North America Forklift Battery Charger Market: By Forklift Type (Electric Forklift, Hybrid Forklift, Diesel Forklift, Others); Battery Type (Sealed Lead Acid (SLA) Battery, Lithium Ion Battery, Nickel-Cadmium Battery Chargers, Others); Charger Type (Standard Chargers, Fast Chargers, On-board Chargers, Smart Chargers); Voltage Type (24V Chargers, 36V Chargers, 48V Chargers, 72V & 80V Chargers); Forklift Class (Class 1, Class 2, Class 3); Output Charging Current Rating (50A-150A, 151A-250A, Above 251A, Below 50A); Power Rating (UP TO 5KW, 5-10 KW, 11-15 KW, >15KW); Industry (Warehouses, Manufacturing, Construction, Retail and Wholesale Stores, Others); Sales Channel (OEMs and Aftermarket); Country—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 20-May-2025 | | Report ID: AA05251320

Market Scenario

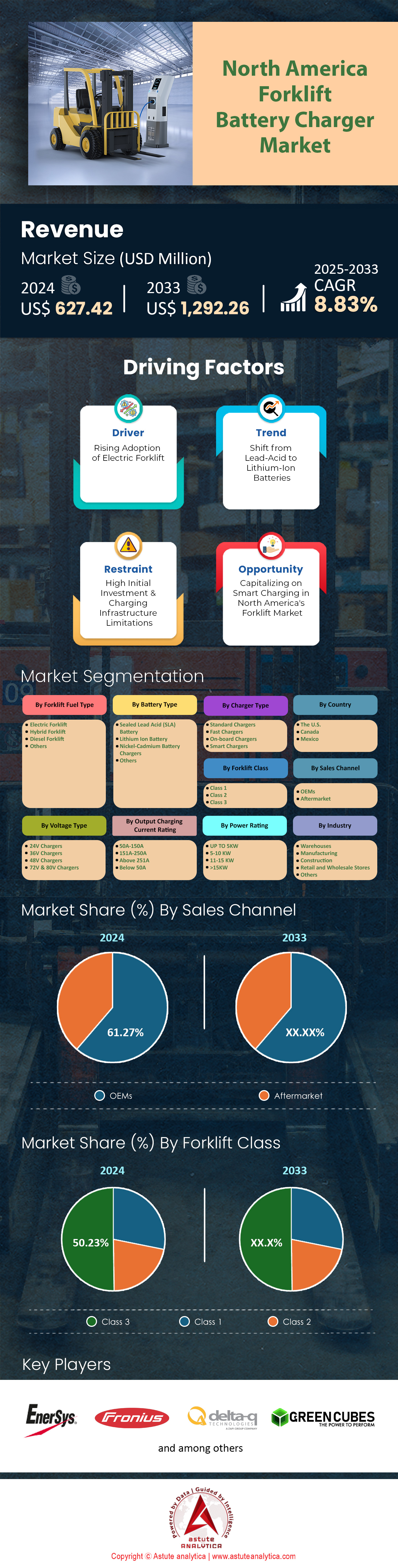

North America forklift battery charger market was valued at US$ 627.42 million in 2024 and is projected to hit the market valuation of US$ 1,292.26 million by 2033 at a CAGR of 8.83% during the forecast period 2025–2033.

Surging electrification of material-handling fleets is rewriting power infrastructure inside North American warehouses: the Industrial Truck Association recorded 291,000 forklift sales in the United States during 2023, of which roughly 206,000 were electric, setting a record for charger pull-through in 2024. Each Class I lithium-ion truck consumes about 14 kWh during one eight-hour shift, so the installed base now demands more than 2.8 GWh of daily charging energy across the region. High-frequency chargers rated at 200–300 A are becoming the dominant replacement for legacy ferroresonant units because they recover 1.2–1.5 kWh per hour of opportunity charging, directly enabling two-shift operations without battery swaps. Regulatory pressure is equally decisive: California’s Advanced Clean Fleets rule bans new internal-combustion forklifts under 12,000 lb from 2026, instantly driving charger purchases among 36,000 facilities that still rely on propane trucks.

On the supply side, seven manufacturers in the North America forklift battery charger market now run dedicated charger assembly lines in North America, up from four in 2021. EnerSys expanded its Dallas plant in February 2024, lifting annual output to 120,000 modular 24–80 V chargers, while Delta-Q Technologies added a second SMT line in Vancouver capable of producing 65,000 1.5 kW boards a year. South Korea’s Samsung SDI and Germany’s Fronius both opened joint ventures in Monterrey, Mexico, primarily to serve USMCA-compliant lithium charger demand in the Midwest. Imports remain critical for niche chemistries: customs data show 44,600 high-voltage silicon-carbide charger stacks entered through the Port of Los Angeles in 2023, destined for fast-charge pilot projects at 18 US retailers. Meanwhile, UL 2580/UL 1973 recertification cycles are shortening from 18 to 12 months, forcing producers to embed software-defined charging profiles that can be updated over-the-air—an emerging differentiator noted by OEMs such as Crown Equipment and Raymond.

Five states dominate real-world consumption. California operates an estimated 38,000 electric Class I–III trucks, paired with roughly 52,000 installed chargers, many clustered in the Inland Empire logistics hub. Texas follows with 31,500 units, where food-grade warehouses near Houston deploy 600 V inline chargers to offset grid congestion in the North America forklift battery charger market. Ohio’s automotive corridor runs 24,800 electric trucks supported by factory-floor chargers that meet GM’s 60-minute turnaround spec, while Illinois and Georgia host 22,000 and 19,000 units respectively, driven by e-commerce fulfillment centers around Joliet and Savannah. Looking forward, the Inflation Reduction Act’s Section 45X credit of US$35 per kWh for domestic battery cells is triggering at least 3 GWh of lithium-ion forklift pack production in Tennessee and Michigan, implying a second-wave charger uplift by late 2025. At the same time, Canadian ports—especially Vancouver—are shipping 12,000 charger cabinets annually to US distributors, signaling a tighter continental supply loop and setting the stage for faster technology diffusion across secondary markets in 2026.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Booming e-commerce warehousing increases electric forklifts requiring rapid chargers deployment

Explosive growth of same-day fulfillment hubs is propelling the core demand driver in the North America forklift battery charger market: rapid-charge readiness inside e-commerce warehouses. The United States added 82 million square feet of new logistics space during 2023, bringing cumulative high-bay facilities to roughly 1.1 billion square feet. Amazon alone commissioned ninety-four multilevel centers that run an aggregate fleet of 27,600 electric Class I trucks, each drawing an average 16 kWh per shift. At two shifts daily this single operator now requires over 880 MWh of charger output every twenty-four hours, forcing procurement teams to prioritize 240–300 A high-frequency chargers across dock zones and mezzanine pick modules for continuous uptime.

Ripple effects extend to regional third-party logistics providers, grocers, and reverse-logistics specialists that cannot tolerate mid-shift battery swaps. GXO Logistics reported in its March 2024 analyst call that fourteen US campuses upgraded to opportunity charging, integrating 1,300 wall-mounted units from Posicharge capable of adding 9 kWh during a standard dock staging cycle. Similar retrofits are underway at Kroger’s automated fresh facilities in Ohio, where 420 lithium forklifts share centralized 800 V busways feeding smart chargers that ramp from 40 kW to 60 kW during off-peak billing windows. These concrete-level investments confirm a structural rise in the North America forklift battery charger market, unseen in prior electrification waves across rooms and high-velocity fulfillment aisles.

Trend: Shift toward modular silicon-carbide chargers optimizing multi-chemistry fleet operations efficiency

Technological momentum within the North America forklift battery charger market is pivoting toward modular silicon-carbide (SiC) architectures that deliver five-kilohertz switching improvements and sharply lower thermal losses. Benchmark lab testing by Underwriters Laboratories in January 2024 recorded heat generation of only 18 W while delivering 30 kW, compared with 110 W for legacy insulated-gate bipolar transistor designs. Phoenix-based Advanced Energy shipped 8,400 SiC power stages in Q1 2024, each plug-compatible with 24–96 V forklifts across lead-acid, lithium-iron-phosphate, and nickel-zinc chemistries. Fleet operators now hot-swap four-pound power modules instead of entire cabinets, trimming mean-time-to-repair from nine hours to forty minutes and slashing maintenance labor during unplanned outages at regional grocery distribution centers and auto plants.

Software advances mirror the hardware shift. The latest SiC charger stacks expose CAN-open, Modbus, and Ethernet links, letting Raymond iTrack pull voltage, temperature, and duty-cycle data every three seconds. This granularity lets operators schedule micro-charge intervals that equalize cell voltages within 0.03 V, extending lithium-iron-phosphate pack life to nearly 7,500 cycles under double-shift duty in the North America forklift battery charger market. In April 2024, Walmart’s Brooksville, Florida facility validated the architecture with a 120-port SiC charger wall consuming 2.1 MWh nightly yet keeping peak draw below 350 kW through staggered sequencing. Investment payback emerges from deferred battery replacements worth roughly US$3.8 million across the pilot’s five-year horizon, demonstrating operating savings for multi-site operators.

Challenge: Utility interconnection delays bottleneck installation of high-power forklift charging stations

Despite record equipment orders, grid-side realities pose the most acute obstacle in the North America forklift battery charger market: protracted utility interconnection queues for loads above 500 kVA. Southern California Edison’s latest queue report shows 176 warehouse projects awaiting feeder upgrades, representing an aggregate 142 MW of charger capacity stalled beyond design completion. Average approval time now stretches to 14.6 months, almost double the building-permit cycle, forcing developers to rent diesel gensets or run hybrid propane forklifts. In Dallas County, a 1.3-million-square-foot fulfillment center commissioned by a national apparel retailer has 640 smart chargers on site but operates only 180 due to transformer shortages, reported by Oncor in February 2024 officially.

Project economics degrade further when temporary power contracts overlap with peak-demand surcharges. In Ontario, Hydro One assessed a seasonal capacity tag of CAD 23.79 per kilowatt on a Brampton auto-parts campus commissioning 78 fast chargers, inflating annual utility spend by roughly US$420,000 until a permanent substation arrives in mid-2025. Stakeholders in the North America forklift battery charger market are countering by pre-ordering pad-mounted transformers; Trane Technologies booked 620 units in its backlog specifically for material-handling sites. Others adopt microgrid strategies: Lineage Logistics added 2.8 MWh of onsite lithium storage in Savannah, discharging at 600 kW between 3 pm and 8 pm to bypass feeder constraints while maintaining uninterrupted freezer operations and forklift uptime margins.

Segmental Analysis

By Charger Type

Standard chargers command 57.91% of the North America forklift battery charger market because they drop directly into the electrical backbone found in legacy warehouses. Roughly 70,000 US and Canadian distribution centers still run three-phase 208 V or 240 V panels limited to 100 A branch circuits, a profile that welcomes 9 kW silicon-controlled-rectifier units without service upgrades. Installing one costs about US$4,000, while a 24 kW fast charger pulls 480 V and needs switchgear that drives project budgets up by nearly US$50,000 per dock row. Fleet data from the Battery Council International list 960,000 flooded lead-acid motive packs in active circulation; their eight-hour charge curve aligns perfectly with standard output, so managers avoid the ventilation and thermal controls fast chargers require.

Reliability keeps momentum on the side of conventional gear inside the North America forklift battery charger market. A well-maintained SCR cabinet delivers a mean time between failure of 32,000 hours and holds fewer than twenty spare parts, enabling on-site technicians to swap boards in under ninety minutes. In Memphis, a regional grocery hub tracked labor and trailer penalties at US$14,600 for every hour of idle equipment; predictable uptime matters more than absolute charging speed. Property insurers quote premiums of US$0.18 per US$100 of value on standard units, compared with US$0.32 for liquid-cooled fast models because lower amperage minimizes arc-flash and thermal events. Facilities also avoid demand spikes—one 9 kW charger draws only 1.1 kWh each operating hour—helping operators steer clear of stiff peak surcharges. Together, compatibility, low capital cost, and dependable performance explain why standard chargers remain the practical choice across a majority of facilities in the market.

By Class

Class 3 pallet trucks and walkie riders hold 50.23% of the end-user base served by the North America forklift battery charger market. The Industrial Truck Association logged 279,000 new Class 3 units entering US fleets in 2023, outpacing the next-largest class by 92,000 trucks. Canadian customs cleared another 41,600 electric pallet trucks through Vancouver, Montréal, and Halifax, bound mainly for grocery, parcel, and cold-chain facilities. Warehouse operators favor these smaller riders because each weighs under 6,000 lb, fits twelve-foot aisles, and needs no floor reinforcement—qualities that saved Kroger about US$18 per square foot when it converted a Romulus, Michigan cross-dock last year. With more than 1.5 million Class 3 forklifts circulating, charger volume naturally tracks their energy habits.

Usage intensity cements their pull on the North America forklift battery charger market. A pallet jack cycling a 24 V 510 Ah battery twice per shift consumes around 14 MWh daily when a 300-unit fleet runs nonstop. Managers pair these trucks with wall-mount chargers in the 5–10 kW, 50–150 A band, enabling lunch-break top-ups that add 6 kWh in twelve minutes—exactly what Walmart’s Brooksville, Florida cold store recorded across 36,000 charge events in February 2024. Sobeys in Canada replaced 1,200 lead-acid pallet jacks with lithium models and trimmed battery-room square footage by 7,600, reassigning two technicians per shift. Crown Equipment reports eight out of ten replacement cables it sells in North America fit Class 3 connectors, confirming the parts ecosystem that supports them. High unit counts, round-the-clock duty, and flexible infrastructure make Class 3 fleets the revenue engine for suppliers in the North America forklift battery charger market.

By Output Charging Current Rating

The 50 A–150 A current band controls almost one-third of the North America forklift battery charger market because it suits the dominant battery capacities—210 Ah walkie riders up to 750 Ah reach trucks—without overloading site feeders. A 100 A charger delivers 4.8 kW at 48 V or 7 kW at 72 V, finishing a mid-range 510 Ah pack within the preferred six-hour window. Pacific Northwest National Laboratory simulations released in March 2024 showed that a 500,000-square-foot warehouse running 300 chargers at 120 A stayed under 1.4 MW peak draw; moving to 200 A lifted the same building to 2 MW and forced a new utility transformer. By staying mid-current, site engineers sidestep expensive capacity upgrades.

Total ownership math reinforces the band’s dominance inside the North America forklift battery charger market. A sealed 120 A high-frequency charger weighs ninety-five pounds and lands at roughly US$5,200; a 300 A liquid-cooled sibling weighs 260 pounds and exceeds US$12,000 after adding coolant loops and vent kits. Shipping class drops from freight to parcel, cutting three days off delivery. FM Global audits reveal charge currents above 180 A require double-wall separation, adding nearly US$27,000 in construction per facility, a cost avoided in the 50–150 A range. Deere’s Ottawa, Kansas parts plant measured 4,800 mate cycles before connector pitting at 150 A versus 2,900 cycles at 225 A, trimming consumable budgets. Balancing grid impact, equipment price, and connector durability, the mid-current segment secures its front-runner position in the market.

By Power Rating

Chargers in the 5–10 kW bracket capture 29.28% of the North America forklift battery charger market because they match mainstream 36 V and 48 V packs while skating under costly electrical thresholds. A 7 kW unit pushes 145 A at 48 V during the bulk phase, then tapers to hold cell temperatures below 113 °F, a profile validated by Sandia National Laboratories, which clocked 92% conversion efficiency and only 0.56 kWh of waste heat per cycle. Facilities logging 1,000 nightly charges save 204 MWh a year over 15 kW alternatives, paring utility bills without sacrificing throughput. Staying below 10 kW per port also avoids the 50 kW per-meter line in NFPA 70E that triggers formal arc-flash studies, shaving eight weeks off commissioning schedules.

Installation agility keeps this segment on top in the North America forklift battery charger market. A 7.5 kW charger drawing 48 A at 208 V often taps existing lighting panels, so electricians finish installs in three hours without trenching. FedEx Ground’s Kansas City retrofit mounted 420 such units on mezzanine columns and saved roughly US$740,000 in conduit labor compared with floor-standing 25 kW posts. Finance houses recognize the liquidity of mid-power gear: Wells Fargo quoted a five-year residual of 22 cents per watt for 7.5 kW models, compared with 15 cents for anything over 15 kW. Maintenance stays light; air-cooling fans cost about US$38 a year, versus US$160 for glycol-cooled designs. Fifty 10 kW ports add under 0.5 MW of coincident load, a level most feeders absorb without transformer swaps. Those practical wins—energy efficiency, rapid deployment, and predictable grid impact—keep 5–10 kW systems firmly anchored as the workhorse tier within the market.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Country Analysis

The United States generates more than 83% of total revenue in the North America forklift battery charger market because it combines the largest electric-forklift fleet with the densest logistics infrastructure in the region. Roughly 1.9 million lift trucks now operate inside U.S. facilities, and the Industrial Truck Association logged 206,000 new electric units last year—three times Canada’s intake—creating a daily charger demand of almost 3 GWh. Tier-one charger makers such as EnerSys (Dallas), Delta-Q (Vancouver, WA), and Advanced Energy (Phoenix) maintain domestic SMT lines that can collectively assemble 340,000 units a year, ensuring product availability even during trans-Pacific bottlenecks. Capital expenditure is fueled by strong automation spend: Prologis customers alone added 120 million square feet of new U.S. warehouse space in 2023, each building budgeting about fifty ports per 100,000 square feet. Federal incentives amplify the pull; Section 45X credits grant US$35 per kWh on domestically produced forklift cells, while the Commercial Clean Vehicle Tax Credit refunds up to US$40,000 per electric truck, making charger procurement a line-item in every fleet electrification plan.

Ten states dominate consumption in the North America forklift battery charger market: California, Texas, Illinois, Florida, New York, Ohio, Georgia, Pennsylvania, Indiana, and Tennessee. Southern California’s Inland Empire runs an estimated 38,000 electric trucks that draw 55,000 installed chargers, a footprint mirrored by Houston’s port-centric cross-docks and Dallas’s e-commerce hubs. Illinois and Indiana leverage auto-parts corridors around Joliet and Lafayette, each pulling more than 600 MWh of charging energy weekly. Florida’s refrigerated logistics in Jacksonville and Lakeland rely on 5–10 kW wall units to avoid heat buildup, while New York’s urban micro-fulfillment sites favor 50–150 A units that slip inside mezzanines. Regional differences arise from grid headroom: Ohio’s older plants use 208 V, 80 A standard chargers, whereas Texas warehouses deploy 480 V, 120 A fast models tied to onsite solar. Sustained demand is reinforced by IoT-enabled chargers that feed WMS platforms with live SOC data, letting operators like Walmart and UPS orchestrate fleets with minute-level precision. The only speed bumps—extended utility interconnection queues and silicon-carbide component shortages—are being addressed through microgrid deployments and new GaN switching fabs in Arizona, helping the United States retain its commanding position in the North America forklift battery charger market.

Top Players in the North America Forklift Battery Charger Market

- PosiCharge

- EnerSys

- Alpine Power Systems

- Viking Power

- Crown Equipment Corporation

- Toyota Material Handling

- OneCharge

- Fronius International GmbH

- Flux Power Holdings, Inc.

- Green Cubes Technology

- Stryten Energy

- East Penn Manufacturing Company

- Advanced Charging Technologies

- Ecotec LTD LLC.

- Power Designers Sibex

- Stanbury Electrical Engineering LLC

- Other Prominent Players

Market Segmentation Overview

By Forklift Fuel Type

- Electric Forklift

- Hybrid Forklift

- Diesel Forklift

- Others

By Battery Type

- Sealed Lead Acid (SLA) Battery

- Lithium Ion Battery

- Nickel-Cadmium Battery Chargers

- Others

By Charger Type

- Standard Chargers

- Fast Chargers

- On-board Chargers

- Smart Chargers

By Voltage Type

- 24V Chargers

- 36V Chargers

- 48V Chargers

- 72V & 80V Chargers

By Forklift Class

- Class 1

- Class 2

- Class 3

By Output Charging Current Rating

- 50A-150A

- 151A-250A

- Above 251A

- Below 50A

By Power Rating

- UP TO 5KW

- 5-10 KW

- 11-15 KW

- >15KW

By Industry

- Warehouses

- Manufacturing

- Construction

- Retail and Wholesale Stores

- Others

By Sales Channel

- OEMs

- Aftermarket

By Country

- The U.S.

- Canada

- Mexico

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |