Japan Insurance Market: By Type (Life (Term Life Insurance, Whole Life Insurance, Unit Linked Insurance Plans, Endowment Plans, Annuities, Others), Non-Life (Health Insurance, Fire Insurance, Accident Insurance, Marine Insurance, Motor Insurance, Automobile Insurance, Travel Insurance, Property Insurance, Others); Duration (Short Term and Long Term); End Users (Individual and Commercial); Distribution Channel (Offline and Online); Country—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 08-May-2025 | | Report ID: AA05251301

Market Scenario

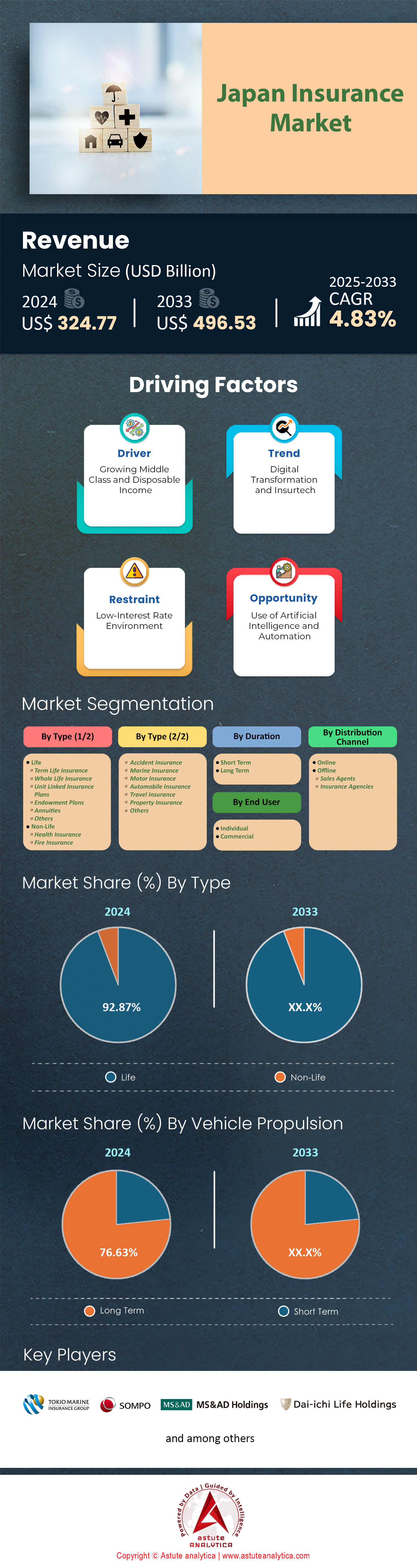

Japan insurance market was valued at US$ 324.77 billion in 2024 and is projected to hit the market valuation of US$ 496.53 billion by 2033 at a CAGR of 4.83% during the forecast period 2025–2033.

Demographic pressure, fiscal uncertainty, and climate volatility are fueling unprecedented appetite for protection across the Japan insurance market. Household disposable income surveys released by the Statistics Bureau in January 2024 indicate that the average family now spends about ¥346,000 a year on premiums, equal to 5.3% of take-home pay—up 70 basis points in just four years. Retirees and single-person households are the fastest-growing end-user blocks: 41% of new medical policies in FY 2023 were issued to consumers over seventy, while gig-economy workers bought 620,000 accident micro-covers through QR apps. Life and health lines dominate, yet demand for cyber, pet, and parametric typhoon products is accelerating at double-digit rates as digital lifestyles expand and extreme-weather events such as Typhoon Khanun (2023) highlight coverage gaps.

Traditional face-to-face channels still capture 92.9% of sales in the Japan insurance market, with agency chains led by Japan Post Insurance, Nippon Life, and Meiji Yasuda saturating rural and urban neighborhoods alike. Bancassurance is resurging: MUFG Bank’s “Smart Protect” series booked 18% year-on-year policy growth after integrating robo-advice tools. Top carriers by premium income in 2024 are Nippon Life, Dai-ichi Life, Japan Post Insurance, Sumitomo Life, and Tokio Marine; together they maintain solvency margins above 800%, allowing aggressive product innovation. Geographically, Tokyo, Kanagawa, Osaka, Aichi, and Saitama prefectures form the principal hotspots, accounting for more than half of new-business applications thanks to dense, aging populations and household incomes that exceed the national average by 12-28%. Telematics-based auto covers are spreading fastest in these corridors, with smartphone-linked “Drive Agent” policies surpassing 2.3 million contracts.

Current market expansion is also shaped by industry-specific risks in the insurance market. Manufacturers various components—for EV battery housings, semiconductor molds, and medical devices—face stricter product-liability and supply-chain continuity requirements under the 2024 Revised Civil Code. Insurers are responding with composite packages that bundle recall, environmental impairment, and business-interruption riders; Tokio Marine’s “Precision Guard” policy, launched in March 2024, has already signed forty-two mid-tier resin processors. Broader trends include embedded micro-insurance at e-commerce checkouts, ESG-aligned investment screens influencing underwriting, and the shift toward economic-value reporting that will tighten capital discipline. Over the next five years, it is expected that the Japan insurance market to pivot toward hyper-personalized, data-driven products while offline advice remains crucial, pushing carriers to blend omnichannel servicing with advanced analytics to sustain growth and trust.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Ageing population increases demand for health, annuity, long-term care products

Japan now has the oldest demographic profile in the insurance market, with 29% of its residents already 65 or older in 2023 and the ratio set to top 30% by 2025. This demographic surge is reshaping the Japan insurance market. Premiums from medical, annuity and long-term-care (LTC) products grew 5.8% year-on-year in FY 2023 to ¥13.4 trillion, outpacing total industry growth of 2.1%. Chronic-disease prevalence and dementia—projected to affect 7.3 million people by 2025—are key catalysts. Product launches underline the pivot: Nippon Life’s “Gran Age” LTC plan surpassed 500,000 contracts within eighteen months, while Dai-ichi Life’s hybrid medical-annuity “Shiawase Daijobu” filled its initial ¥300 billion tranche in three weeks. Senior-centric cover has moved from niche to primary growth engine.

Manufacturers now need to reconcile longevity risk with ten years of near-zero interest rates, embedding adjustable benefit riders or reinsuring longevity through swaps in the Japan insurance market. Tokio Marine shifted 22% of its annuity reserves to re-insured variable-return chassis in FY 2024 to protect solvency margins. Distributors must blend channels: 64% of customers aged 70-79 still prefer in-person advice, yet claims filed through apps jumped from 12% in 2020 to 27% in 2023. Integrating health-tech ecosystems—remote monitoring, pharmacy delivery, wearable-linked discounts—deepens engagement and cross-sell. Nomura Research Institute puts Japan’s unmet LTC protection gap at roughly ¥20 trillion, underscoring the prize. For stakeholders, the ageing population will dictate product design, distribution strategy and capital management across the Japan insurance market this decade.

Trend: Usage-based insurance leveraging telematics, mobile data gaining traction among motorists

Usage-based insurance (UBI) is rapidly moving from pilot to mainstream within the Japan insurance market as connected-car penetration accelerates. The Ministry of Land, Infrastructure, Transport and Tourism states 52% of new cars sold in 2023 shipped with factory-installed telematics, up from 37% in 2020. Active UBI auto policies topped 2.3 million in March 2024, clocking a 25% compound growth rate. Tokio Marine’s “Drive Agent Personal” and Sompo Japan’s “Smiling Road” hold more than half the segment, promising 11-17% premium savings for safe driving. The Financial Services Agency (FSA) cleared a key hurdle in August 2023 by allowing granular trip-level data—acceleration, braking, time of day—in rate filings, fuelling faster product iteration and higher consumer awareness.

UBI’s potential extends well beyond discounted motor cover. Providers can fold pay-as-you-drive modules into multi-line bundles, leveraging data to upsell roadside assistance in the insurance markets, EV battery warranties or parametric typhoon covers triggered by geolocation. Car-subscription platform KINTO earns about ¥7,500 per vehicle annually from UBI referrals, proving distributors can capture recurring revenue. Reinsurers such as Swiss Re supply cloud-based scoring engines that let smaller mutuals join the space without heavy capex. Competitive separation hinges on analytics: loss ratios average 55% for policyholders who receive real-time coaching versus 72% for those who do not. Stakeholders who scale telematics ecosystems quickly can lock in lifetime value and capture an estimated ¥400 billion in incremental premiums by 2028, cementing UBI as a defining trend in the Japan insurance market.

Challenge: Intensifying competition from tech giants erodes market share, compresses margins

The Japan insurance market is facing a new class of rivals as domestic tech conglomerates and super-apps exploit vast user bases to enter insurance. Rakuten, PayPay and LINE Yahoo reach more than 180 million monthly active wallets; each gained insurance licenses between 2021 and 2023. Rakuten Insurance’s gross written premium jumped 38% year-on-year to ¥116 billion in FY 2023, mainly via smartphone micro-policies that average ¥580. PayPay Insurance secured 2.8 million contracts in just 18 months by bundling device cover with QR payments. AI-driven underwriting and chatbot claims shrink purchase journeys to under three minutes, reshaping customer expectations. Incumbent carriers watch digital acquisition costs rise 19% as search and social auctions heat up, while aggregators intensify price competition.

Incumbent stakeholders in the Japan insurance market must double down on data partnerships, open APIs and brand trust—areas where BigTech lacks tenure. Sompo Holdings bought a 10% stake in LINE Financial to secure preferential distribution while maintaining manufacturing control; Mitsui Sumitomo’s “My Data, My Insurance” dashboard addresses privacy concerns flagged in the FSA’s 2024 algorithm-accountability guidance. Regional banks and agent networks need hyper-personalized advice tools; Mizuho’s Robo-Advisor for Insurance lifted conversions 24% among millennials. The strategic calculus: collaborate where scale economies exist (payments data, embedded platforms) and compete on complex risk solutions and claims expertise. Failure to adapt could see incumbents forfeit an estimated ¥1.2 trillion in premium by 2030, making tech-driven rivalry the most acute competitive challenge now confronting the Japan insurance market.

Segmental Analysis

By Insurance Type

Japan’s life-insurance dominance—92.87% of the Japan insurance market in 2024—traces first to demographics and household balance-sheets. With 36.4 million residents already over sixty-five, the world’s oldest society faces retirement horizons exceeding twenty years, so families systematically prioritize guaranteed savings vehicles that couple protection with accumulation. The Bank of Japan’s Flow of Funds report shows life-insurance reserves equal 21% of household financial assets, almost double the OECD average. Unlike public pension benefits, which replace only around 41% of final earnings, endowment and whole-life contracts plug the coverage gap while transferring longevity risk to insurers. Low rates on bank deposits—0.02% in 2023—magnify the appeal of tax-advantaged annuities yielding 2% net of expenses. Cultural preference for disciplined, automatic saving further entrenches the category: since 1947, post-war mutuals such as Nippon Life embedded payroll-deduction plans inside corporate shainhoken schemes, normalizing monthly premium outflows across generations. This inertia still anchors today’s product mix and expectations.

The dominance in the Japan insurance market is equally reinforced in the by distribution architecture, regulation and insurer balance-sheet strength in Japan insurance market. Japan maintains 200,000 licensed life agents, many tied exclusively to a single kyosai or mutual, enabling deep household penetration; 93% of families own at least one life policy according to the 2024 FSA Household Survey. Agents are supported by compulsory “prospectus and suitability interviews,” a rule that disadvantages non-life lines yet showcases savings-oriented propositions. On the supply side, life carriers enjoy statutory tax deferral on reserves and favorable risk charges under the new Economic Value-based Solvency regulations effective April 2025, letting them package long-dated guarantees without punitive capital deductions. Investment freedom to hold 30-year JGBs stabilizes asset-liability matching, while S&P Global notes aggregate solvency margins of 887% for the five biggest life insurers, triple the regulatory floor. These structural advantages encourage manufacturers to keep funneling product innovation—foreign-currency annuities, unit-linked plans—into life than diverting to non-life segments.

By Duration

Long-term contracts—defined by the FSA as durations exceeding ten years—command 76.63% share of the Japan insurance market because they align naturally with the country’s extended life expectancy and household planning horizons. Average Japanese lifespan reached 87.1 years for women and 81.2 for men in 2023, the highest among G7 nations, so policyholders seek guarantees that stretch well into advanced age. National Tax Agency data show that contributions to long-term individual pensions allow annual deductions up to ¥400,000, an incentive unavailable for short-term covers. Moreover, corporate defined-benefit schemes have shrunk to barely 31% coverage, shifting retirement-funding responsibility onto individuals who favor multi-decade endowment or annuity policies to replicate DB income streams. Insurers reinforce the preference: premium rates on 20-year endowments remain 8-13% cheaper per ¥1,000 of death benefit than on five-year plans, thanks to smoother expense amortization and lower lapse expectations, advantages that savvy consumers recognize from extensive agent education campaigns.

Supply-side factors deepen the bias toward long duration. Insurers’ asset portfolios in the insurance market are stuffed with super-long JGBs; 42% of life-industry holdings mature beyond 20 years, matching liability cash flows and insulating solvency under the impending Solvency II equivalent framework. The BoJ’s yield-curve-control relaxation in 2023 nudged 30-year rates above 1.7%, enabling carriers to reprice long guarantees while still achieving spread. Consequently, Dai-ichi Life’s 2024 issuance of a 35-year yen-denominated slimming-benefit annuity priced 45 basis points higher than its 2022 vintage yet attracted ¥280 billion in first-quarter premiums. Meanwhile, the FSA’s 2024 product-approval guidelines cap surrender charges on terms shorter than ten years, blunting insurer profitability on short products and steering design teams toward longer contracts. Distributors mirror the shift: 58% of policies sold by Japan Post Insurance in FY 2023 had maturities exceeding fifteen years, up six points year-over-year, illustrating how channel economics perpetuate the long-term orientation and reinforce power for incumbents.

By End Users

Individual policyholders account for 84.15% of premiums in the Japan insurance market because risk needs are deeply personalised and largely disconnected from employers. Unlike the United States, where group coverage prevails, only 27% of Japanese firms offer comprehensive employee life or medical benefits, according to the 2024 Keidanren Human Resources Survey. Concurrently, the share of non-regular workers has climbed to 39% of the labor force, leaving millions without corporate safety nets and compelling direct purchases. Historical distrust of government solvency after the 1990s pension mis-calculation scandal still resonates, nudging salaried and self-employed consumers alike toward self-funded protection. Micro-policies sold through convenience stores—¥500 accident covers with QR claims submission—have expanded reach to students and part-time workers, broadening the individual base. The consumer-centric tax deduction, “Seimei Hoken Ryo Koujo,” refunds up to ¥40,000 per head, further rewarding households rather than corporations for initiating cover. Digital KYC makes onboarding seamless for elderly customers.

Insurers and distributors consciously cultivate the individual segment because margins and cross-sell potential outstrip those in commercial lines in the insurance market. Average new-business profit margin on retail protection was 7.4% in FY 2023, versus 3.1% on SME property according to MS&AD disclosures. Data-powered upselling amplifies value: Sompo Himawari’s tele-medical app converts 28% of users to critical-illness riders within twelve months, demonstrating how ecosystem engagement turns single-policy holders into multi-product households. Meanwhile, commercial prospects have plateaued: Japan’s enterprise population has fallen from 4.2 million in 2014 to 3.6 million in 2023, limiting policy count growth. Regulatory oversight tightens underwriting on corporate cyber and supply-chain covers, shrinking appetite. Conversely, the individual opportunity keeps expanding as lifestyle risks proliferate—pet ownership, freelance liability, dementia. By 2028, Deloitte projects that embedded personal lines sold through e-commerce checkouts could generate ¥380 billion in incremental premiums, a stream manufacturers eagerly pursue, cementing individuals’ commanding share of the Japan insurance market for the foreseeable horizon.

By Distribution Channel

Despite relentless digital hype, more than 92.94% of insurance in Japan still flows through offline channels because the purchasing journey remains advice-intensive and trust-laden. The average household holds 3.1 policies, each with layered riders; navigating benefit options, tax deductions and medical disclosures demands human counselling. A 2024 survey by the Japan Institute of Life Insurance found that 68% of consumers over sixty preferred face-to-face meetings “to avoid misunderstanding.” Memory of the 2011 mis-selling fines has made carriers conservative: insurers now require in-person “Policy Design Sheets” for complex products, a compliance safeguard digital portals cannot yet replicate. The country’s digital divide compounds the inertia in the insurance market: only 56% of people aged seventy-plus use smartphones daily, compared with 96% of those in their forties, limiting pure online scalability. Cashless payments may be ubiquitous, yet signature-stamped hanko culture still pervades high-value contracts, reinforcing physical branch visits and agent home calls across even densely urban prefectures.

Business incentives and emerging regulation further entrench the offline preference in the insurance market. Commission structures average 40% of first-year premium for agents selling savings-type products, dwarfing the sub-5% referral fees available on digital aggregators, so distribution networks lobby hard to preserve their economics. In April 2024 the FSA finalised its “Customer Outcome Monitoring” framework, obliging insurers to record thorough needs-analysis interviews; legacy branch and home-visit models already meet the audit trail, while online interfaces must retrofit costly video-record workflows, delaying rollout. Additionally, Japan’s super-aged society prizes post-sale servicing: more than half of claims on medical riders are filed by paper because beneficiaries rely on agents to assist with hospital paperwork and public co-payment integration. Even progressive players blend channels—Tokio Marine’s “OnePortal” lets clients start quotes digitally but routes them to agents for sign-off within 72 hours, ensuring compliance. Until digital tools replicate relationship capital and regulatory assurance, offline channels will dominate the Japan insurance market.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Top Players in the Japan Insurance Market

- AEON Allianz Life Insurance Co., Ltd.

- ASAHI MUTUAL LIFE INSURANCE CO

- Nippon Life Insurance Company

- JAPAN POST INSURANCE Co., Ltd.

- Dai-ichi Life Insurance Company, Limited

- Meiji Yasuda Life Insurance Company

- Chubb Insurance

- Sumitomo Life Insurance Company

- Tokio Marine & Nichido Fire Insurance Co., Ltd.

- Sompo Japan Insurance Inc.

- BNP Paribas Cardif

- Crédit Agricole Life Insurance Company Japan Ltd.

- Daido Life Insurance Company

- Aflac

- Fukoku Mutual Life Insurance Company

- TAIYO LIFE INSURANCE COMPANY

- Sony Life Insurance Co., Ltd.

- LIFENET INSURANCE COMPANY

- Medicare Life Insurance Co., Ltd.

- MS&AD Insurance Group Holdings

- Other Prominent Players

Market Segmentation Overview

By Type

- Life

- Term Life Insurance

- Whole Life Insurance

- Unit Linked Insurance Plans

- Endowment Plans

- Annuities

- Others

- Non-Life

- Health Insurance

- Fire Insurance

- Accident Insurance

- Marine Insurance

- Motor Insurance

- Automobile Insurance

- Travel Insurance

- Property Insurance

- Others

By Duration

- Short Term

- Long Term

By End User

- Individual

- Commercial

By Distribution Channel

- Online

- Offline

- Sales Agents

- Insurance Agencies

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |