S. utility sought $228 million for damage caused by 25 storms in 2024, while another spent nearly $450 million after a derecho destroyed thousands of poles.

Such recurring costs highlight the vital importance of resilient and abundant distribution poles that keep millions connected. The demand outlook for the utility poles market is immense, as utilities plan to add or refurbish nearly 80 million kilometers of grids by 2040. For instance, one U.S. utility projected $1.2 billion in hurricane season expenses during 2024, reinforcing the need for structurally strong infrastructure. Further accelerating this demand, the Bipartisan Infrastructure Law allocated $65 billion to grid modernization and broadband expansion, supporting over 350,000 new pole installations in rural regions. These projects form the backbone of last-mile connectivity that sustains the market. Between 2025 and 2030, U.S. utilities alone are set to invest an estimated $1.4 trillion in new infrastructure. Despite the massive scale, a standard 40-foot wooden distribution pole typically costs under $1,000, emphasizing the segment’s high-volume nature.

- The U.S. government allocated $1.5 billion in public funding for four major electricity transmission and distribution projects in October 2024.

- Rural electrification programs in developing regions are a primary driver, necessitating massive new pole installations.

- CenterPoint Energy mobilized over 7,700 personnel to repair equipment after a May 2024 storm, highlighting the scale of restoration efforts.

Steel's Unmatched Durability and Resilience Cement Its Market Dominance

Steel retains its leadership position in the utility poles market, commanding 74.4% of the global share due to its proven strength, longevity, and low lifecycle costs. Galvanized steel poles can operate effectively for more than 60 years, substantially outperforming wood poles, which typically last between 25 and 50 years. Their structural integrity is exceptional, with models engineered to withstand wind speeds of up to 180 mph. This capability is critical in wildfire-prone regions where steel’s non-combustible nature provides a vital safety margin, as it retains most of its load-bearing strength until temperatures exceed 932°F (500°C).

Financially, steel poles also present strong advantages. While their upfront cost is higher than timber, they require significantly less maintenance, avoiding issues like rot, insect damage, or warping in the utility poles market. For instance, one cooperative reduced project costs by $50,000 on a 225-pole line by opting for steel. Further, a 40-foot steel distribution pole is up to 30% lighter—and in some cases even 70% lighter—than a comparable wooden pole, lowering transportation and installation expenses. Their recyclability and capacity for high recycled content also align with sustainability objectives. Ductile iron versions add to their appeal, as they can bear more than 6,500 pounds of load even after severe fire exposure, more than double standard design requirements.

- Hot-dip galvanized steel structures are designed to last over a century with minimal maintenance.

- Unlike wood, steel poles provide uniform structural performance without vulnerabilities to cracking or knots.

- When struck by a vehicle, a steel pole will typically bend rather than shear, keeping energized lines elevated.

The 40-70 Foot Pole The Versatile Backbone of Modern Utilities

Poles between 40 and 70 feet in height form the versatile core of the utility poles market, capturing 44.7% of total share. Their popularity arises from the balance they offer between cost, performance, and adaptability. Commonly used for medium-voltage distribution, telecommunications, and fiber networks, this size class provides ample ground clearance for power lines while supporting additional attachments. In 2023 alone, more than 700,000 poles within this size range were installed globally, compared with about 50,000 taller poles above 70 feet typically used for high-voltage transmission.

Demand within this segment continues to grow. Over the past five years, global installations of 40–70-foot poles increased by around 15%, driven by rapid electrification and urban network expansion. Furthermore, installations within this range for renewable integration—especially solar and wind infrastructure—have surged 20% over the last decade. Regulatory design standards in the utility poles market reinforce this trend; the National Electrical Safety Code (NESC) identifies 60 feet as a critical height threshold for wind-loading performance. As a result, utilities prefer poles in this range as dependable, cost-efficient, and safety-compliant assets.

- This size range is the backbone of power delivery, offering a compromise between height for clearance and cost-effectiveness.

- It is ideal for supporting heavier cable loads required in suburban and industrial areas.

- The vast majority of pole infrastructure for electricity consists of distribution lines supported by poles in this category.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Energy Transmission & Distribution The Core Purpose of Utility Poles

Energy transmission and distribution remain the central applications of the global utility poles market, generating 79.4% of total revenue. The sheer scale of ongoing investment underscores their significance, with clean energy investments estimated to reach $2.2 trillion in 2025—twice the expenditure on fossil fuels. Correspondingly, worldwide transmission and distribution spending is projected to rise from approximately $268 billion in 2023 to $392 billion by 2030. To align with climate objectives, the U.S. alone will require 75,000 miles of new high-voltage lines by 2035. Yet construction progress remains slow; only 888 miles of new high-voltage lines were built in 2024, far below the annual requirement of 5,000 miles.

Specific projects illustrate the utility poles market’s momentum. Key developments in 2024 included the 125-mile, 500-kV Ten West Link connecting Arizona and California, and the 102-mile, 345-kV Cardinal–Hickory Creek line between Iowa and Wisconsin. Additionally, the Midcontinent Independent System Operator (MISO) approved 18 new transmission projects totaling more than 2,000 miles and valued at $10.3 billion. Rising global power demand, expected to increase 4% in 2024, further elevates the need for extensive infrastructure. These projects exemplify how continuous electricity expansion sustains the central role of utility poles in modern energy systems.

- The Ten West Link project enables 3.2 GW of transfer capacity between state boundaries.

- In early 2025, just 62.5 miles of transmission projects had been completed through April in the U.S.

- Achieving net-zero emissions by 2060 would require annual energy sector investments of around $4.3 trillion.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific Spearheads Global Demand With Unmatched Infrastructure Ambitions

The Asia Pacific region, leading the utility poles market in global share, is defined by massive, state-driven capital expenditure programs creating unparalleled demand for new transmission and distribution poles. In China, for instance, the State Grid Corporation increased its planned 2024 grid investment to a record US$ 82.7 billion (600 billion yuan). By early 2025, reports indicated this spending plan was increased further to over US$ 89 billion. This investment directly supports the construction of six new Ultra-High Voltage (UHV) lines in 2024 alone, requiring a substantial volume of specialized support structures. Similarly, India's Power Grid Corporation of India Ltd (PGCIL) is executing an aggressive capex strategy, closing fiscal year 2025 with a record expenditure of ₹26,255 crore.

Looking forward, PGCIL's investment is set to escalate in the utility poles market, with projected capital expenditures of ₹35,000 crore for fiscal year 2027 and ₹45,000 crore for fiscal year 2028. These investments support a massive project pipeline, with total ongoing projects valued at approximately ₹1,43,749 crores as of January 2025, all of which necessitate extensive pole deployment. In another part of the region, Australia's 2024 Integrated System Plan (ISP) calls for urgent investment in 10,000 km of new transmission lines by 2050. Consequently, the initial phase of this plan requires an upfront capital investment of AUD 16 billion for essential transmission projects, directly fueling demand for high-strength poles.

North America's Market Is Driven By Modernization and New Load Growth

North America's utility poles market is fundamentally shaped by a 'super-cycle' of investment aimed at grid modernization and accommodating new industrial loads. As a result, U.S. electric utilities are projected to invest an immense US$ 1.4 trillion in electricity infrastructure between 2025 and 2030, which is double the amount invested over the prior decade. A significant portion of this capital directly funds the procurement and installation of new poles. American Electric Power, for example, raised its five-year capital plan to US$ 72 billion in late 2025 specifically to meet demand from data centers. Furthermore, another utility, NiSource, unveiled a US$ 28 billion capital expenditure plan through 2030, with US$ 7 billion dedicated to data center infrastructure, which requires extensive new power distribution networks. In Canada, wood pole manufacturer Stella-Jones strengthened its capital base by launching a CAD 400 million offering of senior unsecured notes in September 2024 to support its operations amid high demand.

Europe Focuses On Cross-Border Connectivity and Renewable Integration

Europe's utility poles market is being propelled by massive investments from transmission system operators (TSOs) strategically focused on integrating renewables and bolstering cross-border connectivity. This is driving significant demand for high-performance transmission poles. The Dutch-German TSO TenneT, for example, announced plans to invest EUR 160 billion between 2024 and 2033, with EUR 10.6 billion invested in 2024 alone. A large portion of these funds will be allocated to overhead connections, including some 4,800 km of new lines. In a similar push, the Elia Group, which operates in Belgium and Germany, plans to invest a total of EUR 30.1 billion over the next five years. This includes EUR 9.4 billion for projects in Belgium and EUR 20.7 billion in Germany. In the first half of 2024, Elia Group's investments already reached a record EUR 1,735.9 million, underscoring the aggressive pace of grid expansion.

Top 6 Recent Investments and Acquisitions are Reshaping Competitive Landscape of Utility Poles Market

- Hitachi Energy & Blackstone Partnership (October 2025): In a key strategic move, Hitachi Energy acquired a minority stake in Shermco, a Blackstone portfolio company, to form a partnership enhancing grid infrastructure services across North America.

- KKR's Global Climate Fund Growth (May 2025): Private equity firm KKR successfully raised US$ 2.749 billion for its debut climate infrastructure fund, which targets investments in mature renewable energy and storage projects.

- Elia Group's U.S. Transmission Investment (July 2024): Elia Group completed its acquisition of a minority stake in energyRe Giga Projects, deploying an initial US$ 250 million of a planned US$ 400 million investment for U.S. transmission projects.

- Blackstone's Power Grid Components Acquisition (September 2024): Blackstone Energy Partners III invested US$ 600 million to acquire Power Grid Components, signaling a strategic focus on assets benefiting from grid modernization in the utility poles market.

- Stella-Jones's Bond Offering (September 2024): The major wood pole manufacturer launched a CAD 400 million offering of senior unsecured notes to strengthen its capital base and position itself for future growth.

- Power Grid Corporation's Strategic Acquisition (March 2025): PGCIL of India acquired Kurnool III PS RE Transmission Limited for approximately ₹19.04 crore to strengthen its transmission system for renewable energy.

List of Key Companies Profiled:

- A-AERIAL SERVICES.

- ALLIED BOLT PRODUCTS LLC.

- EATON CORPORATION

- EL SEWEDY ELECTRIC COMPANY

- FUCHS EUROPOLES GMBH

- HILL & SMITH HOLDINGS PLC

- NIPPON CONCRETE INDUSTRIES CO., LTD.

- OMEGA FACTORY

- PELCO PRODUCTS INC.

- RS TECHNOLOGIES INC.

- SKIPPER LTD.

- STELLA-JONES INC.

- UTILITY METALS.

- VALMONT INDUSTRIES INC.

- Other Prominent Players

Segmental Overview

By Type

- Transmission Poles

- Distribution Poles

- Light Poles

By Material Type

- Wooden Utility Poles

- Steel Utility Poles

- Stepped poles (ISTPs)

- Swaged poles (ISWPs)

- Concrete Utility Poles

- Fiber Reinforced Polymer (FRP) Composites

By Pole Size

- Below 40ft

- Between 40 & 70ft

- Above 70ft

By Application

- Energy Transmission & Distribution

- Telecommunication

- Street Lighting

- Heavy Power Lines

- Sub Transmission Lines

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Malaysia

- Thailand

- Singapore

- Vietnam

- Indonesia

- Philippines

- Rest of ASEAN

- Rest of Asia Pacific

- Middle East & Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 47.45 Billion |

| Expected Revenue in 2033 | US$ 71.31 Billion |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Bn) |

| CAGR | 4.63% |

| Segments covered | By Type, By Material Type, By Pole Size, By Application, By Region |

| Key Companies | A-AERIAL SERVICES., ALLIED BOLT PRODUCTS LLC., EATON CORPORATION, EL SEWEDY ELECTRIC COMPANY, FUCHS EUROPOLES GMBH, HILL & SMITH HOLDINGS PLC, NIPPON CONCRETE INDUSTRIES CO., LTD., OMEGA FACTORY, PELCO PRODUCTS INC., RS TECHNOLOGIES INC., SKIPPER LTD., STELLA-JONES INC., UTILITY METALS., VALMONT INDUSTRIES INC., Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |