Permanent Magnet Market: By Type (Neodymium Iron Boron (NdFeB) Magnets, Samarium Cobalt (SmCo) Magnets, Alnico Magnets, Ferrite Magnets); Grade (Low Grade, Mid-Grade, High Grade); Manfacturing Process (Sintered Magnets, Bonded Magnets, Injection Magnets, Hot Pressed Magnets); End Users (Automotive, Consumer Electronics, Industrial Equipment, Aerospace & Defense, Semiconductor, Military, Others); End Users (Automotive, Consumer Electronics, Industrial Equipment, Aerospace & Defense, Semiconductor, Military, Others); Distribution Channel (Online, Offline (Direct Sales and Distributors); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 17-Sep-2025 | | Report ID: AA09251504

Market Scenario

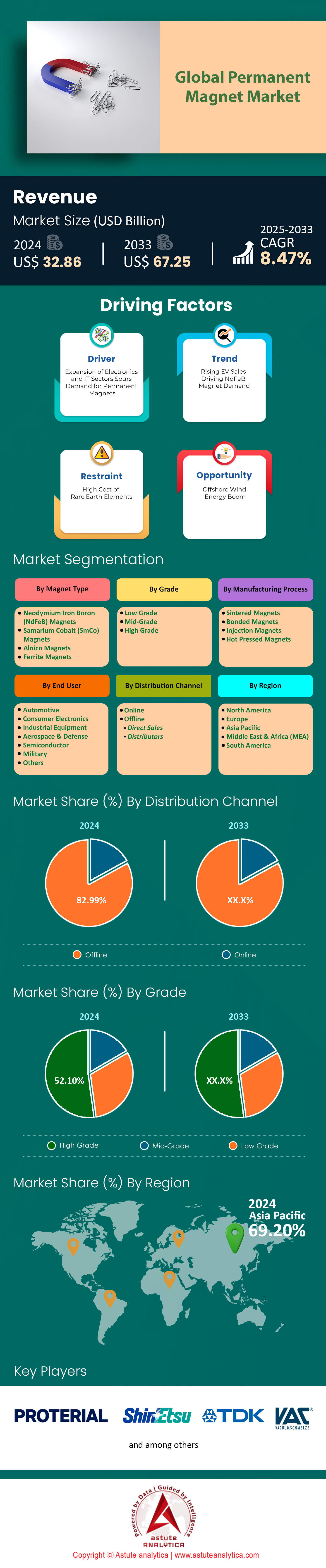

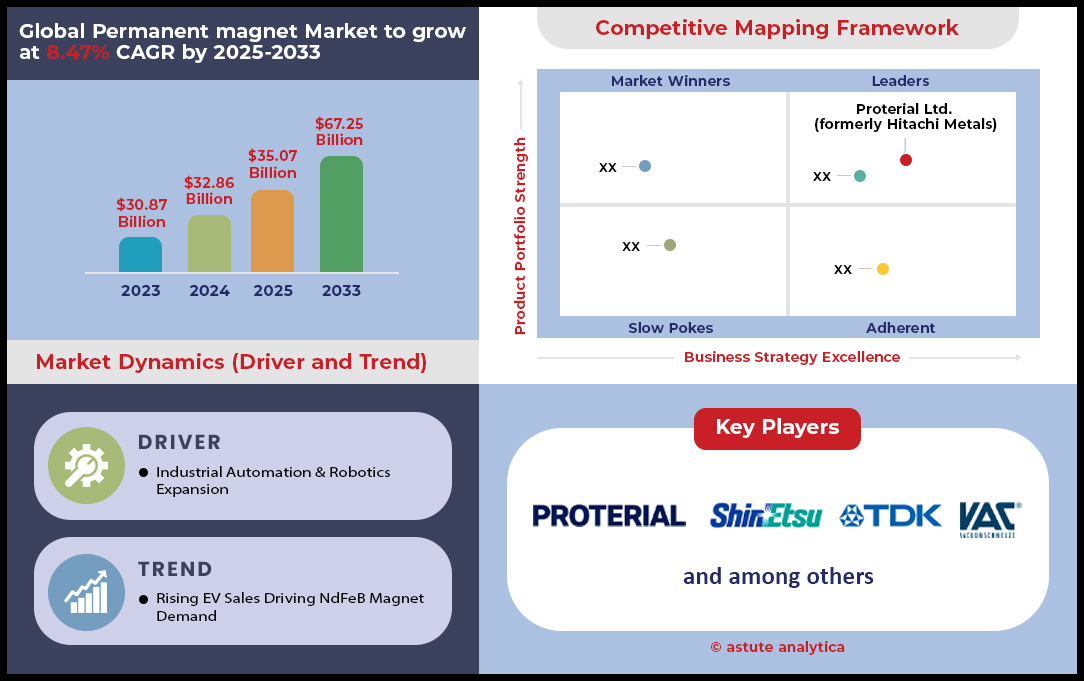

Permanent magnet market was valued at US$ 32.86 billion in 2024 and is projected to hit the market valuation of US$ 67.25 billion by 2033 at a CAGR of 8.47% during the forecast period 2025–2033.

Key Findings

- Based on type, Neodymium Iron Boron (NdFeB) Magnets is dominating the market and is capturing over 48.02% market share.

- Based on manufacturing process, Sintered magnets is leading the manufacturing process for permanent magnet. it is controlling over 64.73% market share.

- Based on end users, automotive industry is the largest buyers and consumers of the permanent magnet with over 39.65% market share.

- Based on grade, high grade is leading the market as it capture over 52.10% market share.

- Asia Pacific is the largest market as it capture over 69.20% market share.

- Global permanent magnet market is poised to reach US$ 67.25 billion by 2033.

The permanent magnet market is experiencing a transformative surge driven by profound industrial revolutions, with the automotive sector emerging as the foremost force reshaping demand. In 2024 alone, electric vehicle motor production soared to an impressive 22.9 million units, with forecasts projecting a robust climb to 28.1 million units by 2025. A dominant share of this growth—19.7 million units in 2024—came from Permanent Magnet Synchronous Motors, underscoring their critical role. This rapid expansion translated to a substantial consumption of 37 kilotons of rare earth elements in 2024, with expectations to escalate to 43 kilotons in 2025. Industry frontrunners like Tesla and BYD, which surpassed production milestones of 2.1 million and 3 million electric vehicles respectively in 2024, exemplify this accelerating trend.

Demand is diversifying beyond automobiles in the permanent magnet market. The renewable energy sector is a major consumer. China's new wind power installations alone totaled 80.45 gigawatts in 2024, requiring 9,735 metric tons of NdFeB magnets. Industrial automation further fuels growth, with China's industrial robot production projected to reach 941,000 units in 2025. Even established sectors contribute heavily; air conditioner production hit 270 million units in 2024, creating a demand for 21,000 metric tons of NdFeB magnets.

The broad-based demand ensures permanent magnet market resilience. The consumer electronics sphere, with nearly 1.3 billion smartphones shipped in 2024, provides a high-volume foundation. Simultaneously, strategic sectors create critical, non-negotiable demand. A single Virginia-class submarine requires 9,200 pounds of rare earth materials, while an F-35 aircraft needs over 900 pounds, cementing the material's strategic importance.

To Get more Insights, Request A Free Sample

Top 2 New Frontiers for Unprecedented Market Expansion

Opportunities in the Permanent magnet market are expanding into highly specialized, high-value sectors, promising significant growth beyond traditional applications.

- The Medical Technology Revolution: Advanced medical devices represent a powerful emerging opportunity. The demand for high-field MRI systems, which rely on powerful superconducting magnets often complemented by permanent magnets for shimming, is growing. In 2024, over 3,000 new 3T MRI systems were installed globally. Furthermore, the burgeoning field of robotic surgery, with an estimated 22,000 new surgical robot installations in 2024, utilizes dozens of small, high-precision permanent magnets in each robotic arm for precise motor control and feedback. Miniaturized magnets are also critical in developing next-generation targeted drug delivery systems and advanced medical sensor technologies.

- The High-Speed Rail and Maglev Megaprojects: The global push for faster, more efficient mass transit is creating massive demand for permanent magnet market in Maglev (magnetic levitation) and other high-speed rail projects. For instance, a new 174-kilometer Maglev line planned in China will require an estimated 3,500 metric tons of high-grade NdFeB magnets for its levitation and propulsion systems. In 2025, Japan is scheduled to begin testing on a new section of the Chuo Shinkansen, a project that will ultimately use over 100,000 magnetic units for its system. These large-scale infrastructure projects represent long-term, high-volume demand channels.

New Demand Catalysts Defining the Next Market Growth Wave

Data Center Power Efficiency Drives Specialized Magnet Integration

The explosive growth of data infrastructure is creating a significant, non-obvious demand channel for the Permanent magnet market. In 2024 alone, construction began on over 300 new hyperscale data centers globally. Each of these facilities requires thousands of high-efficiency motors for cooling. Over 1.5 million high-efficiency permanent magnet motors were installed in data center HVAC systems in 2024. The total power consumption for these new facilities is projected to exceed 15 gigawatts by 2025. This intense energy usage is driving innovation in cooling technology.

The adoption of direct-to-chip liquid cooling is a key trend, with an estimated 450,000 specialized magnetic-drive pumps deployed in these systems in 2024. Projections for 2025 show this number exceeding 700,000 units. These pumps offer superior reliability and control. Furthermore, over 25,000 magnetic levitation chillers were installed in data centers in 2024 for frictionless, efficient operation. The industry saw an investment of over $2 billion in 2024 specifically for upgrading legacy cooling systems to magnet-based solutions. In 2025, an estimated 50 petabytes of data will be generated every second, further fueling the construction of these power-hungry facilities.

Aerospace and Urban Air Mobility Create a High-Value Demand Frontier

A new high-value frontier is opening in the Permanent magnet market, driven by aerospace modernization and the dawn of urban air mobility. In 2024, the development pipeline for electric vertical takeoff and landing (eVTOL) aircraft included over 400 distinct prototypes globally. Major players in this space collectively placed pre-orders for more than 15,000 eVTOL aircraft by the end of 2024. Each aircraft requires between 8 to 16 lightweight, power-dense permanent magnet motors for propulsion. This translates to a near-term demand for over 120,000 high-performance motors.

Investment in the urban air mobility sector surpassed $7 billion in 2024. The "more-electric aircraft" (MEA) initiative in commercial aviation is also a key driver for the permanent magnet market. In 2024, Airbus and Boeing logged orders for over 2,000 MEA-compliant aircraft, which replace heavy hydraulic systems with lighter electromechanical actuators using powerful magnets. Over 500,000 high-performance magnetic actuators were ordered for these new aircraft builds in 2024. Additionally, the booming satellite industry, which launched over 2,500 new satellites in 2024, uses permanent magnets in reaction wheels and actuators for positioning. This demand is forecast to grow as an additional 12,000 satellites are planned for launch by the end of 2025.

Segmental Analysis

NdFeB Magnets Superior Force Redefines Industry Standards

Neodymium Iron Boron (NdFeB) magnets are the undisputed leaders in the permanent magnet market, commanding an impressive 48.02% market share. Their dominance stems from an exceptional energy product, which can exceed 55 MGOe, allowing for significant device miniaturization. For instance, their use in smartphone voice coil motors, measuring just a few millimeters, is critical for audio performance. A key driver is the electric vehicle (EV) sector, where a single EV traction motor often utilizes between 1.5 kg and 2.5 kg of NdFeB magnets. With global EV production projected to surpass 20 million units annually by 2025, the demand is set to soar. In the renewable energy sector, a Vestas V164-10.0 MW offshore wind turbine requires approximately 2,000 kg of these powerful magnets, showcasing their role in large-scale energy generation.

The pull force of a small N52 grade NdFeB magnet, just 1 inch in diameter, can exceed 150 lbs, a testament to its power. This strength is vital in industrial robotics, where servo motors require high torque in compact designs, with some motors containing over 50 individual magnet pieces. Global production capacity across the permanent magnet market is expanding rapidly, with major manufacturers planning to add over 30,000 tons of new capacity by the end of 2025 to meet escalating demand. The price of neodymium oxide, a key raw material, has seen fluctuations between $90/kg and $120/kg in 2024, directly impacting production costs.

- Modern hard disk drives (HDDs) utilize NdFeB magnets that spin at speeds up to 15,000 RPM.

- High-fidelity headphones and speakers use neodymium magnets as small as 8mm in diameter to produce powerful, clear sound.

- In medical applications, magnetic separation systems using NdFeB can process up to 1,000 liters of biological samples per hour.

Sintered Magnets Precision Engineering for Peak Magnetic Performance

The sintered manufacturing process solidifies its lead in the permanent magnet market, controlling a massive 64.73% market share. Its advantage lies in producing magnets with the highest magnetic flux density, achieving a density of around 7.6 g/cm³, which is over 25% denser than typical bonded magnets. This process allows for the creation of magnets with a maximum energy product reaching 52 MGOe, a level unattainable by other methods. Sintering involves heating compacted powder to temperatures often exceeding 1,100°C, creating a solid magnet with superior thermal stability, capable of operating reliably at temperatures up to 230°C for certain grades.

The high intrinsic coercivity of sintered magnets, often surpassing 30 kOe, makes them exceptionally resistant to demagnetization, a critical feature for high-stress applications like EV motors and industrial generators. While the process requires diamond-coated tools for grinding and shaping due to the material's hardness (registering around 600 on the Vickers hardness scale), it ensures precise tolerances, often as tight as +/- 0.05 mm. The production cycle for a batch of sintered magnets in the permanent magnet market, from powder preparation to final coating, can take between 7 to 14 days, reflecting the complexity and precision involved in achieving top-tier performance.

- Sintering enables the alignment of magnetic domains with a precision of over 98%, maximizing the magnet's final strength.

- Protective coatings, such as a 5-10 micron layer of Nickel-Copper-Nickel, are applied to prevent oxidation.

- The scrap rate during the cutting and grinding of brittle sintered blocks can be as high as 30-40%.

Automotive Sector Unprecedented Magnet Demand in Vehicle Electrification

The automotive industry is the primary consumer in the permanent magnet market, accounting for a commanding 39.65% share. The average modern vehicle contains over 100 electric motors, sensors, and actuators that rely on magnets. For example, an electric power steering (EPS) system alone can use up to 0.5 kg of magnets. The explosive growth of EVs is the main catalyst; producing one million EVs requires approximately 1,200 metric tons of permanent magnets. A premium EV like the Tesla Model S Plaid utilizes a tri-motor setup, significantly increasing its magnet content to enhance its sub-2-second 0-60 mph acceleration.

Beyond the powertrain, magnets have become integral to Advanced Driver-Assistance Systems (ADAS). A single vehicle in the permanent magnet market can have over 20 ADAS sensors, including cameras and LiDAR, which use miniature magnets for positioning and stabilization. Even seemingly simple components, like power window motors, use around 8 to 12 small magnets each. The audio system in a luxury car can feature more than 20 speakers, each containing a high-performance magnet. With an estimated 45 million new vehicles equipped with extensive ADAS features expected to be sold in 2025, the consumption of magnets for sensors will continue its upward trend.

- Regenerative braking systems in EVs can recover up to 70% of kinetic energy, a feat enabled by high-performance magnets.

- Each automatic seat adjustment system in a luxury vehicle can contain between 6 and 14 individual motors with magnets.

- The global demand for magnets in automotive micro-motors is projected to exceed 4 billion units by 2025.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

High-Grade Magnets Pushing the Boundaries of Magnetic Strength

High-grade magnets are at the forefront of the permanent magnet market, holding a 52.10% market share by enabling technologies that demand ultimate performance. The distinction between grades is significant; an N54 grade NdFeB magnet has a remanence (Br) of over 1.48 Tesla, about 15% stronger than a standard N42 grade magnet. This increased strength allows engineers to design smaller, lighter, and more efficient motors. For example, in drones, using N52 grade magnets instead of N45 can increase flight time by up to 10% due to weight reduction and motor efficiency gains. In high-speed industrial spindles that can reach 60,000 RPM, high-grade magnets are essential for maintaining performance and stability.

The aerospace and defense industries across the global permanent magnet market utilize high-grade Samarium Cobalt (SmCo) magnets that can operate at temperatures exceeding 350°C, a critical requirement for missile guidance fins and satellite components. The development of laminated NdFeB magnets has been a breakthrough for high-frequency applications, reducing eddy current losses by as much as 50% in motors operating above 10,000 RPM. In medical technology, the field strength of a modern 3T MRI scanner is generated by a superconducting electromagnet, but the precise positioning of gradient coils and other components relies on over 1,000 individual high-grade permanent magnets.

- A high-grade N55SH magnet can maintain its magnetic properties up to a temperature of 150°C.

- In maglev train technology, high-grade magnets are used to achieve levitation gaps of approximately 10 millimeters with complete stability.

- The magnetic field uniformity required in particle accelerators is achieved using hundreds of precisely calibrated high-grade quadrupole magnets.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific Solidifies its Uncontested Global Manufacturing Dominance

The Asia Pacific region, commanding over 69.20% of the market, is the undisputed epicenter of the global Permanent magnet market. This dominance is not accidental; it is the result of a concerted strategy centered in China, which leverages unparalleled control over the entire value chain. In 2024, China's export volume of rare earth permanent magnets reached a record 58,147 tonnes, demonstrating its massive production scale. The nation’s top three export destinations in the first four months of 2024 were Germany (3,359 tons), the United States (2,202 tons), and South Korea (1,936 tons), showcasing its deep integration into global supply chains. This industrial might is built on a foundation of raw material supremacy and continuous government support for capacity expansion.

Beyond China, other regional players in the permanent magnet market contribute to the ecosystem's strength. Japan installed a record 703 MW of new wind power capacity in 2024, a key end-market for high-performance magnets. The total electricity generated by wind in Japan in 2024 was approximately 10.6 TWh. South Korea, a hub for advanced electronics, and Vietnam, an emerging rare earth supplier, further bolster the region's position. The sheer scale is staggering; in 2024, China's production of new energy vehicles, a primary demand driver, exceeded 9.5 million units. Further investment in capacity ensures this leadership will continue for the foreseeable future, making the region the primary engine of the global Permanent magnet market.

Europe Accelerates its Strategic Push for Supply Chain Autonomy

Europe is aggressively working to establish a regional and resilient Permanent magnet market, driven by strategic initiatives like the Critical Raw Materials Act. A landmark development is Solvay’s inauguration of a new rare earth processing line in La Rochelle, France, in April 2025, creating the largest separation facility outside China. The facility currently produces 4,000 metric tons of separated oxides annually and will start producing magnet-grade materials in 2025. By 2030, Solvay aims to satisfy 30% of European demand for these materials. These efforts are crucial as the continent's demand continues to rise, fueled by its automotive and renewable energy sectors.

The end-market demand is robust across the permanent magnet market. In the UK, the September 2024 renewables auction awarded contracts for approximately 5.3 GW of new offshore wind capacity, a significant consumer of large permanent magnets. These projects are part of a larger award of 9.6 GW across 131 new green infrastructure projects. Germany, a primary importer of Chinese magnets, is also a major automotive producer, providing a substantial demand base. The focus is now on connecting these demand centers with nascent European production capabilities, fostering a more secure and autonomous supply chain.

North America Strategically Rebuilds its Domestic Magnet Production Base

North America is executing a deliberate and well-funded strategy to onshore the Permanent magnet market, prioritizing national security and supply chain resilience. The U.S. government is a key financial driver, with the Department of Defense actively funding domestic projects. In December 2024, the DoD approved a US$1.8 million payment to Ucore Rare Metals Inc. for its separation work. This brings the total payments under that specific agreement to US$2.3 million. These investments are creating tangible production capabilities, with USA Rare Earth's Oklahoma facility targeting an initial capacity of 1,200 tons per annum by 2025.

Canada is concurrently building out its processing capabilities in the permanent magnet market. In 2024, Natural Resources Canada invested $4.2 million in Ucore to help commercialize its separation technology in Kingston, Ontario. The Saskatchewan Research Council's new processing plant became operational in 2024, targeting an output of 400 tonnes of NdPr metals per year. Further south, Mexico's automotive industry provides a massive demand anchor, having produced a record-breaking 3,989,403 light vehicles in 2024. Of these, EV production doubled in 2024 to approximately 220,000 units, reinforcing the region's integrated demand structure.

Strategic Investments and Acquisitions Reshape the Competitive Landscape of the Permanent Magnet Market

- USA Rare Earth Goes Public via SPAC: In August 2024, USA Rare Earth announced a definitive agreement to merge with Inflection Point Acquisition Corp. II, valuing the company at $870 million and taking it public to fund its Oklahoma facility.

- Niron Magnetics Secures $25M for Rare Earth-Free Tech: In February 2024, Niron Magnetics raised $25 million in a funding round led by Samsung Ventures, with participation from Magna and Allison Transmission, to scale its iron nitride magnet production.

- Australian Strategic Materials Gets US$600M US EXIM Backing:

In March 2024, ASM received a letter of interest from US Export-Import Bank for a debt package up to approx. $600 million for its Dubbo rare earth project. - Ucore Rare Metals Secures C$4.2M from Canadian Government: In February 2024, the Canadian government invested $4.2 million through its CMRDD program to help Ucore scale up its rare earth separation technology in Ontario.

- Australian Government Grants A$5M to ASM's Dubbo Project: In October 2024, the Australian government awarded a $5 million grant to Australian Strategic Materials to support pathways to production at the Dubbo Project, giving further push to the permanent magnet market growth.

- Solvay and Cyclic Materials Sign Recycling Supply Deal: In June 2024, Solvay signed an agreement for Cyclic Materials to supply recycled mixed rare earth oxide to its La Rochelle hub, securing a key circular economy feedstock.

- Ucore Closes $2.4M Private Placement: In November 2024, Ucore Rare Metals raised $2,401,665 in a non-brokered private placement to fund feedstock agreements and engineering for its Louisiana facility.

- US DoD Awards Ucore with US$1.8M Payment: In December 2024, the U.S. Department of Defense approved a $1.8 million payment to Ucore for completing milestones related to its REE separation work at its Ontario facility.

- ASM Secures A$400M Backing from Export Development Canada:

In 2024, Canadian Export Development Canada conditionally committed A$400 million in debt financing for ASM’s Dubbo Project. - Solvay Inaugurates New Production Line in France: In April 2025, Solvay officially inaugurated its expanded production line at La Rochelle, a strategic investment to begin commercial production of rare earths for permanent magnets in Europe.

Top Companies in the Permanent Magnet Market

- TDK Corporation

- Shin-Etsu Chemical Co., Ltd.

- Daido Steel Co., Ltd .

- MP Materials Corp.

- Lynas Rare Earths Ltd.

- Ningbo Yunsheng Co., Ltd.

- Beijing Zhong Ke San Huan Hi-Tech Co., Ltd.

- VACUUMSCHMELZE GmbH & Co. KG (VAC)

- Arnold Magnetic Technologies

- Electron Energy Corporation

- Adams Magnetic Products Co.

- Hitachi Metals, Ltd.

- Other Prominent Players

Market Segmentation Overview

By Magnet Type

- Neodymium Iron Boron (NdFeB) Magnets

- Samarium Cobalt (SmCo) Magnets

- Alnico Magnets

- Ferrite Magnets

By Grade

- Low Grade

- Mid-Grade

- High Grade

By Manufacturing Process

- Sintered Magnets

- Bonded Magnets

- Injection Magnets

- Hot Pressed Magnets

By End User

- Automotive

- Consumer Electronics

- Industrial Equipment

- Aerospace & Defense

- Semiconductor

- Military

- Others

By Distribution Channel

- Online

- Offline

- Direct Sales

- Distributors

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- The UK

- Germany

- France

- Italy

- Spain

- Poland

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia & New Zealand

- ASEAN

- Cambodia

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |