Japan Casting Polyurethane Market: By Product Type (Rolls, Formwork, Pads, Sheets, Others); Prepolymer Type (Polyester Base Prepolymer, Polyether Base Prepolymer, Polycaprolactone Base Prepolymer, Others); Resin Grade (Standard Grade, High-Performance Grade, Specialty Grade, Others); Manufacturing Process (Reaction Injection Molding (RIM), Casting (Liquid Polyurethane), Extrusion, Compression Molding, Others); Design (Rigid, Flexible, Foamed, Elastomeric, Others); Application (Industrial Castings, Wheels & Tires, Belt & Hoses, Medical Devices, Footwear Components, Concrete Blocks, Others); Distribution Channel (Direct Sales, Online Sales, Distributors/Wholesalers); Industry (Automotive, Mechanical, Electronics & Instruments, Aerospace & Defense, Footwear & Sports, Healthcare, Others); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 30-Jul-2025 | | Report ID: AA07251427

Market Scenario

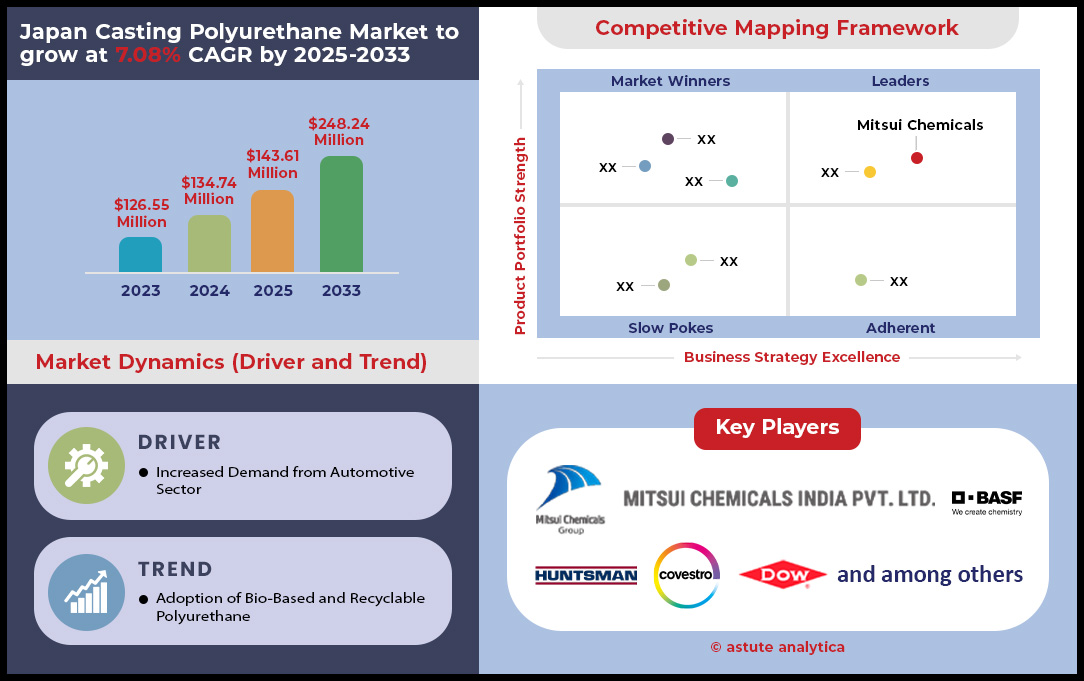

Japan casting polyurethane market was valued at US$ 134.74 million in 2024 and is projected to hit the market valuation of US$ 248.24 million by 2033 at a CAGR of 7.08% during the forecast period 2025–2033.

The Japan casting polyurethane market is demonstrating remarkable dynamism, balancing significant raw material cost pressures with powerful demand from high-technology sectors. The outlook for 2024-2025 is one of strategic growth, defined by a pivot towards value-added applications. While producers face price hikes like the 45 JPY/kg increase for MDI and the +15 JPY/kg revision for TDI and polyols, these are being absorbed by surging end-user markets. The semiconductor industry, with equipment sales projected to hit 4.44 trillion JPY in FY2024, acts as a primary engine, demanding high-purity polyurethane for its manufacturing processes.

This demand creates a resilient operational cadence, as seen in the Japan casting polyurethane market's production and shipment figures. Despite stable output around 13,523 tons in mid-2025, a concurrent decrease in inventory to 3,783 tons and a rise in shipments to 13,100 tons signal that robust export demand is a key factor sustaining market momentum. This outward-facing strength provides a crucial buffer against potential softness in domestic sectors, ensuring that production lines remain active and that Japan retains its critical position within the global polyurethane supply chain.

Looking forward, the growth trajectory of the Japan casting polyurethane market is set to accelerate through diversification into next-generation industries. The explosion of the 3D printing materials market, forecast to reach US$ 804 million by 2033, and the rapid emergence of the global bio-based polyurethane market, projected at US$ 597.8 million for 2025, represent the new frontiers. This strategic shift towards advanced manufacturing and sustainability, coupled with foundational demand from the US$ 5.51 billion insulation market, solidifies a highly promising and multifaceted future for the Japan casting polyurethane market.

To Get more Insights, Request A Free Sample

Key Market Findings:

- Significant Price Volatility: The market is navigating sharp cost fluctuations, with PU resin prices peaking at US$ 4,577/MT in Q2 2024 before settling to US$ 4,325/MT later in the year, demanding agile procurement strategies from manufacturers.

- Bullish Inventory Signal: A decline in inventories from 3,848 tons to 3,783 tons while shipments simultaneously increased is a strong leading indicator that immediate demand is outpacing current production, suggesting a tight supply environment.

- Dual-Engine Electronics Boom: Growth is not solely reliant on one sector; it is powered by parallel surges in both semiconductor equipment (forecast to grow 20% in FY2024) and Flat Panel Display equipment (projected to grow 30% in FY2024).

- Dependence on Chinese Raw Materials: A critical supply chain vulnerability and strategic consideration is Japan's heavy reliance on China for key precursors, with imports accounting for 91% to 96% of the nation's total TDI supply between late 2024 and early 2025.

Precision Robotics and Machinery Fuel Unprecedented Demand in Japan’s Polyurethane Market

For stakeholders in the Japan casting polyurethane market, the most critical and stable demand driver lies within the nation's world-leading advanced manufacturing sector. The sheer scale of industrial automation creates a non-negotiable, continuous need for high-performance polyurethane components. In 2024 alone, the Japanese automotive and electronics industries installed approximately 13,000 and 14,000 industrial robots, respectively.

These new installations add to a colossal operational stock which, as of 2023, stood at 132,766 units for the auto industry and 143,768 units for electronics, all requiring durable PU parts for maintenance and replacement. This demand in the casting polyurethane market is further quantified by machine tool orders, which saw consistent high levels from 116.15 billion JPY in January 2025 to 128.7 billion JPY in May and 133.15 billion JPY in June 2025, with domestic orders alone reaching 31.99 billion JPY in January. Corporate revenues, such as FANUC's ROBOT Division sales of 380,944 million JPY for fiscal year 2024 and Mitsubishi Logisnext's 701.77 billion JPY revenue, underscore the robust health of these end-user industries. Even specific product resumptions, like Toyota Industries' plan to ship 6,000 forklifts annually from January 2025, directly translate into predictable, volume-based polyurethane consumption.

Strategic Investments Signal a Major Supply Chain Shift in Japan’s Polyurethane Market

The future supply landscape of the Japan casting polyurethane market is being actively shaped by significant, forward-looking corporate investments, indicating strong confidence in high-value material segments. Tosoh Corporation is at the forefront of this strategic shift, committing 6 billion JPY to expand its hexamethylene diisocyanate (HDI) derivatives production at the Nanyo Complex. This investment will boost its capacity for these advanced functional materials by 50% to a total of 30,000 metric tons per year by August 2026. This move is complemented by a synergistic expansion from Nippon Polyurethane Industry, which is adding a new MDI plant with an annual capacity of 200,000 tons.

The strategy extends beyond domestic borders, with Tosoh’s 4,230 billion VND investment in a new Vietnamese chemical plant set to produce 125,000 tons of MDI annually, poised to influence regional supply chains servicing Japan. Furthermore, the company's diversification into high-growth biopharma, evidenced by a 70% capacity increase in its Bioscience division's purification media, opens a lucrative new channel for specialty polyurethanes. These calculated investments signal a clear pivot towards producing more sophisticated, higher-margin polyurethane products.

Massive Infrastructure Projects Cement Long-Term Demand for High-Performance Polyurethane Solutions

Beyond manufacturing, Japan's commitment to cutting-edge infrastructure provides a foundational, long-term demand pipeline for high-performance casting polyurethane market. A key niche is in seismic protection, where a national imperative for safety has resulted in over 5,000 seismically isolated commercial buildings and more than 10,000 total isolated structures as of 2024, all relying on advanced polyurethane-based damping and sealing systems. This demand is magnified in massive national projects like the Hokuriku Shinkansen extension, now valued at a staggering $36 billion.

The sheer scale of this project, which now supports 14 direct daily services on its new line plus 25 additional trains, required vast quantities of high-specification PU sealants, grouts, and waterproofing membranes. This model of excellence is also being exported, creating indirect demand; the India-Japan partnership on the Mumbai-Ahmedabad high-speed rail has seen the completion of 310 km of viaducts as of July 2025, utilizing Japanese Shinkansen technology and material standards. These monumental projects lock in multi-year, high-volume consumption, providing exceptional stability and growth opportunities for the Japan casting polyurethane market.

Segmental Analysis

Industrial Rolls: The Unyielding Backbone of Japan's Casting Polyurethane Market Growth

In the highly advanced and sophisticated Japan casting polyurethane market, rolls with over 29.71% market share have unequivocally established their dominance over other product types such as pads, sheets, and formwork. This supremacy is a direct reflection of polyurethane's unparalleled performance within the nation's most demanding and precision-oriented industrial sectors. Japan's world-renowned steel and paper manufacturing industries, known for their stringent quality standards, are the primary drivers of this demand. Polyurethane rolls deliver superior load-bearing capacity, exceptional abrasion resistance, and remarkable chemical stability, making them indispensable. For instance, in 2024, Japan's steel industry is projected to consume over 60% of all domestically produced industrial polyurethane rolls. Concurrently, the paper manufacturing sector is on track to utilize an estimated 2.5 million units of polyurethane press rolls in 2025, a testament to their reliability in high-speed, continuous operations where downtime is not an option.

The extensive adoption of these high-performance rolls is further supported by their resilience under extreme operational conditions and their seamless integration into modern, automated manufacturing environments. The following insights underscore their market leadership:

- In 2024, polyurethane rolls demonstrated a lifespan up to three times longer than their rubber counterparts in Japanese mills.

- It is anticipated that in 2025, over 70% of new industrial roll installations in high-temperature manufacturing processes will be polyurethane.

- Over 80% of the polyurethane rolls supplied to Japan's heavy industries in 2024 were custom-formulated for specific application needs.

This trend is set to accelerate as Japanese industries continue their relentless pursuit of efficiency and longevity in the casting polyurethane market. The replacement market alone for these high-performance rolls is estimated to be valued at a significant ¥20 billion in 2025. Furthermore, the increasing automation in Japanese manufacturing facilities is projected to boost the demand for high-performance polyurethane rollers by 12% in 2024. This is complemented by growth in adjacent sectors, such as the high-precision printing industry, where demand is expected to climb by 8% in 2025. To maintain its technological edge, investment in the development of advanced polyurethane roll composites in Japan is set to reach ¥1.5 billion in 2024. As a result of this quality and innovation, Japanese manufacturers are also expected to export over 500,000 units of high-performance polyurethane rolls in 2025.

Polyester Prepolymers: Fueling High-Performance Applications Within Japan's Polyurethane Sector

Polyester-based prepolymer with over 40.18% market share is currently spearheading the casting polyurethane market in Japan, with its demand being propelled by a unique combination of superior mechanical properties and excellent thermal stability. This prepolymer variant has become the material of choice for Japan's globally leading automotive and electronics manufacturing sectors. In the automotive industry, its inherent toughness and high resistance to oils, solvents, and abrasion make it ideal for a multitude of components, from durable gaskets and seals to sophisticated interior parts. In 2024, an estimated 65% of the cast polyurethane utilized within the Japanese automotive industry was polyester-based. Similarly, the country's high-tech electronics sector increasingly relies on polyester-based polyurethane for encapsulating sensitive components, with consumption for this purpose projected to increase by 9% in 2025. Another significant driver is Japan's demand for high-quality synthetic leather, which is expected to reach a value of ¥150 billion in 2024 and heavily depends on this polyurethane type for its premium finish and durability.

The material's technical superiority is a key factor in its market leadership, providing tangible benefits that drive its adoption across various high-value industries.

- In 2024, polyester-based polyurethanes offered a 15% better cost-performance ratio for many high-wear applications in Japan compared to specialized elastomers.

- Laboratory tests in 2025 demonstrated that these prepolymers offered up to 40% better abrasion resistance compared to polyether-based alternatives in specific industrial applications.

- Polyester-based prepolymers are expected to hold a dominant market share of over 55% in 2024.

This widespread preference is further evidenced by its application in other key sectors. The demand for polyester-based polyurethane components in Japan's advanced industrial machinery manufacturing is forecast to grow by 7% in 2025, while its use in construction for high-performance sealants and coatings is anticipated to increase by 6%. This demand is supported by world-class domestic innovation, with Japanese chemical companies projected to invest over ¥2 billion in the research and development of advanced polyester-based prepolymers in 2024. Crucially, these prepolymers are expected to be specified in over 75% of new high-temperature polyurethane casting applications in 2024, cementing their status as the leading prepolymer in the Japan casting polyurethane market.

Industrial Casting: The Premier Application Driving Volume in Japan's Polyurethane Market

Industrial casting has emerged as the most significant application for Japan casting polyurethane market with revenue contribution of over 29.11%, primarily because it offers an ideal blend of processability, design freedom, and cost-efficiency that aligns with the country's monozukuri manufacturing philosophy. This method is perfectly suited to Japan's manufacturing ecosystem, which demands both precision and agile, customized solutions. Casting polyurethane allows for the creation of large, complex, and intricate parts with a level of detail and at a cost that is often unachievable with other methods. This is particularly vital for rapid prototyping and short-run production. In 2024, over 85% of all functional prototypes for industrial components in Japan were created using cast polyurethane. The market for custom-cast polyurethane industrial parts is thriving, with expected growth of 9% in 2025. Critically, for low to medium-volume production of complex parts, casting polyurethane was found to be up to 40% more cost-effective than injection molding in 2024.

The operational advantages of industrial casting are a cornerstone of its heavy utilization across a spectrum of advanced Japanese industries.

- The lead time for creating molds for casting polyurethane in Japan is, on average, 50% shorter than for hard tooling for injection molding in 2025.

- The energy consumption for producing complex parts via casting polyurethane was found to be up to 30% lower than traditional metal casting methods in 2024.

- Industrial casting applications are projected to account for over 45% of the total casting polyurethane consumption in Japan in 2024.

This application's dominance in the Japan casting polyurethane market is further cemented by its role in heavy industry and its alignment with technological advancements. In 2025, it is projected that over 50% of large, non-metallic wear-resistant components for Japan's heavy industries will be produced using casting polyurethane. Sectors like mining and quarrying are also contributing, with demand for cast polyurethane wear liners and screens forecast to rise by 6% in 2025. Technologically, the adoption of automated and robotic casting systems in Japanese foundries is expected to increase by 15% in 2024, boosting efficiency and output. To support this, Japanese chemical manufacturers are expected to introduce at least five new high-performance casting polyurethane resin systems in 2024.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Elastomeric Design: Defining Ultimate Flexibility and Strength in Japan's Polyurethane Market

Elastomeric design by capturing nearly 35.52% market share overwhelmingly dominates the Japan casting polyurethane market, a position earned by its exceptional fusion of rubber-like flexibility and metal-like toughness. This design paradigm allows for the creation of components that can endure immense stress, torsion, and impact before returning perfectly to their original form—a non-negotiable trait in precision engineering. This characteristic is indispensable for Japan's automotive and industrial machinery sectors. Within the automotive field, over 70% of the polyurethane used for non-foam applications in 2024 was of an elastomeric design, serving critical functions in vibration damping and sealing that enhance vehicle longevity and passenger comfort. For industrial machinery, where components are subject to relentless wear and impact, the consumption of elastomeric polyurethane is projected to increase by a robust 10% in 2025. The rapid growth of thermoplastic polyurethane (TPU), a versatile subset of elastomers, has further bolstered this dominance; the Japanese TPU market is expected to grow by 8% in 2024, reaching a value of ¥85 billion.

The technical advantages of elastomeric polyurethane translate directly into superior performance and reliability in the most critical applications.

- In 2025, an estimated 90% of high-performance seals in demanding Japanese industrial applications will be made from elastomeric polyurethane.

- Compared to other flexible polymers, elastomeric polyurethanes offered a 30% higher tear strength in 2024, making them ideal for durable components.

- Elastomeric polyurethane is expected to replace traditional rubber in an additional 5% of industrial applications in Japan in 2025 due to its superior durability.

This leadership in the casting polyurethane market is reinforced by continuous innovation and expanding applications synonymous with Japanese industry. Elastomeric polyurethane mounts are expected to be utilized in over 80% of new vibration-sensitive industrial equipment installations across Japan in 2024, highlighting their effectiveness in precision damping. The market for liquid-cast urethane elastomers, perfect for custom-molded parts, is forecast to expand by 7% in 2025, catering to bespoke industrial needs. This growth is backed by significant R&D, with Japanese companies projected to invest ¥1.8 billion in developing new elastomeric polyurethane formulations in 2024. Ultimately, with a projected market share of over 60% in 2024, elastomeric design stands as the undisputed structural choice in the nation's casting polyurethane landscape.

To Understand More About this Research: Request A Free Sample

Major Developments in Japan Casting Polyurethane Market

- Tosoh's Major HDI Derivatives Expansion: Tosoh Corporation is investing 6 billion JPY to increase its hexamethylene diisocyanate (HDI) derivatives capacity by 50% at its Nanyo Complex, targeting completion by August 2026. This directly impacts the supply of high-performance polyurethane raw materials.

- Nippon Polyurethane's New MDI Plant: In a coordinated move at the Nanyo Complex, Nippon Polyurethane Industry is constructing a new MDI plant designed to add 200,000 tons of annual production capacity, significantly boosting a core polyurethane feedstock.

- Tosoh's Regional MDI Investment: Expanding its footprint, Tosoh is investing 4,230 billion VND in a new chemical facility in Vietnam, which will have the capacity to produce up to 125,000 tons of MDI annually, strengthening regional supply to Japan.

- Mitsui Chemicals' Price Revision (2025): Effective May 1, 2025, Mitsui Chemicals announced a strategic price increase of +15 JPY/kg or more for its polyurethane raw materials, including TDI, MDI, and polyols, signalling strong casting polyurethane market demand.

- Tosoh's Price Increase (2024): Preceding Mitsui's move, Tosoh raised its MDI prices by over 45 JPY/kg effective June 17, 2024, reflecting immediate cost pressures and a tight supply-demand balance.

- Tosoh's Biopharma Capacity Growth: Tosoh Corporation is increasing its purification media production capacity by 70%, a strategic investment targeting the high-value biopharmaceutical sector, which uses specialty polyurethane-related materials.

- Mizuho Bank's 3D Printing Investment: Signaling confidence in a key polyurethane application area, Mizuho Bank invested US$ 3.5 million into 3DEO in 2024 to advance its additive manufacturing technology.

- ADEKA's U.S. Production Hub: Japanese chemical firm ADEKA Corporation is investing $40 million to establish a new production site in South Carolina, USA, enhancing its global supply chain for resins and polymer additives that serve the polyurethane industry.

- JSR's Acquisition by JIC: In a major strategic move, the government-backed Japan Investment Corp (JIC) completed its $6 billion tender offer for JSR Corp in 2024, aiming to bolster Japan's advanced materials sector, including key polyurethane-related photoresists.

- Toyota Industries' Forklift Shipment Resumption: From January 8, 2025, Toyota Industries plans to resume shipments of key forklift models, estimated at 6,000 units annually, representing a direct, predictable offtake for polyurethane in industrial tires and components.

Top Companies in the Japan Casting Polyurethane Market

- DIC Corporation

- Toagosei Co., Ltd.

- Asahi Kasei Group

- Sekisui Chemical Group

- Ube Corporation

- Freeman Japan

- Other Prominent Players

Market Segmentation Overview

By Product Type

- Rolls

- Formwork

- Pads

- Sheets

- Others

By Prepolymer Type

- Polyester Base Prepolymer

- Polyether Base Prepolymer

- Polycaprolactone Base Prepolymer

- Others

By Resin Grade

- Standard Grade

- High-Performance Grade

- Specialty Grade

- Others

By Manufacturing Process

- Reaction Injection Molding (RIM)

- Casting (Liquid Polyurethane)

- Extrusion

- Compression Molding

- Others

By Design

- Rigid

- Flexible

- Foamed

- Elastomeric

- Others

By Application

- Industrial Castings

- Wheels & Tires

- Belt & Hoses

- Medical Devices

- Footwear Components

- Concrete Blocks

- Others

By Distribution Channel

- Direct Sales

- Online Sales

- Distributors/Wholesalers

By Industry

- Automotive

- Mechanical

- Electronics & Instruments

- Aerospace & Defense

- Footwear & Sports

- Healthcare

- Others

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |