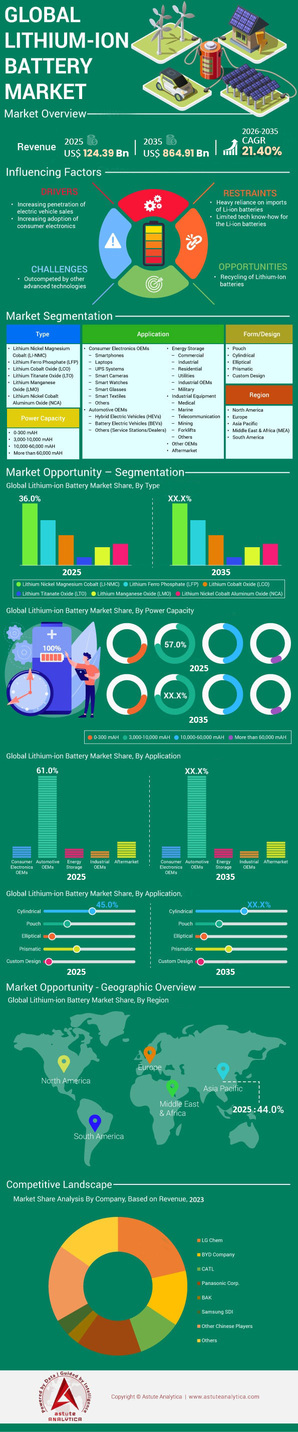

Market Scenario

Lithium-ion battery market generated a revenue of US$ 124.39 billion in 2025 and is projected to surpass the market valuation of US$ 864.91 billion by 2035 at a CAGR of 21.40% during the forecast period 2026–2035.

Key Findings

- By Type, Li-NMC batteries hold a major position in the lithium-ion battery market with a 36% revenue share.

- By power capacity, around the 3,000-10,000 mAh power capacity is leading the market with more than 57% of revenue .

- By application, automotive contribute more than 61% global lithium-ion battery consumption.

- Asia Pacific is projected to continue dominating the lithium-ion battery market with over 44% market share.

The lithium-ion battery market has entered a definitive phase of maturity and hyper-scaling as we navigate through 2025. The Li-ion chemistry has become the fundamental bedrock of the global energy transition. In line with this, the market dynamics have shifted from simple supply constraints to complex narratives involving massive overcapacity, plummeting prices, and fierce geopolitical competition. With global demand crossing historic thresholds, stakeholders are witnessing a reshaping of the energy landscape driven by cost-efficiencies and technological refinement.

What is Fueling the Explosive Demand for Lithium-Ion Batteries in 2025?

The demand for energy storage is surging, driven by a dual-engine growth model: the electrification of transport and the critical need for grid stabilization. Benchmark Mineral Intelligence forecasts that global demand for lithium-ion battery market will reach 1.59 TWh in 2025, a figure that seemed aspirational just five years ago. The primary catalyst remains the automotive sector. Global EV sales are projected to hit 20.7 million units in 2025, significantly up from the 17.8 million units recorded in 2024. Consequently, the sheer volume of cells required to power these fleets is immense, with the automotive segment alone demanding approximately 989 GWh to 1,248 GWh depending on policy scenarios.

However, a secondary, arguably more aggressive driver has emerged: stationary energy storage. The Battery Energy Storage System (BESS) sector is currently expanding faster than the electric vehicle market in percentage terms, recording a 51% year-on-year increase in 2025. Utilities are scrambling to balance intermittent solar and wind, prompting the US Energy Information Administration to forecast 18.2 GW of utility-scale storage additions to the US grid in 2025 alone. As battery pack prices for stationary storage dipped to USD 70/kWh in 2025, the economic case for replacing gas peaker plants with batteries became undeniable, further entrenching the Lithium-ion battery market in global infrastructure.

To Get more Insights, Request A Free Sample

Has Global Production Capacity Finally Outpaced Consumption?

Supply chain constraints, which plagued the industry post-pandemic, have been replaced by a massive manufacturing surplus. Total global Li-ion cell manufacturing capacity surpassed 3 TWh in 2024, effectively double the projected demand for 2025. This oversupply is strategic rather than accidental; manufacturers are engaging in a land grab for market share. China continues to lead this expansion, having announced a staggering pipeline capacity of 6,268 GWh by 2030. In contrast, Western nations are racing to catch up, with United States manufacturing capacity crossing the 200 GWh mark in 2024 due to incentives from the Inflation Reduction Act.

Utilization rates tell a nuanced story within the Lithium-ion battery market. While top-tier players like CATL run factories near optimal capacity, smaller players face utilization rates below 50%, leading to industry consolidation. The equipment market reflects this expansion fervor, valued at USD 21 billion in 2024. This massive build-out ensures that supply shortages are unlikely to return in the near term, shifting the market leverage firmly into the hands of buyers and OEMs.

Which Nations Hold the Reins of Global Battery Manufacturing in the Lithium-Ion Battery Market?

Geographically, the hierarchy of production remains heavily skewed toward East Asia, though regionalization is gaining momentum. China remains the undisputed leader, expected to control over 80% of global solid-state capacity and nearly 96% of sodium-ion capacity in 2025. The domestic Chinese market is projected to absorb 12.9 million EV units in 2025, creating a self-reinforcing loop of local production and consumption. Consequently, Chinese battery makers benefit from economies of scale that Western competitors struggle to match.

Europe serves as the second-largest production hub, driven by aggressive decarbonization mandates. Germany’s production capacity is estimated to reach 164 GWh by 2025, while Poland hosts LG Energy Solution’s massive facility, targeting 100 GWh. Meanwhile, the North American Lithium-ion battery market is rapidly evolving from an import-reliant model to a manufacturing base. With USD 223 billion allocated to US EV and battery manufacturing by 2024, the region is witnessing the fastest relative growth in capacity, aiming to decouple from Asian supply chains.

How Are Industry Titans Battling for Market Share?

Competition within the Lithium-ion battery market has intensified into a price war, with only the most vertically integrated players thriving. CATL dominates the landscape, having installed 339.3 GWh of capacity in 2024, effectively setting the global pricing floor. Their scale allows them to push costs down, forcing competitors to react. BYD, ranking second with 153.7 GWh, leverages its unique position as both a carmaker and a battery supplier to secure its market share. Together, these two entities control more than half of the global market.

Western-aligned manufacturers in the lithium-ion battery market like LG Energy Solution (96.3 GWh) and Panasonic (35.1 GWh) are focusing on high-performance nickel-based chemistries to differentiate themselves from the commoditized LFP market. However, the pressure is immense. The average LFP cell price dropped below USD 60/kWh in 2024, making it difficult for companies without upstream mining assets to compete on price. Mid-tier players like CALB (39.4 GWh) and SK On (39 GWh) are aggressively expanding but face the constant threat of margin compression in this cutthroat environment.

What Technological Breakthroughs Are Redefining Performance?

Innovation in 2025 is less about theoretical science and more about commercializing performance gains. Range anxiety is being systematically eliminated in the lithium-ion battery market. This is because the median range for Model Year 2024 EVs in the US reached 283 miles, with premium models like the Lucid Air pushing beyond 500 miles. These gains are largely due to improvements in energy density, which now hovers around 350 Wh/kg for commercial cells. Furthermore, charging speeds have improved drastically. The 2024 Chevy Silverado EV demonstrated peak charging of 315 kW, allowing drivers to recover hundreds of miles of range in under 30 minutes.

Solid-state batteries remain the "holy grail" for the Lithium-ion battery market, with projected densities of 500-700 Wh/kg. However, in 2025, semi-solid state batteries are the practical bridge, entering limited production for high-end vehicles. Simultaneously, process innovations like dry electrode coating are reducing manufacturing energy consumption and costs, proving that manufacturing efficiency is just as vital as chemical breakthroughs.

Could Emerging Alternatives Dethrone the Lithium-Ion Standard?

Despite the dominance of Lithium-ion, alternative chemistries are carving out specific niches. Sodium-ion batteries are the most prominent challenger for the low-cost segment. With China controlling 96% of this capacity, sodium-ion packs are targeting the sub-USD 50/kWh price point, making them ideal for micro-EVs and budget stationary storage where energy density is less critical.

Hydrogen fuel cells remain a topic of discussion but have largely lost the passenger vehicle battle to the Lithium-ion battery market. They retain potential in heavy-duty trucking, yet electric trucks already accounted for 3% of battery demand in 2024, encroaching on hydrogen’s last stronghold. Flow batteries offer promise for long-duration grid storage but lack the manufacturing scale to compete with cheap LFP batteries in 2025. For now, Lithium-ion remains the gold standard, with alternatives serving as complementary rather than replacement technologies.

What Trends Will Dictate the Market Trajectory Through 2026?

Looking ahead, the lithium-ion battery market is being shaped by circular economy mandates and raw material security. Recycling is no longer optional; with China’s scrap volume expected to reach 470,000 metric tons in 2025, the industry is turning "urban mining" into a profitable revenue stream. In the US, planned recycling capacity is set to increase by 76,000 tons over the next few years. Additionally, raw material prices have stabilized, with lithium carbonate forecast between USD 9,000 and USD 12,000 per ton in 2025, providing a predictable cost structure for OEMs.

Ultimately, the market is transitioning from a period of scarcity and high prices to an era of abundance and affordability. The surpluses in lithium (115,000 tons LCE) and nickel (198,000 tons) in 2025 are enabling mass adoption. As prices for battery packs settle near USD 100/kWh globally, the economic barrier to electrification has effectively dissolved, setting the stage for the Lithium-ion battery market to underpin the future global economy.

Segmental Analysis

By Type, High-Voltage Li-NMC Batteries Enjoying Premium Value Leadership

Li-NMC chemistries retain the highest 36% revenue share of in the lithium-ion battery market by pivoting towards "High-Voltage Mid-Nickel" architectures, which effectively balance cost and energy density against cheaper LFP alternatives. As of 2025, LG Energy Solution commenced mass production of these advanced mid-nickel NCM cells, delivering an energy density of 670 Wh/L while reducing costs by 8% compared to traditional high-nickel variants. This strategic shift allows OEMs to offer extended range in mid-to-high-tier vehicles without the volatility of high cobalt prices.

Furthermore, CATL’s 2024 interim reports highlighted that NCM chemistries accounted for 68% of their domestic EV battery and battery swapping consumption volume in specific high-performance segments, reinforcing that while LFP leads in volume, NMC dominates in value.

The widespread adoption of single-crystal cathode technology in 2025 has further solidified this dominance by enhancing thermal stability and lifespan, making Li-NMC the non-negotiable standard for the profitable long-range EV sector in North America and Europe.

By Capacity,3,000-10,000 mAh to Continue RulingLithium-Ion Battery Market

The 3,000-10,000 mAh segment dominance with over 57% market share is driven by the industrial standardization of the 21700 cylindrical cell (typically 4,800–5,300 mAh), which serves as the fundamental building block for Western EV battery packs. In July 2025, Panasonic Energy began mass production of these 2170 cells at its new Kansas facility, targeting an annual capacity of 32 GWh specifically to supply Tesla’s high-volume models. This specific capacity range is critical in the lithium-ion battery market because it offers the optimal balance of thermal management and packaging efficiency, unlike larger 4680 cells (approx. 26,000 mAh) which faced slower initial yield rates.

Additionally, Samsung SDI secured the "2025 InterBattery Award" for its new 50Amp high-power cylindrical cell within this capacity bracket, designed to meet the dual demand from electric mobility and heavy-duty professional power tools. This cross-sector versatility ensures the 3,000-10,000 mAh range remains the highest revenue generator, aggregating billions of units annually.

By Application, Automotive Sector is Monopolizing Battery Supply Chains

Automotive applications command over 61% of global consumption in the lithium-ion battery market because the sector has successfully transitioned battery manufacturing into a "Terawatt-hour (TWh) era," dwarfing all other applications combined. According to the IEA Global electric vehicle market Outlook 2025, electric vehicles accounted for over 85% of total global lithium-ion battery demand, driven by a fleet-wide shift toward larger pack sizes (averaging 60–80 kWh).

CATL’s 2024 Annual Report confirms this financial hegemony, revealing that EV battery systems generated approximately 70% of their total revenue (CNY 253 billion), compared to just 16% from energy storage systems.

The dominance is further entrenched by 2025 supply chain data showing major players like BYD and SK On dedicating over 90% of their new Gigafactory capacities exclusively to automotive contracts. This volume-value nexus makes the automotive sector the undisputed primary driver of the entire lithium-ion value chain, relegating consumer electronics to a secondary tier.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific: Chinese Manufacturing Hegemony and Regional Integration

Asia Pacific’s dominance in the global lithium-ion battery market is anchored by China’s unprecedented industrial scale, which in 2025 accounted for approximately 69% of global EV battery installations. This leadership is not merely about volume but complete value chain control.

China exports over 81 GWh of batteries annually while simultaneously deploying 12.9 million EVs domestically (+17% YoY). Companies like CATL (38.1% global share) and BYD (16.9% global share) have effectively monopolized the LFP battery market, offering a cost structure that Western competitors cannot match. Beyond China, the region is solidifying its position through strategic integration. Indonesia has leveraged its nickel reserves to attract billions in downstream investment, launching a massive 60,000-ton integrated battery project in 2025 with partners like CATL.

Similarly, India is emerging as a critical growth engine, with EV sales jumping 16% to reach 2.27 million units in 2025, driven by local heavyweights like Tata Motors and widespread adoption of electric two-wheelers. This multi-tiered demand—from Chinese megacities to Indian commercial fleets—creates a self-sustaining ecosystem that keeps Asia Pacific as the undisputed global battery hub.

Europe: Regulatory Mandates Fueling Localization and Technology Shifts

Europe maintains its position as the second-largest lithium-ion battery market by enforcing the world’s most stringent decarbonization mandates, which have successfully decoupled battery demand from purely organic market forces. In H1 2025, European EV registrations surged by 34%, pushing battery demand for passenger vehicles to constitute 85% of the region's total consumption. This growth is underpinned by the EU Battery Regulation, which became fully operational in 2025, mandating carbon footprint declarations that favor localized production.

Consequently, the region is seeing a rapid ramp-up of "Gigafactories" to reduce reliance on imports, although Asian firms still play a major role. German automakers like Volkswagen Group are leading this charge, securing direct supply chains to meet emissions targets that tightened significantly this year.

Despite challenges such as the Northvolt bankruptcy, the structural demand remains robust because effectively 100% of new vehicle fleets must transition to electric drivetrains to avoid crippling EU penalties, guaranteeing a captive market for high-performance NMC and emerging LFP chemistries.

North America: Federal Policy Driving Massive Industrial Capacity Expansion

North America’s lithium-ion battery market position is defined by a massive, policy-driven industrial build-out rather than just immediate sales volume. By Q1 2025, the region had 123 operating battery manufacturing projects with a capacity of nearly 202 GWh, a direct result of the Inflation Reduction Act’s (IRA) local production incentives.

While consumer EV adoption faced headwinds—with sales dipping slightly to 1.8 million units amid policy uncertainty—the manufacturing sector boomed, attracting record investments from joint ventures like Ford-SK On and GM-Samsung SDI. This region is uniquely characterizing itself through the rapid growth of the Battery Energy Storage System (BESS) sector, which saw its share of battery demand jump to 26% in 2025, outpacing global averages. This indicates a lithium-ion battery market that is diversifying beyond just automotive applications to grid-scale resilience.

The dominance here is future-proofed; the sheer volume of capital committed to domestic cell production ensures that North America will remain a top-tier player, converting federal dollars into hard industrial capacity that insulates it from global supply chain volatility.

Top 5 Strategic Developments in the Lithium-Ion Battery Market

1. Panasonic Energy Commences Operations at Kansas Gigafactory

In July 2025, Panasonic Energy officially opened its new cylindrical lithium-ion battery manufacturing facility in De Soto, Kansas. The plant began mass production of 2170 cells, aiming for an annual capacity of 32 GWh to support the North American electric vehicle supply chain.

2. CATL Initiates Mass Production of Sodium-Ion Batteries

Contemporary Amperex Technology Co., Limited (CATL) announced in December 2025 the start of large-scale mass production for its sodium-ion batteries. This milestone followed the April launch of the "Freevoy" battery, with the new sodium-ion cells targeting both EV and energy storage sectors to reduce reliance on lithium.

3. Samsung SDI Starts 46-Series Cylindrical Cell Production

Samsung SDI confirmed the start of mass production for its 46-series cylindrical batteries (46mm diameter) in May 2025. The company showcased these high-density cells, designed for next-generation EVs, earlier in the year at the InterBattery 2025 exhibition in Seoul.

4. BYD Secures World’s Largest Energy Storage Contract

On February 14, 2025, BYD Energy Storage signed a historic contract with the Saudi Electricity Company to supply 12.5 GWh of battery energy storage systems (BESS). This agreement represents the largest single project in the sector's history, cementing BYD's dominance in grid-scale storage.

5. LG Energy Solution Unveils Diversified 46-Series Lineup

During InterBattery 2025 in March, LG Energy Solution officially unveiled its comprehensive lineup of 46-series cylindrical cells (4680, 4695, and 46120). The company announced that mass production for global automotive clients would accelerate throughout the latter half of 2025 to meet Tesla and other OEM demands.

Top Players in Global Lithium-ion Battery Market

- BYD Company

- LG Chem

- Panasonic Corporation

- Samsung SDI

- BAK Group

- Hitachi Corporation

- Johnson Controls

- Toshiba Corporation

- Raja Groups

- Tata Chemicals

- TDK Electronics AG

- Sony Corporation

- Murata Manufacturing Co., Ltd.

- Amperex Technology Limited

- LITEC Co., Ltd.

- GS Yuasa International Ltd.

- Automotive Energy Supply Corporation

- Other Major Players

Market Segmentation Overview:

By Type:

- Lithium Nickel Magnesium Cobalt (LI-NMC)

- Lithium Ferro Phosphate (LFP)

- Lithium Cobalt Oxide (LCO)

- Lithium Titanate Oxide (LTO)

- Lithium Manganese Oxide (LMO)

- Lithium Nickel Cobalt Aluminum Oxide (NCA)

By Power Capacity:

- 0-300 mAH

- 3,000-10,000 mAH

- 10,000-60,000 mAH

- More than 60,000 mAH

By Application:

- Consumer Electronics OEMs

- Smartphones

- Laptops

- UPS Systems

- Smart Cameras

- Smart Watches

- Smart Glasses

- Smart Textiles

- Others

- Automotive OEMs

- Hybrid Electric Vehicles (HEVs)

- Battery Electric Vehicles (BEVs)

- Others (Service Stations/Dealers)

- Energy Storage

- Commercial

- Industrial

- Residential

- Utilities

- Industrial OEMs

- Military

- Industrial Equipment

- Medical

- Marine

- Telecommunication

- Mining

- Forklifts

- Others

- Other OEMs

- Aftermarket

By Form/Design:

- Pouch

- Cylindrical

- Elliptical

- Prismatic

- Custom Design

By Region:

- North America

- The U.S.

- Canada

- Mexico

- Europe

- The UK

- Germany

- France

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia & New Zealand

- Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2025 | US$ 124.39 Bn |

| Expected Revenue in 2035 | US$ 864.91 Bn |

| Historic Data | 2020-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Unit | Value (USD Bn) |

| CAGR | 21.4% |

| Segments covered | By Type, By Power Capacity, By Application, By Form/Design, By Region |

| Key Companies | BYD Company, LG Chem, Panasonic Corporation, Samsung SDI, BAK Group, Hitachi Corporation, Johnson Controls, Toshiba Corporation, Raja Groups, Tata Chemicals, TDK Electronics AG, Sony Corporation, Murata Manufacturing Co., Ltd., Amperex Technology Limited, LITEC Co., Ltd., GS Yuasa International Ltd., Automotive Energy Supply Corporation, Other Major Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

FREQUENTLY ASKED QUESTIONS

Global lithium-ion battery market generated a revenue of US$ 124.39 billion in 2025 and is projected to surpass the market valuation of US$ 864.91 billion by 2035 at a CAGR of 21.40% during the forecast period 2026–2035.

Li-NMC (Lithium Nickel Manganese Cobalt) batteries hold the dominant position with a 36% revenue share. While LFP leads in volume due to lower costs, Li-NMC retains value leadership through high-voltage mid-nickel architectures favored by North American and European automakers for long-range EVs.

The market has shifted to a massive manufacturing surplus, with global cell capacity surpassing 3 TWh in 2024—double the demand. This overcapacity has driven battery pack prices down to approximately USD 100/kWh, shifting leverage significantly toward OEMs and buyers.

While automotive accounts for 61% of consumption in the lithium-ion battery market, the Battery Energy Storage System (BESS) sector is expanding fastest, recording a 51% year-on-year increase in 2025. Utilities are rapidly adopting batteries to stabilize grids, fueled by pack prices dipping to USD 70/kWh for stationary storage.

Asia Pacific dominates with over 44% market share, anchored by China, which accounts for approximately 69% of global EV battery installations. China creates a self-reinforcing loop of local production and consumption that Western competitors are still racing to match via policy incentives.

The industry is standardizing 3,000-10,000 mAh cylindrical cells (specifically the 21700 and 46-series), which now capture 57% of revenue. Additionally, semi-solid state batteries are entering limited production for premium vehicles, acting as a commercial bridge to future solid-state technologies.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |