Flue Gas Treatment Systems Market: By Pollutant Control System (Flue Gas Desulfurization (FGD) Systems, DeNOX Systems, Particulate Control Systems, Mercury Control Systems, Others); Process (Wet, Semi-wet, Dry); Industry (Industrial Boilers, Power, Chemical & Petrochemical, Iron & Steel, Non-Ferrous metal, Cement, Waste Treatment); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 08-Nov-2025 | | Report ID: AA0824888

Market Snapshot

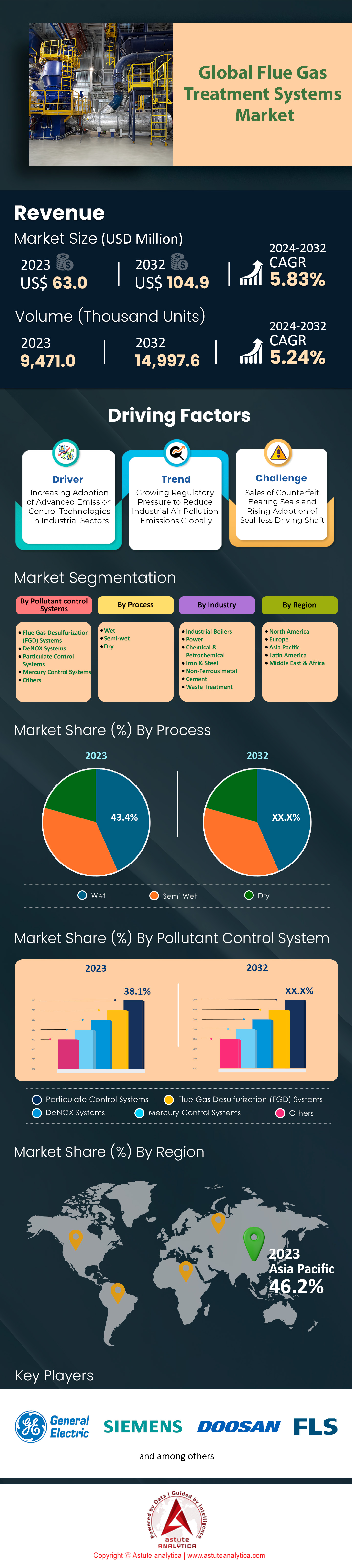

Flue gas treatment systems market was valued at US$ 66.67 million in 2024 and is projected to hit the market valuation of US$ 111.02 million by 2033 at a CAGR of 5.83% during the forecast period 2025–2033.

Key Findings

- Based on pollutant control system, articulate control system is currently dominating the market with over 38.1% revenue share.

- Based on process, the wet process of flue gas treatment systems stands out as the most dominant method with revenue share of over 43.4%.

- By industry, power industry captured the highest revenue share of over 43.6% of the market.

- Asia Pacific to continue leading the market.

- Global flue gas treatment systems market to reach valuation of US$ 111.02 million by 2033.

From the last few years, demand in the flue gas treatment systems market has been solidifying around regulatory compulsion and industrial necessity. Primarily, a stringent global policy landscape is creating non-negotiable demand. For instance, China’s approval of 182 new FGD projects and India's government funding for 96 additional installations exemplify this trend. Similarly, the maritime sector is a critical demand center, now contending with at least 93 global bans on scrubber washwater discharges. Consequently, this compliance-driven environment establishes a baseline of consistent, legally mandated demand for advanced emission control technologies.

In addition to policy, the sheer scale of industrial and energy sector growth provides a second powerful demand pillar for the flue gas treatment systems market. This is evidenced by the more than 6,000 new power plants under development globally in 2024, each representing a potential system installation. Investment is flowing accordingly; Asia, for example, allocated over US$ 14.5 billion to emission control infrastructure in 2024. Furthermore, specific projects like Uzbekistan's US$ 1.3 billion investment in new waste-to-energy plants highlight the significant capital being deployed. This translates into tangible operational demand, illustrated by the consumption of over 43 million metric tons of limestone for FGD applications in 2024 alone.

Looking forward, future growth of the flue gas treatment systems market is intrinsically linked to the global energy transition and robust financial backing. The ongoing expansion of nuclear power, with about 70 reactors currently under construction across 15 countries, signals a long-term, evolving need for specialized treatment systems. Moreover, the surge in renewables, such as the planned deployment of 23 gigawatts of new clean power capacity in the APAC region in 2025, reinforces the broader push for environmental responsibility. Financially, the sector is exceptionally well-supported, a fact underscored by the US$ 4.4 trillion market capitalization held by publicly-listed low-carbon solution providers as of mid-2024.

To Get more Insights, Request A Free Sample

Emerging Opportunities For Advanced Flue Gas Treatment Systems

- Digitalization and AI-Driven Optimization: A primary opportunity is materializing from the integration of digital technologies, specifically IoT and Artificial Intelligence. AI-driven platforms can meticulously optimize combustion processes in real-time, resulting in substantial efficiency improvements. For example, a 2025 analysis of AI integration in waste-to-energy incinerators showed a power generation efficiency increase of over 1.7% in the flue gas treatment systems market. Moreover, the same analysis reported that the plant’s heat rate was reduced by approximately 58 kcal/kWh. This level of digital optimization not only lowers operational expenditures but also refines the precision of emission control, thereby creating a compelling value proposition for operators.

- By-Product Valorization: A second, equally powerful trend is the strategic conversion of captured pollutants into commercially viable products. Flue gas desulfurization (FGD) systems, for instance, produce synthetic gypsum, which is a highly sought-after raw material in the construction sector. In fact, global demand for FGD gypsum specifically for the wallboard industry is projected to reach 99.5 million tons per year in 2025. Similarly, captured fly ash is being increasingly repurposed for use in cement and concrete production. This "waste-to-value" model effectively transforms a compliance-related expense into a profitable revenue stream, aligning perfectly with circular economy objectives.

Circular Economy Principles Transforming Industrial By-Products Into Assets

A pivotal aspect currently defining the flue gas treatment systems market is the adoption of circular economy models, which focus on valorizing industrial by-products. This strategic shift is turning former waste streams into valuable assets, thereby creating a strong economic incentive for investment. The market for synthetic gypsum, a direct by-product of FGD systems, is particularly robust. For 2025, the global synthetic gypsum market is estimated to reach a value of US$ 1.75 billion. The demand is primarily fueled by the construction sector, where FGD gypsum is a key component for drywall and cement. Specifically, the global demand from the wallboard industry alone is projected to reach 99.5 million tons per year in 2025.

Furthermore, this trend is reinforced by the expanding reuse of other captured materials in the flue gas treatment systems market. The global fly ash market, another crucial by-product, achieved a value of US$ 13.9 billion in 2024. In the United States alone, total fly ash utilization is forecasted to increase to 27.8 million short tons by 2039. In addition, emerging carbon dioxide utilization technologies are creating new commercial pathways for captured CO2 in products like fuels, chemicals, and polymers. To illustrate, the total annual production capacity of polycarbonate resin using captured CO2 has already reached 1 million tons. The value of the U.S. carbon dioxide utilization market was estimated at US$ 1.68 billion in 2024 and is projected to expand to US$ 4.52 billion by 2032.

Blue Hydrogen Production Surge Is Creating A New Demand Frontier

The rapid acceleration of blue hydrogen production represents a significant and defining new demand driver for the flue gas treatment systems market. Critically, blue hydrogen is produced using steam methane reforming (SMR), a process that inherently generates a CO2-rich flue gas stream. This stream requires capture and treatment, directly linking hydrogen production to emission control. As nations invest heavily in hydrogen infrastructure, the corresponding need for these systems is soaring. In 2025, the U.S. blue hydrogen sector is expected to see over 1.5 million tons per annum of capacity reach a final investment decision, signaling a massive new demand pipeline.

Moreover, this growth of the flue gas treatment systems market is supported by substantial capital investments and clear project developments. For example, ExxonMobil's Baytown facility is targeting a 1 billion cubic feet per day hydrogen capacity, coupled with a 98% CO2 capture rate. Likewise, Linde's US$ 1.8 billion facility in Beaumont is engineered to sequester 1.7 million tons of CO2 annually. These projects clearly underscore the scale of the opportunity. By the end of the second quarter of 2025, the total active and pipeline CCS capacity linked to blue hydrogen production had reached 125 million CO2 tons per year. The U.S. Department of Energy has also announced US$ 7 billion in funding for clean hydrogen hubs, further cementing future demand.

Segmental Analysis

Particulate Control Systems Unrivaled Dominance in Pollutant Management

Articulate control systems are asserting their flue gas treatment systems market leadership, securing over 38.1% of revenue. Their dominance is a direct result of superior performance in capturing particulate matter from industrial emissions. The segmental market penetration is driven by technological advancements; new electrostatic precipitator installations in 2024 can remove over 250 tons of fly ash daily from large power plants. Meanwhile, advanced fabric filters introduced in 2025 showcase materials extending operational life to 45,000 hours, offering a distinct competitive advantage. The integration of intelligent controls further solidifies their position, with new systems in 2024 reducing energy consumption by 200 megawatt-hours annually per unit, a significant operational saving for the flue gas treatment systems market.

The financial and operational viability of modern articulate control systems underpins their market share. For example, optimized automated cleaning cycles in baghouses from 2025 reduce compressed air usage by 3,000 cubic meters per day. Compact designs facilitated the retrofitting of 15 older industrial plants in 2024, expanding the addressable market. These systems consistently capture particles as small as 0.5 microns. Within the flue gas treatment systems market, a focus on operational continuity is paramount; new diagnostic tools can now forecast maintenance needs 500 operating hours in advance, minimizing costly downtime.

- New electrostatic precipitators achieve particulate emission levels below 5 milligrams per normal cubic meter.

- Over 50 major cement plants globally upgraded to advanced hybrid filter systems in 2024.

- Sophisticated simulation software in 2025 has reduced design and commissioning time by 4 weeks.

Wet Process Technology Asserts Unquestionable Dominance in Treatment Methods

The wet process is the preeminent method in the flue gas treatment systems market, commanding a substantial revenue share of over 43.4%. Its market supremacy is anchored in its profound efficacy in removing a broad spectrum of pollutants, especially sulfur oxides (SOx) and acid gases. In 2024, new large-scale wet scrubber installations within the chemical industry achieved a 99.5% SO2 removal efficiency. These systems are engineered to handle flue gas volumes up to 3 million cubic meters per hour. A key market development in 2025 involves reagent consumption optimization, enabling certain systems to generate annual operational savings of up to US$ 1 million on lime or limestone, reinforcing its value proposition in the flue gas treatment systems market.

Further cementing its market position, ongoing innovations in wet process technology are effectively addressing historical operational challenges. For instance, integrated wastewater treatment modules in 25 new 2024 projects substantially reduce liquid discharge. Furthermore, the high-quality gypsum byproduct from wet flue gas desulfurization (FGD) systems is projected to create a new revenue stream, with commercial sales reaching 20 million tons in 2025. The efficiency of heat recovery from saturated flue gas has also seen improvement, with new heat exchangers capturing an additional 5 megawatts of thermal energy. Such enhancements ensure the flue gas treatment systems market continues to favor wet process technology.

- Advanced wet scrubbers effectively remove over 95% of hydrogen chloride (HCl) emissions.

- The installation timeline for modular wet FGD systems was cut by 1500 man-hours in 2025.

- At least 10 major refineries invested in multi-pollutant wet scrubbers in 2024.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Power Generation Industry Spearheads Adoption and Market Revenue Dominance

The power industry remains the undisputed principal end-user, capturing the largest revenue share at over 43.6% of the flue gas treatment systems market. Its dominance is a function of the immense flue gas volumes produced by fossil fuel combustion. In 2024, approximately 40 coal power units were retrofitted with comprehensive treatment solutions to meet stringent air quality mandates. The operational scale is immense; a standard 500-megawatt coal plant processes over 1.5 million cubic meters of flue gas hourly. These demanding requirements make the power sector the primary driver of investment and technological adoption.

The significant capital allocation from the power sector highlights its market leadership. For 2025, global power utilities are forecast to invest over US$ 10 billion in new and upgraded emission control infrastructure. These are strategic investments that also improve operational stability. For example, enhanced sorbent injection technology enabled 30 power plants to decrease mercury emissions by an average of 90%. The continued global reliance on fossil fuels for baseload power generation guarantees that the flue gas treatment systems market will be shaped by the energy sector's large-scale pollution control needs.

- SCR systems installed in 2024 can operate for 24,000 hours before catalyst replacement.

- Over 60 combined-cycle gas turbine plants installed advanced DeNOx systems during the last year.

- Digital twin technology is optimizing the entire treatment process at 12 major power stations.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific Spearheading Global Demand Through Monumental Industrial Expansion

The Asia Pacific region unequivocally leads the global flue gas treatment systems market, commanding the largest market share through its unparalleled scale of industrial activity and energy infrastructure development. This dominance is not abstract; it is quantified by immense, project-level investments and capacity expansions. For instance, in 2024, China initiated the construction of 68 new coal-fired power units. In parallel, Vietnam's Power Development Plan 8 involves mobilizing up to US$ 135 billion for new energy projects through 2030. Furthermore, India’s industrial sector is set to receive over US$ 8.2 billion in funding for modernization projects that include emission controls by 2026. The pace of development is relentless and directly fuels demand.

Moreover, the region's commitment in the global flue gas treatment systems market extends to diverse energy sources that still require sophisticated flue gas treatment. Japan, for example, is advancing the construction of 21 new large-scale biomass power plants scheduled for operation by 2028. South Korea has also allocated a budget of US$ 1.2 billion for retrofitting 15 major industrial complexes with enhanced air quality control systems by 2027. Indonesia’s Morowali Industrial Park, a massive nickel processing hub, is undergoing an expansion that includes 4 new captive power plants. Additionally, Malaysia has approved 7 new waste-to-energy facilities with a combined processing capacity of 9,800 tons per day. These varied and large-scale projects cement Asia Pacific’s position as the primary demand center for the flue gas treatment systems market.

North America Accelerating Decarbonization With High-Value Technology Investments

North America’s position in the flue gas treatment systems market is defined by its focus on high-technology applications, particularly in carbon capture and clean hydrogen. The U.S. Department of Energy, for instance, has announced US$ 2.52 billion in funding for two major carbon capture demonstration projects in 2024. In Canada, the Pathways Alliance has committed to an initial investment of US$ 1.8 billion for its foundational CCS project in Alberta. The region is seeing tangible project development, with over 30 new carbon capture facilities planned to enter service by 2030.

This investment is creating a robust project pipeline for the flue gas treatment systems market. For example, a new U.S. direct air capture hub in Louisiana is projected to remove 1 million metric tons of CO2 annually. Additionally, 14 industrial sites across the U.S. Midwest have been selected as potential hosts for new carbon capture infrastructure. In the clean fuel sector, Canada’s government has backed 6 new low-carbon hydrogen production projects with a combined investment exceeding US$ 900 million. These technology-forward initiatives are creating a specialized and high-value demand segment.

Europe Driving Market Growth Through Advanced Industrial Green Technology

Europe’s demand for flue gas treatment systems is increasingly driven by industrial modernization and the pursuit of green technology, independent of baseline regulations. The green steel movement is a prime example, with Germany’s Thyssenkrupp plant in Duisburg securing US$ 2.1 billion in funding for a direct reduction plant that requires advanced gas treatment. In the UK, the HyNet industrial decarbonization cluster has attracted over US$ 850 million in private investment for its initial phase. This focus on industrial clusters is a key trend.

Furthermore, the bioenergy sector continues to expand in the flue gas treatment systems market, with 18 new large-scale bioenergy-with-carbon-capture (BECCS) projects announced across the Nordic countries in 2024. Investments are also flowing into next-generation technologies. For instance, a consortium in the Port of Rotterdam has allocated US$ 150 million for a pilot project converting captured CO2 into synthetic fuels. The UK's Drax Power Station is also moving forward with its BECCS project, aiming to capture 4 million tons of CO2 annually. These innovative industrial projects are shaping a sophisticated European market.

Recent Developments in Flue Gas Treatment Systems Market

- Chart Industries Secures Major CO2 Capture Order: In January 2024, Chart Industries received a US$ 4.4 million order from a major energy company for its Cryogenic Carbon Capture™ technology to be used at a gas-fired power generation facility.

- Heirloom Secures US$ 600 Million Investment: In February 2024, direct air capture company Heirloom announced it had raised US$ 600 million in the largest-ever funding round for a carbon removal technology firm, led by Microsoft and TPG.

- Howden Acquired by Chart Industries: While the deal closed in late 2023, its integration in 2024 sees Chart Industries leveraging Howden's expertise in gas handling to offer more comprehensive carbon capture and flue gas treatment solutions.

- Aker Carbon Capture Secures Pre-FEED Contract: In May 2024, Aker Carbon Capture was awarded a pre-FEED contract by a major European power company for a new waste-to-energy plant, signaling strong commercial traction.

- Ecolab Invests in Aquatech International: In early 2024, Ecolab announced a minority equity investment in Aquatech, a leader in water treatment and desalination, to collaborate on solutions for water management in industrial processes, including FGD systems.

- SLB Acquires Majority Stake in Aker Carbon Capture: In March 2024, energy technology giant SLB announced its intent to acquire a majority stake in Aker Carbon Capture for approximately US$ 380 million, aiming to accelerate the scale-up of industrial decarbonization.

- BlackRock Invests US$ 550 Million in Stratos DAC Project: In August 2023, with funds deployed through 2024, BlackRock invested US$ 550 million in Occidental's Stratos direct air capture project, marking a major financial commitment to large-scale carbon removal technology.

- Air Products to Invest US$ 4 Billion in Hydrogen Complex: In late 2023, with spending accelerating through 2024, Air Products announced a US$ 4 billion investment in a new green hydrogen production complex in Texas, driving demand for associated gas handling and purification systems.

- Fluor Awarded FEED Contract for Dow Net-Zero Project: In 2024, Fluor began work on a Front-End Engineering and Design (FEED) contract for Dow’s net-zero chemical complex in Alberta, which includes CO2 capture and flue gas treatment for its ethylene cracker.

Top Players in Global Flue gas Treatment Systems Market

- General Electric

- Mitsubishi Hitachi systems

- Doosan Lenties

- Babcock & Wilcox Enterprises

- Clyde Bergemann Power Group

- FLSmidth

- Marsulex Environmental Technologies

- Thermax

- Other Prominent Players

Market Segmentation Overview:

By Pollutant control Systems

- Flue Gas Desulfurization (FGD) Systems

- DeNOX Systems

- Particulate Control Systems

- Mercury Control Systems

- Others

By Process

- Wet

- Semi-wet

- Dry

By Industry

- Industrial Boilers

- Power

- Chemical & Petrochemical

- Iron & Steel

- Non-Ferrous metal

- Cement

- Waste Treatment

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- U.K.

- Germany

- France

- Spain

- Italy

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |