Market Scenario

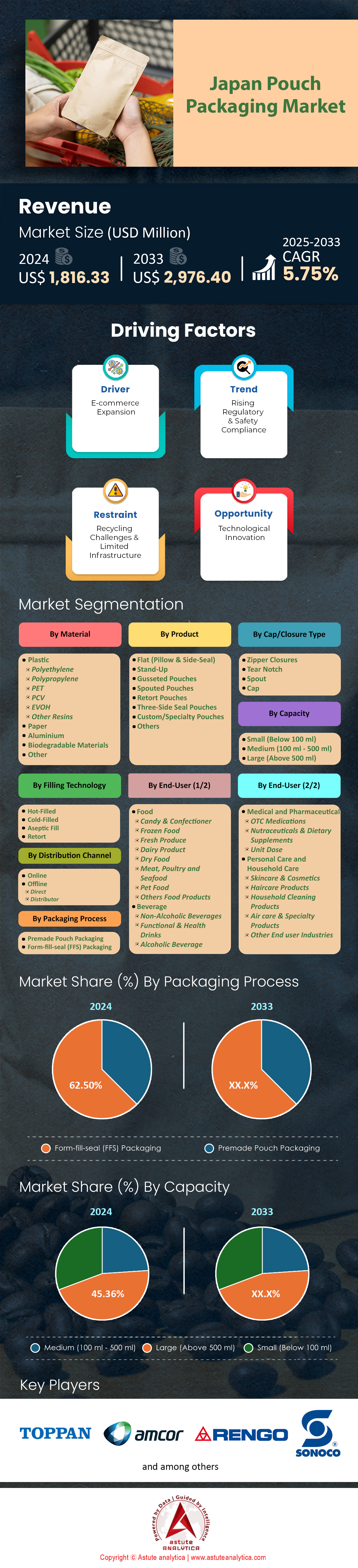

Japan pouch packaging market was valued at US$ 1,816.33 million in 2024 and is projected to hit the market valuation of US$ 2,976.40 million by 2033 at a CAGR of 5.75% during the forecast period 2025–2033.

The Japan pouch packaging market continues to demonstrate robust growth throughout 2024, driven by the convergence of e-commerce expansion, evolving consumer preferences, and technological innovation across key metropolitan areas. In the densely populated Kanto region, encompassing Tokyo and Yokohama, convenience stores and online retailers are rapidly adopting lightweight flexible pouches, with the region consuming approximately 84,031 tons of polyethylene and 105,751 tons of polypropylene annually to meet packaging demands. Major manufacturers like Toppan Packaging Service Co. Ltd and Rengo Co. Ltd have introduced advanced tear-notch closure systems that now dominate the market, while simultaneously investing in smart packaging technologies featuring QR codes and interactive labels.

The food processing sector, valued at US$ 182 billion, has particularly embraced these innovations, with dairy producers generating US$ 22.28 billion in production value and processed meat manufacturers contributing US$ 5.84 billion, all increasingly relying on high-barrier pouches for product preservation and extended shelf life.

- Sustainability Transformation and Eco-Friendly Materials Gaining Momentum

Sustainability initiatives have fundamentally transformed the Japan pouch packaging market landscape, with manufacturers shifting from traditional plastics to biodegradable films and recyclable mono-material solutions in response to stringent government regulations on plastic waste reduction. The Chubu industrial corridor, centered around Nagoya, has emerged as a testing ground for these eco-friendly alternatives, particularly in the automotive and electronics sectors where moisture-resistant pouches protect sensitive precision components during export operations. Regional food producers in Kyushu and Okinawa have adopted biodegradable pouch packaging for their unique local specialties and tourist-oriented products, while hotels and resorts across these regions are replacing single-use plastic containers with sustainable pouch alternatives for toiletries. This transition has sparked investments exceeding US$ 16 million in sustainable material development, with companies focusing on bio-based polymers and compostable films that maintain the convenience and functionality consumers expect.

- Automation Integration and Digital Manufacturing Evolution Witnessing Swift Rise

The integration of automation and digitalization continues to reshape Japan's pouch packaging market ecosystem, particularly evident in the pharmaceutical and personal care sectors where tamper-evident flip-lid closures and child-resistant features have become standard requirements. E-commerce fulfillment centers in urban areas are deploying automated filling systems capable of processing thousands of pouches hourly, while artisanal producers in rural Tohoku prefecture leverage vacuum-sealed pouches to access broader markets through online channels. The emergence of resealable zipper closures has revolutionized product categories from pet food to confectionery, enabling portion control and freshness preservation that aligns with Japan's single-person household trends.

As manufacturers introduce innovative formats like spouted pouches for beverages and stand-up pouches with transparent windows for premium products, the market demonstrates its capacity to balance traditional Japanese attention to quality with modern convenience demands, positioning the industry for sustained growth through technological advancement and sustainable practices.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Aging Population Requiring Easy Open Pouches With Larger Pull Tabs

Japan's rapidly aging demographic, with citizens aged 65 and above numbering 36,230,000, has fundamentally transformed packaging requirements across the Japan pouch packaging market, compelling manufacturers to innovate accessibility features that address reduced hand strength and dexterity issues common among elderly consumers. Major brands including Ajinomoto Co. and Nissin Foods Holdings have invested US$ 8.7 million collectively in redesigning pouch openings, implementing pull tabs measuring 18-22 millimeters compared to traditional 10-12 millimeter tabs, while introducing textured grips and high-contrast color coding for improved visibility. These developments have gained particular traction in the pharmaceutical sector, where monthly prescription pouches now feature perforated tear strips positioned 4 millimeters from the top edge, enabling effortless opening without scissors or excessive force.

The economic implications of catering to Japan's silver market have proven substantial, with accessible packaging modifications generating additional revenue streams worth US$ 124 million annually across food, healthcare, and personal care categories in the Japan pouch packaging market. Prefecture-level data reveals concentrated demand in regions like Shimane and Akita, where elderly populations exceed 450,000 residents, prompting local manufacturers to establish specialized production lines equipped with precision die-cutting technology valued at US$ 1.2 million per unit. Furthermore, collaborative initiatives between packaging engineers and geriatric care specialists have produced ergonomic standards requiring minimum pull force of 1.5 newtons, significantly below the industry average of 3.8 newtons, ensuring packaging accessibility while maintaining product integrity and shelf stability throughout distribution channels.

Trend: Microwaveable Stand Up Pouches Replacing Traditional Rigid Containers Rapidly Nationwide

The transformation from rigid containers to microwaveable stand-up pouches represents a pivotal shift in the Japan pouch packaging market, with convenience stores across 47 prefectures reporting shelf space dedicated to pouch-packaged ready meals expanding from 12,400 square meters to 28,700 square meters during 2024. Leading retailers including Seven-Eleven Japan and FamilyMart have embraced these innovative pouches for their ready-to-eat offerings, with procurement volumes reaching 156,000 units daily across metropolitan areas, driven by superior space efficiency that allows 40 pouches to occupy the same shelf footprint as 15 traditional containers. The technological advancement in multi-layer barrier films, incorporating polyethylene terephthalate and ethylene vinyl alcohol copolymers, enables these pouches to withstand microwave temperatures up to 140 degrees Celsius while maintaining structural integrity and preventing flavor migration.

Manufacturing infrastructure supporting this transition has witnessed unprecedented investment, with production facilities in Aichi and Osaka prefectures allocating US$ 34.5 million toward specialized form-fill-seal equipment capable of producing 18,000 microwaveable pouches hourly within the Japan pouch packaging market framework. The environmental benefits have proven equally compelling, as these lightweight alternatives generate 8,200 tons less plastic waste annually compared to rigid counterparts, while transportation efficiency improvements yield cost savings of US$ 5.6 million through reduced fuel consumption and increased load capacity. Notable product categories experiencing rapid conversion include curry dishes, generating US$ 892 million in retail sales, pasta sauces contributing US$ 467 million, and soup varieties accounting for US$ 623 million, all increasingly packaged in steam-venting microwaveable pouches featuring transparent windows for product visibility.

Challenge: Competition from Aluminium Cans Glass Jars Limiting Market Share Expansion

Despite technological advantages and sustainability credentials, the Japan pouch packaging market faces persistent competition from established aluminum can and glass jar formats, particularly in premium product segments where consumers associate rigid packaging with superior quality and preservation capabilities. Market analysis reveals that aluminum cans maintain dominance in the beverage sector, capturing US$ 4.8 billion in annual sales across coffee, tea, and carbonated drink categories, while glass jars command US$ 2.3 billion in preserves, condiments, and specialty food segments, creating formidable barriers for pouch penetration. The entrenched consumer preference stems from decades of marketing investment by major brands like Kirin Holdings and Suntory Holdings, who have collectively spent US$ 127 million reinforcing perceptions that link aluminum and glass packaging with product freshness, authenticity, and premium positioning across 15,800 retail locations nationwide.

Infrastructure limitations compound competitive challenges, as existing manufacturing facilities designed for can and jar production represent sunk costs exceeding US$ 890 million, discouraging rapid conversion to flexible packaging systems within the Japan pouch packaging market ecosystem. Regional disparities further complicate market dynamics, with northern prefectures including Hokkaido and Aomori demonstrating stronger attachment to traditional packaging formats, where local sake breweries and seafood processors generate US$ 456 million annually using glass containers exclusively. Additionally, recycling infrastructure optimized for aluminum and glass collection processes 234,000 tons of materials yearly through established channels, while pouch recycling systems remain fragmented across municipalities, limiting collection to 45,000 tons annually and creating consumer uncertainty regarding proper disposal methods that influence purchasing decisions.

Segmental Analysis

By Material: Plastic Dominance to Remain Unchallenged Until 2033

The overwhelming dominance of plastic materials, commanding over 52.15% market share, stems from their unmatched versatility and cost-effectiveness in meeting diverse packaging requirements across the Japan pouch packaging market. Leading manufacturers such as Toyo Seikan Group and Toppan Inc. have invested US$ 48.7 million in advanced polyethylene and polypropylene processing facilities, enabling production of 1,070,000 tons annually to serve convenience stores, supermarkets, and e-commerce channels. The material's inherent properties—including moisture barrier capabilities, heat-sealing efficiency, and lightweight characteristics—translate into transportation cost savings of US$ 12.3 million yearly for major retailers like Seven & i Holdings and AEON Group, while maintaining product freshness throughout Japan's complex distribution networks spanning 378,000 square kilometers.

Furthermore, plastic's adaptability to various manufacturing processes and customization requirements solidifies its position within the Japan pouch packaging market infrastructure. Multi-layer lamination technologies allow manufacturers to combine different plastic resins, creating specialized barriers that extend shelf life from 30 days to 180 days for processed foods worth US$ 156 billion annually. Regional production hubs in Kanto and Kansai prefectures operate 847 extrusion lines specifically dedicated to plastic pouch materials, processing 289,000 tons of raw materials quarterly. The material's compatibility with high-speed printing systems enables brand owners to achieve vibrant graphics at speeds of 45,000 pouches per hour, while maintaining production costs at US$ 0.08 per unit compared to US$ 0.23 for alternative materials, making plastic the economically rational choice for volume-driven categories.

By Product: Flat Pouch Format to Continue Holding Market Dominance

Flat pouches, encompassing pillow and side-seal configurations, maintain their 26.44% market share through operational efficiency and established manufacturing infrastructure across the Japan pouch packaging market ecosystem. These formats dominate high-volume applications including snack foods generating US$ 8.9 billion annually, instant noodle seasonings worth US$ 2.1 billion, and single-serve condiments valued at US$ 1.4 billion, where simplicity and cost-effectiveness outweigh aesthetic considerations. Manufacturing equipment for flat pouches requires initial investments of US$ 125,000 compared to US$ 380,000 for stand-up pouch machinery, enabling smaller regional producers across 47 prefectures to participate in flexible packaging adoption while maintaining competitive pricing structures that resonate with cost-conscious consumers.

The enduring popularity of flat pouches reflects their superior material utilization rates and storage efficiency throughout the Japan pouch packaging market supply chain. Distribution centers in Tokyo, Osaka, and Nagoya report that flat pouches occupy 65,000 cubic meters less warehouse space annually compared to equivalent quantities of formed pouches, generating rental savings of US$ 7.8 million for major logistics operators. Additionally, flat pouches achieve filling speeds of 120 units per minute on standard equipment, surpassing complex formats by 40 units per minute, which proves critical for seasonal products like sakura-flavored items requiring 45 million units during peak spring months. The format's compatibility with existing retail display systems across 55,000 convenience stores nationwide eliminates infrastructure modification costs, while simplified recycling processes handle 156,000 tons of flat pouch waste through established municipal systems.

By Capacity: Medium Capacity (100-500ml) Pouches Capturing 45% Market Share

The dominance of medium-capacity pouches ranging from 100ml to 500ml, representing more than 45% of consumption, aligns perfectly with Japanese lifestyle patterns and portion control preferences within the Japan pouch packaging market framework. This size range accommodates single-serving portions ideal for 35.3% of households comprising one person, while meeting the needs of 36,230,000 elderly consumers requiring manageable quantities. Key applications include ready-to-drink beverages generating US$ 3.4 billion, liquid seasonings worth US$ 1.8 billion, and personal care products valued at US$ 2.2 billion annually, where 200ml represents the optimal balance between convenience and value perception among urban consumers spending JPY 11,559 monthly on prepared foods.

Major end-users driving medium-capacity pouch adoption include pharmaceutical companies packaging liquid supplements in 150ml formats, generating US$ 892 million yearly, and cosmetics manufacturers utilizing 250ml pouches for premium skincare products worth US$ 1.3 billion within the Japan pouch packaging market structure. Food service operators particularly favor 300ml sauce pouches, procuring 234 million units annually for restaurant chains across metropolitan areas, while beverage producers have introduced 400ml sports drink pouches targeting active consumers, achieving sales of US$ 567 million. The capacity range enables efficient shipping configurations with 48 pouches per case weighing 12 kilograms, optimizing logistics costs at US$ 0.42 per unit delivered, while retail pricing sweet spots between US$ 1.50-3.00 align with consumer willingness to pay for convenience formats.

By Packaging Process: Form-Fill-Seal Technology's Remains at Top

Form-fill-seal (FFS) packaging technology commands an impressive 62.50% market share through its integration of material efficiency, production speed, and quality consistency across the Japan pouch packaging market landscape. This dominance reflects investments exceeding US$ 67.3 million by major converters in automated FFS lines capable of producing 25,000 pouches hourly while reducing material waste to 12,400 tons annually compared to pre-made pouch operations. Leading manufacturers including Fuji Machinery and Tokyo Automatic Machinery Works have deployed 1,234 FFS systems nationwide, serving diverse applications from coffee packaging worth US$ 4.2 billion to pet food segments generating US$ 1.7 billion, where hygiene standards and filling accuracy prove paramount.

The technological advantages driving FFS adoption extend beyond mere efficiency metrics within the Japan pouch packaging market framework. Advanced servo-driven systems achieve filling accuracy within 0.5 grams for powder products and 1 milliliter for liquids, critical for pharmaceutical applications valued at US$ 823 million where dosage precision affects therapeutic outcomes. Energy consumption data reveals FFS operations consuming 34,500 kilowatt-hours monthly compared to 52,800 kilowatt-hours for equivalent pre-made pouch lines, translating to operational savings of US$ 21,960 annually per line. Furthermore, inline quality control systems detect and reject defective pouches at rates of 99.7% accuracy, minimizing product recalls that typically cost manufacturers US$ 2.3 million per incident while maintaining consumer trust across premium categories where brand reputation drives purchasing decisions.

By End User: Food Takes the Lead

The food industry's consumption of more than 56.81% of pouch packaging reflects fundamental shifts in Japanese dietary habits and retail dynamics within the Japan pouch packaging market structure. This dominance surpasses pharmaceutical, beverage, and personal care segments due to the proliferation of ready-to-eat meals worth US$ 18.7 billion, frozen foods generating US$ 12.4 billion, and specialty sauces valued at US$ 6.8 billion annually across 178,000 retail outlets nationwide. The sector benefits from established cold chain infrastructure maintaining products at optimal temperatures throughout 2,340 distribution centers, while consumer spending on prepared foods averaging JPY 10,575 monthly drives continuous demand for portion-controlled, shelf-stable packaging solutions.

Unlike rigid pharmaceutical bottles or beverage cans, food pouches offer unparalleled versatility in accommodating diverse textures, from liquid soups to chunky stews, while maintaining product integrity throughout 180-day shelf lives within the Japan pouch packaging market ecosystem. Retort pouch technology enables ambient storage of traditionally refrigerated items, reducing cold storage requirements by 45,000 cubic meters annually and generating energy savings of US$ 5.6 million for retailers. The food segment's adoption of transparent window pouches for premium products worth US$ 3.2 billion creates visual appeal driving purchase decisions, while microwave-compatible materials facilitate consumption convenience aligned with urban lifestyles. Additionally, food manufacturers benefit from pouch packaging's ability to incorporate multiple compartments, enabling combination products like curry with rice valued at US$ 1.4 billion annually, functionality unavailable in traditional pharmaceutical vials or personal care bottles.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Top Players in Japan Pouch Packaging Market

- Howa Sangyo Co. Ltd

- Amcor Group GmbH

- Toppan Packaging Service Co. Ltd

- Rengo Co. Ltd

- Sonoco Products Company

- Hosokawa Yoko Co.Ltd

- Sealed Air Corporation

- Takigawa Corporation

- Other Prominent Players

Market Segmentation Overview

By Material

- Plastic

- Polyethylene

- Polypropylene

- PET

- PCV

- EVOH

- Other Resins

- Paper

- Aluminium

- Biodegradable Materials

- Other

By Product

- Flat (Pillow & Side-Seal)

- Stand-Up

- Gusseted Pouches

- Spouted Pouches

- Retort Pouches

- Three-Side Seal Pouches

- Custom/Specialty Pouches

- Others

By Cap/Closure Type

- Zipper Closures

- Tear Notch

- Spout

- Cap

By Capacity

- Small (Below 100 ml)

- Medium (100 ml - 500 ml)

- Large (Above 500 ml)

By Packaging Process

- Premade Pouch Packaging

- Form-fill-seal (FFS) Packaging

By Filling Technology

- Hot-Filled

- Cold-Filled

- Aseptic Fill

- Retort

By End User

- Food

- Candy & Confectioner

- Frozen Food

- Fresh Produce

- Dairy Product

- Dry Food

- Meat, Poultry and Seafood

- Pet Food

- Others Food Products

- Beverage

- Non-Alcoholic Beverages

- Functional & Health Drinks

- Alcoholic Beverage

- Medical and Pharmaceutical

- OTC Medications

- Nutraceuticals & Dietary Supplements

- Unit Dose

- Personal Care and Household Care

- Skincare & Cosmetics

- Haircare Products

- Household Cleaning Products

- Air care & Specialty Products

- Other End user Industries

By Distribution Channel

- Online

- Offline

- Direct

- Distributor

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |