Wireless EV Charging Market: By Charging Technology Type (Magnetic Inductive Charging, Capacitive Coupling Charging, Resonant Inductive Charging); Component Type (Power Transfer Equipment, Control System, Transmission and Reception Equipment); Vehicle Type (Passenger Vehicles, Commercial Vehicles, Two-Wheelers); Application (Residential Charging, Commercial Charging, Public Charging Stations); End User (Individual Consumers, Fleet Operators, Government Agencies); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2034

- Last Updated: 15-Oct-2025 | | Report ID: AA09251509

Market Scenario

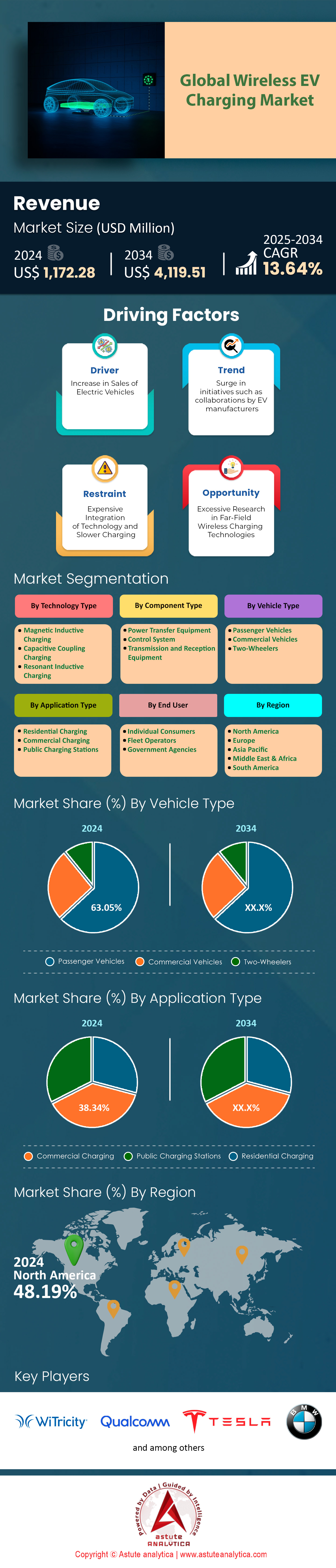

Wireless EV charging market was valued at US$ 1,172.28 million in 2024 and is projected to hit the market valuation of US$ 4,119.51 million by 2034 at a CAGR of 13.64% during the forecast period 2025–2034.

Key Findings in Wireless EV charging Market

- Based on technology, magnetic inductive charging technology is controlling the largest 64.04% market share.

- Based on the component, power transfer equipment with over 59.75% market share are generating the highest revenue of the market.

- Based on vehicle type, passenger vehicles with over 63.05% market share.

- Based on application, commercial charging take up over 38.38% market share of the market.

- North America to remain the key contributor with over 48% market share

- Wireless EV Charging market size is set to surpass US$ 4,119.51 million by 2033.

The demand for wireless electric vehicle charging is surging, propelled by a confluence of record-breaking electric vehicle sales and strategic, high-stakes deployments. With global EV sales projected to surpass 17 million units in 2025, the underlying market for convenient charging solutions is expanding exponentially. This growth is attracting immense investment, with leading wireless ev charging companies like WiTricity and Hevo securing significant funding to scale operations. The market is witnessing the tangible results of these investments; projections for 2025 estimate the deployment of over 5,000 new public and private wireless charging points globally, with each wireless electric charger being a critical step towards building a viable ecosystem.

Government initiatives are a primary catalyst for the electric vehicle wireless charging market, with the U.S. Department of Transportation allocating a significant $635 million in grants in January 2025 to deploy over 11,500 charging ports. A previous grant in 2024 provided $521 million for more than 9,200 ports, underscoring sustained federal support. State-level programs, like California's $55 million "Fast Charge California Project" launched in August 2025, further amplify this infrastructure push.

Innovation and adoption by key industry players are further stoking this demand for wireless charging evs. The potential fleet size of vehicles equipped with a factory-installed wireless charger electric car is now estimated to reach over 200,000 units by 2027, driven by commitments from automakers like Porsche, which will feature 11 kW wireless charging on its 2026 Cayenne EV. Leading countries in the wireless EV charging market such as the U.S., Germany, and China are aggressively fostering this growth through targeted initiatives. For instance, Germany is funding multiple in-road dynamic charging pilots, while the U.S. Department of Transportation's $635 million grant program in 2025 is set to deploy over 11,500 new charging ports, many incorporating wireless technology.

Top players like Siemens, Witricity, and InductEV are capitalizing on this momentum, catering to a burgeoning commercial sector. A notable development is InductEV wireless charging's focus on high-power charging for industrial fleets, with pilot programs at major logistics hubs like the Port of Long Beach. This move into heavy-duty applications is a critical demand driver, demonstrating the technology's viability beyond passenger cars. The combined impact of massive EV adoption, strategic government funding, automaker integration, and successful commercial pilots creates a powerful feedback loop, ensuring that the demand for wireless charging is not just growing, but accelerating at an unprecedented pace.

To Get more Insights, Request A Free Sample

Unlocking New Revenue Pockets in the Wireless EV Charging Market

i. Seamless Vehicle-to-Grid (V2G) Integration: The absence of physical cables makes wireless charging an ideal platform for automated V2G applications. Future EVs parked over wireless pads could autonomously provide grid stabilization services or sell excess power back to utilities during peak demand without any driver intervention. In 2025, several pilot programs are underway to quantify these benefits, with at least 15 utility companies globally running trials. One such program in the Netherlands involves 50 wirelessly connected EVs and has demonstrated the potential to provide up to 500 kW of ancillary services to the grid operator during peak hours.

ii. Automated Charging for Autonomous Fleets: The rise of autonomous vehicles (AVs) presents a compelling business case for the wireless EV charging market, showcasing one of the key future applications of wireless charging. Robotaxis and autonomous delivery vehicles will require charging solutions that need zero human interaction. Startups in this space are attracting significant attention; one autonomous charging company secured $15 million in a Series A funding round in early 2025. Projections show that by 2028, over 20,000 autonomous commercial vehicles will require automated charging solutions, creating a substantial and entirely new market segment.

Commercial Fleets Drive Demand for High-Power Wireless Charging

The operational demands of commercial fleets are creating a robust and specific need for high-power wireless charging. For sectors like logistics, public transit, and port operations, minimizing vehicle downtime is paramount. Consequently, the wireless EV charging market is seeing significant innovation in high-power solutions. Companies like WAVE Charging are demonstrating 500kW systems capable of fully charging a Class 8 electric truck in less than 15 minutes. This project, supported by an $8.4 million grant from the U.S. Department of Energy, is specifically targeting the challenging environment of Midwest logistics.

Furthermore, InductEV is actively deploying systems with power outputs up to 450 kW for port equipment, recognizing that perpetual operations require rapid, opportunistic charging. Their systems are designed to operate in harsh conditions with a temperature tolerance from -35 to +45 degrees Celsius. Another pilot project at the Port of Long Beach, backed by a $3.3 million grant from the California Energy Commission, will use InductEV's technology to power five battery-electric cargo vehicles. Innovation is also reflected in intellectual property, with new patents filed in 2024 and 2025 for polyphase systems capable of transferring over 50 kW of power wirelessly.

The In-Motion Revolution: Dynamic Wireless EV Charging Market Takes the Lead

The demand for dynamic wireless charging for vehicles, the technology that powers them as they drive, is surging. This growth is primarily driven by its potential to eliminate range anxiety and enable continuous, uninterrupted operation for commercial and public transport fleets by charging electric cars wirelessly while on the move. While static charging pads still dominate the market, holding 81.90% of the market share in 2024, dynamic in-road solutions are projected to grow at an explosive CAGR of 18% through 2033.

Current adoption is moving from small-scale pilots to more significant deployments, signaling market readiness. Key players like Electreon, WiTricity, and WAVE are leading this charge. Europe has taken an early lead, commanding 38.20% of the market in 2024, thanks to projects like Sweden's e-motorway and Germany's eCharge initiative. In the U.S., a project in Detroit is testing in-road inductive technology, and another in Indiana is developing a system capable of charging heavy-duty trucks at 200 kilowatts. These real-world applications are crucial for validating the technology and paving the way for wider commercialization.

The dynamic wireless EV charging market potential is immense, particularly in the commercial sector, which is projected to grow at a CAGR of 14.54% between 2025 and 2034. Fleet operators are drawn to the technology's ability to lower labor costs and increase vehicle utilization rates. The supply side is responding with increasingly powerful and efficient systems. For example, some high-power units above 150 kW are set to see robust growth. Although the high initial cost of infrastructure remains a challenge, ongoing advancements and government support are expected to drive down expenses and accelerate the adoption of this transformative technology.

Segmental Analysis

Convenience and Standardization Propel Inductive Charging's Dominance

Magnetic inductive charging technology, a form of EV inductive charging, with its commanding 64.04% market share, leads the wireless EV charging market due to its high efficiency and the critical adoption of industry standards. Technology frontrunners have pioneered systems based on magnetic resonance that achieve grid-to-battery efficiencies between 90-93%, rivaling traditional plug-in chargers. The finalization of the SAE J2954 standard is a monumental factor for inductive charging electric vehicles, establishing a universal protocol for systems up to 11 kW, which ensures interoperability between chargers and a growing number of vehicle models. This standard, developed over a decade, gives automakers the confidence to integrate the technology.

Leading companies hold over 1,000 patents for their technology, showcasing the depth of innovation solidifying this segment's lead. Other companies have also made significant strides with solutions. The cost to install an 11 kW wireless system is becoming more competitive, further lowering the barrier to adoption for consumers who prioritize the immense convenience of simply parking to charge.

This technical maturity has translated into real-world applications and consumer demand. Automakers like BMW and Mercedes-Benz are already planning to implement 11 kW wireless inductive systems, signaling a clear path toward mass adoption. The global wireless EV charging market is bolstered by these advancements, making the technology a must-have feature for the future of autonomous and smart mobility.

- Over 1,200 pilot and commercial projects for wireless EV charging are active globally in 2025.

- Automakers like BMW and Mercedes-Benz are planning to implement an 11 kW wireless inductive charging system.

- The U.S. government allocated over $150 million in R&D grants between 2020 and 2025 for wireless charging demonstrations.

Essential Hardware Makes Power Transfer Equipment the Revenue King

Power transfer equipment, which includes the ground assembly (GA) transmitter pad and the vehicle assembly (VA) receiver pad, generates the highest revenue with a 59.75% share in the wireless EV charging market. The dominance is expected to stay put as it represents the core, non-negotiable hardware of any wireless charging system. These components, manufactured by specialists, contain intricate systems of magnetic coils, ferrite plates, and power electronics that manage the high-frequency energy transfer. The complexity and material costs, especially for high-power systems capable of delivering 75 kW to 450 kW for commercial vehicles, are significant. A major player in this area has been awarded 105 patents for its innovations in this specific area. Companies have engineered their power stations to be surface-mounted or embedded seamlessly into the ground, adding to installation value.

The revenue is further driven by the distinct costs of each part of the system; the GA pad often accounts for up to three-quarters of the total system cost, while the vehicle-mounted receiver is the lower-cost piece. Innovation in this segment is rapid, with companies focusing on smaller, more efficient pad designs and incorporating advanced components like Silicon Carbide (SiC) MOSFETs to handle higher power loads with minimal energy loss. As the wireless EV charging market expands, the demand for this foundational equipment from both automotive OEMs and aftermarket suppliers will continue to drive its revenue leadership.

- Current wireless charging systems from leading providers range from 75 kW up to 450 kW.

- High-power charging pads capable of delivering 11–22 kW are entering commercial deployment, reducing charging times by up to 50%.

- The Qi2 25W standard is being introduced for even faster and more energy-efficient charging.

Operational Efficiency Makes Commercial Charging a Dominant Force

With a 38.38% share, the commercial charging segment's leadership in the wireless EV charging markets is built on a powerful business case: reduced operational costs and maximized vehicle uptime. For commercial fleets, every minute a vehicle is parked for manual plug-in charging is a minute of lost productivity. Wireless charging enables automated "opportunity charging," allowing vehicles like delivery vans and buses to charge while loading, unloading, or during scheduled stops. Research indicates that last-mile EV delivery fleets could save up to 50% in total cost of ownership by using wireless charging instead of plugs. A major player in this space has active deployments with municipal transit in cities like Indianapolis and for port tractors at the AP Moeller Maersk Terminal in New Jersey.

The technology is proven to be robust across the global wireless EV charging market. By the end of 2026, half of all battery-electric buses in Washington state are projected to be charged by wireless on-route systems. Power levels are also substantially higher, with providers offering systems that deliver 200 kW on average, essential for minimizing charging time for large vehicles. The focus on electrifying medium- and heavy-duty vehicles, which account for a disproportionate amount of transport emissions, ensures continued investment and growth in the commercial wireless EV charging market.

- Wireless charging can reduce a fleet's peak electrical demand by half by spreading charging sessions throughout the day.

- Stellantis is actively demonstrating Level 2 wireless charging on its Chrysler Pacifica PHEV fleet vehicles.

- Amazon plans to deploy 100,000 electric trucks for deliveries, driving the need for efficient charging.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Passenger EV Growth Creates a Massive Wireless Charging Arena

Passenger vehicles command a 63.05% revenue share of the wireless EV charging market size, fueled directly by the explosive growth in global electric car sales, which exceeded 17 million units in 2024. This created a global electric fleet of nearly 58 million cars by the end of 2024. A significant portion of these owners represents a prime audience for the convenience of wireless charging. Over 90% of prospective EV buyers want wireless charging as an option on their next vehicle. Automakers are responding to this demand, with OEMs like Hyundai, BYD, and FAW already offering factory-installed wireless charging on select models. One model was among the first to feature this technology, setting a precedent in the premium segment. Another model was the first commercially available hybrid with this feature.

While factory installations are growing, the aftermarket for retrofitting vehicles also contributes significantly. The cost to add a vehicle assembly is the lowest part of the system's expense, making it an attractive upgrade for many of the 10.8 million battery-electric vehicles sold in 2024. The desire to eliminate cumbersome cables is a powerful motivator for consumers, making the passenger segment the primary driver for the wireless EV charging market.

- Over 785 distinct electric car models were available to consumers in 2024, with projections of 1,000 models by 2026.

- In one survey, wireless charging was rated 34% higher in demand by consumers than self-driving capability.

- An 8-kilowatt home system can add up to 24 miles of range to a vehicle for every hour of charging.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America's Infrastructure Surge Creates Unprecedented Market Dominance

North America is aggressively cementing its leadership in the wireless EV charging market, commanding over 48.19% of the global share through substantial government funding and strategic infrastructure projects. The Canadian government's Zero Emission Vehicle Infrastructure Program (ZEVIP) is a major driver, with a recent announcement committing $9.7 million CAD to 23 projects that will install over 850 chargers across the country. One recipient alone, Funding Quebec, received $3 million CAD to install 320 Level 2 chargers. Another federal investment in 2024 provided $14.9 million for 20 different ZEV infrastructure projects nationwide. The program, extended to 2027, has a goal to deploy 84,500 chargers by 2029.

In Mexico, the wireless EV charging market is also experiencing rapid growth, with plans by VEMO and Siemens to install 500 EV charging points by the end of 2024. In a significant push, Mexican company SEV is developing 20 of its own charging centers by the end of 2024, adding to its existing 18 dealerships with charging capabilities. These stations will initially feature 30 kW chargers. The country saw over 42,000 EV chargers installed in 2024 alone. These robust, large-scale investment and deployment figures from across the continent demonstrate a clear and decisive strategy to build a comprehensive wireless charging network, solidifying North America's dominant market position.

Europe's Dynamic Charging Trials and Network Growth Signal Strong Adoption

Europe is rapidly advancing its wireless EV charging market capabilities, focusing on innovative dynamic charging projects and expansive network growth. Germany is a key hub for this innovation, with a pilot project launched in Balingen to install a 1-kilometer-long in-road inductive charging system for public buses, a project valued at €3.2 million. In another initiative, 23 copper coils were installed in a roadway in Bad Hersfeld for testing. Bavaria is also set to begin construction in summer 2025 on a 1-kilometer inductive charging segment on the A6 motorway. Sweden is pioneering the world's first permanent e-motorway, a 13-mile stretch of the E20 highway, slated for completion by 2025.

The broader charging infrastructure across Europe is also expanding at a remarkable pace. At the end of 2024, the continent had just over 1 million public charging points. France leads in volume, reaching 154,694 public charging points by the end of 2024, including 27,986 DC fast-chargers. In December 2024, France recorded an average of 25.7 charging sessions per charging point. Meanwhile, the UK is advancing its own trials, with a government-backed initiative to test wireless charging technology in off-road settings for 18 months. An AI-managed charging trial involving 13,000 UK consumers also demonstrated significant potential for grid management.

Asia Pacific's Innovation and Patent Leadership Shape Future Market Trends

The Asia Pacific region is establishing itself as a powerhouse of innovation in the wireless EV charging market, led by China's overwhelming dominance in intellectual property. Chinese entities have registered an astonishing 62,655 patents related to EV charging technology, vastly outnumbering other nations. In 2024, China's R&D expenditure reached an impressive 3.6130 trillion yuan ($494.34 billion), fueling this innovation. A new patent from Huawei in July 2025 even describes a solid-state battery with a potential energy density of 400–500 Wh/kg. This focus on research ensures the region will heavily influence the technology's future trajectory.

Meanwhile, other countries in the wireless EV charging market are focused on practical implementation and pilot programs. Japan is conducting ambitious tests aiming for practical dynamic charging technology by 2025, with one test demonstrating a small EV running continuously at 15 kilometers per hour on a wireless track. Another Japanese pilot running until March 2025 in Kashiwa-no-ha Smart City is testing wireless charging at traffic lights. In India, the government has allocated ₹2,000 crore under the PM E-DRIVE scheme for charging stations. The nation's EV charging startup scene is also vibrant, with around 50 startups raising nearly $511 million between 2020 and 2024.

Top Recent Developments Affecting Wireless EV Charging Market Positively

1. Porsche and Mercedes-Benz Lead Automaker Adoption

- Porsche has announced that its 2026 Cayenne EV will be its first all-electric SUV to feature an 11 kW wireless charging system.

- Similarly, Mercedes-Benz is actively testing wireless inductive charging on its experimental vehicle, the ELF, with plans to incorporate bidirectional charging capabilities in production models starting in 2026.

2. High-Power Wireless Charging for Heavy-Duty Vehicles

- Companies like WAVE (acquired by Ideanomics) and Momentum Dynamics are developing systems with capacities up to 500 kW, drastically reducing charging times for electric trucks and buses.

- A partnership involving Cummins, Purdue University, and Walmart is developing a 750kW wireless system for Class 8 trucks, aiming to make charging as quick as a 15-20 minute stop.

3. Increased U.S. Federal and State Government Support

- The U.S. Department of Transportation's National Electric Vehicle Infrastructure (NEVI) program, a $5 billion initiative, is a key enabler for the build-out of a national charging network. In early 2025, the "Wireless Electric Vehicle Charging Grant Program Act of 2025" was introduced in the U.S. Congress to provide dedicated funding for wireless EV charging projects, including for medium and heavy-duty trucks.

4. Development of Bi-Directional Wireless Charging (V2G)

- Mercedes-Benz plans to launch its first bi-directional charging services in several European markets in 2026.

Top Companies in the Wireless EV Charging Market

- Witricity Corporation

- Qualcomm Incorporated

- Plugless Power

- HEVO Inc.

- Momentum Dynamics

- BMW AG

- AB Volvo

- Volkswagen AG

- Nissan Motor Corporation

- Tesla, Inc.

- ChargePoint Holdings, Inc.

- Hyundai Motor Company

- Ford Motor Company

- Schneider Electric

- ABB Ltd.

- Other Prominent Players

Market Segmentation Overview

By Technology

- Magnetic Inductive Charging

- Capacitive Coupling Charging

- Resonant Inductive Charging

By Component Type

- Power Transfer Equipment

- Control System

- Transmission and Reception Equipment

By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Two-Wheelers

By Application Type

- Residential Charging

- Commercial Charging

- Public Charging Stations

By End User

- Individual Consumers

- Fleet Operators

- Government Agencies

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- The UK

- Germany

- France

- Italy

- Spain

- Poland

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia & New Zealand

- ASEAN

- Cambodia

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |