Market Snapshot

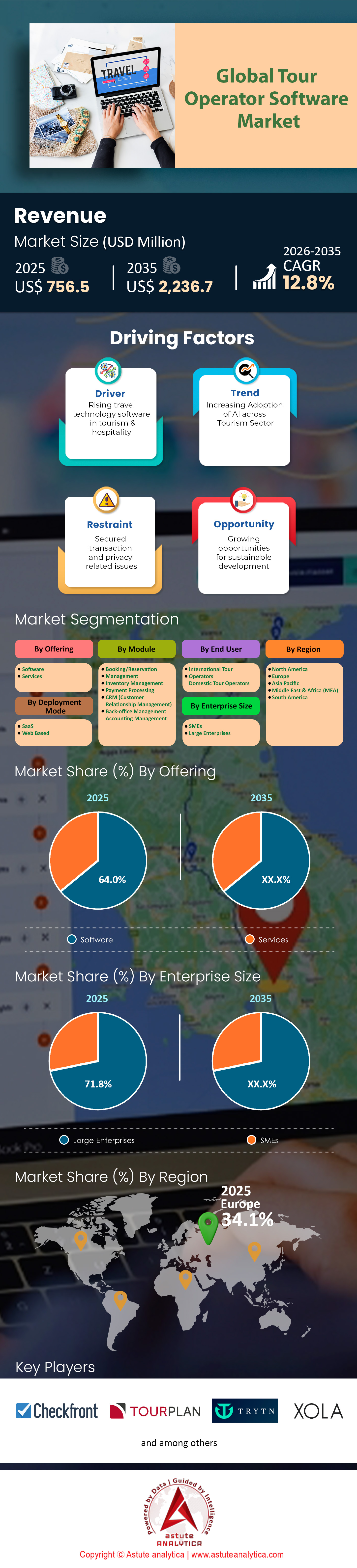

Tour operator software market was valued at US$ 756.5 million in 2025 and is projected surpass the market size of US$ 2,236.7 million by 2035 at a CAGR of 12.8% during the forecast period 2026–2035.

Key Findings

- By module, booking/reservation management contributed over 35.1% of the market.

- By deployment, Software-as-a-Service (SaaS) is dominating the global tour operator software market and holds a substantial share of 57.2%.

- By end users, domestic tour operators held the largest market share of 70%.

- By enterprise size, large enterprises have historically dominated the market, capturing over 71.8% of the market share.

- Asia Pacific is set to remain the largest and fastest growing regional market at a CAGR of 13.40% during the forecast period.

In 2025, the competitive hierarchy of the Tour operator software market has undergone a radical restructuring, which is mainly driven by a wave of strategic consolidation that has redefined market power. Wherein, the formation of Expedition Software Holding is the most significant shift observed, a massive conglomerate resulting from the merger of Rezdy, Checkfront, and Regiondo. Together, this unified entity commands a customer base of approximately 17,000 operators and processes a Gross Booking Value (GBV) exceeding USD 5 billion annually. By combining forces, the group has effectively partitioned the globe: Rezdy secures the Oceania region, Regiondo dominates Europe, and Checkfront anchors the North American sector.

Facing this new powerhouse is FareHarbor, a Booking Holdings subsidiary, which maintains its solitary dominance in the tour operator software market through sheer operational scale. With a massive workforce of 918 employees, the company supports over 20,000 active clients, proving that a single entity can still rival a conglomerate. FareHarbor remains relentless in development, delivering 184 product updates in 2024 alone—averaging one update every two days to outpace rivals. Meanwhile, Peek Pro has fortified its position as a formidable independent contender, backed by a Series C capital injection of USD 80 million and a subsequent USD 70 million raise linked to acquisitions like ACME Ticketing. External validation also plays a role in this hierarchy; GetYourGuide’s 2025 Connectivity Partner Program selected just 3 "Premium" partners—Bókun, Ventrata, and Palisis—out of 150+ integrations, signaling a clear market preference for quality over quantity.

To Get more Insights, Request A Free Sample

Where Is Demand Most Concentrated?

Geographically, the demand within the tour operator software market mirrors the density of the global experience economy. North America continues to act as the primary revenue engine, a trend highlighted by Peek’s concentration of 3,583 active customers within the United States. Across the Atlantic, Europe is witnessing a surge in digitization driven by the need for cross-border functionality; Regiondo addresses this specific demand by supporting 11 distinct languages. The APAC region, particularly Australia and New Zealand, displays high digital maturity, with Rezdy serving 1,055 operators in its home market alone.

However, the "long-tail" of the tour operator software market is where the most volume resides. According to Arival’s 2025 "State of Experiences" report, nearly 4 in 5 tour operators are small businesses serving fewer than 10,000 guests annually. Consequently, this SME segment has become the primary battleground for vendors seeking volume. On the other end of the spectrum, the high-volume attraction sector—defined as entities serving over 50,000 guests—represents a smaller but highly lucrative slice. Enterprise-grade platforms like Ventrata and the newly consolidated Expedition group are aggressively targeting these high-value clients to secure recurring enterprise revenue.

What Trends are Defining the 2025 Roadmap?

Verticalization and embedded financial technology (FinTech) are the twin pillars currently shaping the Tour operator software market as vendors are evolving from simple booking engines into comprehensive financial ecosystems. FareHarbor exemplifies this shift with the rollout of "Link by Stripe" in 2025, a feature designed to streamline checkout flows across 7 key markets, including the US and UAE. Following suit, Regiondo has integrated 5 major digital wallets, including Apple Pay and Google Pay, directly into its booking flow to capture mobile-first travelers.

Alongside these technical upgrades, a shift from "growth-at-all-costs" to "monetization of services" is evident. A pivotal move in tour operator software market involves FareHarbor transitioning its legacy free website products to paid tiers. Operators utilizing these web services now face annual fees of up to USD 5,000, a strategic pivot designed to filter for high-value clients and increase unit economics. Artificial Intelligence is also moving from buzzword to utility; GetYourGuide launched "Actionable AI" tools in late 2024 to help operators analyze customer feedback. To support these increasingly complex, data-heavy dashboards, FareHarbor now recommends a minimum hardware spec of 8 GB RAM, proving that modern software requires modern infrastructure.

What Are the Untapped Opportunities for Revenue?

Despite high adoption rates, the "digital gap" remains the most significant opportunity. Arival data reveals that almost 2 in 5 operators globally still function without a dedicated reservation system, relying instead on manual methods or spreadsheets. This unconnected segment represents billions in untapped transaction volume for the Tour operator software market. Furthermore, macro-economic events act as catalysts for adoption; the 2026 World Cup is projected to generate USD 2 billion in economic impact. Software providers capable of onboarding operators ahead of such mega-events stand to capture immense transaction fees from the influx of visitors.

Beyond initial bookings, cross-selling ancillary services has emerged as a vital revenue stream in the tour operator software market. With travelers now booking an average of 7 distinct experiences per trip, platforms are racing to become "reseller marketplaces." Bókun leads this charge with 27,000 partners in its marketplace, enabling operators to cross-sell tours and earn commissions. Additionally, the rise of "Event Tourism"—where concertgoers spend an average of USD 1,300 per show—opens new doors for software adapted for ticketing and time-slot management, a niche Peek is aggressively entering via its ACME Ticketing acquisition.

How Competitive Is the Feature War?

Competition in the Tour operator software market is currently fought on the battlegrounds of reliability and connectivity. Checkfront differentiates itself by marketing 99.99% uptime reliability, a metric that appeals heavily to risk-averse enterprise clients. Rezdy counters with breadth, offering connections to 25,000 resellers and 30 payment gateways, positioning itself as the ultimate distribution hub. TrekkSoft competes on flexibility, allowing operators to accept payments in 33 currencies to capture international bookings without friction.

Mobile capability is another fiercely contested arena. Peek Pro offers 2 dedicated mobile apps (iOS and Android) to empower guides in the field, acknowledging that operations rarely happen behind a desk. FareHarbor ensures its platform is accessible globally by supporting bank accounts in 3 distinct regions (Americas, EMEA, APAC). To lower barriers to entry, price wars are rampant: Checkfront and Rezdy both anchor the market with USD 49 entry-level plans, while Regiondo matches with a EUR 49 starter tier. Trial periods are weaponized for acquisition; Regiondo and FareHarbor offer 30-day trials, while Rezdy offers 21 days, and Bókun provides 14 days to convert hesitant users.

What Do Leaders in Tour Operator Software Market Say About the Future?

Strategic narratives from market leaders in 2025 focus heavily on "connectivity" and "ecosystem value." Lawrence Hester, the co-founder of FareHarbor who returned in June 2025 to lead the newly formed Expedition Software Holding, emphasized the power of scale, stating that the merger allows them to "leverage unique regional strengths to create a comprehensive global solution." Such statements underscore a move toward unified global platforms rather than regional fragmentation.

On the distribution side, Tao Tao, COO of GetYourGuide, highlighted the necessity of technological maturity in the tour operator software market , noting that their "Premium Connectivity Partners" like Bókun are critical for "accelerating the industry's transition to digital-first operations." Meanwhile, Ruzwana Bashir, CEO of Peek, continues to advocate for a "10-year leap forward in digitization," positioning her platform not just as software, but as a "Shopify for experiences" that empowers SMEs to compete with major attractions. These insights confirm that the market has moved beyond simple booking management to becoming the central nervous system of the global tourism industry.

Segmental Analysis

Unrivaled Inventory Control And Instant Payments Fuel Booking Module Market Supremacy

Centralized control over inventory largely explains why the booking and reservation management module captured a massive 35.1% market share. Modern platforms within the tour operator software market now process over 5,000 transactions daily without manual intervention, effectively eliminating the chaos of spreadsheets. Operators utilize these modules to manage live inventory across multiple channels simultaneously, leveraging direct connections to over 60 prominent Online Travel Agencies like Expedia and Viator. Such connectivity allows systems to facilitate seat availability updates in merely 2 milliseconds, preventing overbooking errors that previously cost companies distinct revenue streams. Furthermore, leading providers have introduced dynamic pricing algorithms that adjust rates based on real-time demand, enabling operators to generate an additional USD 5 per seat on average during peak windows.

- Integrates with over 45 global payment gateways including Stripe and PayPal.

- Supports transactions in more than 100 distinct currencies for global reach.

- Automates ticket generation in under 0.5 seconds for instant customer access.

Beyond simple booking mechanics, financial reconciliation capabilities solidify the dominance of this module. The software automatically matches bookings with payments, saving accounting teams approximately 20 hours per week that were previously lost to manual data entry. Key players in the tour operator software market now allow businesses to store up to 5 years of historical booking data, providing deep insights for future planning. These systems enable seamless management of over 500 separate supplier connections, ensuring diverse product offerings are always synchronized. Robust functionality ensures that operators prioritize this module because it directly influences cash flow. By automating confirmation workflows, companies eliminate the need for manual email drafting entirely.

Cloud Scalability And Subscription Flexibility Cement SaaS Model Market Leadership

Software-as-a-Service (SaaS) models dominate because they remove the barrier of expensive on-premise hardware, securing a 57.2% share. Investment in the tour operator software market has aggressively shifted toward cloud-based solutions that allow businesses to launch full-scale operations with a setup time of just 24 hours. Providers like Rezdy and Checkfront offer tiered subscriptions starting as low as USD 29 per month, democratizing access for operators with limited capital. To ensure reliability, these platforms host data across 15 global server regions, guaranteeing low-latency access for users regardless of their physical location. Rapid deployment is a primary driver, with developers pushing bi-weekly updates to ensure users always have the latest features without the headache of manual installation.

- Connects effortlessly with over 300 third-party applications like Salesforce and Mailchimp.

- Includes a 14 day free trial period allowing risk-free software evaluation.

- Performs automatic data backups every 6 hours to prevent information loss.

The dominance of SaaS is further driven by its ability to support remote workforces through robust mobile capabilities. Top-tier SaaS applications in the tour operator software market have surpassed 10,000 mobile downloads, enabling guides to manage manifests directly from the field. Support infrastructure has also evolved significantly, with leading vendors guaranteeing an initial response time of under 15 minutes for critical issues. Scalability features allow mid-sized operators to expand up to 50 user logins instantly during high season without needing hardware upgrades. Companies no longer need to maintain physical servers, reducing energy costs and office footprint. Consequently, this flexibility makes SaaS the undisputed leader in deployment.

High Volume Local Travel Surges Drive Domestic Operator Market Dominance

Domestic tour operators hold a commanding 70% share primarily because they handle the highest frequency of transactions in the global travel ecosystem. The tour operator software market sees immense adoption from this segment as travelers prioritize local experiences, requiring systems that manage up to 12 daily departure slots per activity. These operators utilize software that interfaces in over 30 languages, catering to diverse local staff and regional travelers who prefer native communication. Many domestic firms manage extensive fleets, necessitating tools that track 20 or more vans simultaneously to optimize pick-up routes. The surge in short-haul trips requires systems capable of handling rapid turnover, with some platforms facilitating bookings with a lead time of just 2 hours prior to departure.

- Manages tax compliance across 50 distinct local jurisdictions automatically.

- Facilitates partnerships with over 200 local vendors and attraction providers.

- Supports customized reporting with 15 pre-built templates for operational analysis.

Government initiatives promoting local tourism have further fueled software adoption among domestic entities. Operators use these platforms to manage diverse inventories, tracking over 50 different activity types ranging from walking tours to river cruises. The software allows for precise resource allocation, enabling companies to create up to 10 distinct staff logins for guides and drivers to access personalized schedules. Domestic operators typically build extensive client histories, with systems supporting databases of over 50,000 customer records for loyalty marketing. Efficiency gains from the tour operator software market are vital for these companies. Automating logistical planning allows them to scale operations without expanding their permanent workforce.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Complex Global Operations And Massive Budgets Secure Large Enterprise Market Authority

Large enterprises historically dominate with a 71.8% share because they possess the budget and scale to implement comprehensive, custom-tailored solutions. Major players invest heavily in the tour operator software market, with annual IT budgets often exceeding USD 2 million to maintain bespoke ecosystems. These conglomerates manage massive inventories, tracking over 1 million distinct Stock Keeping Units (SKUs) across flights, hotels, and excursions. Their operations require systems capable of handling industrial-strength processing, with some platforms executing over 10 million API calls daily from global distribution systems. The sheer scale demands robust architecture, supporting over 5,000 employee seats across various departments.

- Consolidates operations for 15 separate sub-brands under one unified dashboard.

- Requires approximately 500 developer hours for initial custom system implementation.

- Connects directly with an ecosystem of over 10,000 global suppliers.

The dominance of large enterprises is also attributed to their need for complex data management and security. Software tailored for this segment manages data warehouses exceeding 100 Terabytes to power predictive analytics and AI modeling. These organizations utilize the tour operator software market to coordinate logistics across 20 different countries, requiring sophisticated cross-border payment reconciliation. Premium service levels are standard, with vendors providing a dedicated account manager available 24/7 to resolve technical bottlenecks. The ability to negotiate exclusive connectivity and maintain high-volume performance distinguishes these giants from smaller competitors.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific Dominance Fueled by Mobile First Adoption and Rapid Tourism Recovery

The global landscape of the tour operator software market has shifted decisively toward the East, with the Asia Pacific region now controlling the dominant market share and projected to expand at a massive CAGR of 13.40% through 2025. This surge is largely powered by a "mobile-first" consumer base that demands instant, on-the-go booking capabilities. In mature markets like Australia, this trend is solidified by Rezdy, which successfully supports 1,055 active operators in its home territory alone.

The region's diverse financial ecosystem also necessitates broad technical support; vendors here are competing by offering connections to over 30 different payment gateways to accommodate local digital wallets. Furthermore, FareHarbor has entrenched itself by establishing dedicated banking support for the APAC region, ensuring seamless payouts for thousands of operators. The demand here is not just for software, but for infrastructure that can handle high-volume, low-latency mobile transactions native to the Asian traveler.

North America Prioritizes High Value Transactions and Event Based Tourism Revenue

North America retains its stronghold in the tour operator software marketthrough high-yield sophistication and robust infrastructure. The United States remains a powerhouse for premium software adoption, evidenced by Peek Pro’s commanding user base of 3,583 active customers. The market here is driven by the sheer economic scale of the "Experience Economy," where travelers now spend an average of USD 1,300 per concert or major event. Operators are aggressively upgrading their tech stacks to capture revenue from upcoming mega-events like the 2025 Super Bowl, expected to generate USD 480 million, and the 2026 World Cup, which carries a USD 2 billion economic forecast. To manage these stakes, American enterprise clients demand perfection, pushing vendors like Checkfront to guarantee 99.99% uptime reliability.

Europe Demands Multi Lingual Complexity and Cross Border Payment Flexibility

Europe remains a highly complex, fragmented tour operator software market where software demand is dictated by the need for cross-border operability. Regiondo effectively leads this segment by supporting 11 distinct languages, a non-negotiable feature for operators running tours across the continent's fluid borders. Financial flexibility is equally critical here; TrekkSoft maintains its competitive edge by allowing operators to accept payments in 33 distinct currencies, solving the headache of multi-currency management. The market is also being shaped by distribution giants; GetYourGuide’s decision to limit its 2025 program to just 3 "Premium" connectivity partners forces European operators to choose software that guarantees this elite level of connectivity. This region prioritizes software that can seamlessly navigate the regulatory and linguistic maze of the EU.

Top 10 Recent Developments in Tour Operator Software Market

- WeTravel Launches All-in-One Platform (March 24, 2025): WeTravel unveiled a complete platform overhaul, integrating AI-powered interactive itineraries and a "Virtual Credit Card" system for US operators to pay suppliers instantly, marking a major shift from simple payment processing to full operational management.

- Expedition Software Holding Appoints New CEO (June 10, 2025): Following the merger of Rezdy, Checkfront, and Regiondo, the combined entity (Expedition Software Holding) named Lawrence Hester, co-founder of FareHarbor, as CEO, signaling a unified aggressive growth strategy across North America, Europe, and APAC.

- Tripadvisor Merges Viator Operations (November 5, 2025): Tripadvisor announced a strategic restructuring to merge its core brand operations with Viator. This move consolidates engineering and product teams to streamline the "look-to-book" flow for experience seekers, though it resulted in significant operational layoffs.

- FareHarbor Launches "Skipper" AI (October 9, 2025): FareHarbor introduced "Skipper," a dashboard-embedded AI assistant designed to automate item creation and generate real-time reporting, alongside new integrations with Square and QuickBooks Online.

- TUI Musement Integrates with TravelExchange (September 1, 2025): TUI Musement completed a massive API integration placing 750 multi-day tour itineraries onto the TravelExchange platform, allowing 2,600+ agencies to book complex TUI products instantly for the first time in the tour operator software market.

- FareHarbor Monetizes Website Plans (January 1, 2025): In a controversial market shift, FareHarbor transitioned all legacy "free" website plans to paid tiers (up to USD 5,000/year), forcing thousands of operators to re-evaluate their digital infrastructure costs.

- TUI Musement Partners with Travel Counsellors (February 13, 2025): A new global partnership gave 2,100 independent Travel Counsellors immediate access to TUI’s curated portfolio of excursions, reinforcing the trend of B2B API connectivity over direct-to-consumer distinct silos.

- Bókun Restructures Pricing Models (September 19, 2024): Bókun abandoned its single-tier model for "Start," "Plus," and "Premium" subscriptions. This shift allows scaling operators to access advanced "Agent Areas" and lower booking fees (dropping to 1%) as they grow.

- Bókun Releases Departure Management (July 23, 2024): Addressing disruption chaos, Bókun launched a "Departure Management" tool allowing operators to bulk-cancel or reschedule bookings during weather events and automate customer communication via a centralized portal.

- Peek Pro Copilot Dominates Dynamic Pricing (2024-2025): Throughout 2025, adoption of Peek Pro’s "Copilot" surged. The AI tool, which won the 2024 Arival Innovation Award, is now credited with increasing operator revenue by 20% through automated demand-based pricing adjustments.

Key Players in the Global Tour Operator Software Market

- Adventure Bucket List

- Centaur Systems

- Checkfront Inc

- Dolphin Dynamics

- eMinds

- GP Solutions GmbH

- IT Web Services,

- Qtech Software

- Retreat Guru

- Rezdy

- Tourplan

- TechnoHeaven Consultancy

- Travefy, Inc

- TraveloPro

- Trawex Technologies Pvt Ltd

- TrekkSoft (TrekkSoft Group)

- TRYTN, Inc

- Xola, Inc.

- Other Prominent Players

Market Segmentation Overview:

By Offering

- Software

- Services

By Module

- Booking/Reservation Management

- Inventory Management

- Payment Processing

- CRM (Customer Relationship Management)

- Back-office Management

- Accounting Management

By Deployment Mode

- SaaS

- Web Based

By Enterprise Size

- SMEs

- Large Enterprises

By End User

- International Tour Operators

- Domestic Tour Operators

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South Africa

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |