Market Scenario

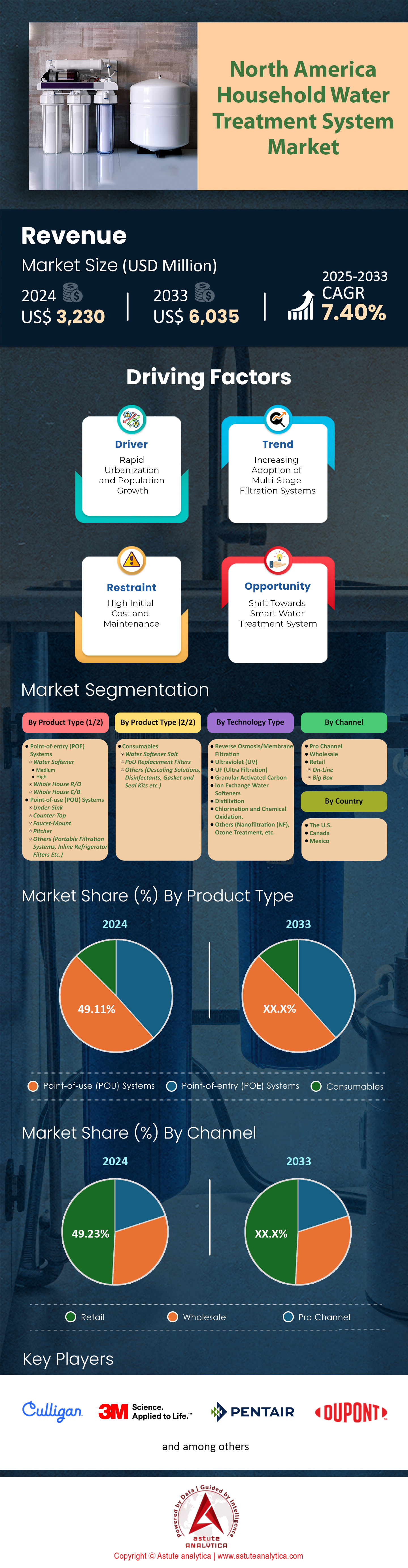

North America household water treatment system market was valued at US$ 3,230 million in 2024 and is projected to hit the market valuation of US$ 6,035 million by 2033 at a CAGR of 7.40% during the forecast period 2025–2033.

The demand and adoption of household water treatment systems in North America are well-established, driven by factors such as water contamination concerns, health awareness, and technological advancements. The United States leads the market, with over 40 million households using some form of water treatment system as of 2024, according to the U.S. Census Bureau. This is largely due to widespread awareness of water quality issues, such as lead contamination and PFAS (per- and polyfluoroalkyl substances) in drinking water. Canada follows closely, with over 30% of households using water treatment systems, as reported by Statistics Canada in 2024.

Mexico, while lagging behind the U.S. and Canada, is witnessing growing adoption, particularly in urban areas. The National Institute of Statistics and Geography (INEGI) reported that 20% of Mexican households now use water purification systems, up from 15% in 2020. This growth is fueled by increasing urbanization and government initiatives to improve water quality. Market players in the North America household water treatment system market are responding by expanding their product portfolios and focusing on affordability. For instance, in 2024, key players like Culligan, Brita, and Aquasana introduced budget-friendly filtration systems targeting low-income households in Mexico. These companies are leveraging advanced technologies, such as IoT-enabled systems and sustainable filtration solutions, to cater to evolving consumer demands. For example, in 2024, Culligan launched a smart water softener system that monitors water quality in real-time, while Aquasana introduced a solar-powered filtration system to appeal to eco-conscious consumers. Additionally, partnerships with government agencies and NGOs are helping market players expand their reach in underserved areas. Overall, the North America household water treatment system market is poised for continued growth, driven by increasing consumer awareness and technological innovation.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Increasing Awareness About Waterborne Diseases and Health Risks

The rising awareness about waterborne diseases and health risks has become a significant driver for the North America household water treatment system market. According to the Centers for Disease Control and Prevention (CDC), there were over 7,000 reported cases of waterborne diseases in the U.S. in 2023 alone, with contaminants like E. coli and lead being the primary culprits. This has led to heightened consumer concern about the safety of drinking water, especially in regions with aging infrastructure. A 2024 report by the Environmental Protection Agency (EPA) highlighted that over 12 million households in the U.S. are still served by lead pipes, which pose severe health risks.

Moreover, the Flint water crisis in Michigan and similar incidents in other states have further amplified public awareness. In Canada, Health Canada reported a 15% increase in water quality complaints in 2023, with many households opting for water treatment systems to ensure safety. The World Health Organization (WHO) also emphasizes that contaminated water is responsible for over 485,000 deaths globally each year, which has spurred demand for household water treatment solutions. As a result, consumers are increasingly investing in advanced filtration systems, such as reverse osmosis and UV purification, to mitigate health risks.

Trend: Shift Towards Eco-Friendly and Sustainable Water Treatment Solutions

The North America household water treatment system market is witnessing a significant shift towards eco-friendly and sustainable solutions. Consumers are increasingly prioritizing environmentally conscious products, driven by the growing concern over plastic waste and energy consumption. A 2024 study by the Environmental Working Group (EWG) revealed that over 60% of households in the U.S. prefer water treatment systems that reduce plastic bottle usage. This trend is further supported by government initiatives, such as the U.S. Environmental Protection Agency’s (EPA) WaterSense program, which promotes water-efficient products.

In Canada household water treatment system market, the government’s Single-Use Plastics Prohibition Regulations, implemented in 2023, have encouraged households to adopt sustainable water treatment solutions. A report by the Canadian Water and Wastewater Association (CWWA) found that 45% of Canadian households now use refillable water filtration systems to minimize plastic waste. Additionally, manufacturers are introducing innovative products, such as biodegradable filter cartridges and solar-powered purification systems, to cater to this demand. For instance, in 2024, a leading manufacturer launched a zero-waste water filtration system that uses recyclable materials and reduces carbon emissions by 30%. This trend is expected to grow as consumers become more environmentally conscious and governments impose stricter regulations on plastic usage.

Challenge: High Initial and Maintenance Costs of Advanced Water Treatment Systems

A primary challenge in the North America household water treatment system market is the high initial and maintenance costs associated with advanced systems. According to a 2024 report by the American Water Works Association (AWWA), the average cost of installing a reverse osmosis system in the U.S. ranges from $1,500 to $3,000, with annual maintenance costs exceeding $200. These costs can be prohibitive for low- and middle-income households, limiting market penetration. In Canada, a similar trend is observed, where the average cost of a whole-house water filtration system is approximately $2,500, according to the Canadian Mortgage and Housing Corporation (CMHC).

Moreover, the complexity of advanced systems often requires professional installation and regular servicing, adding to the overall expense. A 2024 survey by Consumer Reports found that 40% of households in the U.S. are hesitant to invest in water treatment systems due to high maintenance costs. In Mexico household water treatment system market, where the average household income is significantly lower, the challenge is even more pronounced. The National Water Commission (CONAGUA) reported that only 15% of households in Mexico can afford advanced water treatment systems, highlighting the economic barrier. Manufacturers are now focusing on developing cost-effective solutions, such as modular systems and pay-as-you-go models, to address this challenge and make water treatment more accessible to a broader audience.

Segmental Analysis

By Product Type

The dominance of Point-of-Use (POU) systems in the North American household water treatment market, capturing over 49% market share, is driven by their ability to address localized water quality concerns effectively. POU systems treat water directly at the point of consumption, ensuring that contaminants introduced through aging infrastructure are removed. This decentralized approach is particularly valuable in regions where municipal water systems may fail to meet safety standards. For example, POU systems can remove up to 99% of contaminants, including heavy metals, dissolved solids, and harmful chemicals, providing a reliable solution for households concerned about water safety.

The compact design and ease of installation of POU systems make them highly appealing to consumers. These systems can be easily fitted under sinks or attached to faucets, requiring minimal space and effort for setup. The versatility of POU systems is another key factor, as they can incorporate various technologies such as reverse osmosis, ultrafiltration, and activated carbon filters. This allows consumers in the household water treatment system market to choose solutions tailored to their specific water quality needs. For instance, reverse osmosis POU systems are particularly effective in removing dissolved salts and organic compounds, making them a popular choice in areas with high levels of water contamination. Moreover, cost-effectiveness and environmental benefits further drive the adoption of POU systems. Compared to centralized water treatment solutions, POU systems often have lower installation and maintenance costs, making them an attractive option for budget-conscious consumers. Additionally, these systems reduce the need for bottled water, aligning with the growing trend towards sustainability.

By Technology

Reverse Osmosis (RO) and Membrane Filtration technology dominate the US and Canada household water treatment system market, controlling more than 37.32% market share, due to their superior purification capabilities. RO systems are highly effective in removing a wide range of contaminants, including dissolved salts, bacteria, viruses, and organic compounds. These systems utilize a semi-permeable membrane to filter out particles as small as 0.0001 microns, ensuring the production of high-quality water suitable for both residential and industrial applications. The effectiveness of RO technology in addressing various water quality issues has made it a preferred choice for consumers seeking comprehensive water treatment solutions.

The adoption of RO and membrane filtration technologies is further driven by increasing awareness of water contamination issues and stringent water quality regulations. In regions where contaminants such as arsenic, lead, nitrates, and per- and polyfluoroalkyl substances (PFAS) are prevalent, RO systems offer a reliable solution for ensuring safe drinking water in the household water treatment system market. For instance, in areas with high arsenic levels in groundwater, particularly in the western and southwestern United States, RO systems are crucial for removing this carcinogenic contaminant. The ability of RO technology to address a broad spectrum of water quality concerns makes it an attractive option for consumers across diverse geographical areas with varying water quality challenges. Technological advancements and the integration of smart features also support the market dominance of RO and membrane filtration technologies. Modern RO systems often incorporate multi-stage filtration processes, enhancing their efficiency and effectiveness in water purification. The development of more durable membranes has led to reduced maintenance requirements and extended system lifespans, typically requiring membrane replacement every 4-5 years depending on usage and water quality.

By Channel

Retail channels dominate the North American household water treatment system market, accounting for more than 49.23% of sales, due to the extensive network of retailers and their strategic approaches to product distribution. Major retail chains such as Walmart and Home Depot play a crucial role in this sector, leveraging their vast distribution networks to reach a wide consumer base. These retailers utilize both physical stores and online platforms to maximize their reach, ensuring that consumers have easy access to a variety of water treatment products. For instance, Walmart's advanced logistics and distribution strategies enable efficient inventory management and widespread product availability, contributing to high sales volumes of water treatment systems.

The success of retail channels in household water treatment system market is further enhanced by their ability to offer competitive pricing and a wide range of products. Retail giants like Walmart and Home Depot employ data analytics to optimize product placement and inventory levels, thereby increasing sales and enhancing customer satisfaction. These retailers often run promotional campaigns and offer discounts, driving sales volumes and attracting price-sensitive consumers. The convenience of purchasing from well-known retail chains, coupled with their reputation for reliability, contributes significantly to the high sales volumes observed in this market segment. Additionally, the development of omnichannel distribution networks by these retailers integrates online and offline sales channels, providing a seamless shopping experience that caters to diverse consumer preferences.

Key retail chains have also adopted strategies to maintain their dominance in the water treatment systems market. One such strategy is the establishment of exclusive distribution agreements with manufacturers, ensuring that they offer unique products not available through other channels. This exclusivity drives consumer interest and increases sales volumes in the household water treatment system market. Furthermore, retailers invest in customer education and after-sales services, helping consumers make informed purchasing decisions and ensuring long-term satisfaction with their water treatment systems. The combination of extensive distribution networks, competitive pricing, product variety, and customer-focused services positions major retail chains as leaders in the market in North America.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Country Analysis

US Dominance in North America Household Water Treatment System Market

The United States' dominant position in the North American market, capturing over 69% market share, is driven by a combination of factors including water quality concerns, regulatory pressures, and consumer awareness. The US faces significant challenges related to water quality, with the presence of contaminants such as arsenic, lead, nitrates, and PFAS in drinking water sources across various regions. These water quality issues, coupled with aging water infrastructure, have heightened consumer awareness and demand for effective water treatment solutions. For instance, the EPA's Unregulated Contaminant Monitoring Program has identified and assessed up to 30 unregulated contaminants every five years, highlighting the ongoing need for advanced water treatment technologies.

Key players active in the US household water treatment system market include well-established brands such as Samsung, LG, Amazon, Google, Ring, and Bosch, who have leveraged their strong brand recognition and innovative product offerings to capture significant market share. These companies have been particularly successful in integrating smart home technologies with water treatment systems, appealing to tech-savvy consumers. The penetration of smart home devices in the US has been growing steadily, with a significant portion of households adopting devices such as smart thermostats, lighting systems, and security cameras. This trend towards smart home adoption has positively impacted the water treatment system market, as consumers increasingly seek integrated and technologically advanced solutions for their homes.

The future growth outlook for the US household water treatment system market remains positive, driven by increasing regulatory pressures and consumer demand for safer drinking water. The EPA's ongoing efforts to establish and enforce water quality standards, coupled with growing public awareness of water contamination issues, are expected to fuel market growth in the coming years. Additionally, technological advancements in water treatment, such as improvements in reverse osmosis and membrane filtration technologies, are likely to drive innovation and market expansion. As the US continues to address its water quality challenges, the market for water treatment solutions is poised for significant growth, supported by both regulatory requirements and consumer preferences for clean, safe drinking water.

Top Players In the North America Household Water Treatment System Market

- Water Treatment Brands

- 3M

- AO Smith Corporation

- Brondell

- Calgon Carbon Corporation

- Dupont

- Culligan Water

- Evoqua Water Technologies

- APEC WATER

- Canature

- Pentair

- Clack

- AquaTru, LLC

- Express Water Inc.

- Max Water

- Xylem Inc.

- Other Prominent Players

- Wholesale Players

- Ferguson

- Winsupply Inc.

- Robert B Hill Co.

- Water Filters of America

- U.S. Water Wholesale

- HomePlus

- Other Prominent Players

Market Segmentation Overview:

By Product Type

- Point-of-entry (POE) Systems

- Water Softener

- Medium

- High

- Whole House R/O

- Whole House C/B

- Water Softener

- Point-of-use (POU) Systems

- Under-Sink

- Counter-Top

- Faucet-Mount

- Pitcher

- Others (Portable Filtration Systems, Inline Refrigerator Filters Etc.)

- Consumables

- Water Softener Salt

- PoU Replacement Filters

- Others (Descaling Solutions, Disinfectants, Gasket and Seal Kits etc.)

By Technology Type

- Reverse Osmosis/Membrane Filtration

- Ultraviolet (UV)

- UF (Ultra Filtration)

- Granular Activated Carbon

- Ion Exchange Water Softeners

- Distillation

- Chlorination and Chemical Oxidation.

- Others (Nanofiltration (NF), Ozone Treatment, etc.

By Channel

- Pro Channel

- Wholesale

- Retail

- On-Line

- Big Box

By Country

- The U.S.

- Canada

- Mexico

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |