Market Snapshot

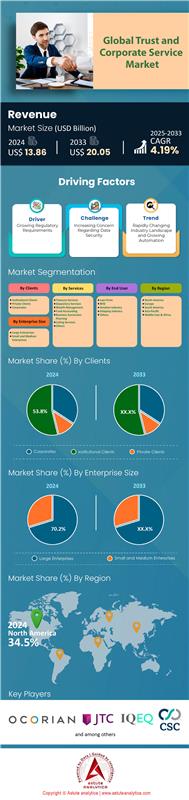

Trust and corporate service market was valued at US$ 13.86 billion in 2024 and is projected to surpass market valuation of US$ 20.05 billion by 2033 at a CAGR of 4.19% during the forecast period 2025–2033.

Key Findings

- Based on client, corporate segment took a significant lead, capturing a notable 53.8% of the total market share.

- Based on services, treasury services have emerged as the most sought-after, holding a commanding 24.2% of the entire market's revenue.

- When assessing by end-users, the BFSI (Banking, Financial Services, and Insurance) sector is prominently positioned, holding a robust 35.5% market share.

- Based on enterprises size, a remarkable 70.2% of the market's revenue comes directly from large enterprises.

- North America is set to capture over 34.50% market share in the coming years.

- Trust and corporate service market is projected to surpass market valuation of US$ 20.05 billion by 2033.

Demand within the trust and corporate service market is intensifying, driven by non-negotiable regulatory requirements and rapid institutional product innovation. Stakeholders are reacting to a complex web of new rules, such as the EU's MiCA framework, which mandates the adoption of 18 distinct technical standards by 2025. The sheer volume of product launches further fuels this need; the SEC was actively reviewing nearly 92 different crypto-ETF applications in 2025, a significant jump from the previous year. These regulated products are attracting enormous capital flows, with U.S. Bitcoin ETFs alone seeing US$ 29.4 billion in inflows by August 2025, all requiring meticulous, third-party administration.

The nature of underlying assets is also expanding, creating new service verticals for the trust and corporate service market. The tokenization of real-world assets is a prime example, with over 200 active institutional RWA projects underway as of June 2024. BlackRock's tokenized fund, BUIDL, accumulated nearly US$ 2 billion shortly after its 2024 launch, illustrating the scale of assets needing specialized management. Concurrently, the institutional pursuit of yield through staking has created another demand vector. An astonishing 826,876 ETH was queued for staking as of September 2025, reflecting a massive operational need for managing these assets compliantly.

The operational workload includes managing over 6,000 active loans on private credit RWA protocols and servicing the total value locked in institutional RWA projects, which hit US$ 65 billion in 2025. Furthermore, service providers like Figment expanded institutional staking support to 8 new protocols in 2024 to meet client needs. The convergence of regulatory pressure, product volume, and asset complexity solidifies the robust and growing demand shaping the Trust and corporate service market.

To Get more Insights, Request A Free Sample

Top 2 New Revenue Streams Through Institutional DeFi and DAO Services

- Institutional DeFi Integration: The migration of institutional capital into decentralized finance (DeFi) is creating a significant service opportunity. As institutions engage with permissioned DeFi pools, which controlled US$ 6.4 billion in volume by mid-2025, they require specialized administrative support. Service providers are needed to manage complex smart contract interactions, provide compliant reporting for on-chain lending activities, and conduct risk assessments for novel protocols. With institutional capital in DeFi reaching US$ 41 billion in total exposure by mid-2025, the demand for corporate services that can bridge traditional compliance with on-chain operations is immense and largely unmet.

- Corporate Services for Decentralized Autonomous Organizations (DAOs): DAOs in the trust and corporate service market have evolved from niche experiments into significant economic entities, creating a new client category. As of 2025, over 13,000 DAOs have been established, collectively managing treasuries with US$ 24.5 billion in assets. These digital-native organizations require traditional corporate services—such as treasury management, payroll, financial reporting, and legal structuring—tailored for a decentralized governance model. Providing these essential functions to the more than 6,000 regularly active DAOs represents a blue-ocean opportunity for service firms willing to adapt their offerings for this innovative organizational structure.

Key Demand Drivers

Specialized Digital Asset Insurance Mandates Sophisticated Administrative Oversight

The institutionalization of digital assets has ignited a critical demand for specialized insurance products, creating a new and complex verification role for the Trust and corporate service market. As institutional investors enter the space, they mandate robust risk mitigation that goes far beyond basic custody. By 2025, providers like Evertas began offering policies with capacities up to US$ 360 million to protect against theft by insiders and external actors. Service providers are now required to administer and verify these intricate policies, which cover specific risks such as staking penalties, technology errors, and even the physical theft of cold-storage media.

This demand is quantifiable and growing rapidly. In 2024, total losses from crypto hacks amounted to US$ 2.2 billion, compelling institutions to seek comprehensive coverage. Consequently, providers are expanding their offerings; as of 2025, US$ 1.8 billion paid out in claims between 2022 and 2024 is properly reconciled.

Cross-Chain Complexity Creates Urgent Need for Advanced Administrative Solutions

The proliferation of assets across numerous blockchain networks has created a severe operational bottleneck, driving an urgent need for advanced administrative solutions within the Trust and corporate service market. Institutions no longer operate on a single chain; their assets are fragmented across a multi-chain ecosystem connected by an expanding web of bridges. Cross-chain bridges facilitated over US$ 1.3 trillion in annual asset movement by 2025, a testament to their critical role in the market. The total value locked in these bridges reached US$ 19.5 billion in January 2025, representing a vast pool of assets requiring sophisticated tracking and reconciliation services.

The sheer volume of cross-chain activity highlights the scale of the administrative challenge. In July 2025, the highest monthly cross-chain transaction volume on the blockchain reached US$ 56.1 billion, a record high. Protocols like Axelar recorded a surge in interchain transactions over the past year, while Wormhole processed over US$ 52 billion through its token bridge since its launch. This activity in the trust and corporate service market is not just retail-driven, enterprise adoption is a primary catalyst, with institutions requiring interoperability to connect private and public blockchains for transparency and verification. Corporate service providers must now offer multi-chain treasury management, reconcile transactions across disparate ledgers, and provide consolidated reporting, a complex task given that over US$ 7 billion worth of illicit crypto has been laundered using cross-chain methods as of 2024.

Segmental Analysis

Corporate Clients Powering the Trust and Corporate Service Market

The corporate segment's commanding 53.8% share of the trust and corporate service market stems from the increasing complexities of global business operations. As corporations expand across borders, they encounter a maze of international regulations, making specialized services essential for ensuring compliance and streamlining financial activities. The use of Special Purpose Vehicles (SPVs) for financial risk isolation and asset management is a significant driver, with the global SPV market holding substantial assets. For instance, in Luxembourg alone, a large portion of the $1.3 trillion in assets under management is composed of SPVs utilized by corporations. Multinational corporations, in particular, depend on these services to consolidate their cross-border operations and maintain seamless financial management. The constant need for tax optimization and efficient corporate structuring further solidifies the corporate segment's leading position in the market.

The intricacies of modern business have led to a surge in demand for expert guidance. To illustrate, banks are spending upwards of $270 billion annually on compliance, a figure that has seen a significant rise over the past decade. The penalties for non-compliance are steep, with fines exceeding $321 billion since the 2008 financial crisis. This has propelled the growth of the RegTech market, which is anticipated to reach $55.28 billion by 2025, as companies increasingly adopt technology to navigate the complex regulatory environment in the trust and corporate service market.

- Over 60% of multinational companies are now outsourcing their corporate governance and compliance functions.

- Investment in compliance-related tools and training saw a 20% increase between 2020 and 2023.

- The global business management consulting services market, a related industry, was valued at $161.2 billion in 2024.

Treasury Services The Strategic Core of Corporate Finance

Treasury services have solidified their position as the most sought-after offering in the trust and corporate service market, capturing 24.2% of the total revenue. This dominance is attributed to the critical role treasury plays in the financial health and strategic direction of a company. As the internal bank of an organization, treasury is responsible for managing cash flow, investments, financing, and financial risks, ensuring operational liquidity and long-term stability. The evolution of the treasury function from a purely operational role to a strategic partner advising senior management on crucial decisions like capital allocation and mergers and acquisitions has further elevated its importance. The need for sophisticated risk management strategies is underscored by the fact that over 90% of large corporations use derivatives for hedging against financial risks.

The financial numbers associated with treasury operations highlight their significance. For example, Apple's treasury managed a colossal $268 billion in cash and investments as of 2022. Following the 2008 financial crisis, General Electric in the trust and corporate service market undertook a major overhaul of its treasury operations, which included a reduction of over $100 billion in commercial paper borrowing to enhance transparency and mitigate risk. Coca-Cola's treasury actively manages more than $20 billion in annual foreign exchange exposure through a centralized hedging program to protect its global cash flows.

- More than 82% of all new treasury implementations are now SaaS-based solutions, reflecting a shift towards cloud technology.

- Within the next two years, 16% of companies are planning to implement a new Treasury Management System (TMS).

- By 2025, over 15% of finance professionals intend to adopt new platforms for bank fee analysis and reconciliations.

BFSI Sector A Pillar of Demand in Trust and Corporate Services

The Banking, Financial Services, and Insurance (BFSI) sector stands as a formidable end-user in the trust and corporate service market, commanding a robust 35.5% market share. The sector's prominence is a direct result of its inherent complexities, stringent regulatory environment, and the sheer volume of assets it manages. Trust assets under management in the global banking sector alone are in excess of a staggering $100 trillion. Furthermore, with insurance assets under management projected to reach $19.7 trillion by 2025, the demand for specialized trust and corporate services is set to intensify. The BFSI sector's continuous engagement in cross-border operations and frequent merger and acquisition activities further necessitates the expertise of trust and corporate service providers to navigate the multifaceted financial landscape.

The financial commitment of the BFSI sector to compliance and technology underscores its reliance on external expertise. The industry's annual spending on compliance across the trust and corporate service market has surpassed $270 billion. To manage the ever-evolving regulatory landscape, the BFSI sector is a major consumer of RegTech solutions, a market expected to grow to $55.28 billion by 2025. Cybersecurity is another critical area of investment, with BFSI firms allocating a significant portion of their IT budgets to it, and the cost of cybercrime for these firms is estimated at $18.5 million per firm annually.

- Global spending on AI in financial services is anticipated to exceed $15 billion by 2025.

- The global risk management market in the BFSI sector is predicted to reach $18.5 billion by 2025.

- Digital transformation investment in the BFSI sector is expected to exceed $300 billion by 2025.

The intricate nature of financial instruments, coupled with the constant pressure to mitigate risk and ensure compliance, makes trust and corporate services indispensable for BFSI institutions. Major players in the financial world like JPMorgan Chase & Co., Goldman Sachs, Allianz, and BlackRock are significant consumers of these services. The ongoing digital transformation and the increasing adoption of cloud-based risk management solutions by over 75% of large banks are further driving the demand for specialized support in the trust and corporate service market.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Large Enterprises The Revenue Engine of the Trust and Corporate Service Market

A remarkable 70.2% of the revenue in the trust and corporate service market is generated by large enterprises, underscoring their pivotal role in this sector. This significant contribution is a direct consequence of the vast and complex operational footprints of these corporations. Large enterprises typically operate across multiple jurisdictions, each with its own unique and intricate financial regulations. This multi-jurisdictional presence necessitates specialized trust and corporate services to ensure seamless compliance, manage complex corporate structures, and facilitate efficient asset management. Their substantial financial resources also mean they are more likely to seek out and invest in premium, comprehensive service packages, further boosting their revenue contribution.

The scale of large enterprise operations demands robust and specialized support. For example, a multinational corporation like Walmart requires multi-jurisdictional compliance and payroll services, driving the need for expert corporate service providers. The increasing trend of globalization means that large enterprises are constantly navigating new regulatory environments, a key factor driving their demand for these services. Companies such as PwC and EY are actively developing AI-based solutions in the trust and corporate service market to help these large entities manage compliance processes more efficiently, with EY investing in platforms to enhance operational efficiency for US-based multinationals.

- Global spending on cloud services is projected to hit $1.3 trillion in 2025, largely driven by large enterprise adoption.

- Enterprise spending on Google's digital acquisition channels saw a 30% month-over-month spike in August 2025.

- Spending by large enterprises on the AI tool Anthropic increased by 55% month-over-month in August 2025.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America's Regulatory Clarity and Product Innovation Cement Market Dominance

North America leads the global Trust and corporate service market with a commanding 34.50% market share, a position fortified by a mature regulatory environment and relentless product innovation. The United States, in particular, drives growth through the creation of regulated investment products. In early 2025, U.S. asset managers had filed more than 30 new applications for various crypto-asset ETFs following initial approvals. The U.S. tokenized Treasury market has also become a significant area, with 9 distinct products available to institutional investors by 2024. Regulatory activity remains high; the SEC initiated 46 separate enforcement actions against crypto entities in 2024, compelling firms to seek expert compliance services.

The trust and corporate service market's infrastructure is robust and expanding. In 2024, crypto industry advocacy groups spent a record US$ 24 million on lobbying efforts in Washington D.C. to shape future legislation. At the state level, a total of 8 new special purpose trust charters were granted to digital asset custodians in Wyoming and South Dakota in 2024. Canada also contributes significantly, with the Ontario Securities Commission registering 12 crypto asset trading platforms by early 2025. The U.S. Patent and Trademark Office granted over 5,000 blockchain-related patents in 2024. Furthermore, by 2025, 4 federally chartered crypto banks were operational in the U.S. This combination of regulated products, legal clarity, and infrastructure solidifies the region's leadership.

Europe's MiCA Framework Creates a Unified and Demanding Service Environment

Europe’s market is rapidly maturing under the comprehensive Markets in Crypto-Assets (MiCA) regulation, creating a standardized but highly demanding landscape for service providers. By the start of 2025, national regulators across the EU had received over 250 formal applications from Crypto-Asset Service Providers (CASPs) seeking MiCA authorization. Germany’s BaFin processed 25 of these applications alone. The region's exchanges are hubs for innovation; Deutsche Börse's Xetra listed 35 new crypto ETPs during 2024.

Switzerland maintains its role as a key crypto hub, with its regulator, FINMA, issuing 12 new fintech and blockchain-related licenses in 2024. The European Central Bank is also advancing its work, involving 40 financial institutions in its digital euro scheme trials in 2025. In Luxembourg, a key fund domicile, the number of registered investment funds with a dedicated digital asset strategy surpassed 60 by early 2025. The focus on a unified regulatory framework is creating substantial opportunities for a specialized Trust and corporate service market.

Asia Pacific's Licensing Regimes Fuel a Highly Competitive Corporate Services Market

The Asia Pacific region is characterized by a dynamic and competitive environment shaped by proactive national licensing regimes. Hong Kong has emerged as a key center for regulated activity; its Securities and Futures Commission (SFC) received more than 24 applications for Virtual Asset Service Provider (VASP) licenses by its 2024 deadline. The city also successfully launched 6 spot crypto ETFs in 2024. Singapore continues to be a central hub, with the Monetary Authority of Singapore (MAS) granting 14 new Major Payment Institution licenses with digital asset permissions in 2024.

Elsewhere, Japan’s Financial Services Agency (FSA) approved 5 new crypto-asset exchanges for operation in 2024. South Korea’s Financial Intelligence Unit (FIU) conducted on-site inspections of 16 regulated digital asset exchanges in 2024 to enforce new AML rules. In Australia, 25 organizations participated in the next phase of the RBA’s CBDC research pilot in early 2025. This focus on country-level licensing and regulation is fostering a robust and rapidly growing Trust and corporate service market across the region.

Strategic Consolidation and Capital Inflows Defining the Trust and Corporate Service Market’sCompetitiveness

- BitGo Acquires Brassica: In a strategic move to expand its digital asset services to the private securities market, custodian BitGo acquired Brassica, an alternative asset platform, in May 2024.

- Fordefi Raises US$ 10 Million: The institutional MPC wallet provider secured US$ 10 million in a seed extension round in February 2024 to expand its team and develop new security features for decentralized finance. ([Reference])

- Farcana Secures US$ 10 Million Funding: The Web3 gaming ecosystem raised US$ 10 million in seed funding in January 2024 from major investors to build out its platform, highlighting investment in the broader digital asset space.

Key Players in Global Trust and Corporate Service Market

- Corporation Service Co.

- Intertrust Group B V

- IQ-EQ Group Holdings S.a r.l

- JTC Plc

- Ocorian Ltd.

- The Citco Group Ltd.

- TMF Group B.V.

- Tricor Services Ltd.

- Vistra Group Holdings S.A.

- Wolters Kluwer NV

- Other Prominent Players

Market Segmentation Overview:

By Clients

- Institutional Clients

- Private Clients

- Corporates

By Services

- Treasury Services

- Depository Services

- Wealth Management

- Fund Accounting

- Business Succession Planning

- Listing Services

- Others

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

By End User

- Law Firms

- BFSI

- Aviation Industry

- Shipping Industry

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |