Digital Surgery Technologies Market: By Component (Hardware, Software, and Service); Product Type (Surgical Navigation & Advanced Visualization , Surgical Simulation, Surgical Planning, Surgical Data Science); Technology (AI and Big Data, IoT and Robotics, Extended Reality (ER: AR/VR/MR), and Others); Application (General Surgery, Neurological Surgery, Cardiovascular Surgery, Orthopedics Surgery, Urology Surgery, Gynecological Surgery, Ophthalmological Surgery, and Others); End Users (Hospitals, Ambulatory Surgical Centers, Clinics, and Others); Region—Market Analysis and Forecast for 2025–2033

- Last Updated: 29-Oct-2025 | | Report ID: AA0723543

Market Snapshot

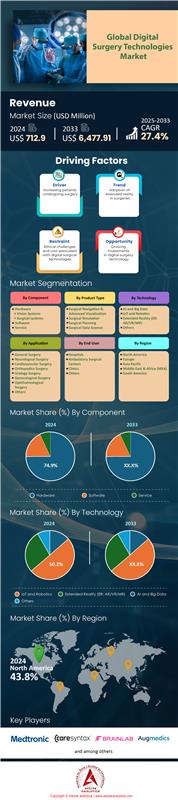

Digital surgery technologies market was valued at US$ 712.9 million in 2024 and is projected to attain a valuation of US$ 6,477.91 million by 2033 at a CAGR of 27.4% during the forecast period 2025–2033.

Key Findings Shaping the Market

- Based on Product, the surgical navigation and advanced visualization segment held the majority market share, accounting for over 59.8% of the global market.

- Based on technology, IoT and robotics segment captured the largest share, accounting for over 50.2% of the global market.

- When it comes to application, gynecological surgery dominated the global digital surgery technologies market with a substantial share of 27.6%.

- North America holds the lion’s share of over 43.80%.

A dramatic escalation in procedural volume is creating powerful momentum within the Digital surgery technologies market. For instance, a projected 3 million surgeries will be performed by robots annually in 2024. Specifically, Intuitive Surgical's systems were used in 2,683,000 procedures in 2024 alone. Consequently, system installations are accelerating; the company placed 493 da Vinci systems in the last quarter of 2024 and another 427 systems in Q3 2025. As a result, the total installed base of da Vinci systems reached 10,763 by September 2025. These figures clearly indicate a soaring demand for digital surgery platforms from healthcare providers worldwide.

Furthermore, this demand is expanding into new care environments. The number of Medicare-certified ASCs grew to 6,377 in 2024, opening a significant new channel for technology adoption. In addition, surgeon enthusiasm is a critical demand driver; more than 60,000 surgeons have received training on da Vinci Systems as of 2024. Moreover, over 2,500 surgeons are already utilizing the new da Vinci 5 system, showcasing rapid uptake of next-generation platforms. The training of over 15,000 medical professionals by CAE Inc. in 2024 further signifies a deep-seated reliance on these advanced surgical tools.

Underpinning this growth is strong financial confidence and a favorable regulatory climate in the digital surgery technologies market. Robotics startups attracted an impressive $4.2 billion in funding in the first half of 2024. High-value investments, such as MMI's $110 million raise in February 2024, confirm strong investor belief. Concurrently, regulatory pathways are becoming more established. More than 200 AI-based medical devices are forecasted for FDA authorization in 2024. Indeed, GE HealthCare already possesses 100 FDA-cleared AI tools as of 2025, providing a solid foundation for continued market expansion.

To Get more Insights, Request A Free Sample

Unlocking New Opportunities in the Digital Surgery Technologies Market

- The advent of surgical nanorobotics marks a pivotal opportunity: These microscopic robots, capable of navigating the human vascular system, are moving from theoretical models to practical applications. Early-stage companies are attracting significant venture capital for developing nanobots designed for ultra-precise drug delivery to cancer cells and for clearing arterial blockages. The potential to perform procedures at a cellular level opens up entirely new therapeutic areas and creates a demand for sophisticated control and imaging systems, representing a multi-billion dollar sub-market in the making.

- Augmented Reality (AR) overlays are creating the next wave of surgical navigation: Beyond simple visualization, AR systems in the digital surgery technologies market are now integrating real-time patient data, advanced imaging, and AI-driven predictive analytics directly into the surgeon's field of view. This creates a "digital twin" of the patient on the operating table. Companies are developing AR headsets and software that reduce cognitive load and improve surgical accuracy by projecting critical information onto the patient. The opportunity lies in creating seamless, intuitive platforms that can be integrated with existing robotic systems, enhancing surgical precision and shortening procedure times.

Healthcare Institutions Make Substantial, Long-Term Financial Commitments

Healthcare institutions are making substantial, long-term financial commitments, underscoring the escalating demand within the digital surgery technologies market. Hospitals are now frequently engaging in multi-year acquisition plans, with over 300 signing lease-to-own agreements for next-generation surgical robots in 2024. In a clear example of this trend, one leading health network earmarked $150 million for robotic system acquisitions through 2025. The upfront investment is significant, as the average capital expenditure for a single robotic surgery suite in new hospital construction now exceeds $3.5 million. This commitment extends beyond the initial purchase, with hospitals spending an average of $175,000 annually per machine on service contracts.

Moreover, the infrastructure to support these systems is a key investment area in the digital surgery technologies market. In 2024, at least 500 medical centers initiated operating room upgrades to accommodate new robotic platforms. The demand for specialized talent is also reflected in financial planning, with over 1,200 new positions for robotic surgery coordinators being funded in 2024. Additionally, hospitals are investing heavily in data infrastructure, spending an average of $500,000 per facility on surgical data analytics platforms. To support these programs, philanthropic donations for robotic surgery centers at hospitals exceeded $200 million in 2024, while teaching hospitals purchased 800 robotic surgery training simulators. As a result, over 400 hospitals have established dedicated steering committees to manage these ongoing investments.

Surging Procedural Tooling Consumption Reflects Deep Clinical Integration

The consistent and growing consumption of procedure-specific instruments highlights the deep clinical integration shaping the digital surgery technologies market. Every robotic procedure requires disposable or limited-use tools, creating a substantial revenue stream. In 2024, for instance, the number of individual robotic instrument trays shipped globally surpassed 4 million units. Specifically, sales of proprietary robotic stapling and vessel sealing instruments are projected to reach 1.5 million units in 2025. The cost of these consumables is significant, as the average for a single prostatectomy was approximately $2,800 in 2024. Consequently, a high-volume hospital can easily spend over $2 million annually on robotic surgical consumables alone.

The demand for tooling is becoming more specialized across the global digital surgery technologies market. For instance, more than 50 new, highly specialized robotic instruments for niche procedures were launched in 2024. The supply chain has expanded to meet this need, with over 100 third-party manufacturers now producing compatible accessories. Furthermore, the logistics of managing these supplies have grown, with an estimated 25,000 hospital supply chain professionals now involved in procurement. The market for related items like robotic endoscope sheaths and cleaning systems also saw significant growth, with sales reaching 5 million units in 2024. Finally, with over 1,200 patents filed for novel robotic surgical instruments and ambulatory surgery centers ordering over 5,000 instrument starter kits in 2024, both innovation and market expansion are accelerating.

Segmental Analysis

Surgical Navigation and Visualization Leads with Unprecedented Clarity

The surgical navigation and advanced visualization segment's commanding 59.8% share of the digital surgery technologies market is driven by the critical need for precision in complex procedures. Surgeons increasingly rely on these systems to provide a detailed, real-time map of the patient's anatomy, which is crucial for minimizing invasiveness and improving outcomes. The integration of technologies like augmented reality overlays and 3D imaging provides "GPS-like" guidance, a factor underscored by significant investment and innovation. For instance, in 2024, AI-powered 3D medical imaging firm Axial3D secured $18.2 million in funding to advance patient-specific surgical solutions. This investment trend is further highlighted by the venture capital funding for surgical robotics startups, which exceeded $860 million in 2023 and continued to attract investors in 2024.

The momentum is also evident in regulatory approvals and new product launches. In 2024, Johnson & Johnson planned to submit its Ottava soft-tissue surgical robotics system for an FDA investigational device exemption to begin clinical trials. Similarly, a new FDA clearance was granted in 2024 for Zeta Surgical's Cranial Navigation System, enhancing its software and accessory compatibility in the digital surgery technologies market. A4Lab is also pursuing FDA approval in 2025 for its surgical navigation system that reduces surgery preparation time to one minute. These advancements are expanding the applications of advanced imaging across various surgical specialties. The global market for 3D printed surgical models, a key visualization tool, was valued at $68.62 billion in 2024. Furthermore, a 2024 survey involving 1,000 U.S. surgeons revealed that 85% believe technologies like virtual reality could significantly improve surgical training. The global C-arms market, essential for real-time imaging, was sized at $2.32 billion in 2025.

- Amsterdam-based Surgical Reality secured new funding in 2025 to advance its 3D surgical imaging technology.

- The 22nd Annual Advanced Imaging Methods Workshop in January 2025 will bring together researchers to discuss emerging microscopy techniques.

- In November 2025, a conference will be held to discuss clinical trials in intraoperative molecular imaging for cancer surgery.

Gynecological Surgery Leads Application with High Adoption of Robotics

Gynecological surgery has secured a substantial 27.6% share of the digital surgery technologies market, making it a leading application area. This dominance is primarily due to the high volume of procedures such as hysterectomies and myomectomies, which significantly benefit from the precision and minimally invasive approach offered by robotic systems. The complexity of these procedures, often performed in confined pelvic spaces, makes the enhanced dexterity and 3D visualization of robotic platforms particularly advantageous, leading to reduced blood loss, shorter hospital stays, and faster patient recovery. The global surgical robotics market for gynecological applications was valued at $3.1 billion in 2023 and is projected to grow.

The high adoption rate is reflected in the sheer number of procedures in the digital surgery technologies market. Since its introduction, over 14 million robotic surgeries have been performed across all specialties, with gynecology being a major contributor. A bibliometric analysis of robotic surgery in gynecologic oncology identified 561 relevant publications between 2005 and 2025, indicating robust research activity. The demand is also driving innovation in specialized robotic platforms. In October 2025, Medtronic initiated a clinical study for its Hugo™ RAS system for use in gynecological procedures, which will enroll up to 70 patients across five U.S. hospitals. Furthermore, single-port robotic surgery is a rapidly evolving technique, with a comprehensive literature search in February 2024 highlighting its growing use in gynecology. The number of surgeons trained in robotic surgery has now surpassed 76,000 worldwide.

- In 2024, Moon Surgical's Maestro system, used in over 200 gynecologic and other surgeries, received FDA clearance, with a broader launch expected in 2025.

- A retrospective study published in 2025 analyzed 260 patients who underwent robotic myomectomy between 2013 and May 2024.

- By the end of 2025, it is estimated that nearly 111,000 U.S. women will have been diagnosed with a gynecological cancer, many requiring surgery.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

IoT and Robotics Revolutionize Surgical Procedures with Smart Automation

The IoT and robotics segment has captured a dominant 50.2% share of the global digital surgery technologies market, fundamentally reshaping the operating room. The driver behind this dominance is the technology's ability to enhance surgical precision, reduce recovery times, and enable less invasive procedures. The rapid adoption of systems like Intuitive Surgical's da Vinci platform illustrates the industry's trajectory. In 2024, approximately 2.68 million procedures were performed with da Vinci systems. The company's momentum continued with the placement of 1,526 da Vinci systems in 2024, an increase from 1,370 in 2023. By the end of 2024, the total installed base of Intuitive's systems surpassed 10,600 units.

The financial investment in this sector underscores its significance in the digital surgery technologies market. By September 2025, surgical robotics companies had raised $462 million in equity funding, a substantial increase from the $305 million raised by the same point in 2024. Innovation is also a key factor, with Intuitive Surgical placing 362 of its new da Vinci 5 systems in 2024 following its FDA clearance in March. These next-generation systems have already been used in over 32,000 procedures during their initial commercialization phase in 2024. The installed base is projected to grow, with the number of da Vinci systems reaching 10,763 by the third quarter of 2025. Further illustrating the growth, 20 remote robotic-assisted procedures were successfully demonstrated in a 2024 preclinical trial. By June 2024, Meril's MISSO surgical robot for knee replacement was also launched.

- The total number of cumulative procedures performed on da Vinci platforms is now close to 17 million.

- Looking ahead, Intuitive Surgical anticipates a 13% to 16% procedure volume growth for da Vinci in 2025.

- The first remote surgery in space was successfully performed in 2024, demonstrating the feasibility of telesurgery.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America Sustains Unrivaled Digital Surgery Technology Adoption and Leadership in Digital Surgery Technologies Market

North America, commanding over 43.80% of the market, continues to be the epicenter of the market through substantial investment and deep clinical integration. The sheer volume of procedures underscores this dominance, with over 2.6 million surgeries involving robots occurring in the United States during 2024. Notably, this figure represents a significant increase from the previous year. Furthermore, Canadian hospitals are rapidly expanding their capabilities, with plans for at least 40 new robotic system installations slated for 2025. Investment in specialized training is also robust, as evidenced by the more than 600 robotic surgery fellowship positions offered across the U.S. and Canada for the 2025 academic year.

The expansion into outpatient settings is a critical growth driver. For instance, in the U.S. digital surgery technologies market, over 800 ambulatory surgery centers integrated robotic-assisted surgery platforms in 2024. Moreover, U.S. medical device companies collectively invested more than $4 billion in surgical robotics R&D in 2024. This financial commitment is fueling innovation, which is clearly demonstrated by the 5,000th installation of Philips' Zenition mobile C-arm system in a U.S. facility in late 2025. In another key development, the U.S. Veterans Health Administration performed over 15,000 robotic surgical procedures in 2024. In addition, U.S. hospitals purchased more than 1,000 new surgical simulation systems in 2024. Finally, at least 250 American hospitals now operate five or more distinct surgical robotic systems, indicating widespread, facility-level adoption.

Asia Pacific Emerges as a Global Hub for Rapid Innovation

The digital surgery technologies market in Asia Pacific is characterized by explosive growth and homegrown innovation. China is a formidable force, with its domestic manufacturers installing over 300 new surgical robots in Chinese hospitals in 2024. Impressively, the nation also achieved a major milestone in November 2024 by setting a world record with a 12,000-kilometer intercontinental telesurgery procedure. In parallel, India is making significant strides, performing approximately 60,000 robot-assisted operations in 2024 with an installed base of over 170 robots. Specifically, the country's domestic SSI Mantra system has already been used in over 150 urological procedures since its recent approval. Meanwhile, Japan's Hinotori system, approved in 2020, is now operational in more than 40 Japanese hospitals. Similarly, the South Korean-developed Revo-i system is gaining international traction, securing purchase orders from 8 different countries as of early 2025.

Europe Focuses on Deep Clinical Integration and Specialized Training

Europe is solidifying its position in the digital surgery technologies market through methodical adoption and a strong emphasis on surgeon education. For example, the UK's National Health Service (NHS) is driving significant volume, currently performing 70,000 robot-assisted minimally invasive surgeries annually. Likewise, in Germany, the number of robotic-assisted knee and hip replacement surgeries surpassed 25,000 in 2024, demonstrating deep penetration in orthopedics. Training remains a major priority across the continent. To illustrate, the ORSI Academy in Belgium trained over 1,000 surgeons from various countries on advanced robotic techniques in 2024. Meanwhile, France allocated more than 50 research grants specifically for the development of AI-driven surgical platforms in 2024. Reflecting this investment in innovation, the Spanish company Rob Surgical is on track to install 50 of its new Bitrack systems in European hospitals by 2025. Ultimately, more than 30 pan-European clinical trials for new robotic surgery platforms were initiated in 2024, signaling a robust future.

Top 9 Recent Developments in Digital Surgery Technologies Market

- Distalmotion secured over $130 million in a financing round led by Revival Healthcare in September 2024 to accelerate the commercial expansion of its Dexter surgical robot across Europe.

- Noah Medical raised $150 million in a Series B funding round in April 2023 to scale its Galaxy System, a robotic platform for navigated bronchoscopy.

- Medical Microinstruments (MMI) raised $110 million in a Series C financing round in February 2024, supporting expansion of its Symani Surgical System for microsurgical procedures.

- Moon Surgical secured $55.4 million in a financing round in May 2023 to support the commercial launch of its Maestro Robotic System for laparoscopic surgery.

- Karl Storz announced its intent and moved to acquire Asensus Surgical in April 2024, integrating advanced digital and robotic surgical capabilities.

- Ronovo Surgical closed a $67 million Series D funding round in September 2025, led by Johnson & Johnson’s venture arm, to advance its Carina robotic platform.

- EndoQuest Robotics secured $42 million in a Series C financing round in April 2024 to further develop its flexible endoluminal robotic system for gastrointestinal interventions.

- Stryker completed its acquisition of Artelon in June 2024, enhancing its soft tissue fixation portfolio relevant to robotic and biologic repair procedures.

- Agilis Robotics raised approximately $10–13 million in funding between late 2023 and 2024 for its flexible robotic platform for urological surgeries.

Key Players in the Global Digital Surgery Technologies Market

- Augmedics Ltd.

- Brainlab AG

- Caresyntax Inc

- Centerline Biomedical

- DASH Analytics

- EchoPixel Inc.

- FundamentalVR

- Medtronic plc

- Mimic Technologies, Inc.

- Novadaq Technologies Inc.

- Osso VR Inc.

- Surgical Science Sweden AB

- VirtaMed AG

- Other Prominent Players

Market Segmentation Overview:

By Component

- Hardware

- Vision Systems

- Surgical Systems

- Software

- Service

By Product Type

- Surgical Navigation & Advanced Visualization

- Surgical Simulation

- Surgical Planning

- Surgical Data Science

By Technology

- AI and Big Data

- IoT and Robotics

- Extended Reality (ER: AR/VR/MR)

- Others

By Application

- General Surgery

- Neurological Surgery

- Cardiovascular Surgery

- Orthopedics Surgery

- Urology Surgery

- Gynecological Surgery

- Ophthalmological Surgery

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers

- Clinics

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |