Market Scenario

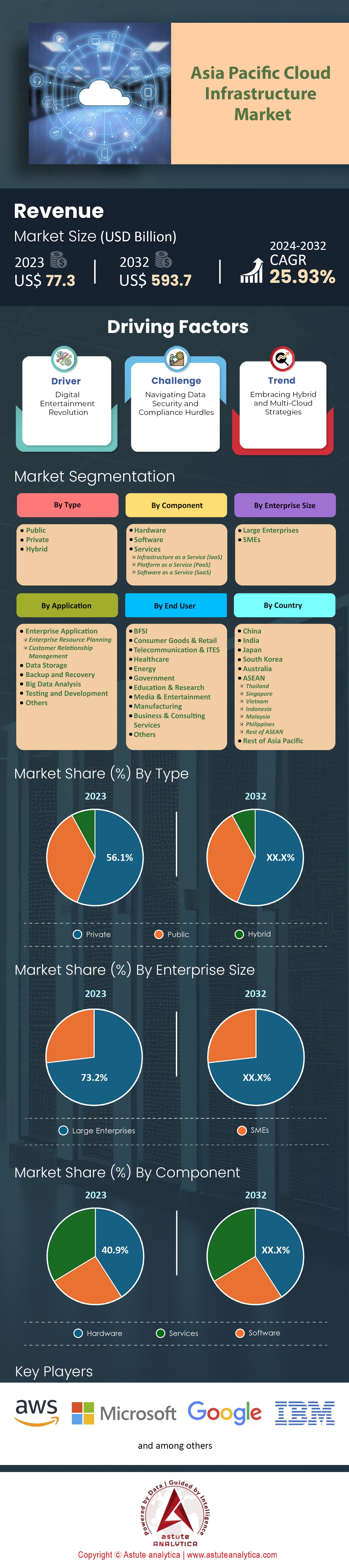

The Asia Pacific Cloud Infrastructure Market was valued at US$ 77.3 billion in 2023 and is projected to hit the market valuation of US$ 593.7 billion by 2032, at a CAGR of 25.93% during the forecast period 2024–2032.

Enterprises relentlessly pursuing digital transformation, internet-connected devices multiplying in number and cost-effective IT solutions are factors that have led to exponential growth. The flourishing e-commerce ecosystem in the region is a major driver behind this boom, fueled by increasing smartphone penetration and internet connectivity. Consequently, there has been an unprecedented surge in demand for cloud infrastructure that supports online shopping platforms. Alibaba Cloud, China's top provider of cloud services, recorded significant growth in its e-commerce segment which caters for the booming online retail market across Asia Pacific. A good 27% of respondents from this area said they intend to use Alibaba Cloud by 2023.

At the same time, cloud infrastructure market demand has been driven by rapid advancements within Financial Technology (fintech) industry. With the widespread adoption of mobile payments systems all over the world combined with digital banking services being introduced everywhere; it’s necessary that these types of mission-critical applications should be supported by secure scalable reliable clouds. According to Astute Analytica forecasts on spending patterns related to financial technology companies located within APAC regions alone were projected at around $10 billion dollars spent annually up until 2025 signifying just how much trust these organizations have placed upon their ability use cloud technologies during their journey towards digital transformation.

The gaming industry also plays a big role in this growth. Cloud gaming services are becoming more popular in the region because they allow you to play games without having high-end hardware. Niko Partners predicts that by 2023, the Asia Pacific cloud gaming market will be worth $3 billion due to strong internet connection and an increasing number of gamers from countries like China, Japan and South Korea where there has been steady growth over time. For example, 60 million Asian gamers used cloud gaming platforms last year which could reach up to half a billion users by 2028 making access easier for most people who can’t afford expensive computers or consoles as well those without any gaming console with disc.

Furthermore, government initiatives aimed at promoting digital transformation through cloud adoption have had positive impacts on Asia Pacific’s cloud infrastructure market expansion within different sectors thus boosting business opportunities for various stakeholders involved within these areas such as Singapore's Cloud First policy which encourages public sector agencies embrace clouds thereby creating demand therefore driving growth within cities like Singapore where such policies exist.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Digital Entertainment Revolution

In Asia Pacific cloud infrastructure market, the digital entertainment industry is seeing a massive shift because of factors like growing incomes among consumers, increasing internet usage rates as well as number of streaming platforms available. This change has created a need for more cloud infrastructures that can support online gaming delivery systems, video streaming websites, and content distribution networks across this region.

It is expected that revenue generated from video streaming in Asia Pacific will be $32.64 billion by 2024 which indicates a CAGR of 8.88%. Additionally, in 2023 alone mobile game spending by consumers was found to account for 64% worldwide with most money being spent within this area too; considering there are over 5.2 billion mobile subscribers here it should come as no surprise that APAC leads the rest when it comes down to numbers or percentage points either way around them all together. Cloud infrastructure provides an important foundation for companies involved with digital entertainment to deliver games and streams of the highest quality throughout Asia Pacific cloud infrastructure market. For example, Tencent uses clouds such as those provided by Amazon Web Services (AWS), Microsoft Azure or Google Cloud Platform (GCP) among others – these power some its most popular titles like Honor Of Kings & PUBG Mobile; similarly, Netflix relies on similar technology but only so much peering arrangements exist between different networks could allow seamless transition from one provider’s servers over wire through another one's data centers back onto user device screen.

Trend: Embracing Hybrid and Multi-Cloud Strategies

There is a shift in cloud infrastructure adoption happening in the Asia Pacific region where more firms are turning to hybrid and multi-cloud strategies for peak performance, maximum flexibility and risk reduction. By 2022, at least 90% of enterprises based in Asia Pacific cloud infrastructure market will have adopted multi-cloud strategies as recognized by following these findings, which reveals that diversifying cloud environment has many advantages. This change can be attributed to different things but mainly to agility, scalability and data sovereignty compliance. Workload distribution across several cloud providers is one way that they can achieve this because each platform has got its own capabilities; For instance, Alibaba Cloud integrates well with Chinese regulatory requirements whereas AWS offers variety services plus international coverage too among others. This also ensures continuity of operations for organizations while optimizing costs since they will not be tied down to one vendor only. In fact, already some leading companies throughout APAC cloud infrastructure market have started enjoying fruits brought about by adopting such kind of arrangement like Singapore Airlines which uses both AWS & Microsoft Azure together so as power their digital transformation programs including krisConnect airline services platform.

Toyota Motor Corporation does so globally where it combines on-premises infrastructure with public cloud services from Amazon Web Services (AWS) as well as Microsoft Azure through hybridizing these two clouds together thus enabling them support its worldwide operations even more effectively than before. Based on this therefore still being part and parcel any given enterprise’s digital strategy especially those operating within highly competitive business environments hence should always remain so according to shifting nature today’s rapidly advancing world technologies.

Challenge: Navigating Data Security and Compliance Hurdles

In a changing cloud infrastructure market in the Asia Pacific, companies face significant hurdles around data security and compliance. The enforcement of strict rules like Singapore’s Personal Data Protection Act (PDPA) and Europe’s General Data Protection Regulation (GDPR) has made it crucial to protect data privacy while ensuring regulatory conformity. Based on our research, 73% of Asia Pacific organizations identify concerns about data privacy and security as their number one barrier to adopting cloud services. These challenges are compounded by the complexity of understanding data residency and sovereignty laws which often have no logical pattern or explanation. As information moves across borders and resides within various jurisdictions, firms must deal with different standards for each country or region within APAC where they operate. For example, China requires that certain types of records should be stored physically within its territory under its Cybersecurity Law.

Furthermore, there is an increasing need for strong measures against breaches due to publicity surrounding such incidents coupled with rising rates of cyber threats. In the last year alone, Marsh and Microsoft found that 55% of companies surveyed in Asia Pacific cloud infrastructure market had experienced some form cyber-attack according their joint 2021 APAC Cyber Risk Survey. These attacks result not only financial loss but also loss customer trust as well reputational damage suffered by organizations affected.

Leading businesses throughout APAC cloud infrastructure market have already begun taking proactive approaches towards addressing cloud-based data security risks alongside compliance issues too. One case study would be GovTech who came up with MTCS SS among other things being done by them; this is certification scheme designed enable organizations assess strengthen levels protection offered their environments based on different tiers defined under it. Currently, financial institutions are also investing heavily in more advanced threat intelligence capabilities alongside cyber security technologies. These efforts are part of mitigation against evolving attacks methods used by hackers seeking gain f0r unauthorized access critical system resources either steal from them directly or indirectly obtain sensitive client/customer information.

Segmental Analysis

By Type

The private cloud segment currently holds the highest share of 56.1% in the Asia Pacific cloud infrastructure market driven by multiple factors such as stringent data security and compliance requirements, concerns about data sovereignty and control, and the need for customization and tailored solutions. Various companies ranging from finance, healthcare to government among others prefer private cloud deployments for their data and resources control, adherence to regulatory compliance as well as meeting critical application performance and reliability requirements.

Conversely, the public cloud sector is growing rapidly at a CAGR of 26.88% in the Asia Pacific region which is the highest worldwide. This increased adoption rates of public clouds are due to scalability, agility and cost efficiency among other things. More so, organizations are now embracing public cloud platforms such as Microsoft Azure, Amazon Web Services (AWS) and Google Cloud Platform (GCP); this move allows them utilize advanced capabilities offered by these providers while also gaining access to many different services hence speeding up digital transformation endeavors.

By Component

In the dynamic landscape of the Asia Pacific cloud infrastructure market, the hardware segment commands the highest share, driven by the foundational role of traditional infrastructure components like servers, storage devices, and networking equipment. The servers, storage devices and networking equipment are among the traditional infrastructure components that form this segment. The segment was responsible for 40.9% of total regional cloud expenditure in 2023. Organizations invest in hardware to create private clouds, enable hybrid deployments as well as ensure performance, reliability and security of their workloads on the cloud.

The fastest growing segment of this cloud infrastructure market is services which had a CAGR of 26.81% in 2023; it offers an array of professional and managed services focused around cloud adoption, implementation, migration, optimization & support etcetera. Cloud service usage enables businesses go digital faster while improving operational efficiencies across all sectors such as finance; healthcare; retailing; manufacturing industry among others including governments worldwide too.

By Application

The APAC cloud infrastructure market is led by the enterprise applications segment, which accounted for 31.6% of revenue share. Today, various industries such as finance, healthcare, manufacturing, retail and government rely heavily on enterprise applications. They include customer relationship management (CRM), human resource management (HRM), supply chain management (SCM), and other systems that serve different functions within an organization. Businesses can make their processes more efficient and collaborative among employees or stakeholders while also saving costs through moving these critical business applications onto the cloud. Furthermore, these types of programs are flexible enough to allow for scalability where necessary without incurring unnecessary expenses when demand fluctuates either upwards or downwards so companies only pay what they use at any given time.

Apart from this, big data analysis segment of the cloud infrastructure market is projected to keep growing at the highest CAGR of 27.66% during the forecast period due to heavily increasing volume of data at rapid rate; In the last few years, the world has witnessed a significant upsurge in the number of IoT devices, which is further driven by available digital services like e-commerce platforms among others. These factors create massive amounts of information every second thereby necessitating real-time actionable insights from scalable cloud based big data analytics solutions equipped with processing capabilities needed to handle such volumes efficiently. Using predictive analytical tools supported by machine learning systems powered with artificial intelligence algorithms enables firms gain competitive edge over their rivals besides driving growth across various sectors such as marketing finance health care cyber security etc. For instance, medical institutions could utilize cloud based HRMS while retailers may adopt SCM system hosted on clouds; at same time, banks might employ analytics software sitting atop clouds for better decision-making purposes.

By End User

The Asia Pacific cloud infrastructure market is strongly influenced by the Banking, Financial Services and Insurance sector or BFSI. The BFSI segment is currently dominating the market with more than 24% market revenue share and is also projected to keep growing at the fastest CAGR of 27% in the years to come. This dominance is attributed to one reason as institutions work with huge volumes of sensitive data which require secure as well as scalable infrastructure hence making them a good fit for cloud solutions. Besides this fact, there are regulatory compliance challenges that face the BFSI industry; however, compliance-ready solutions are provided by cloud platforms thereby reducing such burdens on establishments. In order to improve operational efficiency, streamline processes and deliver new services to clients; businesses within this space may need to adopt innovations brought about by cloud computing in terms of their infrastructure. Apart from this, the segment is witnessing growth due to swift growth in digital banking and fintech solutions adoption along with growing digital economy across different parts of Asia Pacific region. The use of clouds enables faster innovation besides facilitating agility within operations while also enhancing customer experiences so that firms operating under BFSI can be well placed for growth during digital age characterized with high levels of competition in the cloud infrastructure market.

Also, banks are using core systems based on cloud technologies. For instance, insurance firms implementing claims processing platforms hosted over clouds; FinTech start-ups relying heavily on scalable operations supported through clouds among others. Furthermore, both homegrown or international vendors have come up with specific offerings meant only for Financial Services Innovation Business Units needs thus driving further investments into such areas within this industry vertical alone. Additionally, there were findings from surveys done recently which revealed that more than four out five financial companies plan on increasing their investments into this technology over next couple years

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Country Analysis

China and India are the biggest markets in Asia Pacific cloud infrastructure market due to their large populations and fast-growing economies. These factors have created an environment that is conducive for digital transformation as well as cloud adoption. In addition, China and India are making massive investments on infrastructure development such as telecommunications and internet connectivity that are necessary for delivery of cloud services. Equally important, in both nations there exist vibrant startup ecosystems coupled with thriving technology sectors that drive demand for cloud infrastructure to support innovation and foster growth. Moreover, in China alone there are government initiatives which promote digitalization while at the same time encourage adoption of cloud technologies thereby further expanding its markets like never before.

It is worth noting down that China accounts for the largest share within Asia pacific cloud infrastructure market and is projected to keep growing at a CAGR of 26.87 %. On the other hand, India market is projected to expand at a CAGR of 27.62 %. Alibaba Cloud, one of many Chinese tech giants, extended their range of products so that they can serve various industries vertically while Tencent Cloud also did something similar but it targeted different sectors horizontally this time round. Some Indian companies like Reliance Jio Infocom have been using clouds as part its strategy towards driving digital transformations across organization levels including individual businesses units such as retail stores among others.

Also, recently more collaborations between Chinese enterprises and Indian counterparts have been observed within APAC cloud infrastructure market hence fostering innovation through increased competition at market place level. Furthermore being home to very large number skilled IT professionals makes significant contributions towards realization regional solutions based on clouds since most organizations would require these experts during implementation processes beside many other roles played by them thus promoting wider usage throughout industry segments over here .Another thing is regulatory reforms being implemented aimed at enhancing data security as well as localization within clouds which has started shaping infrastructure landscape for different states like Karnataka located South India. Finally, more investments are expected in edge computing and 5Gs infrastructures, which is projected to accelerate adoption rates within China especially where there is already availability.

Recent Developments

- In 2023, the Directorate General of Training (DGT) announced a collaboration with Amazon Web Services (AWS) India to enhance the skillsets of students in cloud computing, data annotation, artificial intelligence (AI), and machine learning.

- In 2023’s Q3, China spends $9.2bn on cloud infrastructure with focus on AI

- In January 2024, US gov't announced its plant to introduced a new cloud rule to throttle China AI development

- In February 2024, Alibaba slashes China cloud prices by 20% to boost growth. Move aims to re-energize cloud division amidst slowing sales.

Key Players in the Asia Pacific cloud infrastructure market

- Adobe

- Alibaba

- AWS

- Cisco

- Dell Inc.

- Dropbox

- HashiCorp

- HPE

- IBM

- Intel

- Microsoft

- Nutanix

- Oracle

- OVHcloud

- Salesforce

- SAP

- ServiceNow

- VMware

- Workday

- Other Prominent Players

Market Segmentation Overview:

By Type

- Public

- Private

- Hybrid

By Component

- Hardware

- Software

- Services

- Infrastructure as a Service (IaaS)

- Platform as a Service (PaaS)

- Software as a Service (SaaS)

By Enterprise Size

- Large Enterprises

- SMEs

By Application

- Enterprise Application

- Enterprise Resource Planning

- Customer Relationship Management

- Data Storage

- Backup and Recovery

- Big Data Analysis

- Testing and Development

- Others

By End User

- BFSI

- Consumer Goods & Retail

- Telecommunication & ITES

- Healthcare

- Energy

- Government

- Education & Research

- Media & Entertainment

- Manufacturing

- Business & Consulting Services

- Others

By Country

- China

- India

- Japan

- South Korea

- Australia

- ASEAN

- Thailand

- Singapore

- Vietnam

- Indonesia

- Malaysia

- Philippines

- Rest of ASEAN

- Rest of Asia Pacific

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |