Market Scenario

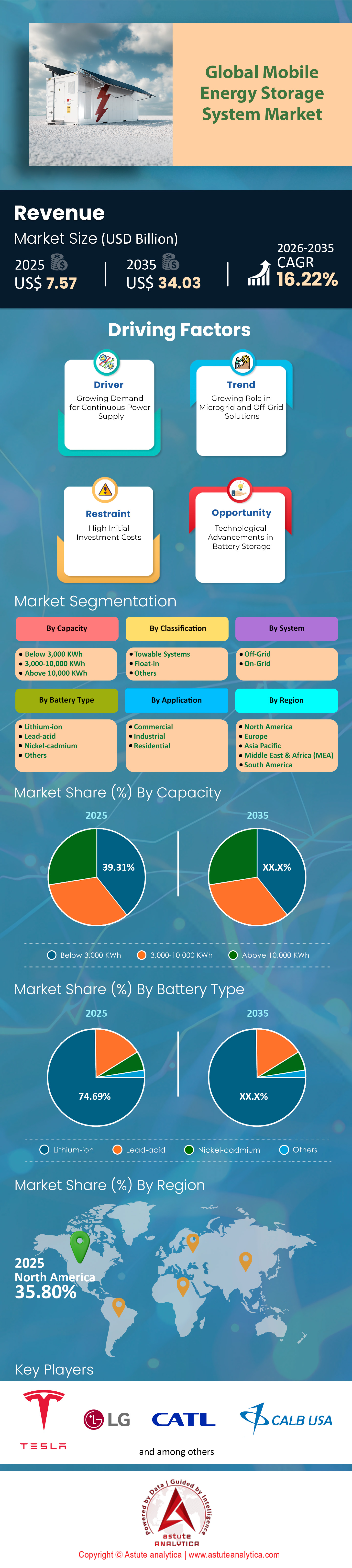

Mobile energy storage system market was valued at US$ 7.57 billion in 2025 and is projected to hit the market valuation of US$ 34.03 billion by 2035 at a CAGR of 16.22% during the forecast period 2026–2035.

Key Findings

- Based on capacity, mobile energy storage system market is led by the below 3,000 KWh segment with over 39.31% market share.

- Based on classification, mobile energy storage system market is led by towable system segment with over 55.61% market share.

- Based on battery type, lithium-ion batteries accounted for the highest share 74.69%.

- Based on system, Off-Grid mobile energy storage systems holds strong prominence in the market with over 61.50% market share.

- North America is set to continue leading the market by capturing more than 35.80% market share.

What is A Mobile Energy Storage System and Why Is It Critical Now?

A Mobile Energy Storage System (MESS) is essentially "grid-infrastructure-on-wheels," designed to provide high-capacity battery power that can be rapidly deployed to locations where the electrical grid is either non-existent, insufficient, or compromised. Unlike stationary battery energy storage systems (BESS) which are permanently anchored, MESS units are mounted on trailers or skids, allowing for immediate transport via truck or forklift. These systems bridge the gap between diesel generators and permanent green infrastructure.

The demand for these systems in the mobile energy storage system market is exploding globally due to a convergence of grid instability and aggressive decarbonization mandates. As of 2024, the US grid reached a total battery capacity of 26 GW, yet stability issues persist. Developers added 10.4 GW in 2024 alone and planned another 19.6 GW for 2025, but static storage cannot move to where disasters strike. Consequently, mobile solutions are filling the void. In May 2024, the US Department of Energy (DOE) awarded USD 27 million specifically for clean energy resilience, validating the sector's importance. Cities like Houston secured USD 2 million from this pool for facility retrofits, proving that municipal governments are now prioritizing mobile resilience to combat extreme weather events.

To Get more Insights, Request A Free Sample

Who Are The Primary End-Users Driving Consumption?

The consumption profile for mobile energy storage system market is shifting from niche pilots to critical infrastructure support. The most prominent end-users include utility companies, the events industry, construction firms, and defense agencies. Utilities are utilizing these units for peak shaving and substation maintenance; for instance, Nomad Transportable Power Systems projected USD 150,000 in seasonal savings for a DSO Electric Cooperative during a single pilot.

Simultaneously, the entertainment sector is abandoning diesel. A single mobile unit at a 2024 concert series prevented 2 metric tons of CO2 emissions, while hybrid deployments have demonstrated a 70% reduction in fuel usage. Defense is also a major consumer; the US National Guard awarded contracts in June 2024 for microgrids that can be set up in under one hour, requiring rugged units that accept solar input and operate in hostile environments.

Which Companies Are Currently Dominating The Competitive Landscape?

Four key players have established dominance by offering diverse technical specifications and securing massive capital for expansion:

- Aggreko: A global leader in temporary power, Aggreko committed USD 200 million in 2024 to expand its BESS fleet. Their technical prowess is evident in their "500 kW" mobile unit, which boasts a usable capacity of 221 kWh and achieves a full charge in just 0.5 hours, setting the standard for rapid turnaround.

- Nomad Transportable Power Systems: Nomad dominates the high-capacity segment. Their flagship Traveler unit offers a massive 2.0 MWh capacity with 1 MW of power output. They have proven financial viability, securing USD 7.21 million in debt financing in early 2024 to scale operations.

- Northvolt: Representing European innovation, Northvolt’s Voltpack Mobile units utilize battery cells that achieved a lifespan equivalent to 1.5 million kilometers in heavy-duty applications. Their systems operate at high voltages (up to 797 V), making them ideal for industrial use.

- Hitachi Energy: a key player in heavy industry electrification, Hitachi commenced formal sales of mobile systems in Europe in 2024. Their technology is critical for construction, capable of charging a 13-ton electric excavator 2 times on a single charge cycle, directly addressing the needs of electrified job sites.

Which Nations Control The Production and Innovation Hubs?

Production dominance in the global mobile energy storage system market is split between cost-leaders and innovation-leaders. China currently rules the manufacturing landscape due to sheer scale and cost efficiency. By late 2024, turnkey energy storage system bids in China had plummeted to USD 66 per kWh, significantly lower than the global average battery pack price of USD 115 per kWh. This price advantage allows Chinese manufacturers to flood international markets with affordable hardware.

Conversely, the United States is leading in high-tech innovation and resilience application, fueled by federal subsidies. The DOE announced USD 125 million in September 2024 for next-generation battery research hubs. Meanwhile, European nations are driving production through strict environmental mandates, with companies like Alfen (Netherlands) generating €123.7 million from energy storage systems in H1 2024 alone.

What Are the Key Applications Fueling Market Expansion?

The most explosive application area of the mobile energy storage system market is Mobile EV Charging. With 85 million EVs projected to be on the road by the end of 2025, fixed infrastructure is lagging. Although Tesla’s network is growing to 29,083 ports, gaps remain. L-Charge has capitalized on this by deploying mobile units with 2,000 kW output that can charge a vehicle in 10 minutes.

Disaster Relief is the second critical pillar. Following the allocation of resilience grants, NYC Sanitation committed to holding 200 mobile battery collection events to manage waste and test logistics, targeting 35,000 pounds of material. Additionally, Construction and Mining applications are growing as operators seek to replace noisy generators; Atlas Copco’s units now operate with 0 noise emissions, a mandatory requirement for many urban construction zones in 2025.

What Technological Developments Are Defining The Future?

Future developments in the mobile energy storage system market are centered on energy density and extreme weather resilience. The market is moving toward higher capacity in smaller footprints. For example, Aggreko’s 250 kW unit packs 518 kWh into a trailer weighing 11 tons, but newer designs are shaving weight while maintaining power. Thermal management has also seen breakthroughs; modern units are now certified to operate in temperatures ranging from -20 degrees Celsius to 50 degrees Celsius, ensuring reliability from the Arctic to the desert.

Another key development across the mobile energy storage system market is the integration of high-speed active charging. The ability of the Aggreko 500 kW unit to charge in 30 minutes fundamentally changes the "rental" economics, allowing a single unit to serve multiple sites in one day.

What Recent Trends Are Shaping Market Trajectory?

A major trend is the shift toward the Circular Economy. The industry is actively preparing for end-of-life management to avoid environmental backlash. AMP received USD 6.43 million in 2024 to automate battery sorting, ensuring that mobile units can be recycled efficiently.

Furthermore, the "Energy-as-a-Service" (EaaS) model is gaining traction. Instead of purchasing expensive assets, clients are renting capacity. Nomad’s savings projection for DSO Electric Cooperative (USD 150,000) was based on this seasonal deployment model, which reduces CapEx risk for utilities.

What Challenges Are Currently Hindering Market Growth?

Despite the optimism, financial instability remains a severe threat to the mobile energy storage system market growth. The high capital intensity of building mobile fleets can be fatal for mismanaged firms. The bankruptcy of Moxion Power in 2024 serves as a stark warning; the company reported liabilities between USD 100 million and USD 500 million while holding only USD 201,980 in cash. The collapse resulted in 247 layoffs and shook investor confidence.

Additionally, supply chain volatility and grid interconnection delays continue to plague the sector. While battery prices have dropped, the logistical cost of deploying heavy units (often exceeding 10,000 pounds) requires specialized transport, limiting rapid deployment in infrastructure-poor regions. However, as the grid becomes more volatile, the market views these challenges as growing pains rather than existential threats.

Segmental Analysis

Below 3,000 KWh System Hold Market Prominence Due to Optimized Capacity For Versatile Urban Construction and Event Power Needs

Based on capacity, mobile energy storage system market is led by the below 3,000 KWh segment with over 39.31% market share. The industry clearly favors this specific capacity range because it strikes the perfect equilibrium between providing sufficient energy density and maintaining logistical agility. Manufacturers aggressively target this sweet spot, evidenced by Moxion Power engineering the MP-75/600 unit to deliver exactly 600 kWh of energy. Nomad Power followed a similar trajectory with the Voyager Hawk offering 664 kWh, while their Voyager Falcon pushes the segment boundary with 1.3 MWh. Alfen strategically modularized their Mobile X portfolio to offer scalable 360 kWh, 540 kWh, and 720 kWh options. These specific capacities allow operators to charge between 6 to 12 electric vehicles simultaneously, a critical metric for modern fleet management.

The dominance of this segment within the mobile energy storage system market is further reinforced by the ability to fit high-capacity power into restricted urban footprints. Greener Power Solutions upgraded their mobile fleet units to 422 kWh specifically to handle intensive event loads without requiring multiple units. Nomad Power addressed lighter commercial needs with the Pathfinder unit offering 150 kWh. To satisfy this specific capacity appetite, Moxion targets an annual production capacity of 700 MWh. Greener Power Solutions subsequently expanded their active fleet to over 60 mobile batteries to meet regional demand. Alfen engineered these capacities to fit precisely within standard 10-foot containers. Furthermore, Moxion designed their 600 kWh systems to physically fit through standard double doors.

Agile Towable Units Secure Global Dominance Through Logistical Superiority

Based on classification, mobile energy storage system market is led by the below towable system segment with over 55.61% market share. This dominance is fundamentally driven by the "hitch-and-go" capability that eliminates the need for specialized heavy-haulage logistics. Unlike float-in or containerized systems that require cranes and flatbed semis, towable units like the Nomad Pathfinder are engineered to weigh under 10,000 pounds, allowing them to be transported by standard heavy-duty pickup trucks. The mobile energy storage system market favors this form factor because it democratizes access to power; any site manager with a standard vehicle can relocate the asset immediately as project needs shift. Moxion Power capitalized on this by designing the MP-75/600 to offer utility-grade power in a trailer footprint that fits through standard double doors, making it indispensable for urban construction zones where space is at a premium.

The global demand for towable systems is further accelerated by the rapid operational tempo of the events and disaster relief sectors. Atlas Copco’s ZenergiZe units, which are 70% lighter than traditional generators, allow for instant deployment in noise-sensitive areas without complex site preparation. Generac Mobile reinforced this trend in 2025 with their SBE series, specifically targeting the rental market which prioritizes assets that integrate seamlessly into existing vehicle fleets. In disaster zones, the ability to tow power directly to a damaged facility without waiting for heavy machinery is critical. Consequently, the mobile energy storage system market continues to see its highest growth in this segment, as operators prioritize speed, flexibility, and lower transportation costs over static capacity.

Lithium-Ion Batteries Enjoy Lion’s Share Thanks to Superior Chemistry and Safety Profiles Accelerating Technology Adoption

Based on battery type, lithium-ion batteries dominates the mobile energy storage system market. The segment accounted for the highest share of 74.69% and is also projected to grow at the highest CAGR of 16.75%. This segment's commanding position is driven by rapid maturation in cell chemistry that now allows for safe, high-density energy storage in mobile form factors. The mobile energy storage system market has pivoted toward Lithium Iron Phosphate (LFP) chemistry to mitigate thermal runaway risks in mobile applications. Moxion Power exclusively utilizes LFP chemistry for its superior thermal stability. Alfen also adopted LFP technology for its Mobile X line. Kyon Energy notes a technological shift from 314 Ah cells to larger 500 Ah battery cells in 2025. Nomad Power utilizes nickel manganese cobalt racks supplied by Kore Power.

Beyond safety, the performance characteristics of modern lithium-ion cells are displacing legacy technologies. LFP batteries offer thousands of cycles, far exceeding lead-acid alternatives. Moxion units operate silently, a critical advantage for film sets. The energy density of these modern packs in the mobile energy storage system market allows 600 kWh storage in compact trailer footprints. Alfen units support both 50 Hz and 60 Hz frequencies. Solid-state battery technology is emerging for pilot testing in 2025. Moxion units provide consistent power for heavy construction loads like concrete grinding.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Off-Grid Systems Holds Strong Prominence In The Market

Based on system, Off-Grid mobile energy storage systems holds strong prominence in the market with over 61.50% market share. This segment is capturing the majority of market value because regulatory pressure and sustainability goals are forcing industries to abandon diesel generators. Greener Power Solutions reported saving 1.5 million liters of diesel through their off-grid fleet. Sunbelt Rentals validated this demand by placing an order for 600 Moxion off-grid units. The mobile energy storage system market is witnessing massive capital inflows here, with Greener Power Solutions raising USD 45 million. Moxion also secured a USD 15 million grant to expand manufacturing.

The practical necessity of off-grid power for disaster recovery and remote operations cements this dominance in the mobile energy storage system market. Moxion units were deployed in San Francisco to provide emergency relief during power outages. Greener Power Solutions grew their total fleet capacity to 20 MWh. Nomad Power units demonstrated autonomous power capabilities at the Distributech conference. Construction crews utilized Moxion batteries to run heavy equipment like concrete grinders. Nomad units are actively supporting microgrids for remote communities. Alfen units were deployed for Project Pollix.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America Secures Top Market Position Through Federal Resilience Grants And Defense

North America currently commands a dominant 35.80% market share of the Mobile energy storage system market, a position solidified by the United States' aggressive use of federal funds to combat climate instability. In 2025, the market narrative here is defined by "Resilience." The US Department of Energy’s allocation of USD 27 million for local government resilience directly subsidizes the acquisition of mobile fleets. Specific municipal investments, such as Houston’s USD 2 million for facility retrofits and Chicago’s USD 2.2 million for electrification, demonstrate that city planners are prioritizing mobile storage to survive increasingly frequent outages.

The defense sector further anchors this lead in the Mobile energy storage system market, evidenced by Nomad Transportable Power Systems securing a 2024 contract to deploy microgrids for the National Guard that require less than one hour to set up. These strategic procurements ensure North America remains the primary revenue generator globally.

Asia Pacific Dominates Manufacturing Scale And Industrial Heavy Equipment Electrification Sectors

Asia Pacific, led by China and Japan, controls the supply chain and heavy industrial applications in the mobile energy storage system market. China’s manufacturing scale has successfully driven turnkey energy storage bids down to a rock-bottom USD 66 per kWh in late 2024. This aggressive pricing strategy allows Chinese OEMs to undercut global competitors, maintaining high export volumes.

Japan compliments this volume with high-tech specialization in construction. Hitachi Construction Machinery’s 2024 deployment of mobile chargers capable of powering 13-ton electric excavators two times per daily cycle highlights the region's focus on operational efficiency. Consequently, the region is indispensable, serving as both the global factory floor and the testing ground for heavy-duty mobile electrification.

Europe Accelerates Adoption Via Stringent Carbon Mandates And Major Fleet Investments

Europe follows closely, holding strong dominance in the "Events" and "Rental" segments of the mobile energy storage system market due to strict regulatory frameworks that penalize diesel emissions. The region’s market is characterized by massive corporate fleet expansion rather than just government pilots. Aggreko’s commitment of USD 200 million to expand its battery fleet underscores the commercial viability of temporary green power across the UK and EU. Financially, European pure-play storage firms are performing robustly; Alfen generated EUR 123.7 million from energy storage systems in H1 2024 alone.

Innovation in Sweden also supports this growth, with Northvolt’s mobile cells achieving a verified lifespan equivalent to 1.5 million kilometers. Such longevity appeals to European rental operators focused on maximizing asset ROI over long periods.

Recent Developments in Mobile Energy Storage System Market

JEM containerised BESS (India): Jupiter Electric Mobility launched 10 ft and 20 ft containerised BESS, fully indigenously built, with modular capacities from 241 kWh to 3 MWh for grid-scale and C&I use. The systems are designed for rapid deployment and round-the-clock clean power, supporting India’s Net Zero 2070 vision.

Volvo Group PU2000 BESS: Volvo Group introduced the PU2000, a smart, safe, energy-cost-optimized BESS platform aimed at flexible deployments in commercial and industrial applications. The system targets scalable, transportable storage integrated with Volvo’s broader energy ecosystem.

Samsung SDI containerized utility BESS: Samsung SDI showcased a new NCA-based containerized BESS up to 6.14 MWh, plus an LFP-based SBB 2.0 system using dual 20 ft containers for utility projects. Both emphasize enhanced safety via “Enhanced Direct Injection” fire suppression and are slated for U.S. manufacturing from 2026.

Fluence Smartstack 7.5 MWh platform: Fluence Energy launched Smartstack, a highly modular AC-based BESS with up to 7.5 MWh per unit, optimized for logistics and maintenance. Its architecture splits capacity into smaller, more easily transportable units to meet road weight limits, especially in Europe.

BYD MC Cube-T next-gen system: BYD released MC Cube-T, a next-generation containerized energy storage system with 6.432 MWh capacity, improving system energy by up to 35.8 percent over its predecessor. The compact design reduces footprint by up to 24.7 percent, enabling denser, mobile multi-MWh deployments.

Top Players in Mobile Energy Storage System Market

- Tesla

- LG Electronics Inc.

- CALB USA Inc.

- NextGen NRG

- Caterpillar Inc.

- Hamedata Technology

- Roypow Technology Co. Ltd.

- Aggreko

- Power Edison

- Delta Electronics

- Nomad Transportable Power System

- Generac Power Systems Inc.

- Alfen

- Other Prominent Player

Market Segmentation Overview:

By Capacity

- Below 3,000 KWh

- 3,000-10,000 KWh

- Above 10,000 KWh

By Classification

- Towable Systems

- Float-in

- Others

By Battery Type

- Lithium-ion

- Lead-acid

- Nickel-cadmium

- Others

By System

- Off-Grid

- On-Grid

By Application

- Commercial

- Industrial

- Residential

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

FREQUENTLY ASKED QUESTIONS

Mobile energy storage system market was valued at US$ 7.57 billion in 2025 and is projected to hit the market valuation of US$ 34.03 billion by 2035 at a CAGR of 16.22% during the forecast period 2026–2035.

A MESS is grid-infrastructure-on-wheels designed for rapid deployment to areas with compromised or non-existent power. Demand is exploding because static grid storage cannot address localized disasters; MESS bridges the gap between diesel generators and permanent green infrastructure, supported by significant DOE resilience grants.

The primary end-users are utility companies using units for substation maintenance, the events industry seeking to replace diesel generators to reduce CO2, construction firms powering electric machinery, and defense agencies like the US National Guard requiring rapid-deploy microgrids.

Key players include Aggreko, which committed USD 200 million to fleet expansion; Nomad Transportable Power Systems, known for its 2.0 MWh Traveler unit; Northvolt, offering high-voltage systems for industrial use; and Hitachi Energy, which specializes in heavy equipment electrification.

This segment holds over 39.31% market share because it represents the logistical sweet spot. Capacities between 360 kWh and 664 kWh offer sufficient power for EV fleets and events while remaining compact enough to bypass heavy-haulage regulations and fit through standard double doors.

Lithium-ion batteries account for 74.69% of the market, with a strong shift toward Lithium Iron Phosphate (LFP) chemistry. This dominance is driven by LFP’s superior safety profile, thermal stability, and extended cycle life compared to lead-acid alternatives, making it safer for mobile transport.

North America leads with a 35.80% market share, driven by federal resilience grants and defense spending. Conversely, Asia Pacific controls the manufacturing supply chain, with Chinese producers driving turnkey bid prices down to USD 66 per kWh, significantly undercutting global competitors.

The sector faces high capital intensity and financial instability, highlighted by the 2024 bankruptcy of Moxion Power. Additional hurdles include supply chain volatility and the logistical difficulties of transporting units that often exceed 10,000 pounds to remote locations without specialized infrastructure.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |