Brazil Industrial Gears Market: By Product Type (Spur Gear, Planetary Gear, Helical Gear, Rack and Pinion Gear, Worm Gear, Bevel Gear, Others); Material Type (Steel, Cast Iron, Aluminium Alloy, Nylon, Polycarbonate, Others); Shape Type (Elliptical, Triangular, Square); Design Type (Catalogue, Customized); Transmission (Manual and Automatic)—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 25-Jul-2025 | | Report ID: AA07251415

Market Scenario

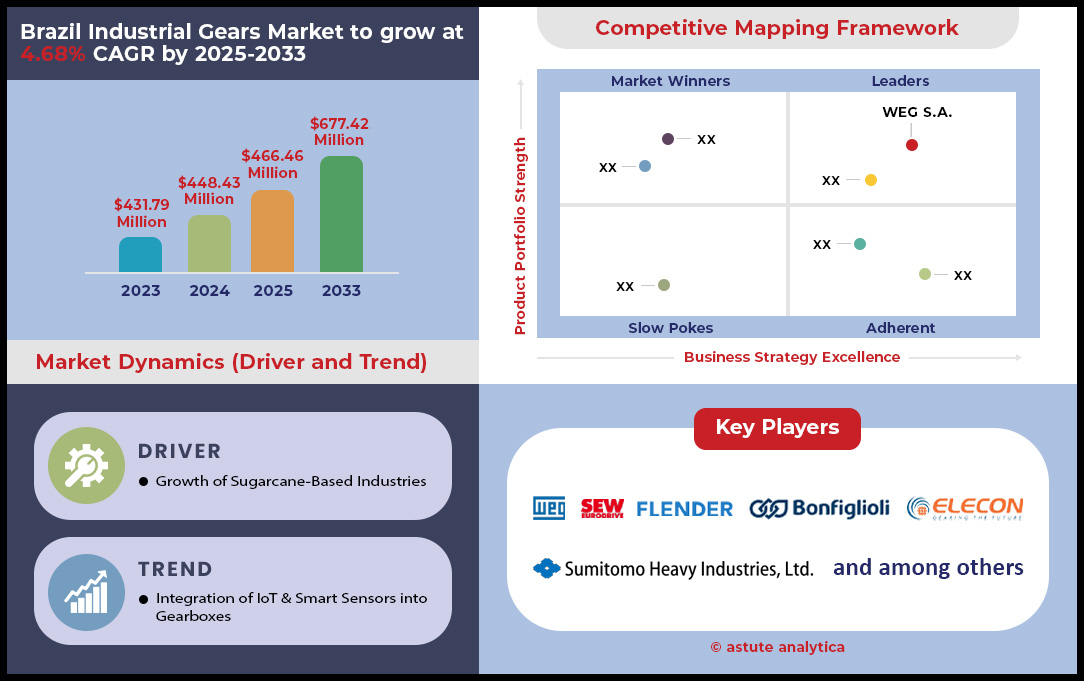

Brazil industrial gears market was valued at US$ 448.83 million in 2024 and is projected to hit the market valuation of US$ 677.42 million by 2033 at a CAGR of 4.68% during the forecast period 2025–2033.

The Brazil industrial gears market is poised for a historic growth cycle, fueled by a powerful convergence of private capital and public investment. A staggering BRL 11 billion investment from Toyota and a BRL 2.8 billion commitment from Nissan are set to drive automotive production towards a projected 2.75 million units in 2025, creating immense demand for precision gears. This is bolstered by a monumental BRL 1.7 trillion national infrastructure program (Novo PAC), with the BNDES alone budgeting up to BRL 160 billion for 2025, ensuring sustained demand for heavy machinery.

Further private investment in infrastructure in Brazil the industrial gears market is projected to reach BRL 372.3 billion by 2029, with São Paulo alone launching projects worth 19 billion BRL. The resource sector adds another layer of robust demand, with a $68.4 billion investment forecast for mining and a specific BRL 13.2 billion plan from CSN Mineração. Simultaneously, Brazil's push to add 10 GW of power capacity in 2025, underpinned by 97 offshore wind projects in evaluation, opens a high-value market for specialized turbine gearboxes. The rapid adoption of technology, evidenced by over 2,000 Starlink units sold for John Deere machinery, signals a wider industrial modernization that will rely on advanced, high-performance gears. This multi-sectoral boom creates an unprecedented and highly lucrative landscape for gear manufacturers.

To Get more Insights, Request A Free Sample

Trend Analysis: Brazil's Gear Market Pivots to Smart, Sustainable, and Custom Solutions

The industrial gears market in Brazil is undergoing a significant transformation, moving beyond traditional manufacturing to embrace the principles of Industry 4.0. The prevailing trend for 2025 is a decisive shift towards integrated, data-driven gearing solutions that prioritize efficiency, customization, and predictive capabilities. This evolution is propelled by Brazil's increasing investments in factory automation and the growing demand for precision in key sectors like automotive, mining, and renewable energy. A core aspect of this trend is the surge in demand for high-efficiency gear types, such as helical and planetary gearboxes, which are essential for modernizing Brazil's agricultural and mining machinery. Simultaneously, there's a pronounced move toward tailored gearboxes designed for specific, high-value applications, a niche where manufacturers can deliver enhanced performance and command premium pricing.

The most impactful trend reshaping the industrial gears market is the integration of predictive maintenance (PdM) technologies. The predictive maintenance market in Brazil is projected to grow at a remarkable CAGR of 24.2% between 2025 and 2033. This is fueled by the widespread adoption of the Industrial Internet of Things (IIoT), with sensors and AI-powered analytics enabling real-time monitoring of gear health to anticipate failures before they occur. This proactive approach significantly reduces costly unplanned downtime, which can average $260,000 per hour for manufacturers, and extends the lifespan of critical assets by as much as 20%. As companies increasingly leverage digital twins and smart platforms, the ability to offer gears with embedded intelligence and predictive analytics is becoming a powerful competitive differentiator in the Brazil market.

Capitalizing on Automotive Titans’ Multi-Billion Bets for Unprecedented Gear Market Dominance

The automotive sector presents the most immediate and high-volume opportunity within the Brazil industrial gears market. The announced investments are not merely for capacity expansion but for a technological evolution, demanding a new class of sophisticated gear systems. Toyota's 11 billion BRL investment, with a substantial 5 billion BRL being deployed by 2026, is directly tied to the production of a new hybrid-flex vehicle beginning in 2025. This pivot to hybrid technology translates into direct demand for complex planetary gearsets, power-split devices, and reduction gears that are fundamentally more advanced and hold higher value than traditional components.

Similarly, Nissan’s 2.8 billion BRL investment is funding the launch of two new SUV models and, crucially, a new turbo engine assembly line. New vehicle platforms and advanced turbocharged engines require entirely new gear geometries and materials, creating a significant R&D and supply opportunity. These specific, high-tech manufacturing plans, when multiplied across the projected 2.75 million vehicles to be produced and 2.8 million to be sold in 2025, illustrate a market shifting from commodity replacement to high-value, integrated powertrain solutions.

Unlocking Generational Profits from Brazil’s Massive Public and Private Infrastructure Investment

The sheer scale of planned infrastructure spending provides a long-term, foundational demand for heavy-duty industrial gears that will last for a decade or more in the Brazil industrial gears market . The government's 1.7 trillion BRL Novo PAC program acts as the bedrock, underwriting a generational renewal of the nation's core infrastructure. This is not a distant goal; it is an active market, with the Brazilian Development Bank (BNDES) injecting immediate liquidity through a financing budget of up to 160 billion BRL for 2025. This public funding is powerfully complemented by a projected 372.3 billion BRL in private infrastructure investment between 2025 and 2029.

The specific allocation of these funds to highways (288.6 billion BRL) and railways (168.9 billion BRL) provides a clear roadmap for gear manufacturers. This translates directly into sustained demand for gear systems in construction fleets (graders, excavators), material handling (conveyors, cranes), and transport (locomotives). The 19 billion BRL program for 55 projects in São Paulo further illustrates how this national strategy is cascading down to tangible, localized opportunities, guaranteeing a robust and predictable order book for suppliers to the Brazil industrial gears market.

Fueling Brazil’s Mining and Energy Sectors with Critical High-Performance Gear Technology

Brazil's resource and energy sectors offer a dual opportunity for both high-torque, heavy-duty gears and high-precision, specialized gearboxes. The mining industry's projected investment of $68.4 billion between 2025 and 2029 signals a massive wave of expansion and modernization. This is made concrete in the Brazil industrial gears market by CSN Mineração's 13.2 billion BRL plan to increase capacity, which necessitates new heavy-duty gear systems for crushers, grinding mills, and conveyors capable of withstanding extreme operational stress.

Simultaneously, Brazil's energy transition is creating an entirely new high-value market. The projection to add 10 GW of new power capacity in 2025, driven by the 97 offshore wind projects currently under evaluation, is a direct catalyst for the wind turbine gearbox market—one of the most complex and valuable applications for gear technology. Finally, the rapid uptake of over 2,000 Starlink units on John Deere machinery since January 2025 is a powerful indicator of a wider trend: the modernization of Brazil's primary industries. This drive for precision and efficiency requires more sophisticated machinery, which in turn depends on more advanced and reliable gears, solidifying the long-term potential of the Brazil industrial gears market.

Segmental Analysis

By Product: Helical Gear Driving Revenue and Efficiency in Brazil's Demanding Industrial Landscape

The market dominance of helical gears within the Brazilian industrial gears market by capturing more than 31.95% market share is a direct result of their superior engineering characteristics. Wherein, they are perfectly aligned with the operational demands of the nation's key economic sectors. Unlike spur gears, the angled teeth of helical gears engage more gradually, a design that yields smoother and quieter operation. This quality is paramount in applications requiring constant power transmission with minimal vibration, such as in the expansive mining, agriculture, and automotive manufacturing industries. The inherent efficiency and high load-bearing capacity of these gears make them the undisputed choice for heavy-duty machinery. From the powerful conveyor systems in mineral extraction to the robust drivetrains of agricultural harvesters, helical gears provide the reliability and performance necessary to minimize downtime and maximize productivity, cementing their position as the highest revenue-generating gear type.

The statistical evidence supporting their leadership in the country’s industrial gears market is compelling and widespread across industries. Within Brazil's formidable mining sector, it is noted that more than 70% of gearboxes in heavy-duty trucks now depend on helical gear sets for their final drive. In agriculture, the durability is quantified by the average operational lifespan of helical gears in sugarcane harvesters, which reaches approximately 15,000 hours. The efficiency gains are tangible, with conveyor systems in Brazilian ports realizing an 8-10% improvement and industrial noise levels dropping by 15-20 decibels. Their superior strength is highlighted by a load capacity that is typically 25% higher than spur gears of a similar size. This performance has led to their standardization in over 90% of high-torque agricultural applications and in the main spindle drives of over 80% of machine tools manufactured in the country.

Why Steel Remains the Uncontested Material of Choice for Brazilian Gear Manufacturing

Steel's position, 52% market share, as the most dominant material for industrial gear production in Brazil is secured by a powerful combination of intrinsic strength, manufacturing viability, and strategic economic advantages. The material's fundamental properties, including exceptional hardness and high tensile strength, make it uniquely capable of withstanding the extreme stress and heavy loads characteristic of industrial operations. Furthermore, steel's versatility allows for various heat treatments and alloying processes, enabling manufacturers in the Brazil industrial gears market to customize gears with specific performance characteristics tailored to diverse applications. Critically, Brazil's status as a major global steel producer provides local gear manufacturers with a stable, cost-effective, and readily available supply of raw materials. This domestic capacity insulates the industry from the price volatility and logistical challenges of importing alternative materials, reinforcing steel’s economic and practical supremacy in the market.

The data overwhelmingly confirms steel's foundational role. An estimated 95% of all industrial gears manufactured in Brazil are forged from a steel alloy, a decision heavily influenced by cost; raw steel is approximately 30-40% cheaper than imported specialized alloys. The nation's domestic steelworks are robust enough to meet over 90% of the demand from its gear manufacturers in the industrial gears market, which drastically reduces production lead times by an average of 4-6 weeks. This reliance is evident in sectors like the sugar and ethanol industry, where high-strength carbon steel is used almost exclusively. The sustainability of steel is also a factor, with a recycling rate from decommissioned machinery exceeding 80%. This dominance is further reflected in the high number of local foundries specializing in steel casting and in Brazilian technical standards, which consistently specify steel as the default material for gearing.

By Shape: Elliptical Gears to Continue Holding Market Dominance

A precise understanding of the Brazil industrial gears market reveals that its core is built upon the widespread application of elliptical gear shape, not specialized or niche designs. Currently, the segment is controlling nearly 69.11% market share. The market's volume and revenue are overwhelmingly driven by helical, bevel, spur, and worm gears. These designs are fundamental to machinery across all major industries because they provide the consistent and reliable power transmission required for most industrial processes. In contrast, non-circular gears, such as elliptical gears, serve a very different purpose. They are engineered to produce a variable output speed or torque from a constant input speed. This unique function limits their application to highly specialized machinery, such as specific models of textile machines, automated packaging equipment, or custom robotics, where a fluctuating motion profile is a deliberate design requirement.

Consequently, elliptical gears are technologically significant as they represent a substantial share of adoption or deployment in the broader Brazilian industrial context. The primary demand within the nation's heavy industries—mining, construction, agriculture, and energy—is for the relentless and predictable transfer of power. A mining conveyor, a tractor's powertrain, or a wind turbine's gearbox requires the steadfast performance delivered by conventional gearing.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By Transmission: Manual Transmissions to Continue Their Enduring Dominance in the Brazilian Automotive Sector

Manual transmission to continue holding more than 62.75% in the Brazil industrial gears market. Wherein, highest penetration of manual gearboxes highlights a deeply entrenched market reality in Brazil. This enduring dominance over automatic transmissions is rooted in a pragmatic blend of economic factors, maintenance considerations, and consumer preferences. The primary driver is cost; vehicles equipped with manual transmissions are considerably less expensive to manufacture, a saving that is passed directly to the consumer at the point of sale. For a large segment of the Brazilian population, this lower initial purchase price is a decisive factor. Beyond the showroom, manual transmissions are mechanically simpler, leading to a reputation for robustness and significantly lower repair costs over the vehicle's lifespan. This long-term economic benefit is highly valued by both private car owners and commercial fleet operators who prioritize reliability and manageable operating expenses.

The supporting data paints a clear picture of this industrial gears market preference. The price gap between manual and automatic versions of the same car model in Brazil frequently stands between R5,000 and R7,000. This trend is even more pronounced in the commercial sector, where over 85% of light commercial vehicles sold in 2024 featured manual transmissions. The cost of a major repair on an automatic transmission is, on average, two to three times higher than for a manual one. This has led large logistics companies to continue prioritizing manual trucks for their fleets. This preference is reinforced early, as over 70% of new drivers learn on a manual vehicle. Furthermore, the aftermarket strongly favors manuals with wider availability of spare parts and a significantly larger number of qualified mechanics, making them the practical and economical choice for the majority of the Brazilian vehicle market.

To Understand More About this Research: Request A Free Sample

10 Major Developments in Brazil’s Industrial Gears Market Showing How Market Players are Reactive to Gain a Competitive Edge

- Toyota's Landmark Automotive Investment (Announced Feb 2024): Toyota announced a monumental investment of 11 billion BRL (approx. $2.2 billion USD) in its Brazilian operations through 2030. A significant portion, 5 billion BRL, is slated for 2024-2026 to produce a new compact hybrid-flex car and another hybrid vehicle, directly driving demand for advanced transmission gears and powertrain components.

- Great Wall Motor's Production Start (Q2 2024): Chinese automaker Great Wall Motor (GWM) commenced the modernization of its factory in Iracemápolis, São Paulo, in the second quarter of 2024. This is part of a larger 10 billion BRL investment plan through 2032, with the first hybrid vehicles expected to roll off the production line in the first half of 2025, creating a new, large-scale consumer of precision gears.

- BNDES's Substantial 2025 Financing Budget (Announced 2024): The Brazilian Development Bank (BNDES) has confirmed a financing budget of approximately 150-160 billion BRL for 2025. This funding is critical for companies across sectors like infrastructure and manufacturing to acquire new machinery, directly fueling the order books for industrial gears market’s suppliers.

- CSN Mineração's Massive Expansion Funding (Announced 2024): Mining giant CSN Mineração announced a 13.2 billion BRL investment plan for the 2025-2030 period. The goal is to significantly expand its iron ore production capacity, which will require substantial investment in new heavy-duty gear systems for conveyors, grinding mills, and heavy mobile equipment.

- Nissan's Ongoing Investment Cycle (2023-2025): Nissan is in the midst of a 2.8 billion BRL investment cycle at its Resende plant, which concludes in 2025. This funding is being actively used to prepare for the production of two new SUV models and to assemble a new turbo engine, driving immediate and ongoing demand for specialized automotive gears.

- John Deere's Construction Division Expansion (Announced Feb 2024): Reflecting strong demand in the construction and forestry sectors, John Deere announced the hiring of more than 200 new employees for its division in Brazil. This expansion is directly tied to the launch of a new motor grader line, indicating growth in heavy machinery production that relies on robust gearboxes.

- BYD's New Manufacturing Hub Investment (Confirmed 2024): Chinese electric vehicle giant BYD has confirmed an investment of 3 billion BRL to establish a new manufacturing complex in Camaçari, Bahia. The plant is scheduled to begin operations in late 2024 or early 2025, creating a significant new demand center for EV-specific gear systems and reducers.

- Weg's Continuous Expansion Investments (Ongoing 2024/2025): Weg, a major Brazilian motor and industrial equipment manufacturer, continues its aggressive investment in expanding its production capacity. In 2024, the company announced investments to expand motor production in Brazil and gearbox production in its overseas plants that supply the Brazilian industrial gears market, reflecting strong demand for integrated powertrain solutions.

- São Paulo's Major Infrastructure Program (Announced 2024): The city of São Paulo has initiated a program featuring 55 major projects with a combined investment of around 19 billion BRL. As these projects move into execution in 2025, they will drive significant demand for construction machinery and other industrial equipment, all dependent on industrial gears.

- Mining Sector's Long-Term Investment Forecast (Updated 2024): Brazil's mining industry association, IBRAM, has forecast total sector investments of $68.4 billion for the 2025-2029 period. This long-term, high-value investment pipeline provides a strong and predictable demand forecast for suppliers of heavy-duty and specialized gears for mining operations.

Top Companies in the Brazil Industrial Gears Market

- Sumitomo Drive Technologies

- Anant Engineering

- SEW-EURODRIVE

- Flender

- HAR Engineering

- Other Prominent Players

Market Segmentation Overview

By Product Type

- Spur Gear

- Planetary Gear

- Helical Gear

- Rack and Pinion Gear

- Worm Gear

- Bevel Gear

- Others

By Material Type

- Steel

- Cast Iron

- Aluminium Alloy

- Nylon

- Polycarbonate

- Others

By Shape Type

- Elliptical

- Triangular

- Square

By Design Type

- Catalogue

- Customized

By Transmission Type

- Manual

- Automatic

By Industry

- Automotive

- Metalworks

- Sugarcane

- Wind Energy

- Oil and Gas

- Agribusiness

- Aeronautics

- Others

By Distribution Channel

- Online

- Offline

- OEMs

- Aftermarket

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |