Global FPC for Smartphone Market: By Type (Single Layer, Double Layer, and Multi-Layer); Application (Foldable and Non-Foldable); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2024–2032

- Last Updated: 24-Oct-2024 | | Report ID: AA1024953

Market Scenario

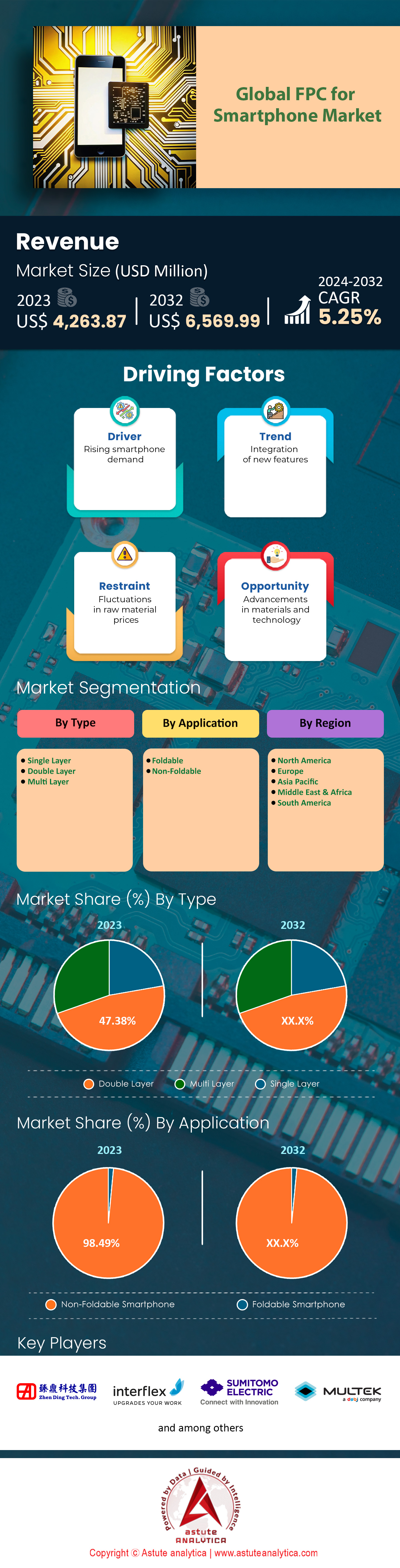

Global FPC for smartphone market was valued at US$ 4,263.87 million in 2023 and is projected to hit the market valuation of US$ 6,569.99 million by 2032 at a CAGR of 5.25% during the forecast period 2024–2032.

Flexible Printed Circuits (FPCs) are crucial components in modern smartphones, serving as the connective pathways between various electronic parts within these compact devices. Made from flexible substrates like polyimide, FPCs can bend and fold without losing conductivity, allowing for more complex and space-efficient designs. Major applications of FPCs in smartphones include connections for displays, cameras, antennas, and other internal modules. Their flexibility enables manufacturers in the FPC for smartphone market to create thinner devices with advanced features, meeting consumer demands for sleek and powerful smartphones.

The demand for FPCs in smartphones is on the rise due to the increasing complexity and functionality of new devices. In 2023, it is estimated that 1.4 billion smartphones will be sold globally, each incorporating multiple FPCs to support features like high-resolution cameras, biometric sensors, and foldable screens. The push towards 5G technology, with over 600 million 5G smartphones expected to be shipped in 2024, also drives the need for sophisticated FPCs that can handle higher data speeds and enhanced connectivity. Smartphone sales directly impact the FPC for smartphone market, as each device requires several flexible circuits. Leading manufacturers like Apple and Samsung shipped over 229 million and 300 million smartphones respectively in 2023, significantly contributing to FPC demand. The average smartphone now contains more than 10 FPC components, including connections for OLED displays, under-screen fingerprint sensors, and multi-lens camera systems. This proliferation of advanced features intensifies the need for reliable and efficient FPC solutions.

The future of the FPC for smartphone market looks promising, with continued growth driven by technological advancements and consumer preferences. Innovations such as foldable smartphones, expected to sell over 17 million units in 2024, up from total of 15.9 million in 2023, require highly flexible and durable FPCs. Additionally, investments in research and development, exceeding $1 billion globally in 2023, are leading to thinner and more robust circuits, opening opportunities for even more advanced smartphone designs.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Growing Demand for Advanced Smartphones Requiring Complex FPC Integration

The surge in consumer demand for advanced smartphones significantly propels the need for complex FPC integration. In 2023, the global smartphone user base reached approximately 4.25 billion individuals, intensifying competition among manufacturers in the FPC for smartphone market to deliver innovative products. The average smartphone now includes over 10 FPC components, a notable increase from previous years. Features like high-resolution multi-lens cameras, which saw shipments of over 500 million units globally in 2023, rely on intricate FPCs for seamless connectivity. In line with, manufacturers like Apple and Samsung report that their flagship models incorporate up to 20 individual FPC assemblies. The inclusion of technologies such as under-display fingerprint sensors, utilized in over 150 million devices in 2023, necessitates advanced FPC solutions. Additionally, the trend towards bezel-less designs, with screen-to-body ratios surpassing 90%, demands flexible circuits that can conform to slim profiles without compromising performance.

The integration of emerging technologies like augmented reality (AR) and artificial intelligence (AI) further heightens the reliance on FPCs. Smartphones equipped with AR capabilities reached sales of 200 million units globally in 2023. These advanced functions require additional sensors and processors, interconnected through flexible circuits to maintain device compactness. Consequently, the increasing appetite for advanced smartphones directly stimulates growth in the FPC for smartphone market through the necessity of sophisticated integration solutions.

Trend: Rise of Foldable Smartphones Utilizing Advanced Flexible Circuits

Foldable smartphones represent a significant trend in 2023, profoundly impacting the FPC for smartphone market. Global shipments of foldable smartphones reached 15.9 million units in 2023, demonstrating substantial growth. Brands like Samsung, LG, and Huawei have introduced models that rely extensively on cutting-edge FPC technology. For example, the Samsung Galaxy Z Fold series incorporates flexible circuits that can endure over 200,000 folds without failure, as verified by durability tests. The complexity of foldable smartphones requires innovative FPC designs with improved flexural endurance and enhanced conductivity. FPCs used in these devices are often less than 0.05 millimeters thick, facilitating ultra-thin profiles. In 2023, investments in research and development for foldable FPC technology surpassed $500 million globally. The market value of FPCs for foldable smartphones is projected to reach $1 billion by 2025, highlighting significant growth potential.

Consumer interest is spurring manufacturers to accelerate production, with surveys indicating that over 20 million consumers express interest in purchasing foldable devices. Industry collaborations, such as partnerships between FPC manufacturers and smartphone companies, aim to co-develop bespoke solutions. These developments position foldable smartphones as a key driver of innovation and growth within the FPC for smartphone market.

Challenge: High Production Costs of Complex FPCs Affecting Profitability

High production costs remain a critical challenge for the FPC for smartphone market in 2023. The intricate nature of modern FPCs requires advanced materials and precision engineering, leading to increased expenses. The cost of polyimide films, a primary material for FPCs, reached $50 per kilogram due to supply constraints and high demand. Precision equipment for manufacturing thin circuits entails significant capital investment, with state-of-the-art production lines costing upwards of $10 million.

These elevated costs impact profitability, with profit margins for FPC companies averaging around 5% in 2023, a decline from previous years. Smaller manufacturers struggle to compete without economies of scale, and some reported net losses; a mid-sized FPC manufacturer noted a $2 million loss this year due to rising expenses. Ongoing investment in research and development, exceeding $1 billion in 2023, is necessary to innovate and improve production efficiency but places additional financial strain on companies. Strategies like materials substitution and production automation are being explored to mitigate costs. However, implementing these solutions requires time and capital, making high production costs a significant hurdle to overcome for sustained growth in the FPC for smartphone market.

Segmental Analysis

By Type

Double layer Flexible Printed Circuits (FPCs) have seen significant adoption in smartphones due to their optimal balance between functionality and cost-effectiveness. In 2023, the double layers segment captured over 47.3% market share. They offer more complexity than single-layer FPCs without the increased production costs associated with multi-layer variants. This balance is crucial for smartphone manufacturers who aim to integrate advanced features while maintaining affordability. In 2023, the global FPC for smartphone market value surpassed $15 billion, with double layer FPCs constituting a substantial portion of this market due to their widespread use in mobile devices.

The demand for double layer FPCs over single and multi-layer types is driven by their enhanced electrical performance and mechanical flexibility. They support more complex circuitry necessary for modern smartphone components such as high-resolution cameras, sensors, and advanced display technologies. For instance, the integration of 5G technology requires more intricate circuit designs, which double layer FPCs can adequately provide. Reports indicate that the production of double layer FPCs reached over 100 million units in 2023 to meet the growing technological demands of the smartphone industry.

Double layer segment in the FPC for smartphone market are unique and desirable because they allow for compact and lightweight smartphone designs without compromising on performance. Their flexibility enables them to fit into the slim profiles of modern smartphones, facilitating innovative design elements like curved edges and foldable screens. Additionally, they enhance signal integrity and reduce electromagnetic interference, which is vital for device reliability. Major smartphone brands have incorporated double layer FPCs to support features like dual-camera systems and biometric sensors, highlighting their dominance in the market. The continued innovation in smartphone functionalities ensures that double layer FPCs remain a preferred choice for manufacturers globally.

By Application

As per application, the non-foldable smartphones are capturing a significant share of 98.4% in the FPC for smartphone market and is also poised to grow at the highest CAGR of 5.26%. Flexible Printed Circuits (FPCs) are predominantly used in non-foldable smartphones primarily because these devices make up the majority of the global smartphone market. In 2023, global sales of non-foldable smartphones exceeded 1.3 billion units, driven by consumer preference for traditional smartphone designs and their affordability compared to foldable models. Key consumers of FPCs in this segment include leading smartphone manufacturers like Apple, Samsung, and Xiaomi, who utilize FPCs extensively in their flagship and mid-range devices to enhance performance and reduce size.

The demand for FPCs is higher in non-foldable smartphones due to the extensive internal component requirements that necessitate flexible, space-saving circuit solutions. Non-foldable smartphones in the FPC for smartphone market integrate numerous features such as multi-lens cameras, high-resolution displays, and advanced sensors, all of which require complex circuitry that FPCs can provide. In contrast, foldable smartphones, while innovative, represent a smaller market segment with around 10 million units sold in 2023. The relative infancy and higher production costs of foldable technology limit their impact on the overall FPC demand.

The dominance of non-foldable smartphones shapes the FPC for smartphone market by driving mass production and technological advancements in FPC manufacturing. Factors contributing to this dominance include the continued consumer demand for reliable and cost-effective devices and the widespread global availability of non-foldable smartphones. Manufacturers focus on optimizing FPC designs for non-foldable devices to improve performance while reducing costs. This focus ensures that the FPC industry aligns its innovations with the needs of the vast non-foldable smartphone market, which remains the primary driver of FPC demand globally.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Regional Analysis

The Asia Pacific region leads the Flexible Printed Circuit (FPC) market for smartphones with over 57.68% market share due to its massive manufacturing base and high consumer demand. Key countries like China, India, South Korea, and Japan contribute significantly to this dominance. In 2023, smartphone unit sales in the Asia Pacific region surpassed 800 million units, with China accounting for over 350 million units and India reaching approximately 200 million units. China's vast manufacturing capabilities and India's rapidly growing smartphone market are pivotal in propelling the FPC for smartphone market forward. Wherein, China's contribution is marked by its status as the world's largest smartphone manufacturer and consumer. Chinese companies produce millions of smartphones annually, incorporating FPCs extensively to enhance device functionality and design. India's impact is seen in its expanding smartphone user base, which fuels demand for devices that rely on FPC technology. India's smartphone market growth rate has been one of the highest globally, adding millions of new users each year. This surge increases the demand for FPCs, as manufacturers cater to the preferences of a youthful and tech-savvy population.

The key factors behind the regional dominance include a robust supply chain, availability of raw materials, and significant investments in technology and innovation. The Asia Pacific region houses leading FPC manufacturers who benefit from economies of scale, allowing for lower production costs and higher output. Government initiatives in countries like China and India supporting electronics manufacturing also bolster the FPC for smartphone market. North America follows distantly, with smartphone unit sales around 200 million units in 2023. The region's smaller population and market size contribute to its secondary position, though it remains significant due to high consumer spending power and technological advancement.

North America's FPC for smartphone market is driven by major technology companies based in the United States, such as Apple, which incorporates FPCs in its devices. However, many manufacturing operations are outsourced to Asia Pacific due to cost efficiencies. The combination of high production capacity in Asia and strategic business decisions by North American companies reinforces the Asia Pacific region's leadership in the market for smartphones. This dynamic is expected to continue as emerging markets in Asia grow and technology companies expand their global reach.

Key Developments Taking Shape in the FPC for Smartphone Market

- Increased Use of FPCs in Smartphones: Apple leads the industry with the integration of up to 16 FPCs in its iPhones, setting a trend that other manufacturers like Samsung, Huawei, and OPPO are following by increasing their FPC usage in smartphones.

- Advancements in FPC Antenna Technology: The FPC antenna market is growing rapidly, driven by innovations in materials and design that enhance performance and reliability. This includes the integration of multi-band capabilities and eco-friendly materials.

- Miniaturization and Lightweight Design: The demand for miniaturized, lightweight, and high-performance communication technologies is driving the growth of FPCs in smartphones and IoT devices.

- Expansion in Asia-Pacific Markets: The Asia-Pacific region, particularly China, Japan, and South Korea, is experiencing rapid growth in FPC production and demand, driven by their status as electronics manufacturing hubs.

- Sustainability Initiatives: There is a growing emphasis on sustainable practices in FPC production, with companies enhancing flexible PVC-based materials to support eco-friendly practices.

- Ultra-thin FPC for smartphone Growth: The ultra-thin FPC for smartphone market is poised for significant growth, driven by technological advancements and consumer demand for smaller, more efficient devices.

Top Players in Global FPC for Smartphone Market

- Nippon Mektron

- Zhen Ding Technology Holding Limited

- InterFlex

- Sumitomo Electric Industries, Ltd.

- Nitto Denko Corporation

- Fujikura Ltd.

- Multek

- Si Flex

- Career Technology MFG Co Ltd

- Flexium Interconnect Inc.

- Luxshare Precision Industry Co., Ltd.

- Stemco

- Other Prominent Players

Market Segmentation Overview:

By Type

- Single Layer

- Double Layer

- Multi Layer

By Application

- Foldable

- Non-Foldable

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |