Market Scenario

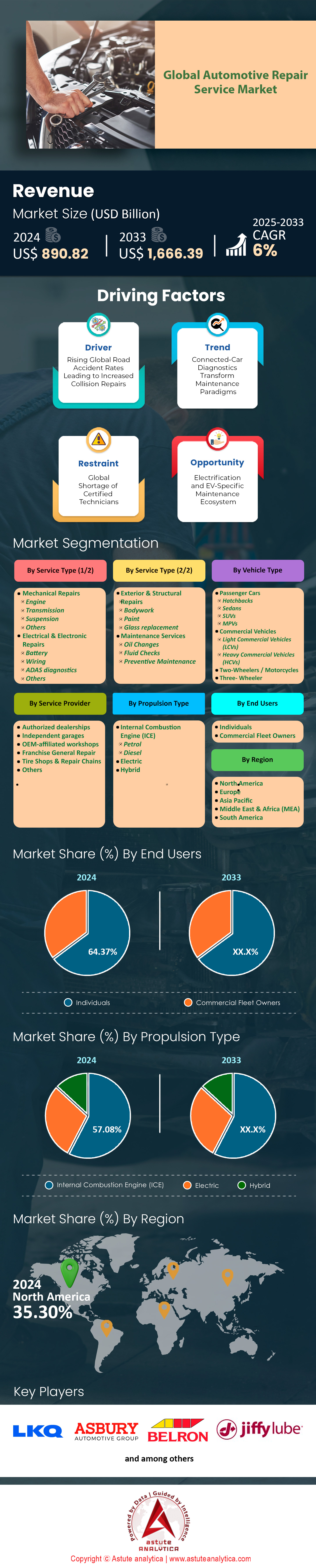

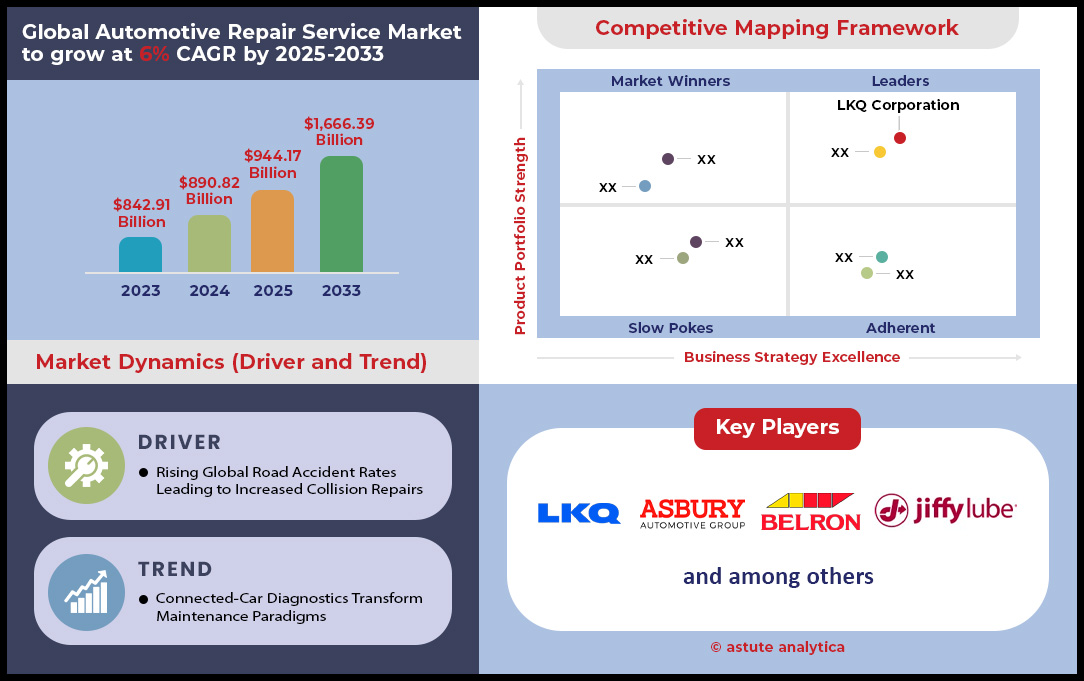

Automotive repair service market size was valued at US$ 890.82 billion in 2024 and is projected to hit the market valuation of US$ 1,666.39 billion by 2033 at a CAGR of 6% during the forecast period 2025–2033.

Key Findings

- By service type, mechanical repair services account for 44.96% of the global automotive repair service market.

- Based on vehicle type, passenger vehicles account for 48.14% of the global market.

- Based on service provider, independent garages take up over 38.02% of the market.

- Based on propulsion type, vehicles having internal combustion engines held the largest segmental share of 57.08%.

- North America set to remain the region with over 35.20% market share.

A profound shift in workforce needs is redefining the automotive repair service market. An incredible surge in demand is set to create over 30,000 new technician jobs in 2024 alone, a number forecasted to climb to 50,000 in 2025. Yet, a significant skills gap looms, with some cities in 2024 reporting a challenging technician-to-EV ratio of just one for every 150 vehicles. The industry is responding proactively; the National Institute for Automotive Service Excellence will administer over 15,000 EV-specific certification tests in 2024, while major franchises are funneling over US$ 10 million to upskill 20,000 technicians by 2025.

Mirroring the investment in people is a massive wave of capital pouring into technology. To remain competitive, independent repair shops are spending an average of US$ 50,000 on new EV diagnostic tools in 2024. By 2025, over 30,000 service centers are expected to install Level 3 DC fast-chargers simply for testing purposes. Collision centers are undergoing a similar transformation, with the number of EV-certified shops projected to reach 15,000 by 2025. The high stakes are clear, especially when a single EV battery replacement can cost an average of US$ 12,000 in 2024, justifying these substantial upgrades.

The very nature of service delivery is also being reimagined within the automotive repair service market. For ultimate convenience, mobile EV service fleets are expanding rapidly, with their numbers projected to hit 3,500 vans by 2025 and handle an estimated 500,000 minor repair jobs that year. Simultaneously, a competitive rift is widening between OEM dealerships, with labor rates around US$ 175 per hour in 2024, and independent shops offering rates closer to US$ 140 per hour. This market tension is set to intensify, with stakeholders closely watching the outcome of over 100 anticipated "Right to Repair" legal actions in 2025.

To Get more Insights, Request A Free Sample

Unlocking New Revenue Streams in a Rapidly Evolving Automotive Aftermarket

The automotive repair service market is presenting savvy business owners with incredible opportunities for growth. Looking beyond the obvious, two powerful trends are emerging that promise to create significant new revenue streams.

- Pioneering Service for Alternative Powertrains: While battery electric vehicles capture the headlines, a quieter revolution is happening with other advanced powertrains. Consider the rise of Hydrogen Fuel Cell Electric Vehicles (FCEVs), where giants like Toyota and Hyundai are investing heavily. As these innovative vehicles begin to populate our roads, they will create an entirely new and specialized service demand for components like fuel cell stacks and hydrogen storage systems. Shops that invest in this expertise early will position themselves as market leaders in a high-value, low-competition niche.

- Building Loyalty with Subscription-Based Care: Today's consumers value predictability and convenience more than ever. This shift is paving the way for subscription-based maintenance models in the automotive repair service market. Imagine offering your customers a simple, fixed monthly fee that covers all their routine service and common repairs. This approach provides them with peace of mind and budget certainty, while simultaneously giving your shop a stable, recurring revenue stream and fostering unmatched customer loyalty. It’s a true win-win that builds a lasting relationship beyond a single repair job.

Advanced Driver-Assistance Systems Fueling a High-Tech Service Revolution

Today's vehicles are becoming rolling supercomputers, and their sophisticated safety systems are creating a vital new focus for the automotive repair service market. Advanced Driver-Assistance Systems (ADAS) are now standard, and their delicate networks of sensors require expert recalibration after even minor incidents. This is not optional; it's a critical safety procedure. In 2024, the number of vehicles needing these recalibration services after a collision is expected to climb beyond 3 million in the United States. Consequently, shops must invest in the right technology, with the average cost for a complete set of ADAS calibration tools hitting US$ 60,000 in 2024.

The momentum behind this trend is only accelerating into 2025. Leading equipment suppliers are preparing to launch over 40 new ADAS calibration toolkits to meet the growing demand. To effectively use these tools, the industry will need to train an additional 15,000 technicians specifically in ADAS procedures by the end of 2025. The sheer volume of work is staggering, with the number of individual sensor recalibration events forecasted to eclipse 10 million procedures nationwide. Fueling this long-term demand is the fact that the average number of ADAS sensors on a new car is expected to grow from 12 in 2024 to 15 by 2025.

Managed Fleet Services Driving Consistent and High-Volume Repair Demand

The constant buzz of e-commerce and last-mile delivery is creating a powerful, behind-the-scenes engine for the automotive repair service market. The maintenance needs of these commercial fleets offer a consistent and high-volume business opportunity. By 2024, the total number of commercial vehicles managed under third-party maintenance contracts is projected to surpass 5 million in North America. These contracts provide shops with a reliable workflow, shielding them from the unpredictable nature of individual customer repairs. In fact, in 2025, predictive maintenance alerts from fleet telematics are expected to generate over 1.5 million unscheduled repair orders.

Tapping into this lucrative segment requires a focused strategy in the automotive repair service market. Independent service providers are forecasted to spend an average of US$ 25,000 annually on specialized diagnostic software for fleet management in 2024. Furthermore, to minimize costly downtime for their clients, it is estimated that over 10,000 repair shops will offer dedicated mobile maintenance units for on-site fleet service by 2025. The reward for this focus is clear, as the number of scheduled maintenance tasks per fleet vehicle is set to rise to an average of six per year in 2025, cementing this segment's role as a cornerstone of the modern repair industry.

Segmental Analysis

Mechanical Repairs are Unwavering Engine of the Automotive Aftermarket

The mechanical repair services segment, commanding a significant 44.96% of the global market, remains the bedrock of the automotive repair service market. This dominance is fundamentally driven by the sheer necessity and frequency of these services. In 2024, the average cost for a 5-year-old car's annual repairs and maintenance stood at US$ 1,519.50. The increasing age of vehicles on the road, now averaging between 12.6 and 12.8 years, naturally leads to more wear and tear on essential components. Basic services, which are a regular necessity, cost between US$ 95 and US$ 237 per visit, while more involved annual services range from US$ 157 to US$ 355. Unexpected repairs typically set consumers back US$ 500 to US$ 600 on average.

The financial scope of mechanical repairs is substantial and varied. A simple oil change can cost anywhere from US$ 35 to US$ 125, and a tire rotation is typically between US$ 60 and US$ 70. However, when major systems fail, the costs can escalate dramatically, with some major repairs reaching up to US$ 10,000. By August 2025, the average repair cost is projected to be US$ 838, reflecting the growing complexity and cost of parts and labor in the automotive repair service market.

- The cost for major, non-routine services can range from US$ 296 to US$ 474 per job.

- Preventative maintenance is a significant driver of recurring revenue for mechanical repair shops.

- The high cost of new vehicles is encouraging owners to invest more in maintaining their current cars.

Passenger Vehicles are Primary Driving Force in Automotive Repair Demand

Holding a 48.14% share of the global market, passenger vehicles are the undeniable cornerstone of the automotive repair service market. The sheer volume of these vehicles in operation is a primary factor; in the United States alone, there were over 284 million registered vehicles in 2024. The average age of these vehicles continues to climb, from 12.5 years in 2023 to an estimated 12.8 years in 2025, leading to a higher frequency of necessary repairs. The cost of maintaining these vehicles varies significantly with age; a new car in 2025 might only require US$ 500 in annual maintenance, while a vehicle over ten years old can command a budget of US$ 1,500 to US$ 2,000.

The lifecycle of passenger vehicles also fuels this segment's dominance. Since 2020, approximately 27 million passenger cars have been scrapped, while only 13 million new ones were registered, indicating that older cars are being kept on the road longer. In contrast, 45 million new light trucks were registered while only 26 million were scrapped. Specific models illustrate the long-term repair costs; a Honda Accord is estimated to have a 10-year maintenance and repair cost of US$ 5,412, while a Mitsubishi Mirage has a 5-year cost of US$ 1,285, showcasing the consistent and predictable revenue stream within the automotive repair service market.

- The trend of keeping vehicles for longer periods is a direct contributor to market stability.

- The disparity between scrapped and newly registered vehicles highlights a growing repair-dependent fleet.

- Financing a new car is a major expense, making repairs a more economical choice.

Internal Combustion Engines are the Powerhouse of the Automotive Repair Service Market

Vehicles powered by internal combustion engines (ICE) hold the largest segmental share of 57.08%, underscoring their continued dominance in the global vehicle fleet and, consequently, the automotive repair service market. The sheer number of these vehicles on the road, with 283,027,600 ICE and hybrid vehicles in operation, ensures a steady stream of repair and maintenance work. An ICE powertrain is a complex piece of machinery with approximately 2,000 parts, a stark contrast to an electric vehicle powertrain which has only about 20. This complexity inherently leads to a higher potential for repair needs over the vehicle's lifespan.

The sales figures for 2024 further solidify the prevalence of ICE vehicles; approximately 14,182,468 new ICE and hybrid vehicles were sold, alongside 12,913,339 gasoline-powered vehicles specifically. In comparison, 1,233,458 new electric vehicles were sold during the same period. Even with the rise of electric mobility, the sales data from early 2025, with 185,992 EVs sold in January and February, shows that the vast majority of vehicles on the road will be powered by internal combustion for the foreseeable future, securing a dominant position for ICE-related services in the automotive repair service market.

- The established infrastructure for ICE repairs makes them more accessible and affordable.

- The vast and readily available inventory of ICE parts supports a quick and efficient repair process.

- Many consumers in various global markets still prefer the range and refueling convenience of ICE vehicles.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Independent Garages Takes the Lead as Trusted Neighborhood Hubs of Automotive Service

Independent garages command a substantial 38.02% of the automotive repair service market, a testament to their deep-rooted community presence and consumer trust. In 2024, the United States was home to 299,348 auto mechanic businesses, a number projected to grow to 302,754 by 2025. These establishments, with an average of five employees, are the backbone of the industry. The operational scale of these garages is significant; a typical shop services around 2.2 vehicles per bay each day. The average annual revenue for these businesses ranges from US$ 901,420 to a more robust US$ 1,226,000.

Despite their market leadership, independent garages face modern challenges. A significant operational hurdle is access to vehicle data, which costs the independent sector an estimated US$ 3.1 billion annually. This often results in lost revenue, with shops spending an uncompensated 2 to 4 hours on a vehicle before having to send it to a dealership. Operationally, these garages run on a lean model, with about 0.7 technicians per bay and one service advisor for every three bays, which underscores their efficiency and cost-effectiveness in the competitive automotive repair service market.

- There are approximately 79,429 independent auto repair shops in the United States.

- The growth in the number of independent garages indicates a healthy and expanding sector.

- The personal relationships built between customers and local mechanics foster high retention rates.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America: A Market Defined by High-Tech Workforce Advancement

North America proudly stands at the helm of the global automotive repair service market, holding a commanding 35.30% share. Its leadership isn't just about size; it's built on a deep, strategic investment in its people and the technology they use. The backbone of this strength is the region's vast and skilled workforce, with the U.S. alone boasting an estimated 887,000 technicians, of whom around 250,000 held ASE certifications in 2024. To nurture the next generation of talent, U.S. community colleges are aiming to graduate over 12,000 students with automotive technology degrees in 2025, while in Canada, over 5,000 new apprentices are expected to join automotive trades in 2024.

This focus on human expertise is matched by an enthusiastic embrace of cutting-edge technology in the automotive repair service market. In 2024, independent shops across the United States are on track to collectively invest a massive US$ 500 million in new diagnostic scanning and ADAS calibration tools. Looking ahead, it is forecasted that more than 4,000 specialized EV battery repair facilities will be operational across the continent by 2025. Service is also becoming more convenient, as Canadian mobile repair fleets are expected to grow to over 2,500 vehicles by 2025. In Mexico, the trend of consolidation continues, with the number of independent workshops joining larger chain networks anticipated to surpass 1,500 in 2024, ensuring a powerful and unified market presence.

Europe: Adapting to an Electric Future with Specialized Infrastructure

Europe’s automotive repair service market is in the midst of a deliberate and impressive transformation geared toward an all-electric future. In Germany, the heart of European automaking, there's a determined push to have over 40,000 technicians certified for high-voltage systems by the beginning of 2025. Across the channel in the United Kingdom, local garages are also making significant strides, planning to install an additional 15,000 EV charging points on their properties by the end of 2025. These efforts are a direct and practical response to the ever-growing number of electric cars gracing European roads.

This commitment to electrification is creating ripples across the service ecosystem. In France, for example, subscriptions by independent garages to OEM-specific diagnostic data platforms are expected to climb past 20,000 in 2024. In the UK, spending on essential MOT testing bay upgrades is forecasted to top US$ 100 million in 2024. Looking to the horizon, technical colleges across the continent are preparing for the next wave of innovation by introducing more than 300 new training modules focused on autonomous vehicle repair by 2025, ensuring the region remains at the forefront of automotive service.

Asia Pacific: Scaling Up Through Rapid Network and Franchise Expansion

The story of the Asia Pacific automotive repair service market is one of breathtaking scale and incredible speed. The region is undergoing a massive shift from fragmented, individual shops to powerful, organized service networks. In China, this consolidation is set to add an astounding 150,000 technicians to independent workshop chains in 2024 alone. India is on a similar path, with the number of multi-brand car service franchise locations expected to soar past 8,000 by 2025, bringing standardized, quality service to millions of vehicle owners.

This rapid growth is powered by substantial investment in technology and specialized skills. In Japan, the number of facilities equipped to handle second-life EV battery processing is forecasted to exceed 300 by 2025, creating a circular economy for batteries. Meanwhile, South Korea’s collision repair sector is projected to invest over US$ 80 million in eco-friendly waterborne paint systems in 2024. Underpinning all this progress is a deep commitment to education, with collective investment in automotive vocational skills training in China expected to reach a remarkable US$ 1 billion in 2024, securing the region's bright and dynamic future.

Recent Developments Shaping the Competitive Landscape of Automotive Repair Service Market

- Gerber Collision & Glass Expands Footprint: Continuing its relentless growth, Gerber acquired numerous independent collision repair centers across the U.S., significantly deepening its national service network.

- Repairify Acquires Automotive Training Group: Bridging the gap between technology and talent, diagnostics leader Repairify acquired ATG to embed world-class technical training directly into its service ecosystem.

- Valvoline Announces Major Refranchising Initiative : Valvoline strategically shifted its business model by refranchising 38 of its company-owned locations in Texas to Velocity Auto Care.

- ICV Partners Invests in Valvoline Franchisee : Showing strong faith in the franchise model in the automotive repair service market, private equity firm ICV Partners took a major stake in Interstate Auto Care, a 26-location Valvoline franchisee with big plans for expansion.

- AutoLeap Secures Series B Funding : The innovative shop management software provider, AutoLeap, successfully closed a major Series B funding round to fuel product innovation and market growth.

- Penske Automotive Group Acquires Don Allen Auto Service : Expanding its service portfolio, Penske Automotive Group purchased the well-regarded independent repair facility Don Allen Auto Service for US$ 12 million.

Top Companies in the Automotive Repair Service Market

- LKQ Corporation

- Asbury Automotive Group Inc.

- MEKO

- 3M Car Care Store

- Jiffy Lube International Inc

- CarMax Autocare Center

- Inter Cars S.A.

- USA automotive

- EUROPART

- M&M Automotive

- TVS Accessories

- Mobivia Groupe

- Sun Auto Service

- Hance's European

- Safelite Group

- Other Prominent Players

Market Segmentation Overview

By Service Type

- Mechanical Repairs

- Engine

- Transmission

- Suspension

- Others

- Electrical & Electronic Repairs

- Battery

- Wiring

- ADAS diagnostics

- Others

- Exterior & Structural Repairs

- Bodywork

- Paint

- Glass replacement

- Maintenance Services

- Oil Changes

- Fluid Checks

- Preventive Maintenance

By Vehicle Type

- Passenger Cars

- Hatchbacks

- Sedans

- SUVs

- MPVs

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Two-Wheelers / Motorcycles

- Three- Wheeler

By Service Provider

- Authorized dealerships

- Independent garages

- OEM-affiliated workshops

- Franchise General Repair

- Tire Shops & Repair Chains

- Others

By Propulsion Type

- Internal Combustion Engine (ICE)

- Petrol

- Diesel

- Electric

- Hybrid

By End Users

- Individuals

- Commercial Fleet Owners

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |