India Penicillin G Acylase Market: By Source (Bacteria, Yeast, Fungi); Product Type (Free PGA, Immobilized PGA , Recombinant PGA); Form (Powder, Liquid, Granules / Tablets); Grade (Industrial and GMP/API); End Users (Pharmaceutical Manufacturers, CDMOs/CMOs, Research Institutes, Industrial Chemical Companies); Distribution Channel (Direct Sales, Distributors, Online/E-commerce); Country—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2026–2035

- Last Updated: 06-Jan-2026 | | Report ID: AA01261641

Market Snapshot

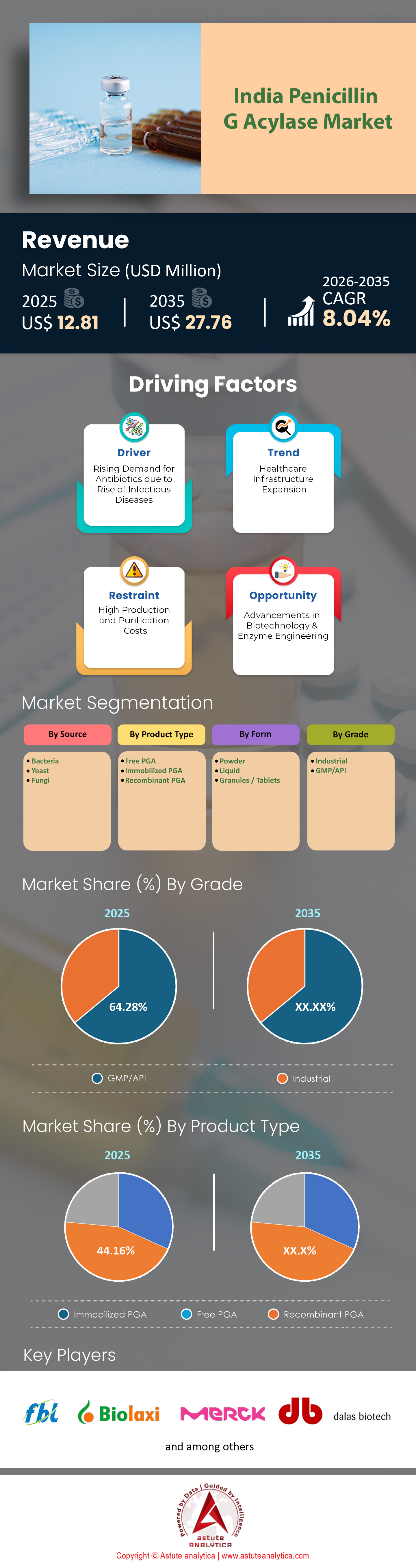

India penicillin G acylase market size was valued at USD 12.81 million in 2025 and is projected to hit the market valuation of USD 27.76 million by 2035 at a CAGR of 8.04% during the forecast period 2026–2035.

Key Findings

- Based on source, the Bacteria segment accounts for 55.61% market share of the India penicillin G acylase market.

- Based on product type, Immobilized PGA accounts for 44.16% market share.

- Based on form, the Powder segment accounts for 43.16% market share.

- Based on grade, the GMP/API segment accounts for 64.28% market share of India penicillin G acylase market.

- Based on end users, the Pharmaceutical Manufacturers segment accounts for 52.36% market share.

- Based on distribution channel, the Direct Sales segment accounts for 62.94% of the market.

How Deeply Has India Anchored Its Position in the Global Enzyme Landscape?

The narrative of India’s penicillin G acylase market has historically been one of formulation dominance, but as we navigate through early 2026, the sub-sector of biocatalysis—specifically the market for Penicillin G Acylase (PGA)—has matured into a robust, self-sustaining ecosystem. No longer merely a satellite to the Chinese API industry, India’s PGA market has transitioned from an import-dependent infancy to a stage of aggressive adolescent growth. This shift is quantitatively visible; the Indian market for penicillin amidases is currently valued at approximately $48.5 million, contributing a significant wedge to the broader Asia-Pacific market which now commands over 42% of global consumption.

The establishment of Indian penicillin G acylase market is deep-rooted, driven by a critical pivot in the manufacturing of 6-Aminopenicillanic acid (6-APA), the backbone of beta-lactam antibiotics. Where chemical hydrolysis once ruled, the enzymatic route now accounts for nearly 95% of production in regulated facilities, signaling a market that has not only adopted technology but has standardized it. The "Make in India" initiative, specifically the Production Linked Incentive (PLI) scheme for Key Starting Materials (KSMs), has acted as a potent accelerant, pushing the domestic CAGR for industrial enzymes to a healthy 8.2%, outpacing the global average of 6.4%.

Where is the Industrial Heart of This Enzymatic Revolution Beating?

If one were to map the pulse of PGA production in India penicillin G acylase market, the "Golden Corridor" of Western India would emerge as the undisputed epicenter. The geographical concentration is heavily skewed toward the states of Gujarat and Maharashtra, which together house approximately 75% of the installed fermentation capacity for this specific enzyme. Gujarat, particularly the industrial belts of Ahmedabad, Vadodara, and the Dahej SEZ, serves as the primary hub, leveraging its proximity to petrochemical feedstocks and established port infrastructure to facilitate the import of raw materials and export of finished enzymes. Maharashtra follows closely, with the Thane-Belapur belt and Nashik offering a rich legacy of bio-engineering talent.

However, the landscape of the penicillin G acylase market is not entirely unipolar. Recent years have witnessed a strategic spillover into the North and South. The Bhiwadi region in Rajasthan has emerged as a cost-efficient alternative for high-purity enzyme production, while the Genome Valley in Hyderabad remains the critical consumption center, absorbing the vast majority of PGA for downstream antibiotic synthesis. This clustering is not accidental but a result of logistic optimization, reducing the "lab-to-vat" transfer time which is critical for maintaining enzyme activity levels that often degrade during prolonged transport.

To Get more Insights, Request A Free Sample

Who Are the Titans Steering the Ship in a Concentrated Market?

The competitive hierarchy of the Indian penicillin G acylase market is defined by a monopolistic competition structure, where a handful of colossal players dictate price and technology trends. Leading this vanguard is Concord Biotech, a behemoth that has effectively cornered the market on fermentation-based APIs and enzymes. Following their massive capacity expansion post-2024, they now command an estimated 20% global market share in select fermentation segments, supplying to over 70 countries. Their dominance is challenged by Fermenta Biotech, a legacy player that has successfully pivoted from Vitamin D3 to a broader enzyme portfolio, now serving as a critical supplier to domestic beta-lactam manufacturers. Another formidable contender is Advanced Enzyme Technologies, based in Nashik, which has leveraged its proprietary R&D to produce high-stability enzymes that operate efficiently at higher pH levels.

The penicillin G acylase market is also feeling the weight of Rossari Biotech, which, through strategic acquisitions of companies like Unitop and Tristar, has integrated backward into the specialty chemical space, boasting a combined operational capacity exceeding 86,000 MTPA. These players do not just compete on volume; they compete on "specific activity"—the measure of enzyme potency per milligram—where Indian variants are now consistently hitting benchmarks of >250 U/g wet weight, rivaling European standards.

Is the Country’s Production Capacity Sufficient to Feed the World?

India’s production prowess in the global penicillin G acylase market has moved beyond merely meeting domestic needs. It is now structurally designed for global scale. As of the latest fiscal reports, the country’s installed fermentation capacity for specialized enzymes has crossed the 4,500 m³ threshold. To contextualize this, the production of 6-APA—which consumes the vast majority of PGA—requires the enzyme to be immobilized on solid supports to allow for reusability.

Indian manufacturers have mastered this immobilization technology, with current facility upgrades focusing on increasing the "cycle life" of the enzyme from 200 cycles to over 450 cycles. This efficiency gain effectively doubles the virtual capacity without requiring new steel on the ground. For instance, the PLI-beneficiary plants commissioned in late 2024 are now operating at roughly 85% utilization rates, churning out thousands of tons of immobilized enzyme annually. This surge is critical because the global demand for Amoxicillin alone requires over 25,000 metric tons of 6-APA, and India is positioning itself to capture 30% of this processing market by 2027, backed by a capital infusion in the sector that rose by 18% year-on-year.

How Far Does the Indian Influence Reach in Global Trade?

The export analysis of India’s penicillin G acylase market reveals a fascinating transition from a net importer to a strategic export hub. While India still imports high-grade, genetically modified strains and specific niche variants from China and Denmark—evidenced by an import bill that still hovers around $15 million annually—the export trajectory is sharply upward. Under the HS Code 350790, India’s enzyme exports have penetrated the markets of Southeast Asia, Latin America, and increasingly, the generic-friendly markets of Eastern Europe.

The value proposition driving this is clear: Indian manufacturers offer a price arbitrage of nearly 20-25% compared to their European counterparts, without a compromise on pharmacopeial standards. In 2025 alone, export volumes of immobilized lipase and acylase enzymes saw a jump of 14.5%, signaling that international buyers are validating Indian quality. The trade balance is slowly tipping; for every dollar India spends on importing enzyme technology, it is now generating roughly $1.60 in enzyme-related exports, a ratio that was at parity just five years ago.

What Key Trends Are Reshaping the Strategic Horizon of IndianPenicillin G Acylase Market?

Three distinct, overarching trends are carving the future of this market.

- "Green Shift" to enzymatic processing. Environmental regulations regarding solvent disposal are tightening globally, forcing manufacturers to abandon chemical hydrolysis. This has created a captive market for PGA, with the "green enzymatic route" segment growing at a CAGR of 9.5%.

- Technological leap toward "Immobilized Enzyme Engineering." The market is moving away from liquid enzymes to robust, solid-state catalysts that can withstand rigorous industrial churning. The adoption rate of immobilized PGA in India has surpassed 75%, driven by the economic necessity to reuse enzymes for hundreds of batches to amortize costs.

- "Backward Integration." Major antibiotic manufacturers are no longer content with buying enzymes; they are building in-house fermentation capabilities to secure their supply chains against geopolitical shocks. This vertical integration is blurring the lines between enzyme suppliers and pharmaceutical manufacturers, creating "super-integrators" that control the entire value chain from the spore to the finished pill.

How Intense is the Rivalry in this High-Stakes Arena?

The competitive intensity of the Indian penicillin G acylase market can be best described as a "Red Ocean" domestically, but a "Blue Ocean" in the high-value export segment. In the domestic arena, price sensitivity is acute. With the cost of the enzyme contributing nearly 8-12% to the total cost of 6-APA production, pharmaceutical companies exert immense pressure on enzyme suppliers, compressing margins to the single digits. The Herfindahl-Hirschman Index (HHI), a measure of market concentration, remains high, indicating that the top three players wield significant pricing power, making it incredibly difficult for new entrants to survive without massive capital buffers.

Wherein, barriers to entry in the Indian penicillin G acylase market are formidable, establishing a viable fermentation plant requires a CAPEX of upwards of $20 million and, more importantly, access to high-yielding microbial strains which are closely guarded intellectual property. However, for those who can navigate these waters, the rewards are lucrative. The shift toward high-potency, genetically recombinant enzymes offers better margins, and the impending patent cliffs for several biologic drugs are opening new avenues for enzymatic applications, ensuring that while the competition is fierce, the pie itself is expanding rapidly.

Minimum Import Price Policy Catalyzes Growth in Domestic Penicillin G Acylase Market Demand

The Indian government’s finalization of a Minimum Import Price (MIP) for Penicillin G serves as a critical stabilizer for India’s burgeoning fermentation industry, directly benefiting the ancillary Penicillin G Acylase (PGA) market. By shielding new domestic manufacturers like Lyfius Pharma from predatory pricing and dumping by Chinese competitors, the MIP ensures the operational viability of local Pen-G plants. Since PGA is the essential biocatalyst required to hydrolyze Pen-G into 6-APA for antibiotic production, a secure and continuously operating domestic Pen-G sector guarantees a consistent, baseline demand for the enzyme. This policy shift effectively de-risks the supply chain, encouraging enzyme suppliers to scale operations to meet the requirements of a protected, reliable local customer base rather than relying on volatile import-dependent processors.

Furthermore, this development fosters a strategic ecosystem for long-term growth within the enzyme sector. With the threat of market destabilization removed, Indian pharmaceutical companies in the penicillin G acylase market can confidently commit to forward integration and consistent production schedules. This stability allows PGA manufacturers to optimize their inventory and pricing models, moving away from spot-market fluctuations caused by erratic raw material costs. Ultimately, the MIP not only secures India’s upstream Key Starting Material (KSM) independence but also strengthens the secondary market for processing aids. This creates a resilient, self-sustaining loop where the demand for Penicillin G Acylase is anchored by a government-backed, robust domestic fermentation infrastructure.

Segmental Analysis

Bacterial Sources Dominate Enzyme Production with 55.61% Market Share

Bacterial strains remain the primary source in India's penicillin G acylase market, reflecting scalability advantages and superior catalytic efficiency. Achromobacter sp. CCM 4824 and recombinant E. coli BL21 strains form the cornerstone of commercial PGA production globally and specifically across India's expanding PLI-subsidized manufacturing complex. Recombinant E. coli BL21 (DE3), engineered to eliminate ATP-dependent proteases (Lon and OmpT proteolytic pathways), delivers threefold higher PGA yields compared to wild-type strains—achieving 150 U/g wet cell weight versus approximately 50 U/g in natural strains. This advancement directly enabled India's PLI-backed penicillin G manufacturing restart after three decades of import dependence.

Aurobindo Pharma's landmark 15,000 MT annual Pen-G capacity facility at Kakinada (Andhra Pradesh), commissioned in October 2024 at ₹2,400 crore investment, requires sustained bacterial PGA fermentation for penicillin G-to-6-APA conversion essential to semi-synthetic antibiotic synthesis. Site-directed mutagenesis of Achromobacter strains achieves improved synthesis-to-hydrolysis (S/H) ratios and 92% penicillin G-to-6-APA conversion efficiency, substantially outperforming wild-type strains (37-68% conversion). Fermenta Biotech, pioneering India's bacterial PGA production since 1986, recently secured board approval for ₹50 crore investment expanding fermentation capacity to 75 KL at Dahej (Gujarat), directly addressing demand surge from PLI-incentivized 6-APA manufacturers. The

Immobilized Enzyme Technology Achieves 44.16% Market Dominance Through Cost and Operational Efficiency

Immobilized penicillin G acylase captures nearly half the penicillin G acylase market segment revenue through superior reusability economics, thermal stability, and industrial-scale operational feasibility. Unlike free enzymes requiring continuous replacement after single-use cycles, immobilized PGA maintains 66% catalytic activity across 12 consecutive operational cycles and demonstrates commercial viability for 250+ industrially-relevant reaction cycles. Immobilization technology delivers cost savings approximating 60% compared to free enzymes at prevailing market enzyme pricing—a critical advantage for margin-constrained pharmaceutical manufacturers producing generic antibiotics competing against Chinese price aggression (penicillin G prices collapsed 40-50% between March 2024 and August 2025).

Fermenta's proprietary DILBEADS immobilization platform achieves 85% enzyme stability in organic solvents critical for 6-APA synthesis reactions, directly supporting Lyfius Pharma's 3,600 MT 6-APA facility scale-up and cost competitiveness. Immobilized PGA in the penicillin G acylase market exhibits superior thermal stability at 45°C (industrially optimal operational temperature), with enzyme conformational integrity preserved by carrier-matrix interactions compared to soluble enzyme counterparts experiencing rapid denaturation.

Powder Formulation Captures 43.16% Share via Superior Stability and Supply Chain Economics

Lyophilized powder formulation represents the dominant commercial distribution form for penicillin G acylase market in India's fragmented pharmaceutical supply chain, reflecting superior thermodynamic stability and cross-regional logistics efficiency. Powder eliminates water-dependent enzyme hydrolysis, protein aggregation, and microbial degradation pathways inherently active in aqueous enzyme solutions, maintaining specific activity (Units/mL normalized) across 12-24 months at ambient storage conditions (2-8°C) without requiring ultra-low-temperature infrastructure (−70°C freezer costs). This storage capability directly addresses India's pharmaceutical distribution challenges across varied climatic zones (tropical humidity, temperature fluctuation) where refrigerated supply chains prove economically prohibitive for enzyme suppliers serving distributed formulation manufacturers.

Enzymatic unit reconstitution achieves precise standardization—enabling batch-to-batch consistency critical for pharmaceutical manufacturers operating under GMP quality protocols. This is also helpful in achieving reproducible 6-APA conversion yields in the penicillin g acylase market. Logistics economics strongly favor powder distribution: 50 kg powder batches are equivalent to 500+ liters dilute liquid enzyme formulation, reducing freight weight by 90% and proportionally reducing cross-border shipping costs—essential for India's antibiotic API exports spanning 150+ destination countries.

India's global antibiotic supply role (40% of worldwide generic antibiotic doses) depends on powder PGA stability across variable-temperature transits through Asian maritime supply chains and terrestrial customs corridors experiencing temperature swings (15-45°C).

GMP/API Grade Dominance Reaches 64.28% Share Through Regulatory Certification Infrastructure

GMP (Good Manufacturing Practice) and API-grade penicillin G acylase dominate India's penicillin G acylase market at nearly two-thirds share, directly reflecting mandatory pharmaceutical regulatory compliance ecosystem and India's unparalleled global manufacturing certification infrastructure. India operates 499 USFDA-approved pharmaceutical facilities worldwide—the highest concentration outside the United States—with 262 specifically designated for API (Active Pharmaceutical Ingredient) manufacturing across regulated pathways. This regulatory landscape extends to 1,400+ WHO-GMP certified manufacturing plants across India, establishing baseline pharmaceutical-grade quality expectations that pharmaceutical buyers prefer among enzyme suppliers to minimize regulatory risk and ensure finished-product compliance.

Fermenta Biotech's novel penicillin G acylase (NPGA) carries GMP certification and pharmaceutical-grade specifications enabling direct integration into Cipla, Lupin, and Sun Pharma's 6-APA synthesis and semi-synthetic antibiotic production lines without additional regulatory qualification cycles. The PLI (Production Linked Incentive) scheme in the Indian penicillin G acylase market explicitly mandates GMP compliance across all 34 commissioned projects producing 25 critical bulk drugs—including penicillin G and 6-APA intermediates—directly cascading GMP enzyme procurement mandates to all participating pharmaceutical manufacturers receiving government financial incentives.

Pharmaceutical Manufacturers Drive 52.36% Market Demand Through Massive Semi-Synthetic Antibiotic Scale

Pharmaceutical manufacturers and formulation companies command over half the Indian penicillin G acylase market through enormous 6-APA (6-aminopenicillanic acid) intermediate demand for semi-synthetic penicillin and cephalosporin synthesis. India's antibiotics market reached USD 2,927.1 million in 2024, with growth projections reaching USD 4,493.1 million by 2033 (4.8% CAGR), with cell wall synthesis inhibitors (penicillins and 6-APA-derived semi-synthetic variants) accounting for 57.12% of therapeutic market volume. India supplies 40% of global antibiotic doses by volume—amounting to billions of individual antibiotic units manufactured annually—requiring proportionally scaled fermentation-based 6-APA intermediate production to meet downstream formulation demand.

Aurobindo Pharma's integrated Lyfius complex (15,000 MT annual Pen-G fermentation + 3,600 MT 6-APA conversion capacity) exemplifies manufacturer-driven vertical integration in the penicillin g acylase market, which directly cascading penicillin G acylase procurement requirements downstream across the company's formulation divisions. Cipla, Lupin, and Sun Pharma collectively operate antibiotic production infrastructure exceeding 1,500 MT annual capacity, with Sun Pharma commanding 8.08% market share within India's broader pharmaceutical market and maintaining specialized fermentation-based 6-APA synthesis capabilities. Amoxicillin (primary 6-APA-derived semi-synthetic penicillin) captures USD 214.25 million market value within India, projecting USD 257.12 million by 2030 (3.23% CAGR)—directly proportional to underlying PGA enzymatic demand for 6-APA synthesis.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Recent Developments in India Penicillin G Acylase Market

India Market Developments

- Aurobindo Pharma Pen-G Plant Commercialization (2025): Aurobindo Pharma confirmed the commercial operationalization of its massive Penicillin G plant in Andhra Pradesh in Q4 FY25. The facility, operated by its subsidiary Lyfius Pharma, is set to produce 15,000 MT annually, ending India's decades-long import dependence and creating a massive captive market for PGA.

- Fermenta Biotech ₹110 Crore Expansion (Dec 2025): Fermenta Biotech Limited approved a significant capital expenditure of ₹110 crore in December 2025 to expand its Dahej facility. The investment is specifically earmarked for enhancing capacity in "green chemistry enzymes," including Penicillin G Acylase (PGA), to support the surging domestic demand from PLI beneficiaries.

- Kinvan Pvt. Ltd. Clavulanic Acid Breakthrough (2025): Kinvan Pvt. Ltd. commenced commercial production of Clavulanic Acid in 2025 under the PLI scheme. As a fermentation-based manufacturer, this development marks a critical step in India’s backward integration, utilizing similar enzymatic infrastructure and expertise relevant to the broader beta-lactam ecosystem.

- Orchid Pharma 7-ACA Project Progress (2025): Orchid Pharma announced it has spent ₹20 crore by January 2025 on its new 7-ACA project under the PLI scheme. The company is actively setting up downstream processing facilities that will rely heavily on enzymatic conversion, reinforcing the demand for industrial biocatalysts.

- Government Minimum Import Price (MIP) for Pen-G (Dec 2025): The Indian government initiated the finalization of a Minimum Import Price for Penicillin G in late 2025. This policy intervention is designed to shield new domestic manufacturers like Lyfius Pharma from predatory pricing by Chinese competitors, ensuring the viability of local fermentation plants.

Top Companies in the India Penicillin G Acylase Market

- Fermenta Biotech

- Biolaxi Enzymes Pvt Ltd

- Dalas Biotech Ltd.

- Merck

- Biosynth

- Dalment

- Other Prominent Players

Market Segmentation Overview

By Source

- Bacteria

- Yeast

- Fungi

By Product Type

- Free PGA

- Immobilized PGA

- Recombinant PGA

By Form

- Powder

- Liquid

- Granules / Tablets

By Grade

- Industrial

- GMP/API

By End User

- Pharmaceutical Manufacturers

- CDMOs/CMOs

- Research Institutes

- Industrial Chemical Companies

By Distribution Channel

- Direct Sales

- Distributors

- Online/E-commerce

FREQUENTLY ASKED QUESTIONS

The market is on a robust upward curve, valued at USD 12.81 million in 2025. It is projected to reach USD 27.76 million by 2035, expanding at a CAGR of 8.04%. This growth is anchored by the resurgence of domestic antibiotic manufacturing.

The PLI scheme has been a game-changer by incentivizing the domestic production of Key Starting Materials (KSMs) like Penicillin G. Projects like Aurobindo Pharma’s 15,000 MT plant create massive, captive demand for PGA, which is essential for converting Penicillin G into 6-APA.

Immobilized PGA commands 44.16% of the market because it offers superior economic viability. Unlike free enzymes, immobilized variants can be reused for over 450 industrial cycles, reducing enzyme costs by approximately 60% and ensuring stability in organic solvents.

The MIP on Penicillin G protects new domestic manufacturers from predatory pricing by Chinese competitors. By ensuring the survival of local Pen-G plants, the policy guarantees a consistent, baseline demand for PGA enzymes, effectively de-risking the supply chain for enzyme manufacturers.

The market is consolidated, with titans like Concord Biotech and Fermenta Biotech leading the space. Concord alone commands a significant global share in fermentation-based APIs. The high barrier to entry regarding microbial strain technology keeps the market oligopolistic.

Powder formulations account for 43.16% of the market due to logistics. In India’s tropical climate, liquid enzymes degrade faster; powder offers stability at 2-8°C and reduces freight weight by 90%, making it ideal for cost-efficient distribution.

India is transitioning from dependency to self-reliance. While high-grade strains are still imported ($15M annually), India is rapidly becoming a net exporter. For every dollar spent on imports, India now generates roughly $1.60 in enzyme exports, targeting markets in Latin America and Southeast Asia.

Stringent environmental regulations regarding solvent disposal are forcing a 95% shift toward the enzymatic route. PGA is the enabler of this Green Shift, allowing manufacturers to bypass dirty chemical hydrolysis methods, thus driving its CAGR of 9.5% in the green segment.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |