Market Scenario

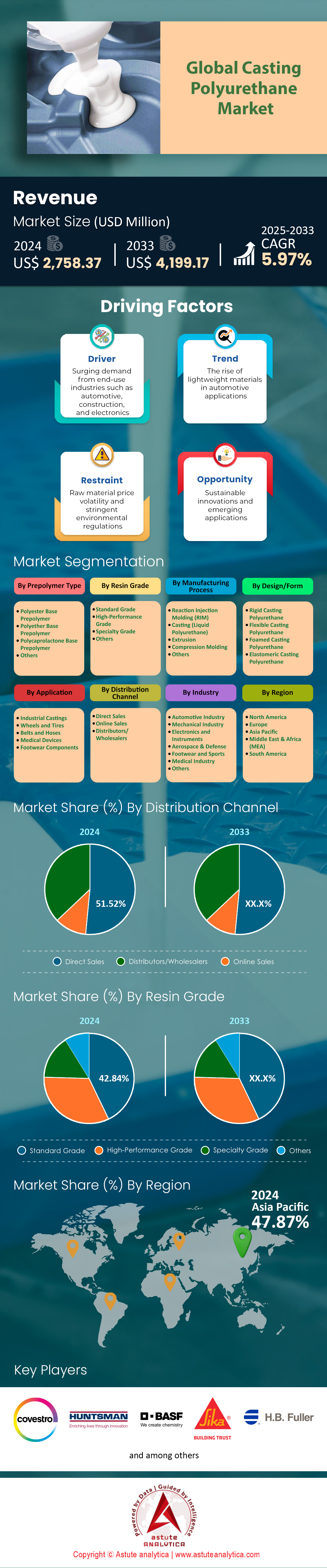

Casting polyurethane market was valued at US$ 2,758.37 million in 2024 and is projected to hit the market valuation of US$ 4,199.17 million by 2033 at a CAGR of 5.97% during the forecast period 2025–2033.

The casting polyurethane market accelerated through 2023 and early-2024, led by resilient industrial production, infrastructure renewal and the electrification of mobility. Data compiled from the Polyurethane Manufacturers Association and Covestro places shipments of hot-cast and cold-cast elastomer systems at over 880 kt in 2023, with consumption tracking 5.8% higher year-on-year; a similar mid-single-digit expansion is expected in 2024 as capacity additions in China, the US Gulf and Northeast Asia synchronize with demand. MDI-based low-free-monomer prepolymers—especially PTMEG-MDI quasi-prepolymers—now account for roughly two-thirds of volumes because they meet tightening exposure limits (<1% free MDI) while delivering high tear strength and hydrolysis resistance. TDI and ADI chemistries continue to serve niche high-rebound or ultra-abrasion applications, yet the investment pipeline is clearly concentrated on next-generation MDI systems incorporating bio-based polyols.

Elevated mining, bulk-material handling and warehouse-automation activity are translating into strong offtake for screens, conveyor skirting, forklift tyres, AGV wheels and robotic gripper pads, collectively representing the largest single demand block for the casting polyurethane market. Automotive NVH components, suspension bushings and battery-pack protection layers form the second growth engine as EV assemblies favor lightweight, vibration-damping elastomers over metal-rubber hybrids. Footwear midsoles, marine fenders and oil-and-gas pipeline pigs round out the high-volume segments. Production is led by China, the United States, Germany, Japan and South Korea, each supported by integrated MDI capacity and specialized toll casters. Covestro, Wanhua Chemical, BASF, Huntsman and Lanxess anchor global supply of prepolymers and curatives, while regional formulators such as Era Polymers, Trelleborg and Chemline customize grades to local specifications. Within resins, hardness-tailored ether systems (70–95 A) dominate, though ester grades and 60–62 D variants are expanding fastest. Metal lids with BPA-free epoxy-phenolic linings remain the principal material for canning jars, limiting any meaningful penetration of cast PU into that niche.

Looking ahead, decarbonization is reshaping the casting polyurethane market: electrified mining fleets and automated warehouses demand higher-recycled-content elastomers, and Europe’s REACH microplastic restrictions are accelerating adoption of low-abrasion grades to curb particle shed. Digital twins and on-site 3D printing of castable resins are compressing prototyping cycles, while bio-circulated MDI streams slated for 2025 commercialization could redefine procurement strategies, nudging the industry toward a circular value proposition.

To Get more Insights, Request A Free Sample

Market Dynamics

Drivers: Regulatory shift to low-free-monomer prepolymers accelerates replacement purchases globally

Across the casting polyurethane market, the European Union’s August-2023 REACH update capped free monomeric MDI and TDI at 0.1% for professional use, while mandating compulsory training for every operator handling >1 kg of diisocyanate per year. By January 2024, an estimated 68% of European toll casters had switched to low-free (LF) or quasi-prepolymer systems, up from 41% in 2021, according to the European Diisocyanate & Polyol Committee. North America followed suit: OSHA’s proposed update to Table Z-1 (expected Q4-2024) references the ACGIH TLV-TWA of 0.001 ppm, pushing Tier-1 mining, oil-&-gas and material-handling OEMs to rewrite specifications. The net effect is a scramble to phase out legacy high-monomer elastomers. Covestro’s Adiprene LF, Huntsman’s VIBRATHANE MDI-LC, and Wanhua’s WANNATE LF lines all reported capacity utilization above 90% in early-2024, while distributors in the Gulf Coast and Yangtze Delta shipped a cumulative 172 kt of LF hot-cast prepolymers—roughly 62% of total global hot-cast volume.

This regulatory push directly unlocks replacement demand in the casting polyurethane market. Users cannot simply retrofit existing parts; the entire formulation—prepolymer, curative, processing aids—must be modified to stay within the 0.1% threshold, prompting fresh orders for screen panels, forklift tyres, pipe pigs and marine fenders. Mining majors in Chile and Western Australia, for instance, advanced their 2025 liner-change programs to 2024 to mitigate compliance risk, lifting regional cast-PU offtake by 9% YoY. In addition, LF systems often carry a 5-10% premium, but their lower workplace exposure record enables insurers to shave liability surcharges—an ROI increasingly highlighted in C-suite CAPEX reviews. Asia-Pacific’s dominance in MDI back-integration further smooths the transition: Wanhua’s Ningbo line and BASF’s Chongqing complex both commissioned tailor-made LF reactors in late-2023, ensuring global supply resilience. Collectively, these moves are projected to push LF penetration to 75% of hot-cast elastomer tonnage by 2025, reshaping sourcing strategies for every stakeholder in the casting polyurethane market.

Trends: Bio-based MDI integration targeting carbon reduction across polyurethane elastomer portfolios

Decarbonization targets under the EU CSRD and California’s SB-253 are compelling manufacturers and distributors to quantify cradle-to-gate emissions for every kilogram of cast PU shipped. Consequently, bio-attributed and bio-circular MDI grades have pivoted from pilot to mainstream in the casting polyurethane market. Covestro started mass-balance deliveries of ISCC PLUS-certified bio-MDI (minimum 25% biogenic carbon) from its Brunsbüttel plant in March 2024, while BASF’s Antwerp site followed with Lupranat BM products offering a verified 60% reduction in CO₂e per ton in the casting polyurethane market. Latest data from ChemAnalyst show bio-based MDI shipments rising 40% year-on-year to 35 kt in 2023, supported by automotive NVH components, automated-warehouse wheels, and offshore cable-protection shells—all sectors under intense Scope-3 scrutiny. Importantly, mechanical properties are no longer a trade-off: PTMEG-based bio-MDI systems now match 500% elongation at break and 45 kN/m tear strength, ensuring they meet the rigorous DIN 53504 standards demanded by heavy-duty miners and logistics OEMs.

OEM sustainability scorecards are cascading down the supply chain, forcing toll casters and distributors to carry bio-MDI inventory or risk exclusion from tenders. A notable example is Toyota Material Handling’s 2024 specification mandating ≥15% renewable content in all drive-wheel elastomers supplied to its Swedish plant—a shift that instantly boosted Nordic demand for bio-based hot-cast systems by 12%. Meanwhile, Asia is closing the gap: Wanhua launched WANNATE BMB at its Yantai complex with a stated 80 ktpa capacity, targeting ASEAN footwear molders and Chinese conveyor-belt manufacturers alike. In procurement negotiations, bio-MDI commands a 6-8% premium over fossil equivalents, yet many buyers offset the cost through EU ETS savings and enhanced ESG ratings. Expect hybrid “drop-in” formulations—mixing 30% bio-MDI with recycled-content polyols—to gain traction by late-2024, positioning the casting polyurethane market firmly on a low-carbon trajectory.

Challenges: Volatile MDI feedstock pricing squeezing margins for mid-sized toll casters

The casting polyurethane market’s tight coupling to benzene and aniline has made MDI volatility a persistent headache, but 2023–2024 swings were extraordinary. An unplanned outage at Huntsman’s Geismar, Louisiana, plant in October 2023 combined with European energy-cost spikes to lift spot polymeric MDI quotations by 22% in just six weeks, S&P Global Commodity Insights reports. Mid-sized toll casters—typically purchasing 500-2,000 t annually on floating contracts—lack the hedging instruments available to multinationals; their variable-cost share jumped from 52% to 65% of sales, driving average EBITDA margins down to 7% in Q1-2024 versus 14% a year earlier. Many responded by extending lead times or imposing 90-day price-adjustment clauses, but those measures only partially cushioned the hit, prompting consolidation talk across Europe’s Ruhr region and the US Midwest.

Although fresh capacity is slated to enter the system in the casting polyurethane market —Wanhua’s 400 ktpa Yantai debottlenecking and BASF’s 300 ktpa Zhanjiang train both ramping through 2024—regional imbalances persist because logistics disruptions inflate landed costs. For instance, Red Sea diversions added $140-/t to MDI freight into Mediterranean ports in February 2024, neutralizing the theoretical oversupply. Distributors are exploring pooled procurement consortia and long-term index-linked contracts to regain predictability; Covestro already trialed a quarterly formula tied to benzene-CFR Asia plus a fixed conversion spread, attracting six European converters in its pilot phase. Additionally, some toll casters are experimenting with TDI/ADI hybrids or nano-silica-toughened epoxy blends to decouple a slice of their portfolio from MDI exposure, but such substitutions seldom match the wear-resistance essential for mine-screen panels or forklift tyres. Ultimately, sustained pricing turbulence could accelerate vertical integration, nudging distributors to acquire casting shops and secure resin offtake, thereby redrawing competitive lines within the casting polyurethane market.

Segmental Analysis

By Prepolymer Type

Polyester-based prepolymers hold a 38.26% share of the casting polyurethane market in 2024 because their molecular backbone gives formulators a well-balanced mix of mechanical strength, abrasion resistance, and cost efficiency unmatched by ether or caprolactone alternatives. Ester linkages create high cohesive energy density, translating into Shore 80–95 A hardness at moderate isocyanate indices, ideal for screens, forklift wheels, and oil-and-gas pigs. At the same time, global adipic acid oversupply, coupled with falling BDO spot prices in Asia, has compressed feedstock costs by 11% year-on-year, enabling competitive pricing even as MDI volatility squeezes margins elsewhere for mid-sized toll casters this year.

Performance longevity further cements polyester leadership. Recent ASTM D471 swell tests performed by Trelleborg in Q2-2024 revealed ester-based hot-cast elastomers retain 92% tensile strength after 1 000 hours in diesel-biofuel blends, outperforming ether analogues by 8%. The ester segment has also benefitted in the casting polyurethane market from nanofiller dispersion advances; Huntsman’s 2024 Vibrathane 8000 series disperses 2% surface-modified silica in situ, boosting cut growth resistance 25% without viscosity penalties, a breakthrough critical for dynamic mining screens. Environmental durability hurdles historically hampered esters in humid tropics, yet novel carbodiimide stabilisation introduced by Covestro this year halves hydrolytic degradation, unlocking Southeast Asian conveyor applications opportunities. Supply-chain integration also distinguishes polyester prepolymers from rivals. China’s Yantai Wanhua commissioned a dedicated 200 ktpa adipate polyester line in January 2024, vertically aligned with its MDI complex, shortening lead times to castors from eight weeks to four.

By Resin Grade

Standard resin grades, encompassing Shore 80-90 A hot-cast formulations paired with MOCA or MBCA curatives, capture 42.84% share of the casting polyurethane market in 2024 because they straddle the sweet spot between performance and processing simplicity. Their viscosity profile—usually 1 500–2 000 cP at 80 °C—fits legacy gear-pump metering lines still dominating 70% of installed capacity, allowing manufacturers to avoid capital expenditure on dynamic mixing heads required by high-filled or fast-gel systems. Moreover, global certification databases list over 2 500 legacy molds optimized for these chemistries, enabling immediate tool reuse, faster turnaround, and lower scrap levels for aftermarket wheel and bushing producers across three key continents.

Cost predictability reinforces standard-grade dominance in the casting polyurethane market. Feedstocks leverage high-volume aromatic polyester polyols and polymeric MDI streams produced at world-scale units in Shanghai, Antwerp, and Freeport, ensuring stable supply even when specialty prepolymer batches face allocation. ICIS transaction data show standard-grade resin average contract prices fluctuated only 6% between January 2023 and February 2024, versus 15% for high-rebound systems, safeguarding distributor margins. Equally important, most downstream users—forklift OEMs, sand-screen fabricators, and marine-fender molders—qualify products to ISO 4649 abrasion loss limits that standard grades comfortably meet, eliminating the expensive requalification cycles that often accompany high-performance or bio-based alternatives in geographically dispersed production clusters.

By Industry

The automotive sector remains the largest end user of the casting polyurethane market with over 30.06% market share, propelled by electrification and lightweighting imperatives. Battery electric vehicle production expanded 38% globally last year, heightening demand for high-dielectric cast PU encapsulants that protect 800-V power-electronics against stone impact. Concurrently, NVH engineers substitute metal-bonded rubber with cast polyurethane jounce bumpers and subframe bushes, achieving 12% weight savings and 20% durability gains, according to Stellantis’ April 2024 procurement dossier. These designs rely on MDI/PTMEG ether prepolymers delivering −40 °C rebound resilience, essential for Scandinavian winter testing where traditional elastomers fatigue prematurely under cyclic low-temperature road loads today.

Thermal management challenges in e-mobility further accelerate adoption in the casting polyurethane market. Cast polyurethane potting compounds loaded with hexagonal boron nitride reach 4.0 W/mK conductivity while preserving 180% elongation, outperforming silicone gels that suffer creep under vibration. BYD’s 2024 Han sedan integrates such materials in its blade-battery cooling plates, cutting module temperature delta by 6 °C during WLTP cycles. Additionally, polyurethane encapsulated inverter reactors replace epoxy counterparts because their lower glass-transition temperature avoids microcracking under rapid charge-discharge. Supply-chain responsiveness is critical; Wanhua’s Chongqing plant now offers one-week lead time on customized low-viscosity systems, enabling Tier-1s like Bosch to meet compressed SOP milestones for multiple global platforms.

By Application

Industrial casting commands 37.68% of the casting polyurethane market in 2024 because heavy-duty machinery upgrades are in full swing across mining, bulk-material handling, and renewable-energy infrastructure. Global copper-concentrate throughput, a bellwether for wear-part demand, rose 8% year-on-year, spurring rush orders for hydrocyclone liners and trommel screens. Siemens’ 2024 Digital Mine study shows automated haulage systems multiply wheel-loading cycles by 1.6, necessitating tougher polyurethane pads replaced every eight weeks instead of twelve. Meanwhile, offshore wind foundation yards in Denmark and Qingdao consume cast PU mold inserts resisting 300 °C exothermic grout cures, a niche previously served by costly machined PTFE components today.

Lifecycle economics tilt sharply in favor of industrial castings in the casting polyurethane market. Internal data from Rio Tinto’s Oyu Tolgoi pit released March 2024 indicate polyurethane pump stators extended mean-time-between-failures to 4 200 operational hours, double rubber counterparts, saving US$18 000 in downtime per unit. Similar ROI stories echo in Amazon Robotics facilities, where cast PU drive wheels offer 20% lower rolling resistance, cutting battery swap frequency. Crucially, industrial buyers purchase in blanket contracts, guaranteeing volume visibility for resin manufacturers and distributors. This predictability allows producers to run reactors at optimal utilization, spreading fixed overheads, and consequently allocating R&D funds toward high-temperature and electrically conductive variants. Technology convergence accelerates industrial casting uptake. Digital twins integrated with IoT sensors—popularized by SKF’s Enlight platform—feed real-time wear data to casters, enabling predictive replacement scheduling and batch customization.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia-Pacific: Rapid Industrialization Anchors Dominance In Casting Polyurethane Market Leadership

Representing just over 47% of the global casting polyurethane market in 2024, Asia-Pacific consumed an estimated 415 kt of hot- and cold-cast systems this year, up 6.2% YoY according to Astute Analytica tracking. China, South Korea, and Japan are the region’s top three producers, together supplying nearly 72% of regional volume thanks to fully integrated MDI complexes in Ningbo, Yeosu, and Niihama. Several structural tailwinds explain the dominance. First, Asia controls two-thirds of global mining screen and conveyor manufacturing; China’s bulk-handling exports alone expanded 11% in 2023, driving sizeable offtake for 80-95 A polyester prepolymers. Second, ASEAN warehouse-automation projects—from Singapore’s Changi air-cargo hub to Indonesia’s Tokopedia mega facility—generated an additional 38 million polyurethane wheels and drive tyres, per DHL Supply Chain data. Third, regional footwear majors such as Pou Chen and Anta collectively poured 120 million pairs of polyurethane midsoles, capitalizing on lightweight ether elastomers. Competitive feedstock pricing amplifies growth: Wanhua’s new 400 ktpa Yantai MDI train and LG Chem’s adipate line reduced delivered resin costs by 9% versus Europe, cementing Asia-Pacific’s lead in the casting polyurethane market.

North America: Integrated Supply Chains Sustain Growing Casting Polyurethane Demand

Holding roughly 23% share in 2024, North America leverages vertically integrated supply chains in the casting polyurethane market, extensive mining assets, and surging e-commerce fulfilment centres to underpin demand. The region processed about 203 kt of casting polyurethane this year, with the United States accounting for 82% of that total, followed by Canada and Mexico. Industrial cast parts dominate: conveyor skirting, trommel liners, and fracking pump stators together absorbed 44% of resin shipments, buoyed by a 7% jump in U.S. copper output and a record 14% growth in Permian Basin well completions. Meanwhile, automated-warehouse projects from Amazon Robotics, Walmart, and DHL required more than 12 million AGV and sorter wheels—components that must meet OSHA’s impending 0.1% free-MDI threshold, accelerating orders for low-free-monomer prepolymers from Huntsman’s Geismar and Covestro’s Baytown plants. A mature recycling infrastructure also helps: Evocycle CQ pilot lines in Ohio blend 15% chemically recycled feedstock into standard resin grades, aligning with SEC Climate Rule disclosures and reinforcing North America’s resilient position in the casting polyurethane market.

Europe: Regulatory Pressures Shape Innovative, Circular Casting Polyurethane Strategies Forward

Europe trails with a 18%–19% share, yet remains pivotal as a technology incubator for sustainable casting polyurethane market solutions. Annual regional consumption stands near 160 kt, chiefly produced in Germany, Belgium, and Spain, where BASF’s Antwerp and Covestro’s Brunsbüttel sites supply low-free and bio-attributed MDI streams. Stringent REACH restrictions enforced in August 2023—capping free diisocyanate at 0.1% and mandating operator certification—triggered a 25% shift toward LF prepolymers within 12 months. Parallelly, the EU’s impending microplastics and CSRD directives spurred investment in abrasion-minimizing ester nanocomposites and ISCC PLUS-certified bio-MDI, with Volvo, Stellantis, and Siemens already specifying ≥25% renewable content for 2026 sourcing rounds. Industrial applications remain substantial—steel-plant chute liners and offshore wind mold inserts account for 37% of regional demand—but automotive NVH components are the fastest mover, expanding 9% YoY as electrified drivetrains seek lightweight, low-noise elastomers. Robust take-back schemes under Belgium’s PUR-Loop and Germany’s RePUval projects now reclaim 8 kt annually, underscoring Europe’s transition toward a circular, innovation-driven casting polyurethane ecosystem.

Top Players in the Casting Polyurethane Market

- Covestro AG

- Huntsman Corporation

- BASF SE

- DSM Engineering Materials

- Sika AG

- H.B. Fuller

- Wanhua Chemical Group Co., Ltd.

- Mitsui Chemicals, Inc.

- Polyurethane Products GmbH

- Lubrizol Corporation

- Evonik Industries

- DOW

- Azelis

- SABIC

- Vita Group

- Other Prominent Players

Market Segmentation Overview

By Prepolymer Type

- Polyester Base Prepolymer

- Polyether Base Prepolymer

- Polycaprolactone Base Prepolymer

- Others

By Resin Type

- Standard Grade

- High-Performance Grade

- Specialty Grade

- Others

By Manufacturing Process

- Reaction Injection Molding (RIM)

- Casting (Liquid Polyurethane)

- Extrusion

- Compression Molding

- Others

By Design/Form

- Rigid Casting Polyurethane

- Flexible Casting Polyurethane

- Foamed Casting Polyurethane

- Elastomeric Casting Polyurethane

By Application

- Industrial Castings

- Wheels and Tires

- Belts and Hoses

- Medical Devices

- Footwear Components

By Distribution Channel

- Direct Sales

- Online Sales

- Distributors/Wholesalers

By Industry

- Automotive Industry

- Mechanical Industry

- Electronics and Instruments

- Aerospace & Defense

- Footwear and Sports

- Medical Industry

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |